DXC - DXC Technology Stock: Poor Trends But Restructuring Can Unlock Value

2023-09-12 07:33:48 ET

Summary

- DXC has been under pressure amid falling sales and poor earnings.

- Management is attempting to streamline the operation by focusing on the strengths in its core Global Business Services segment.

- The stock has turnaround potential, but will need a few quarters of positive results to convince the market.

DXC Technology Company (DXC) is a global provider of IT services, helping companies scale through modernized analytics and optimized data architecture. Despite a well-established market position with operations in more than 70 countries, the company has been challenged in recent years amid a shifting competitive environment.

Indeed, the stock holds the poor distinction of being one of the worst-performing current constituents of the S&P 500 Index ( SP500 ) over the last 5-years, losing more than three-quarters of its value. Sales are down and earnings have suffered, but it's also important to recognize that the business remains profitable with some core strengths.

We're looking at the stock as a potential turnaround opportunity. The setup here is an ongoing restructuring where management has exited certain underperforming business lines to focus on growth areas. While there is still a lot of work to be done, we believe DXC will survive with the current strategy moving in the right direction. Room to reclaim earnings momentum into 2024 could be positive for the stock as the company unlocks underlying value.

DXC Financials Recap

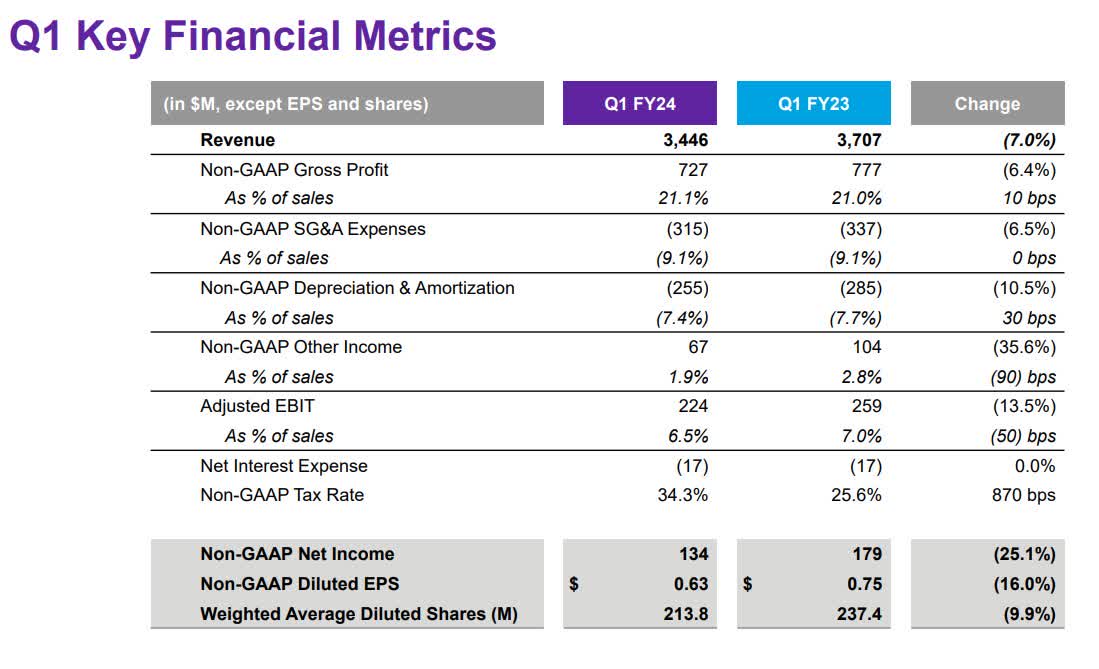

DXC last reported its fiscal 2024 Q1 results back in early August with a non-GAAP EPS of $0.63, coming in $0.19 below consensus. Revenue of $3.5 billion, down by -7% year-over-year also missed estimates.

This was an ugly report by most measures, resulting in a deep selloff on the day. While the adjusted gross profit margin of 21.1%, ticked higher by 10 basis points from Q1 fiscal 2023, the adjusted EBIT at $224 million, fell by -13.5% with the 6.5% margin, down from 7.0% in the period last year.

Management explains that the weaker-than-expected results , below previous guidance, were based on a slowdown in client activity as a broader macro theme. There is also an aspect of softer IT equipment resales, which is a smaller part of the business and lower margin historically, contributing to the bulk of the revenue shortfall this quarter.

