DXC - DXC Technology Sees Lumpy Bookings As Clients Reduce Discretionary Spending

2023-12-01 16:15:08 ET

Summary

- DXC Technology Company reported its FQ2 2024 financial results, matching revenue and beating earnings estimates.

- The company provides business and technology software engineering and outsourcing services.

- Despite strong share buybacks, the company's growth is slowing and it faces challenges in the U.S. soft demand environment.

- I remain Neutral [Hold] on DXC Technology Company.

A Quick Take On DXC Technology

DXC Technology Company ( DXC ) reported its FQ2 2024 financial results on November 1, 2023, matching revenue and beating consensus earnings estimates.

The firm provides a range of business and technology software engineering and outsourcing services to organizations.

I previously wrote about DXC with a Hold outlook on slowing growth amid a change in focus for its operating model.

Given the U.S. soft demand environment as clients reign in non-discretionary project spending and continued GIS segment drag on revenue, I remain Neutral [Hold] on DXC Technology Company shares for the near term despite strong share buybacks.

DXC Technology Overview And Market

Virginia-based DXC Technology was founded in 1959 and operates in two business segments:

-

Global Business Services - software engineering, analytics

-

Global Infrastructure Services - transforms legacy systems to the cloud.

The firm is led by Chairman and CEO Mike Salvino, who joined DXC in 2019 and was previously Managing Director at Carrick Capital Partners and Group Chief Executive at Accenture Operations.

DXC also provides business process outsourcing for selected industry verticals such as insurance.

Per a 2023 market research report by Grand View Research, the global market for software consulting (as a subset of the firm’s broader array of services) was estimated at $273 billion in 2022 and is forecast to reach $681 billion by 2030.

This represents a forecast CAGR of 12.1% from 2023 to 2030.

The main drivers for this expected growth are the continued transformation of business activity to the cloud, the growing use of digital touchpoints across all aspects of the enterprise and the need to outcompete on the basis of technology, wherever possible.

Also, the chart below shows the historical and projected future growth trajectory of the U.S. software consulting market from 2020 through 2030:

Grand View Research

Major competitive or other industry participants include:

-

Accenture

-

Atos

-

Capgemini

-

CGI Group

-

Clearfind

-

Cognizant

-

Deloitte Touche Tohmatsu Ltd.

-

Ernst & Young

-

IBM

-

Oracle Corp.

-

PricewaterhouseCoopers

-

Rapport IT

-

SAP SE.

DXC Technology’s Recent Financial Trends

Total revenue by quarter (blue columns) has continued to decline year-over-year; Operating income by quarter (red line) has remained positive:

Seeking Alpha

Gross profit margin by quarter (green line) has trended slightly higher recently; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have been volatile:

Seeking Alpha

Earnings per share (Diluted) have recovered more recently:

Seeking Alpha

(All data in the above charts is GAAP.)

