REIT - Earnings Can't Cure Gloom

2023-10-29 09:30:00 ET

Summary

- U.S. equity markets remained under pressure this week despite a retreat in benchmark interest rates as concerns over Middle East instability offset economic data showing decent growth and moderating inflation.

- Posting its worst October in five-years and closing at its lowest level since May, the S&P 500 dipped another 2.5% this week, officially entering "correction" territory.

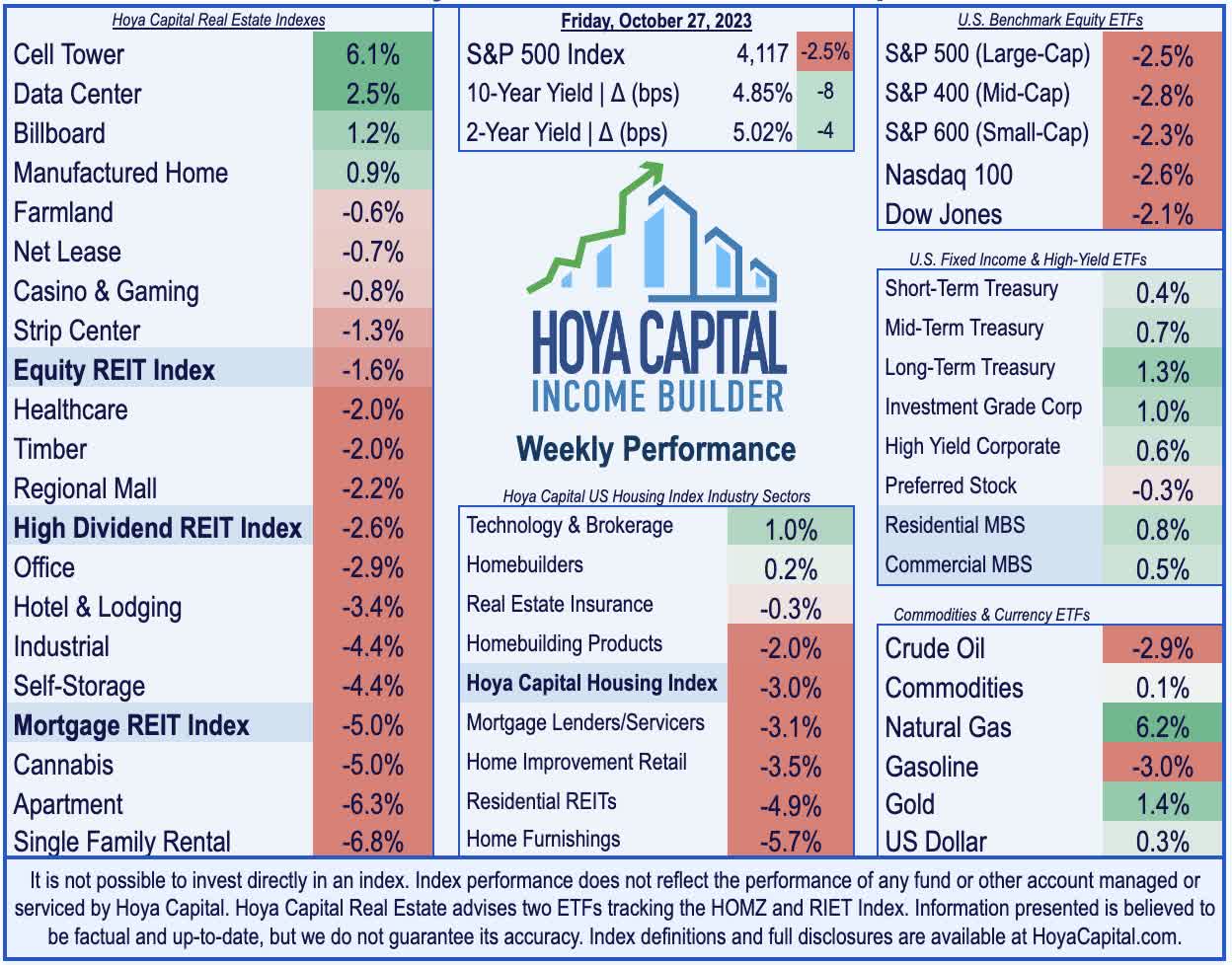

- Real estate equities posted modest outperformance over the major benchmarks, lifted by a decent slate of earnings results, a handful of dividend hikes, and a retreat in interest rates.