{kind=link}

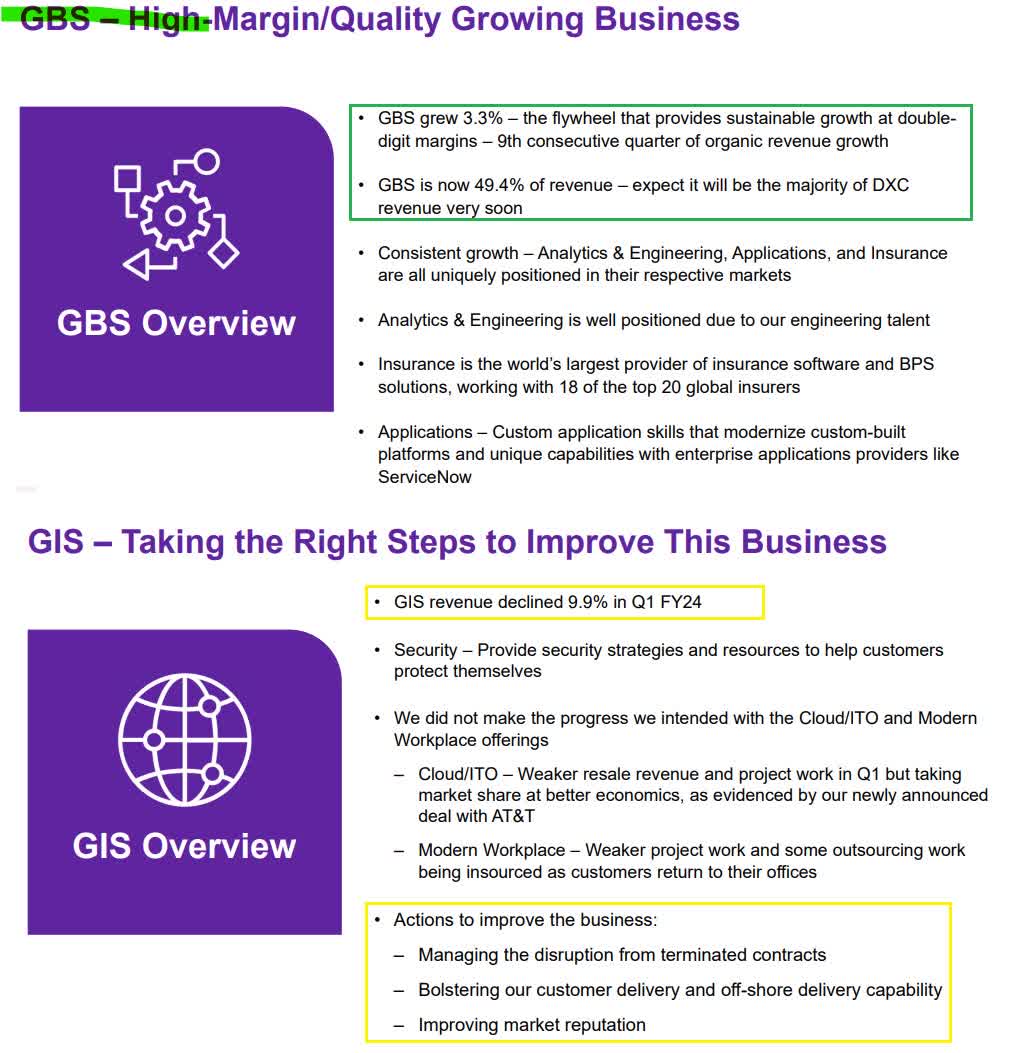

By segment, Global Business Services ((GBS)) has been the one strong point, with sales up 3.3% y/y in Q1. Currently, GBS represents 49% of the overall business, but the plan now is to divert resources to this group which maintains some competitive advantages in certain niches.

On this point, DXC notes that its insurance software is recognized as the most widely used "business process solution" in the industry worldwide, counting on 18 of the top global insurers as customers. That type of market positioning also seen with some high-profile customers in the analytics platform highlights the value of the DXC overall which still has relevant pieces.

GBS has balanced some of the weaknesses in the Global Infrastructure Services ((GIS)) segment, where revenues fell by 9.9% in Q1. One trend that has been seen is customers "insourcing" some types of work to their internal IT departments contributing to lower project levels.

