DXC - DXC Technology: Cheap Due To FCF Growth And SG&A Reduction

2023-09-18 12:19:07 ET

Summary

- DXC Technology is a leading global corporation in the IT services market, offering solutions to Fortune 500 companies.

- The company focuses on delivering measurable results and reducing business risks for clients, with a strong emphasis on the employee experience.

- DXC's restructuring efforts, potential M&A transactions, and international exposure may lead to further growth in free cash flow.

DXC Technology Company ( DXC ) appears to be making significant reductions in SG&A, and offers both international exposure and large clients. In my view, if the restructuring efforts do not fail, and further M&A transactions are successful, we may see further FCF growth in the coming years. There are obvious risks from cyber attacks or failed M&A efforts, however given the recent guidance, in my view, DXC appears undervalued.

DXC Technology

DXC is a leading global corporation in the IT services market, providing solutions to Fortune 500 companies around the world. Its portfolio of global business services includes analytics and engineering, applications, and business process services. On the other hand, its portfolio of global infrastructure services includes cloud and security, IT outsourcing, and modern workplace implementation.

DXC focuses on delivering predictable and measurable results while reducing business risks and operating costs for its clients. Its focus on the employee experience provides a consumer-like digital experience that fits the needs of today's professionals.

The company offers innovative technology services in two segments: Global Business Services or GBS and Global Infrastructure Services or GIS. GBS provides analysis and engineering solutions, applications, and business process services to help clients address business challenges and accelerate the transformation of their operations.

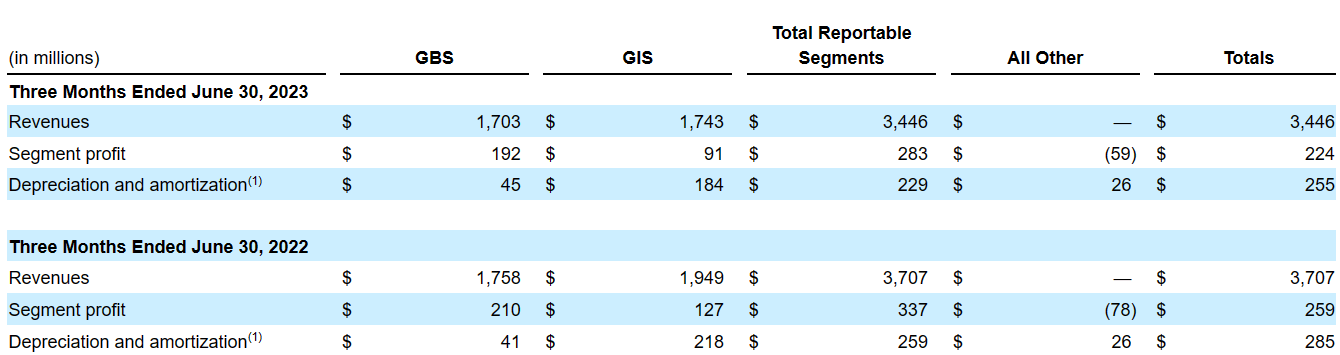

For its part, GIS provides cloud and security services, IT outsourcing, and implementation of modern workplaces to reduce operational costs and business risks. The business model focuses on delivering predictable and measurable results to clients while adapting to the specific needs of each industry and client. As shown in the table below, both GIS and GPS report approximately the same amount of net sales, but the profit reported by GBS is more significant.

{kind=link}

It is also worth considering that DXC operates in the United States, the United Kingdom, Europe, and Australia. In my opinion, geographic diversification may make future net sales and FCF volatility a bit lower. Besides, I believe that the company may deal better than other competitors with a global recession or anything similar.

Source: 10-Q

With that about the business model, I think that DXC is an appealing play mainly after the recent guidance given for the year 2024. The company expects lower net sales growth, however non-gaap diluted EPS close to $3.15-$3.4 and 2024 FCF close to $800 million are great reasons to have a look at the stock.