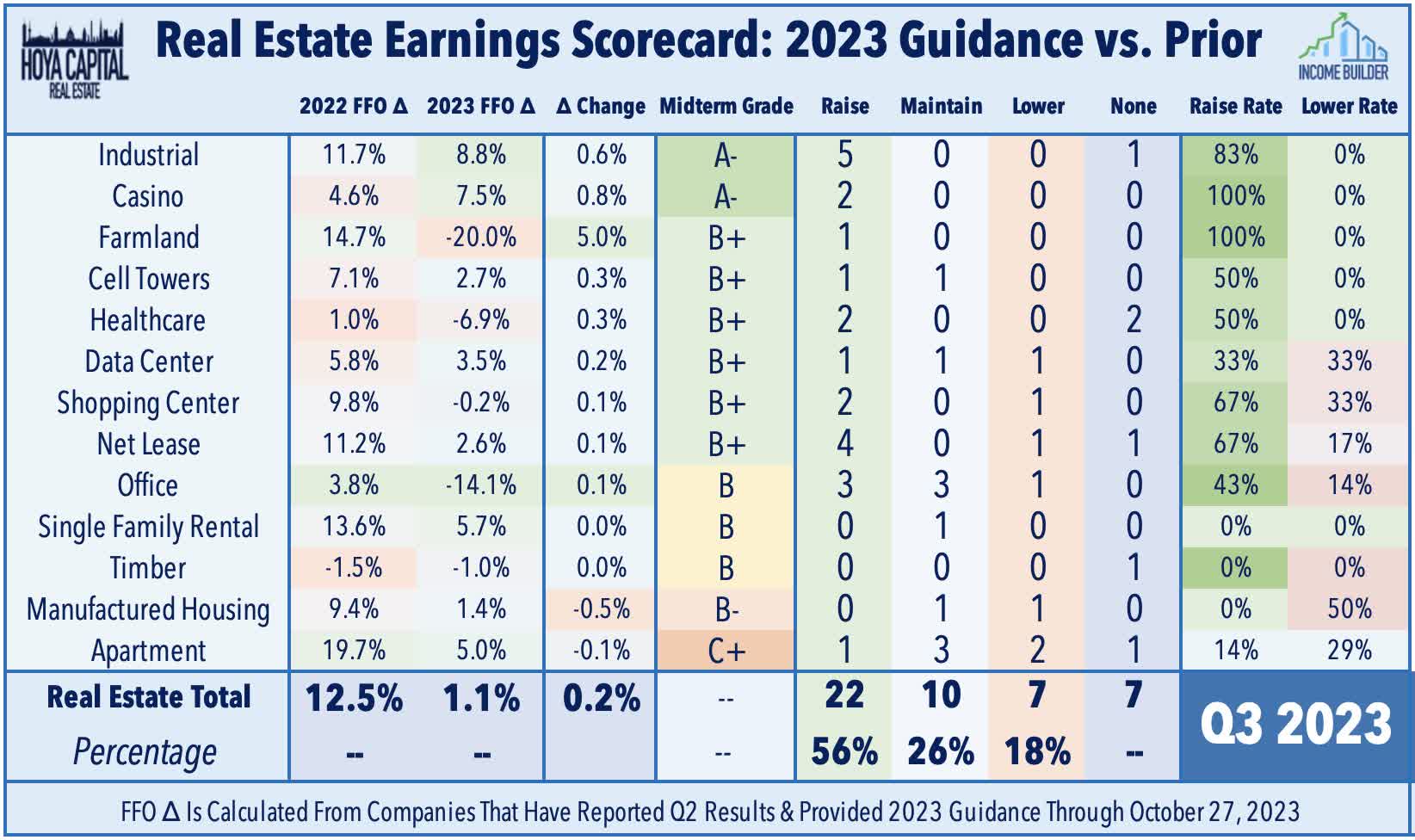

- REIT earnings results thus far have been stronger than expected. Of the 39 equity REITs that have provided updated full-year FFO guidance, 56% have increased their forecast, while 18% have lowered their outlook.

- REIT earnings season kicked into gear this week. Results thus far have been stronger than expected. Of the 39 equity REITs that have provided updated full-year FFO guidance, 56% have increased their forecast, while 18% have lowered their outlook.

Real Estate Weekly Outlook

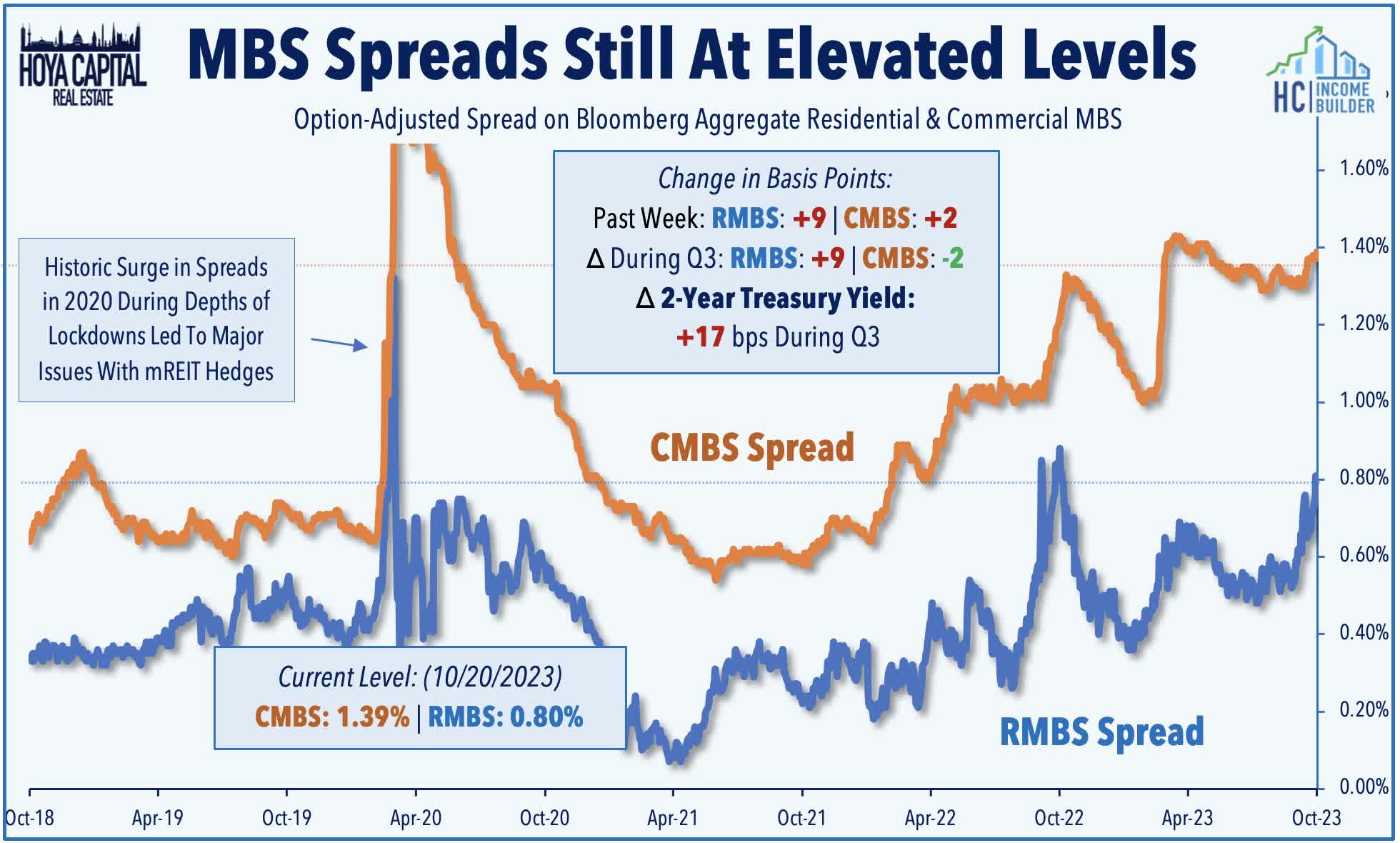

U.S. equity markets remained under pressure this week despite a retreat in benchmark interest rates as concerns over Middle East instability and a mixed slate of earnings results offset economic data showing stronger-than-expected growth coupled with a continued retreat in inflationary pressures. Central banks come back into the spotlight in the week ahead, and while the Fed is all but certain to maintain the Fed Funds rate at its current 5.50% upper bound in this meeting, the focus will be on the outlook for future rate hikes. Underscoring the amplified economic uncertainty, swaps market now imply a 25-30% probability that the Fed will hike once again by January, but are pricing in roughly three rate cuts by the end of 2024.