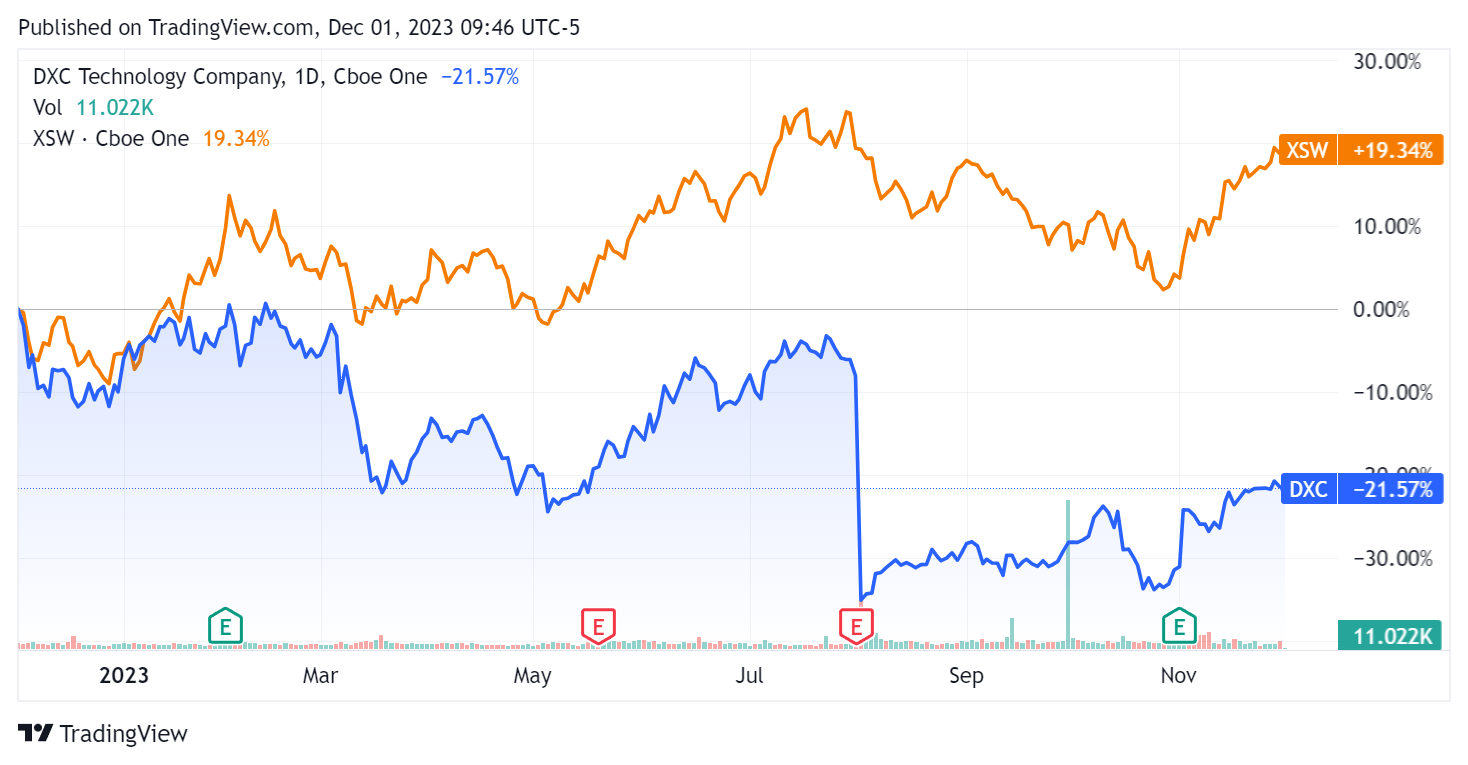

In the past 12 months, DXC’s stock price has fallen 21.57% vs. that of the SPDR® S&P Software & Services ETF’s ( XSW ) gain of 19.34%:

{kind=link}

For balance sheet results, the firm ended the quarter with $1.4 billion in cash and equivalents and $4.0 billion in total debt, of which $476 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $1.19 billion, during which capital expenditures were $229.0 million. The company paid $100.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For DXC Technology

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 0.6 |

| Enterprise Value / EBITDA |

| 18.2 |

| Price / Sales |

| 0.4 |

| Revenue Growth Rate |

| -8.7% |

| Net Income Margin |

| -4.0% |

| EBITDA % |

| 3.4% |

| Market Capitalization |

| $4,520,000,000 |

| Enterprise Value |

| $8,750,000,000 |

| Operating Cash Flow |

| $1,420,000,000 |

| Earnings Per Share (Fully Diluted) |

| -$2.47 |

| Forward EPS Estimate |

| $3.23 |

| Free Cash Flow Per Share |

| $4.47 |

| SA Quant Score |

| Hold - 3.09 |

(Source - Seeking Alpha.)

DXC’s most recent Rule of 40 calculation was negative (4.3%) as of FQ2 2024’s results, so the firm is in need of substantial improvement in this regard, per the table below.

| Rule of 40 Performance (Unadjusted) |

| FQ4 2023 |

| FQ2 2024 |

| Revenue Growth % |

| -11.3% |

| -8.7% |

| Operating Margin |

| 3.9% |

| 4.4% |

| Total |

| -7.4% |

| -4.3% |

(Source - Seeking Alpha.)

Commentary On DXC Technology

In its last earnings call (Source - Seeking Alpha ), covering FQ2 2024’s results, management’s prepared remarks highlighted organic growth for its GBS business segment.

The company is shifting its focus toward its GBS segment but continues to see its GIS segment produce revenue declines, resulting in overall revenue decline.

The GBS segment now accounts for 49.7% of total revenue.

Management is moving the firm to an "infrastructure-light" approach which it believes will enable it to sell underutilized assets and solidify the margin of the GBS segment in the future.

On capital allocation, the company has repurchased 10% of its stock year-to-date and still had another $500 million authorized under its fiscal 2024 repurchase program.

In the earnings call, I tracked the frequency of various terms and keywords used by management and analysts:

Seeking Alpha

The firm and its clients are facing cyclical challenges, with customers focused on mission-critical work and delaying discretionary projects amid macroeconomic uncertainties.

Analysts questioned leadership about the demand outlook and cost savings opportunities.

Management said that it is producing improved results converting pipeline to revenue, admitting that bookings have been lumpy.

On reducing costs, the firm is focused on facilities optimization, reducing contractors and rationalizing its onshore/offshore mix of expenses.

Total revenue for FQ2 2023 fell by 3.6% YoY while gross profit margin increased by 1.2%

Selling and G&A expenses as a percentage of revenue rose by 1.1% year-over-year, and operating income grew by 2.0%.

The company's financial position is good, with ample liquidity but significant long-term debt and strong positive free cash flow.

However, net interest expense rose materially in FQ2, highlighting the firm’s substantial debt exposure.

Management didn’t disclose any customer or revenue retention rate metrics.

Looking ahead, consensus revenue estimates for fiscal 2024 suggest a decline of 5.3% versus fiscal 2023’s results.

If achieved, this would represent a reduction in revenue decline rate versus fiscal 2023’s decline rate of 11.3% versus fiscal 2022.

Given the U.S. soft demand environment as clients reign in non-discretionary project spending and the firm’s GIS segment drag on revenue, I remain Neutral [Hold] on DXC for the near term.

For further details see:

DXC Technology Sees Lumpy Bookings As Clients Reduce Discretionary Spending