Source: Presentation To Investors

Balance Sheet

As of June 30, 2023, DXC reported cash and cash equivalents worth $1576 million, receivables and contract assets close to $3.285 billion, and prepaid expenses of about $652 million. Total current assets were equal to $5744 million, and the current ratio stands at more than 1x, so I am not concerned about any liquidity issue here.

Besides, with intangible assets of $2.441 billion, goodwill of $539 million, and property and equipment worth $1922 million, total assets stand at $15.293 billion. The asset/liability ratio is also larger than 1x. Hence, I think that the balance sheet stands in a healthy position.

Source: 10-Q

The total amount of liabilities decreased a bit as compared to that in the previous quarter. The list of liabilities included short-term debt and current maturities of long-term debt of about $694 million, with accounts payable close to $701 million, which is -10.3% lower than that in March. Accrued payroll and related costs stood at $613 million, with current operating lease liabilities worth $303 million, -4% less than that in the last quarter.

The company also reported accrued expenses and other current liabilities worth $1587 million, -13% less than that in the previous quarter. Besides, with deferred revenue and advance contract payments of about $1008 million, total current liabilities were equal to $5057 million.

Moreover, with long-term debt of $3891 million, the company also noted non-current income tax liabilities and deferred tax liabilities of about $579 million, -1% less than that in the previous quarter. Finally, total liabilities were equal to $11.690 billion, representing a decline of 2% as compared to the figure reported in March 2023.

Source: 10-Q

We Could Expect New Acquisitions To Enhance Net Sales Growth And FCF Growth

DXC focuses on a transformation journey to build strong customer and employee relationships, unlock value in the enterprise technology stack, and optimize costs. More in particular, I think that the company is focused on stabilizing revenue. It has made acquisitions such as Luxoft Holding to complement its offerings and provide opportunities for future growth. DXC seeks to run a long-term sustainable business and strengthen its financial footing by seeking strategic alternatives and rationalizing its portfolio. Under my DCF model, I assumed that these initiatives would bring net sales growth and FCF generation.

The Stock Repurchase Plan Will Most Likely Accelerate The Demand For The Stock, And May Enhance The Stock Price

Considering the total amount of shares outstanding acquired and the expectations for 2024 Q1, I believe that it is worth having a look at the stock repurchase program. The company seems to have repurchased close to 20% of the share count. In my view, sooner or later, further stock repurchases will most likely push the price up.

Source: Presentation To Investors

Divestitures May Bring Cash In Hand, Which May Make The Balance Sheet More Appealing

DXC reported some business divestitures, and noted that it has certain other business units as held for sale. It has also sold businesses like HPS and HHS, and is in the process of selling FDB. In my view, if DXC successfully finds buyers, cash in hand may increase, which could make the balance sheet even more appealing. Additionally, I believe that more investors would have a look at DXC. The demand for the stock may accelerate.

During the first quarters of fiscal 2024 and fiscal 2023, the Company sold insignificant businesses that resulted in a loss of $5 million and a gain of $38 million, respectively. During the first quarter of fiscal 2023, the Company also classified certain insignificant businesses as held for sale and recognized a loss of $9 million. Source: 10-Q

I Assumed That Restructuring Efforts Would Not Fail

During fiscal year 2024, DXC approved global cost savings initiatives designed to better align the DXC’s facilities and data centers. I think that investors will not waste their time by looking at the amount of money invested in these initiatives. Under my cash flow model, I assumed that these transformations would enhance future FCF growth.

{kind=link}

In the last quarterly report, DXC Technology also commented about $20 million in Q1 2024 to align the facilities and data center. I believe that investors may want to have a look at the following lines.

During fiscal 2024, management approved global cost savings initiatives designed to better align our facilities and data centers. Total restructuring costs recorded, net of reversals, was $20 million for the first quarter of fiscal 2024, a decrease of $13 million compared to a year ago. Source: 10-Q

Further Reduction In Expenses Related To Professional Services And Vendor-related Expenses Could Lead To FCF Growth

I also assumed, in my DCF model, that further reduction in SG&A expenses would most likely accelerate FCF growth. In the last quarterly report, management noted lower SG&A expenses driven by reduction in vendor-related expenses. In the last two years, the total decrease in SG&A was quite impressive.