{kind=link}

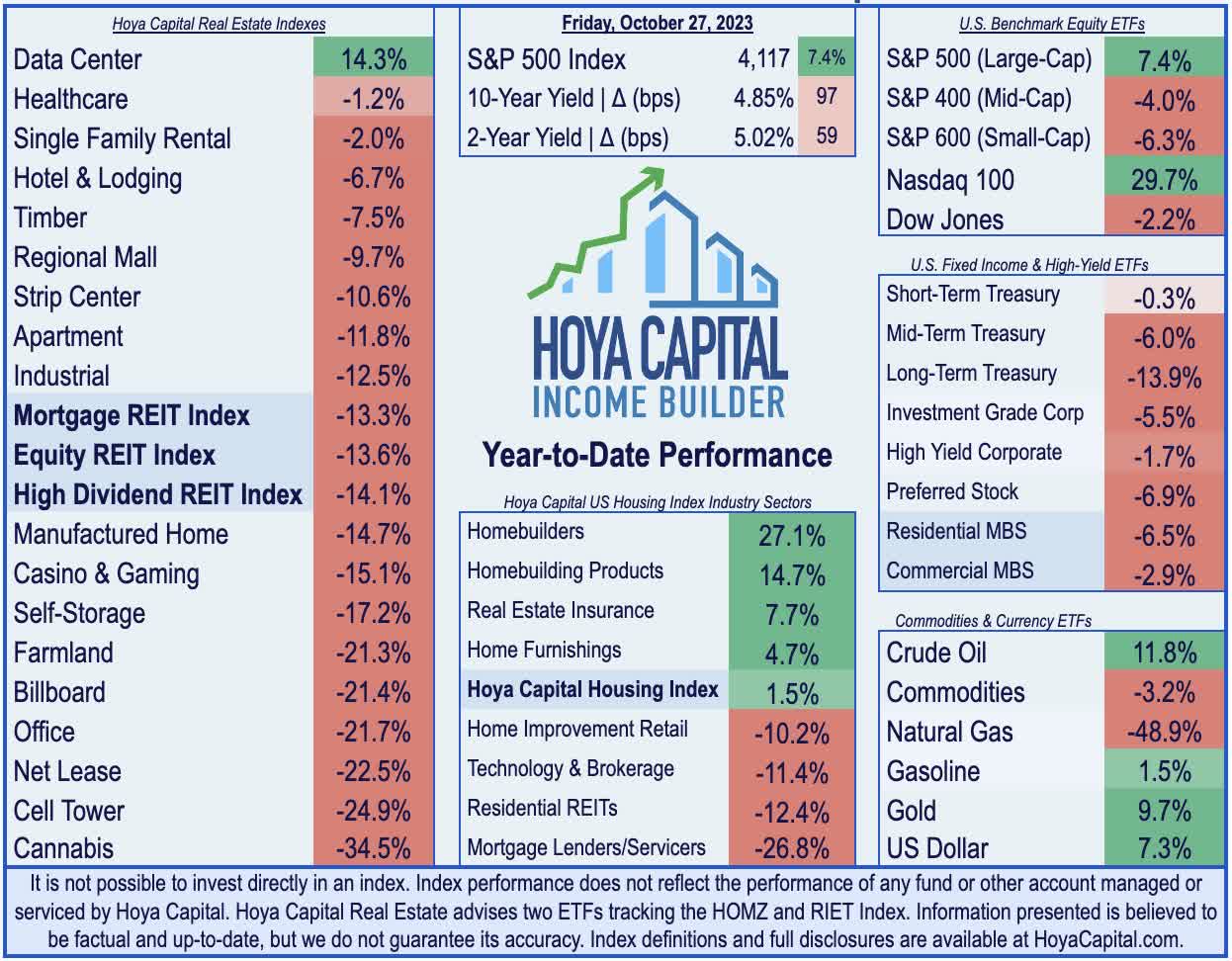

Declining for a second week and closing at its lowest level since May, the S&P 500 dipped another 2.5% this week, officially entering "correction" territory with declines of over 10% from its recent July peak. The other major benchmarks - the Mid-Cap 400 and Small-Cap 600 - also posted similar declines this week, with each approaching the "bear market" threshold with drawdowns of 15% and 18%, respectively. Real estate equities posted modest outperformance over the major benchmarks, lifted by a decent slate of earnings results and a retreat in interest rates. The Equity REIT Index declined 1.6% this week, with 14-of-18 property sectors in negative territory, while the Mortgage REIT Index dipped 5%. Homebuilders were among the leaders after earnings results showed that the nation's largest builders are still seeing some base level of demand despite the surge in mortgage rates, benefiting from historically low levels of available single-family inventory.

{kind=link}

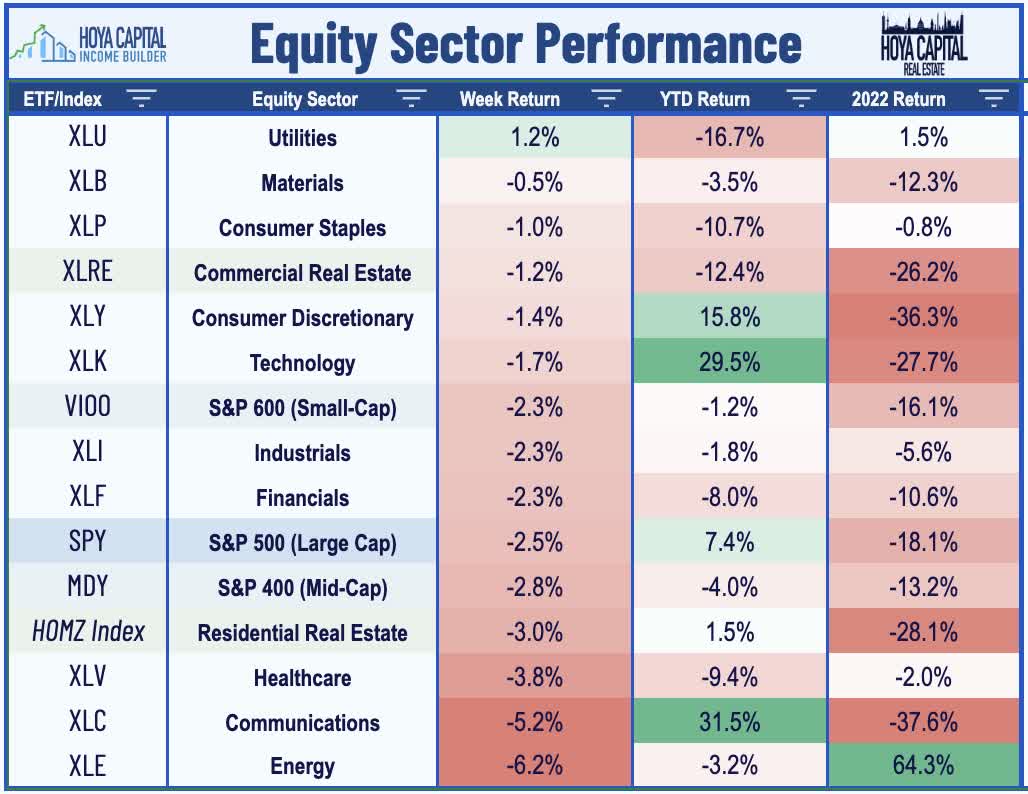

"Risk-off" was the theme of the week, as bonds finally caught a bid as investors assumed a defensive stance amid a jam-packed slate of corporate earnings results, economic data, and unsettled Middle East developments. After briefly trading above the 5.0% threshold early in the week, 10-Year Treasury Yield finished the week at 4.85% - lower by eight basis points - while the 2-Year Treasury Yield fell by four basis points to 5.02%. The CBOE Volatility Index - a measure of equity market volatility - closed the week around its highest levels since March. WTI Crude Oil prices retreated 3% this week to around $85/barrel amid a volatile week of geopolitical newsflow, while the US Dollar strengthened to its highest levels of the year. Ten of the eleven GICS equity sectors finished lower on the week, with particularly sharp pressure on Communications ( XLC ) stocks following a generally downbeat slate of mega-cap tech earnings results.