The strategy going forward is to invest more towards the GBS while working to at least stabilize the GIS. There is also a move to shift its sales and marketing into an "offering-led model" to help drive engagement. From the earnings conference call :

We have changed how DXC engages with the market by moving to an offering led operating model. The offering led operating model moves us from a regional model where leaders were generalists concerning offerings to a global operating model where the leaders are experts and focused 100% on growing revenue and margin for their offerings. This model increases our customer coverage and assures we bring the right skills to our customers to deliver and win new work.

{kind=link}

DXC ended the quarter with $1.6 billion in cash against $4.6 billion in debt. Considering an adjusted EBITDA run rate of around $1 billion, a net debt leverage ratio of 3x is elevated but otherwise stable with room for improvement going forward.

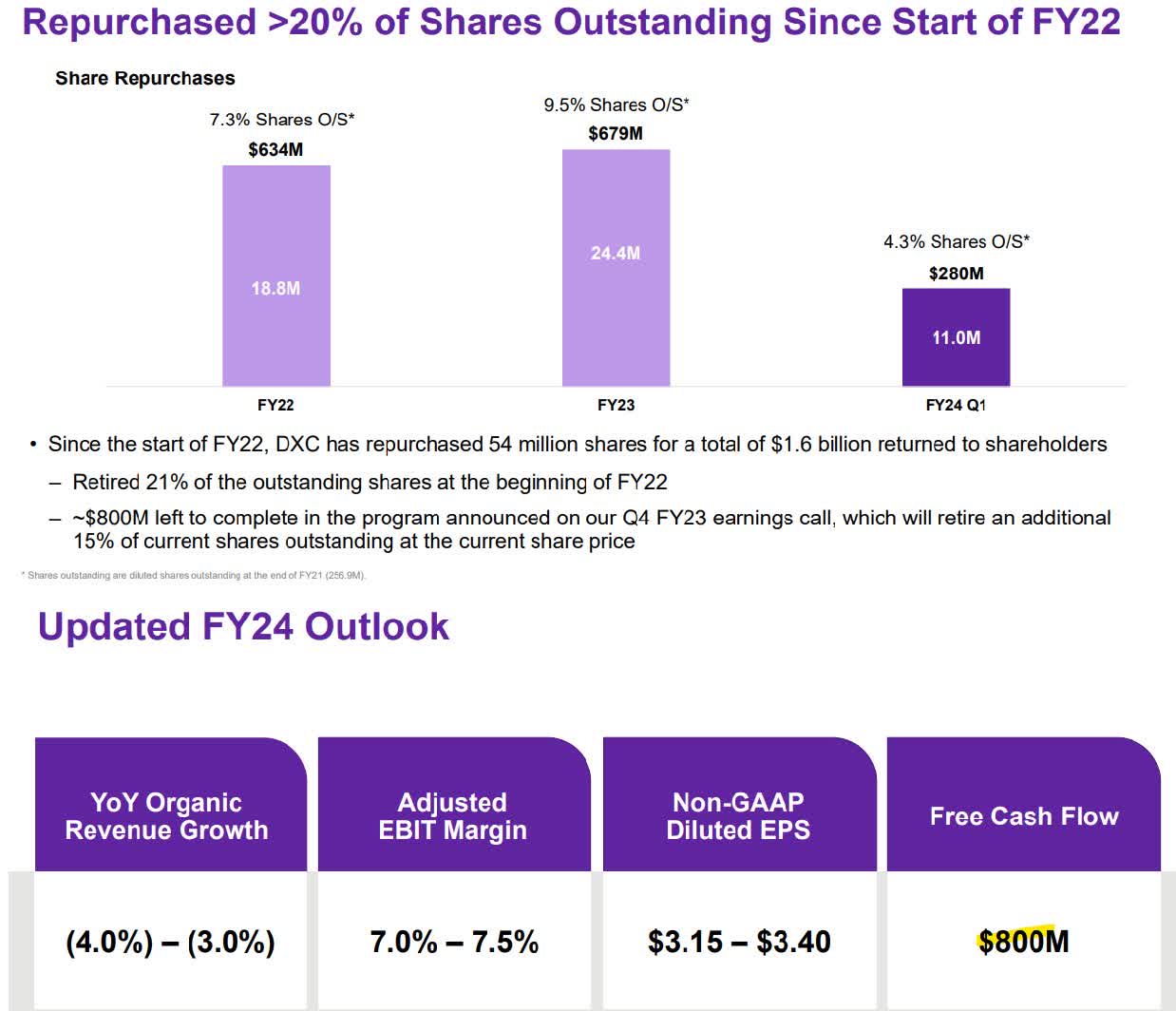

The company has been active with buybacks, repurchasing $280 million in shares during the quarter, with $800 million remaining under the existing authorization. The expectation is for a continuation of repurchases supported by underlying free cash flow.