Selling, general and administrative expense, excluding depreciation and amortization and restructuring costs, was $327 million for the first quarter of fiscal 2024, a decrease of $22 million compared to a year ago. The $22 million decrease in SG&A expenses was primarily driven by reductions in professional services and vendor-related expenses. Source: 10-Q

Source: Ycharts

Cash Flow Expectations

My expectations included 2034 net sales close to $15.066 billion, with 2034 net sales growth of less than 1%, and net income of about $1.494 billion, with net income/sales ratio of 9%. Note that I included declines in net sales growth, but increases in the profit margin. In my view, my numbers are conservative, and are in line with previous figures reported by DXC.

{kind=link}

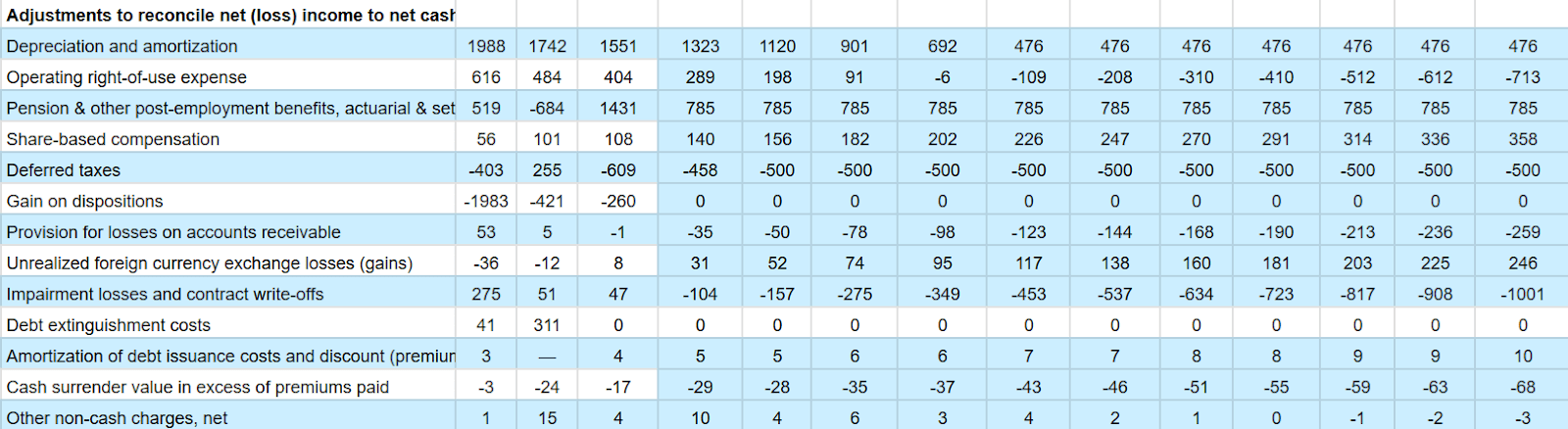

My cash flow model also included forecasts about adjustments to reconcile net income to net cash provided by operating activities. I used 2034 depreciation and amortization of $476 million, operating right-of-use expenses worth -$714 million, and pension and other post-employment benefits, actuarial and settlement losses of about $785 million.

Besides, I assumed share-based compensation of $358 million, which is in line with previous compensation reported by management, deferred taxes worth -$500 million, but no gain on dispositions. Additionally, with changes in accounts receivable close to -$259 million and unrealized foreign currency exchange losses close to $246 million, I also included amortization of debt issuance costs and discount of about $9 million.