{kind=link}

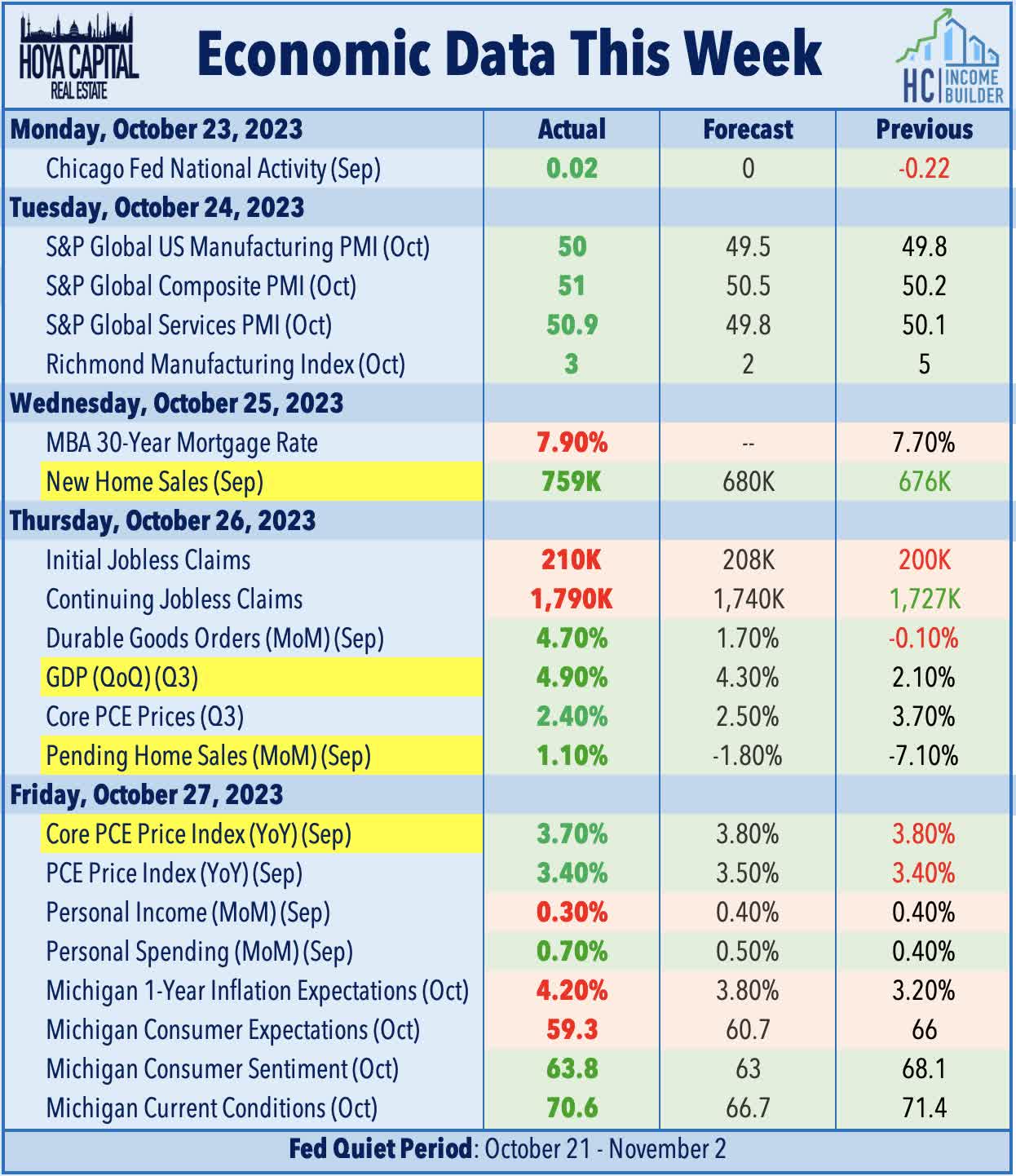

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

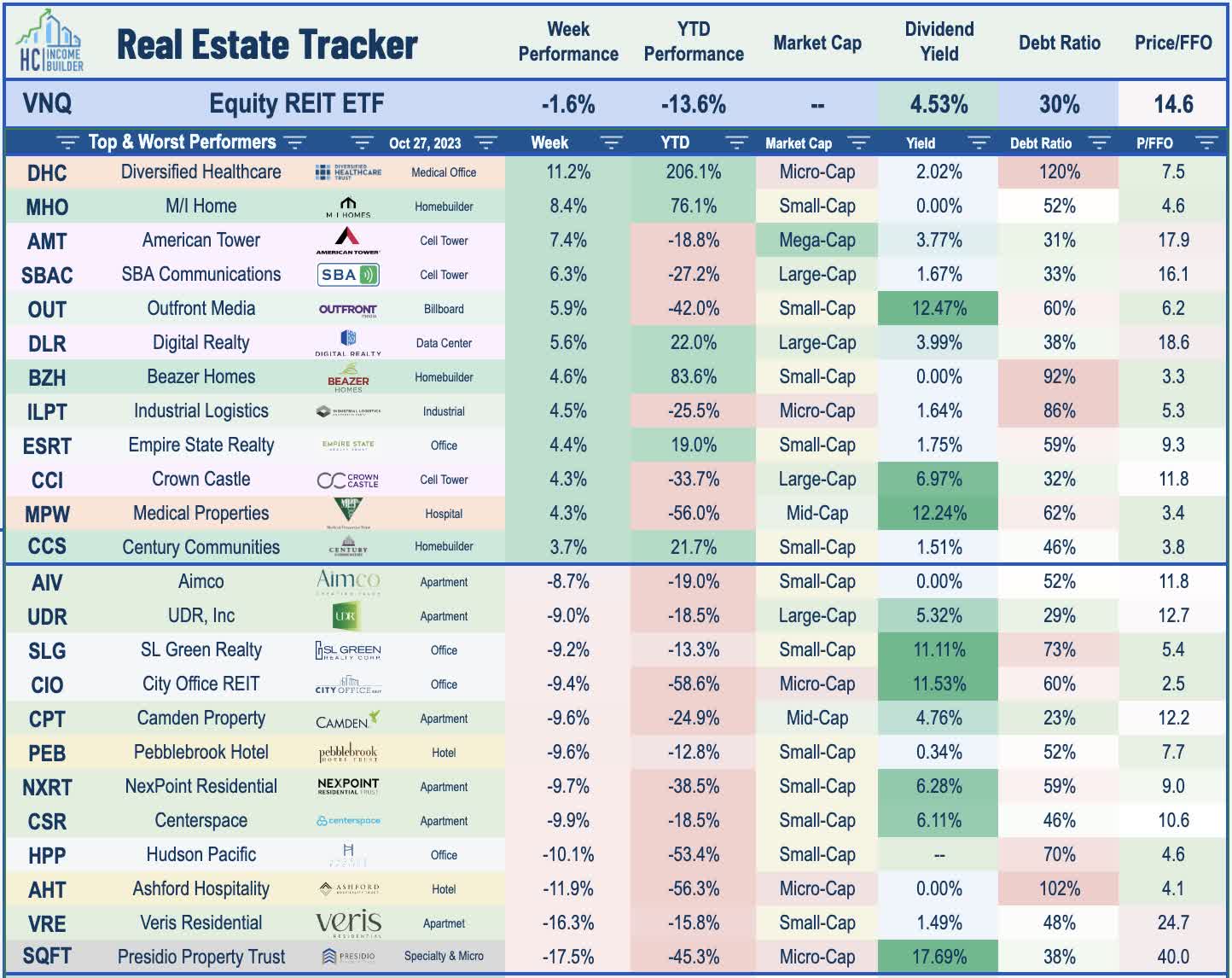

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Real estate earnings season kicked into gear this week with reports from roughly 50 REITs and a half-dozen homebuilders. As we'll discuss in our Earnings Halftime Report published later this weekend, results thus far have been stronger than expected across the majority of property sectors - and certainly stronger than the recent dismal share price performance of REITs would indicate. Of the 39 equity REITs that have provided updated full-year FFO guidance, 56% have increased their forecast, while 18% have lowered their outlook. We've also seen over a half-dozen REITs raise their dividend over the past two weeks - lifting the full-year total across the REIT sector to 70 - but the number of REIT dividend cuts has also ticked higher to 29. Industrial and data center REITs have been the notable upside standouts thus far, each exhibiting resilient pricing power and reporting manageable levels of supply growth. Stubbornly persistent expense pressures has been a common thread across residential sectors, with insurance and property taxes rising by double-digits across most markets and segments. As expected, soaring interest expense has prompted a number of downward guidance revisions - a theme that will be seen with greater frequency in the back-half of earnings season.