For the full year ahead, management is guiding for organic revenues to be down between -3% and -4% compared to fiscal 2023. An EPS target between $3.15 and $3.40, if confirmed, would represent a -5% annual decline. All that being said, DXC expects to generate $800 million in free cash flow this year.

{kind=link}

What's Next For DXC?

It's clear to us that DXC has a growth problem. When we go through each of the company's wide range of offering s, one explanation for the apparent "downfall" in recent years is the rise of smaller software players specializing in specific niches or industry verticals that have essentially chipped away at DXC's market share.

It's fair to say the company lost a step on the innovation side compared to numerous software-as-a-service ((SAAS)) start-ups that have simply been more effective with their go-to-market strategy.

Still, DXC remains a major player with the advantage of having some deep relationships and an extensive customer base across the globe. We mentioned the GBS segment that grew 3.3% in Q1, with that side of the business representing nearly half of all revenues. Excluding the weaker GIS, DXC is a cash cow with a highly profitable consulting franchise.

The expectation is for 2024 to be a sort of transitional year, where management streamlines the operation into the high-value areas, to reduce expenses and help firm margins. If successful, the path is for a turnaround eventually.

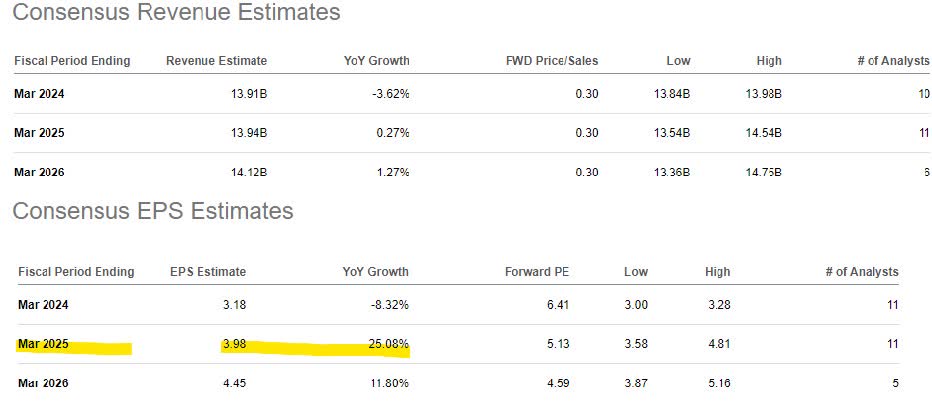

According to consensus, DXC's current year EPS and revenue estimates are in line with management guidance. The outlook turns more interesting for fiscal 2025, where EPS is forecast to climb by 25% toward $3.98. This would be achieved as revenue growth turns marginally positive and margins accelerate.

By this measure, assuming this recovery plays out, there is a case to be made that shares have value here today trading at a 6x forward P/E or 5x into the fiscal 2025 estimates. That depressed valuation right now reflects the uncertainty and risks considering the recent poor trends but would reprice higher if the targets are reached.

{kind=link}

Looking at the stock price chart, shares dived the heels of this last quarterly report from nearly $29.00, down to the current level of under $21.00 to a near three-year low. Our take is that this leg lower has discounted some of the softer trends, but could also offer an attractive entry point for investors with some confidence in the operating strategy and financial turnaround.

{kind=link}

Final Thoughts

There's no hero call here that shares are suddenly going to rocket higher. We see potential and lean bullish, but DXC remains a story stock until the company delivers. The biggest knock on shares right now is its lack of catalyst. Without a couple of quarters with improving financial metrics, there is not much reason to see a sustainable rally with shares likely to remain under pressure.

Officially, we rate shares as a hold, implying a natural view of the direction of the stock in the near term but looking ahead to the next few quarters. Key monitoring points include trends in the GBS segment as the future direction of the company along with the gross profit margin as a measure of pricing power and operating momentum.

On the downside, the risk is that results continue to disappoint which would force a reassessment of the long-term earnings potential. DXC also remains exposed to volatile macro conditions where a slowdown in global business spending would undermine demand for its services.

For further details see:

DXC Technology Stock: Poor Trends, But Restructuring Can Unlock Value