{kind=link}

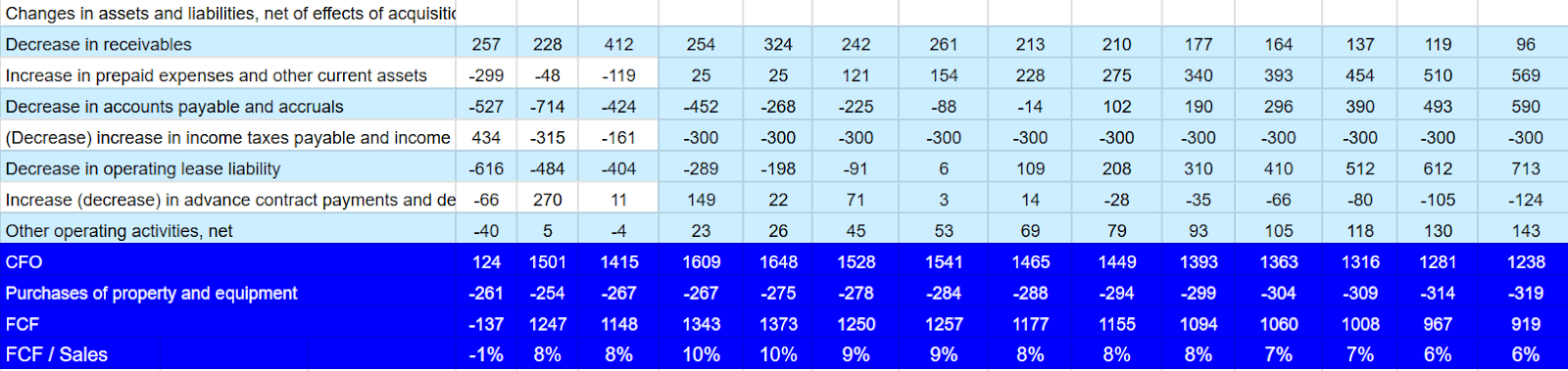

The changes in assets and liabilities included in future cash flow models include changes in receivables of about $95 million, with changes in accounts payable and accruals of close to $589 million, changes in advance contract payments and deferred revenue of about -$124 million, and 2034 CFO of $1.237 billion. Finally, with a capex of -$319 million, 2034 FCF would be about $918 million.