{kind=link}

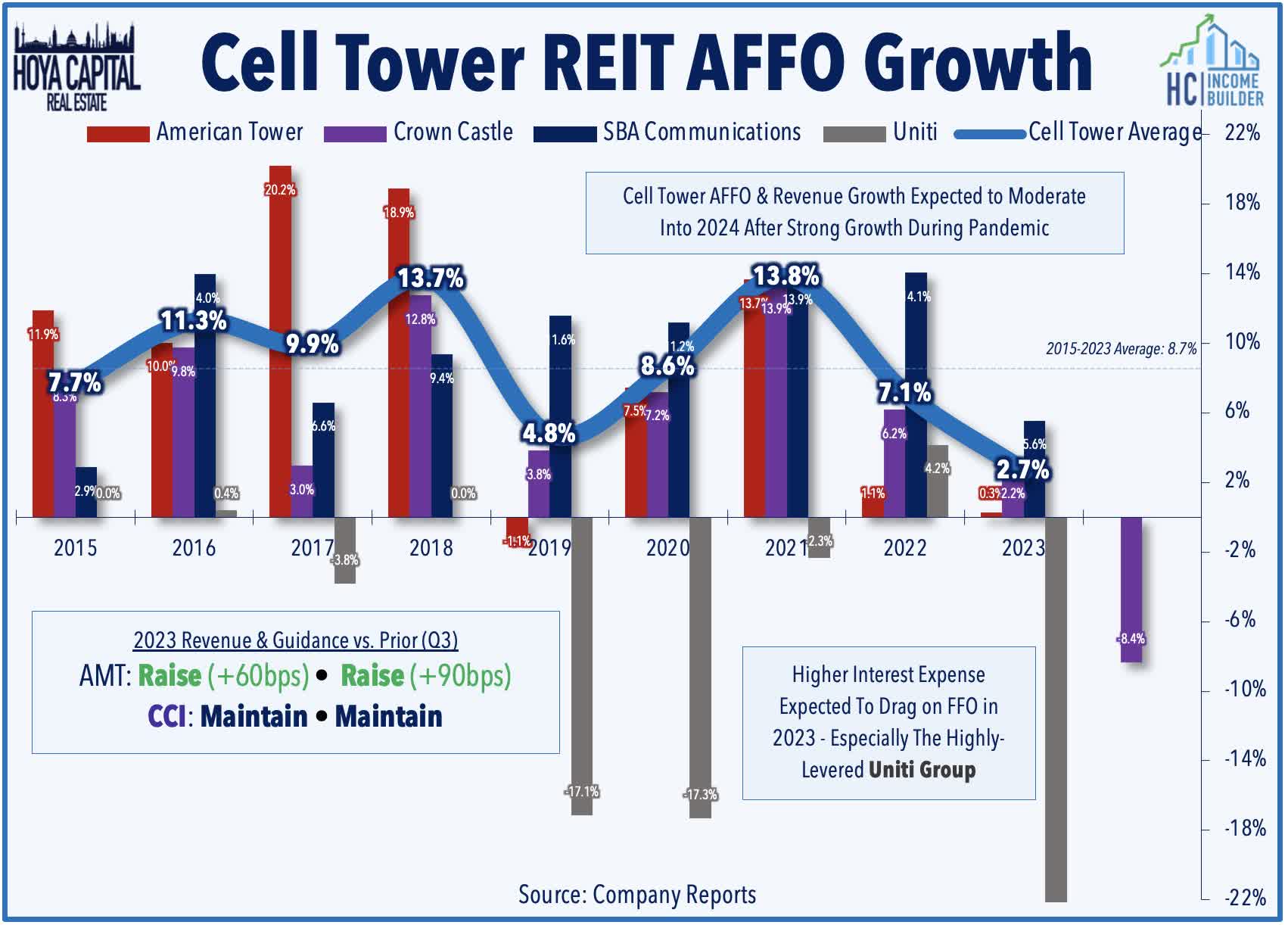

Cell Tower : Beginning with the upside standouts this week, American Tower ( AMT ) rallied 7.5% after reporting very strong results and raising its full-year outlook, while pushing back on concerns over a broader industry slowdown and noting the outperformance of its newly acquired data center business. Driven by domestic same-store ("organic billings") revenue growth of 6.3% - an acceleration from the 6.2% reported last quarter - AMT increased its full-year FFO growth target to 0.3% at the midpoint - up 90 basis points from its prior outlook. Pushing back on concerns over a 5G network spending slowdown, AMT commented that it "retains a high degree of conviction that there's a long tail of 5G network investment to come... Today, Phase 1 is winding down. We expect Phase 2 to be characterized by moderating spend from the record levels of 2022 to roughly $35 billion in 2023, which is $5 billion above 4G averages. A third capacity-focused phase will follow aimed at significant densification of 5G networks." While AMT did not provide a full 2024 outlook, it noted that it expects continued same-tower revenue growth of "at least 5% in the U.S. and Canada segment between 2023 and 2027."

{kind=link}

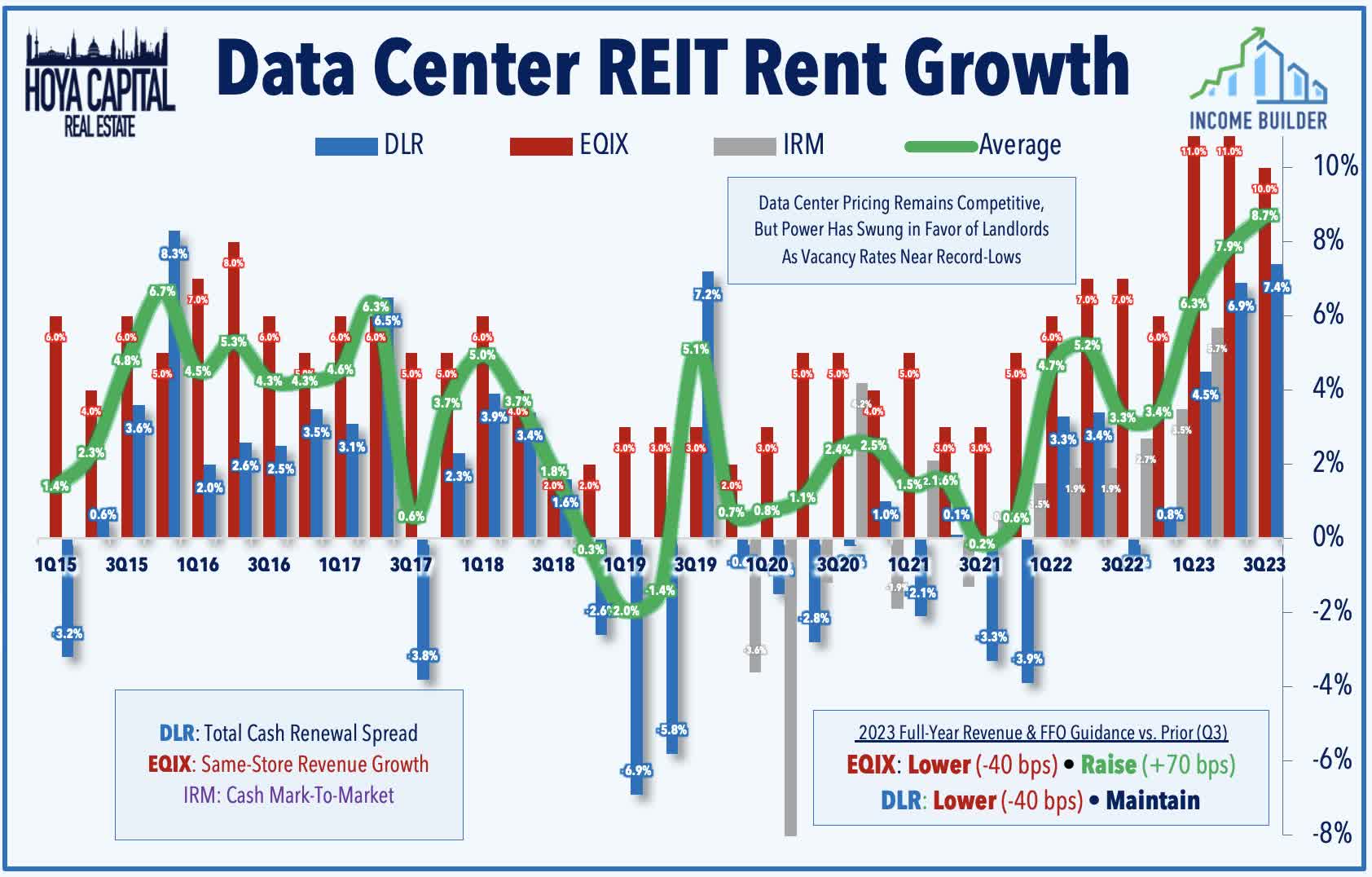

Data Center : Sticking in the tech space, Digital Realty ( DLR ) rallied 6% this week after reporting strong results, with robust underlying pricing and AI-fueled demand trends partially offset by currency headwinds. DLR reported total bookings of $152M - its strongest quarter of leasing activity in a year - and achieved renewal rent growth of 7.4% - its best quarter for pricing since 2015. DLR now expects 5.0% rent growth on renewals - up from 4.0% last quarter - and expects same-capital cash NOI growth of 6.5% - up from 4.5% last quarter. DLR has been an active seller this year, raising $2.5B through non-core asset sales and joint venture monetizations in an effort to bolster its balance sheet and reduce its variable rate debt exposure, which remains relatively elevated at 14% of total debt. Underscoring this rate headwind, DLR maintained its guidance that its FFO will decline 1.5% this year despite a 17.2% jump in revenues. Equinix ( EQIX ) gained 1% after reporting similarly solid results and raising its dividend by 25% to $4.26/share (2.5% dividend yield). EQIX now expects its full-year FFO to increase by 8.4% - up 70 basis points - while its revenue outlook was trimmed on FX adjustments.