{kind=link}

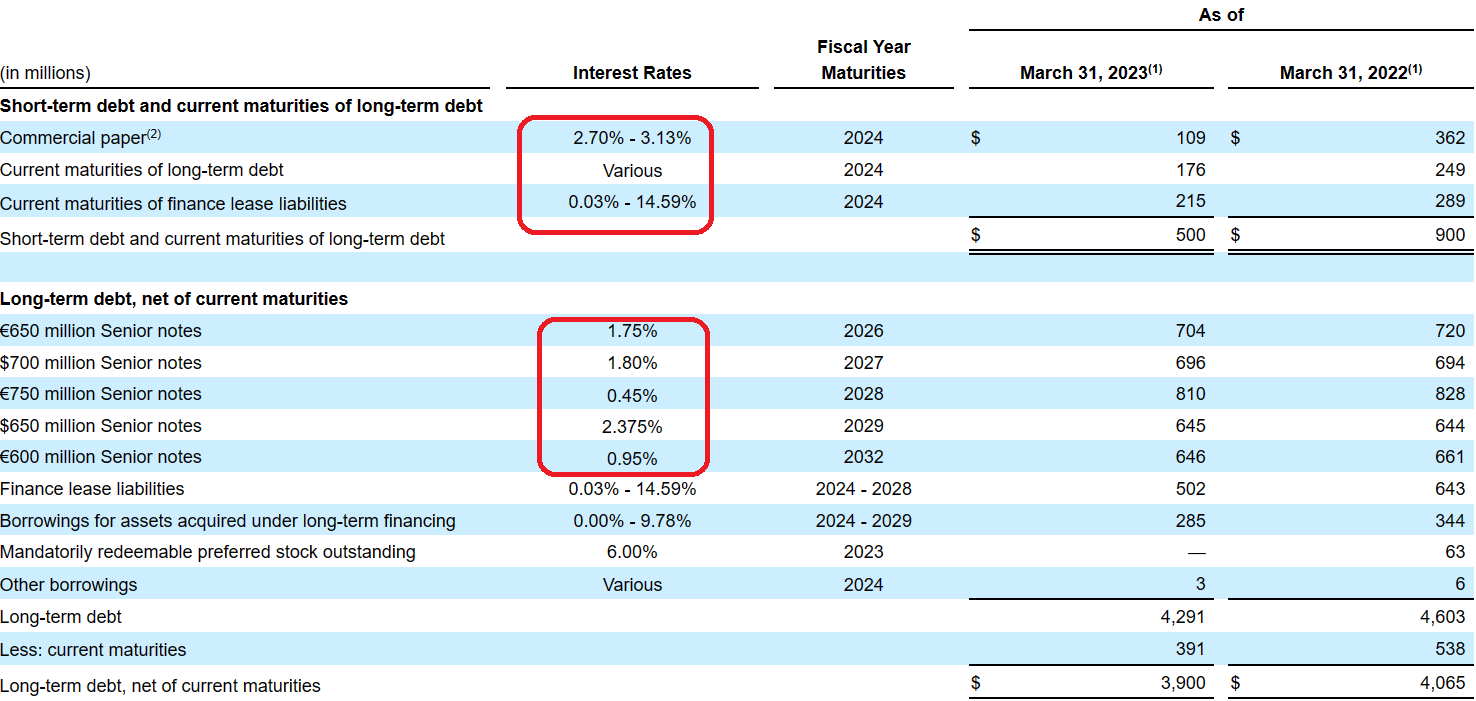

For the calculation of the WACC, I studied a bit the interest rates being paid by DXC, which seem to be close to 2% and 9%. I really cannot mention the interest rates that the company may have to pay in the future, so my financial model includes a conservative rate from 7% to 12%.

{kind=link}

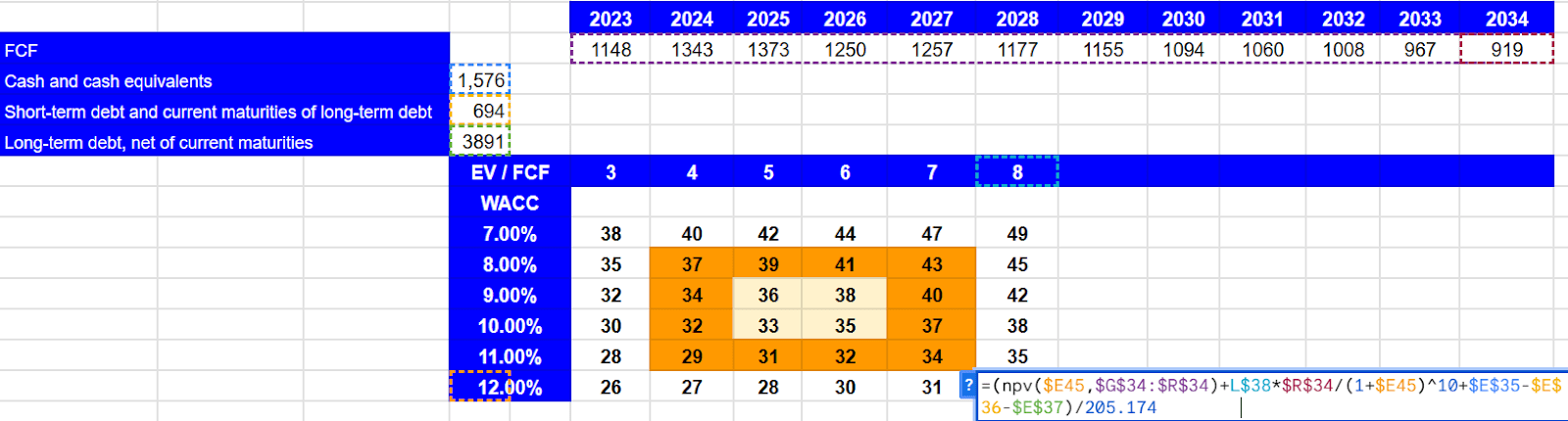

I also assumed cash and cash equivalents of about $1576 million, and subtracted short-term debt and current maturities of long-term debt of about $694 million and long-term debt close to $3.891 billion. Also, with changes in the WACC ranging from 7% to 12% and EV/FCF of 3x-8x, the implied forecasted price would be between $26 and $49 per share. Considering the current stock price, I believe that the undervaluation is significant.