{kind=link}

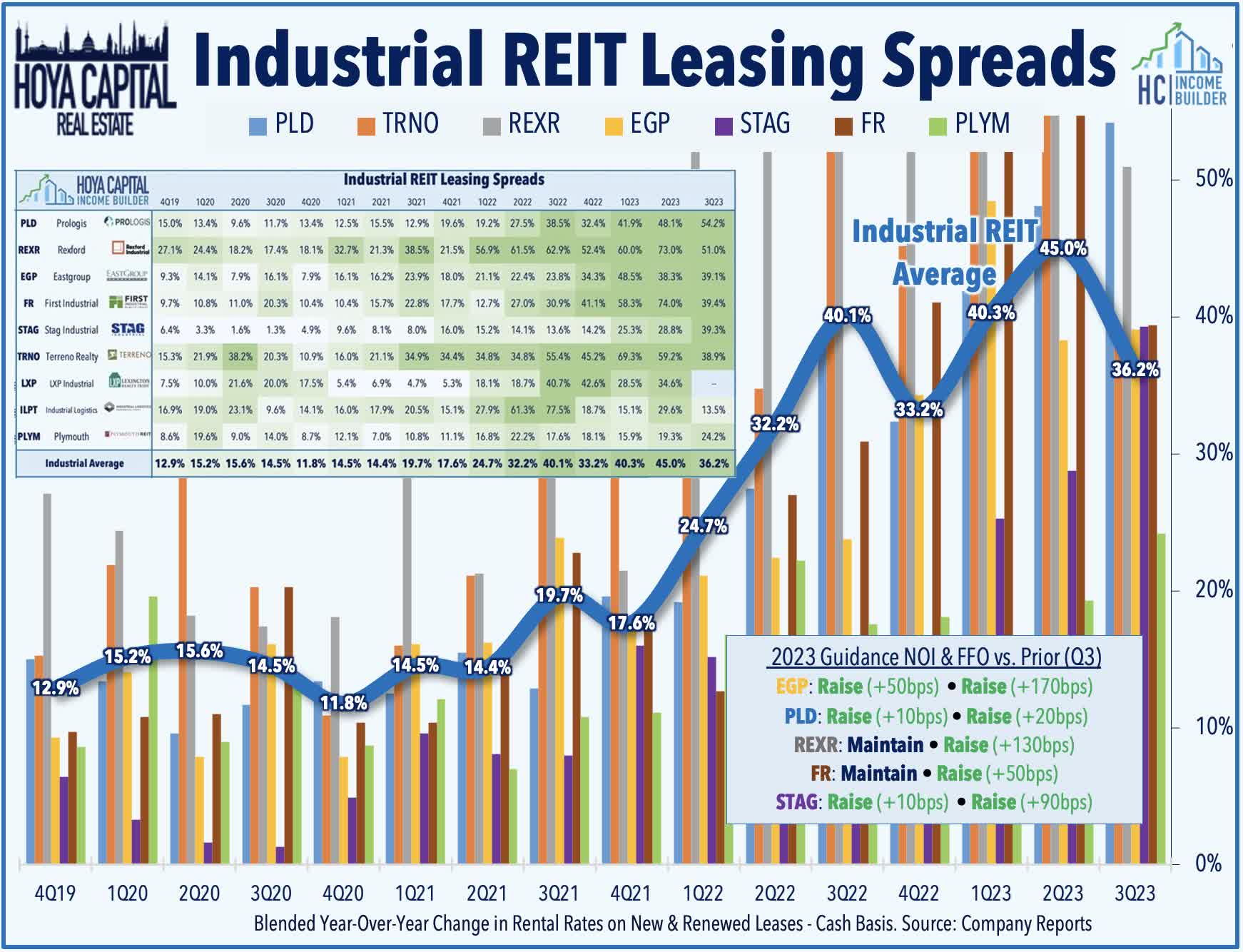

Industrial : Sunbelt-focused EastGroup ( EGP ) - which we own in the Dividend Growth Portfolio - gained 0.5% this week after reporting strong results and raising its outlook. EGP now expects full-year FFO growth of 10.7% - up 170 basis points - and expects same-store NOI growth of 7.8% - up 50 basis points. Bucking the trend of moderating leasing spreads seen across other industrial REITs, EGP reported an acceleration in cash leasing spreads to 39.1% in Q3, up from 38.3% in the prior quarter. EGP also upwardly revised its full-year occupancy outlook to 97.9% at the midpoint, up from 97.8% last quarter. EGP's commentary was notably upbeat, remarking that the "day-to-day industrial market remains resilient" and noted that it has seen a material decline in new construction starts this year. Stag Industrial ( STAG ) was little-changed this week after reporting similarly solid results and raising its full-year outlook. Leasing activity and rent growth were particularly impressive, with STAG recording record-high blended cash leasing spreads of 39.3% on 2.3M square feet of space in the third-quarter. STAG now expects full-year FFO growth of 2.7% - up 90 basis points - and expects same-store NOI growth of 5.4% - up 30 basis points. STAG noted that it believes its Sunbelt-heavy portfolio in secondary markets is particularly well-positioned given the period of elevated supply growth that will persist through mid-2024.