{kind=link}

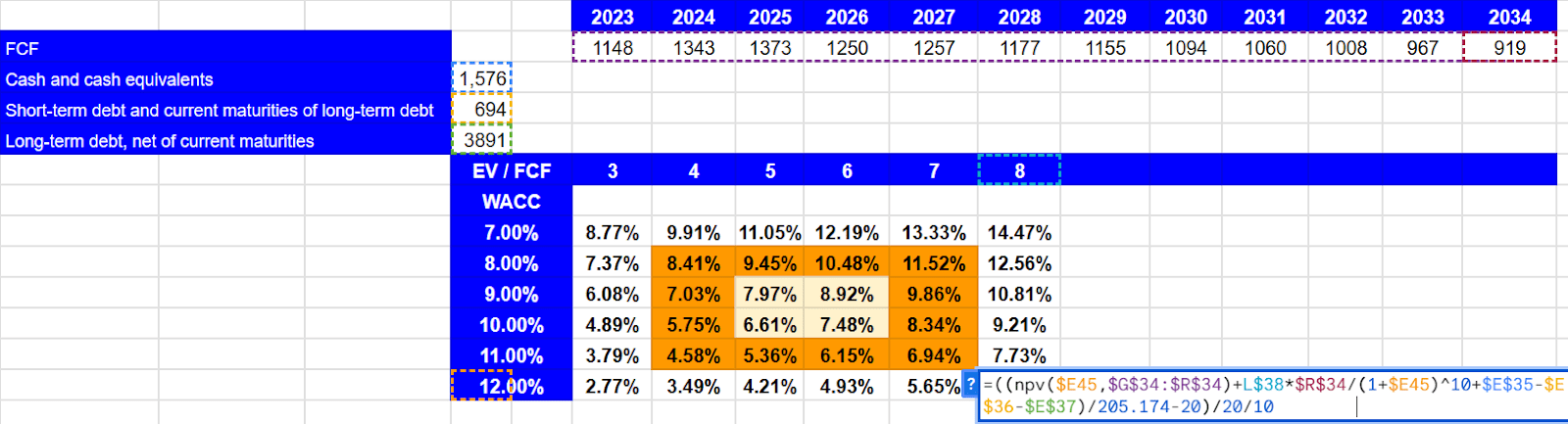

I also obtained results of the internal rate of return with the given WACC of 7%-12% and EV/FCF of 3x-8x. The IRR would be close to 2%-14%, but I think that the most likely IRR would be around 6%-8%.

{kind=link}

Risks and Competition

The business faces various risks, such as vulnerability to security breaches and cyberattacks, the inability to accurately estimate the cost of services, and the schedule for the termination of contracts among others. The company may also be affected by natural disasters, inflation, non-compliance with laws and regulations, and pending litigation. In addition, restructuring, supply chain disruption, negative publicity, and other factors can adversely affect the business and its financial results.

The IT and professional services market is highly competitive, and is not dominated by any one company. There are numerous competitors, including large multinational companies, offshore service providers, smaller companies, and internal functions of corporations. The primary methods of competition are strategic vision, integrated solution capabilities, performance and reliability, global and diverse talent, customer responsiveness, competitive pricing, industry and technical expertise, reputation, and financial stability. The ability to win and retain business depends on technology and the independent perspective of the best solutions, successful relationship management with strategic partners, financial stability, and strong corporate governance.

Opinion

DXC's focus on the employee experience and delivering predictable and measurable results to clients has allowed it to maintain a strong position in a highly competitive marketplace. I believe that DXC has demonstrated its ability to adapt to changes in the market and strengthen its financial footing by rationalizing its portfolio. In my opinion, new acquisitions and divestitures will most likely reshape the balance sheet, and may retain the attention of investors. Besides, the impressive stock repurchase program recently enacted will most likely have a beneficial effect on the stock price sooner or later. There are several risks from cyber attack, reputational damages, and failed M&A, however I believe that the company remains quite undervalued.

For further details see:

DXC Technology: Cheap Due To FCF Growth And SG&A Reduction