{kind=link}

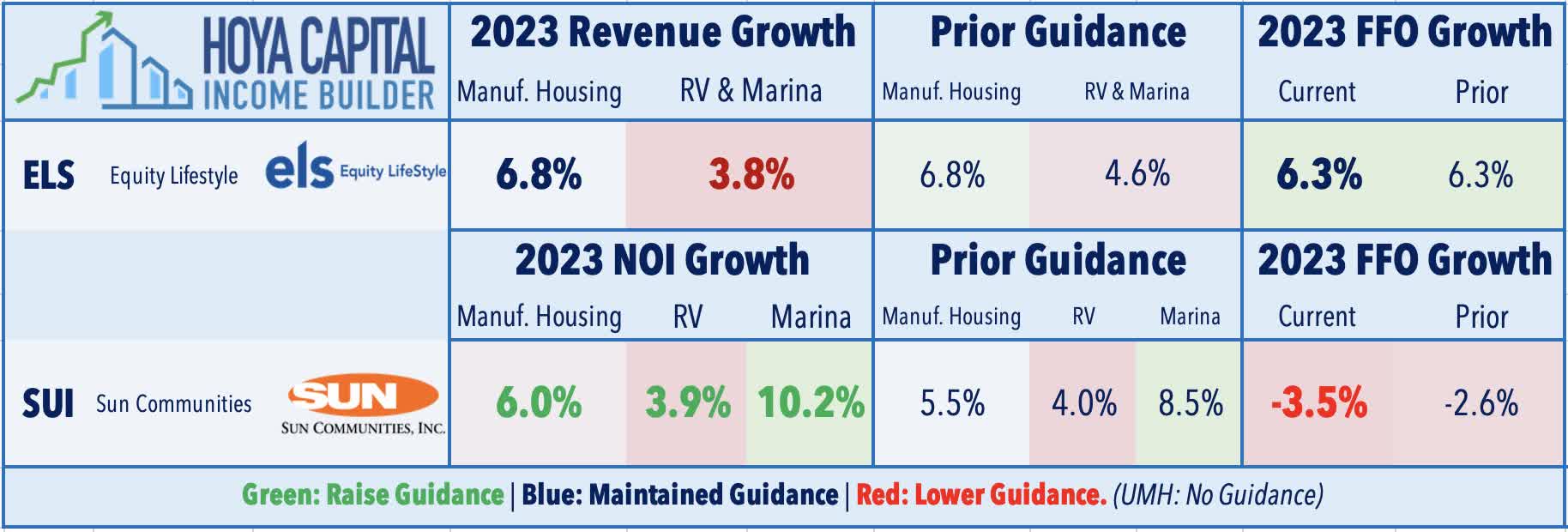

Manufactured Housing : Turning to the residential sector, Sun Communities ( SUI ) - which we own in the Dividend Growth Portfolio - was a notable upside standout after reporting solid results, as strong property-level fundamentals in the U.S. offset ongoing weakness in its international segments. SUI boosted its full-year NOI growth outlook for each of its three U.S. business segments, projecting growth of 6.0% in its core MH portfolio, 3.9% in its RV segment, and 10.2% in its marina segment. Sun also established preliminary guidance for 2024, noting that it expects MH rent growth of 5.4%, RV rent growth of 6.5%, and marina rent growth of 5.6%. Sun's ill-timed international expansion into the UK last year continues to weigh on its overall results, however, as continued weak home sales performance in its Park Holiday portfolio and a separate default on a $361M loan to a different UK manufacturing housing operator prompted a downward revision to its FFO forecast. Sun commented that it plans to "realign our strategy to focus on our proven, durable income streams [by] recycling capital out of non-core investments to decrease our leverage return to the consistency of our earnings we have long enjoyed."

{kind=link}

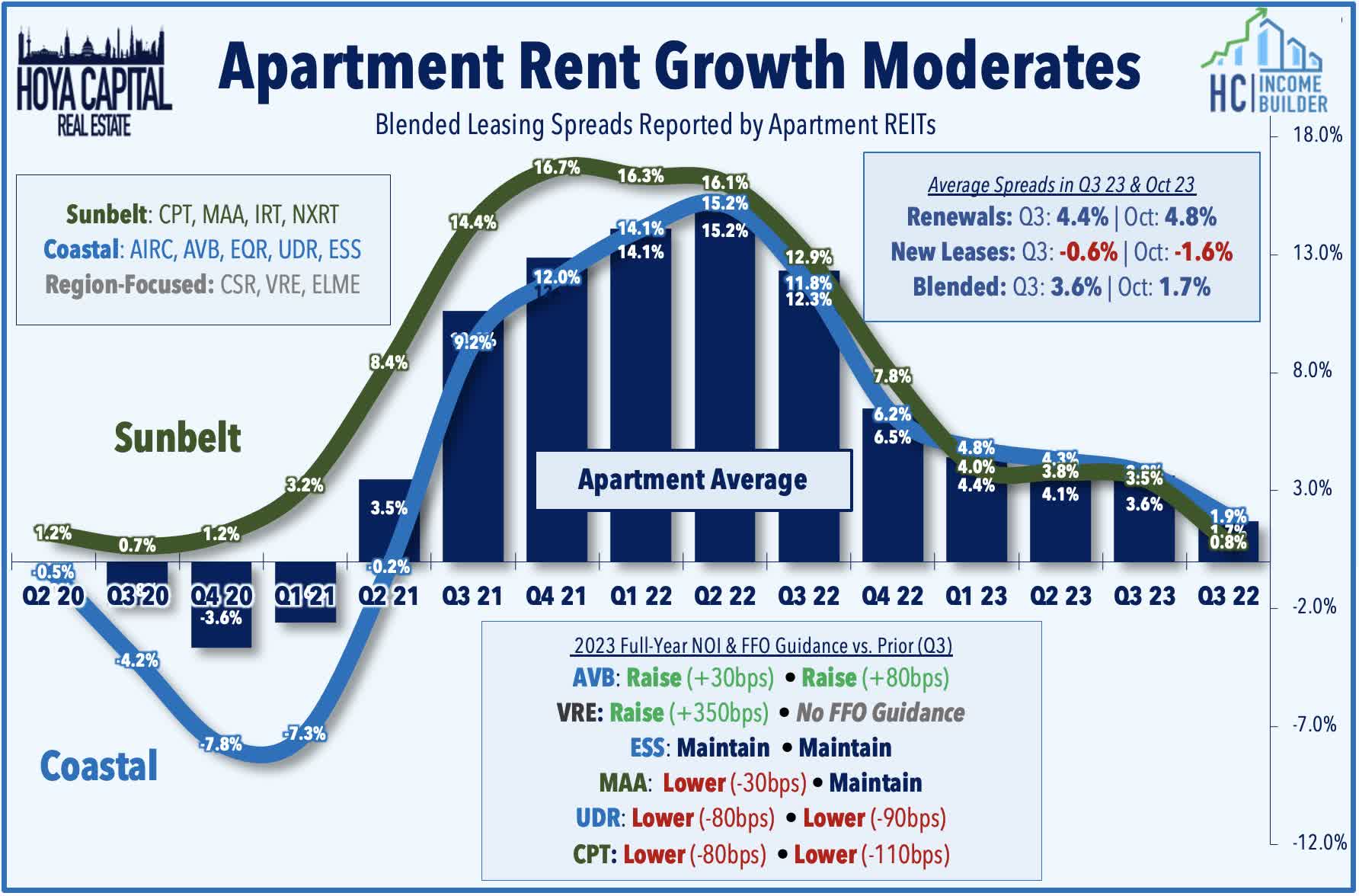

Apartment : Supply growth was the theme across a mixed slate of apartment REIT earnings this week. Sunbelt-focused Camden Property ( CPT ) dipped nearly 10% after reporting soft results and lowering its outlook. CPT notes that its blended rent growth cooled to 2.5% in Q3 and dipped into negative-territory in October at -0.4% - the weakest among the apartment REITs to report results thus far. CPT now expects full-year FFO growth of 3.3% - down 110 basis points - and trimmed its same-store NOI target to 4.2% - down 80 basis points. Coastal-focused UDR Inc ( UDR ) dipped 9% after reporting similarly soft results and lowering its full-year outlook, noting that "resident financial health remains resilient but elevated new apartment supply is resulting in less robust pricing power than we had previously expected." UDR recorded a deceleration in rent growth to around 1% in Q3 and into early Q4. UDR now expects full-year FFO growth of 6.2% - down 90 basis points from its prior outlook - and trimmed its same-store NOI target to 6.8% - down 80 basis points. AvalonBay ( AVB ) dipped 4% despite reporting the strongest results of the group and raising its outlook across the board, while noting that it's seeing less supply growth than its peers given its focus on suburban Coastal markets. West Coast-focused Essex ( ESS ) declined 2% this week after reporting relatively solid results as well and maintaining its full-year outlook. ESS reported that blended rent growth cooled to 2.1% in Q3, but actually accelerated in October to 2.9% driven by strong renewal rent growth.

{kind=link}

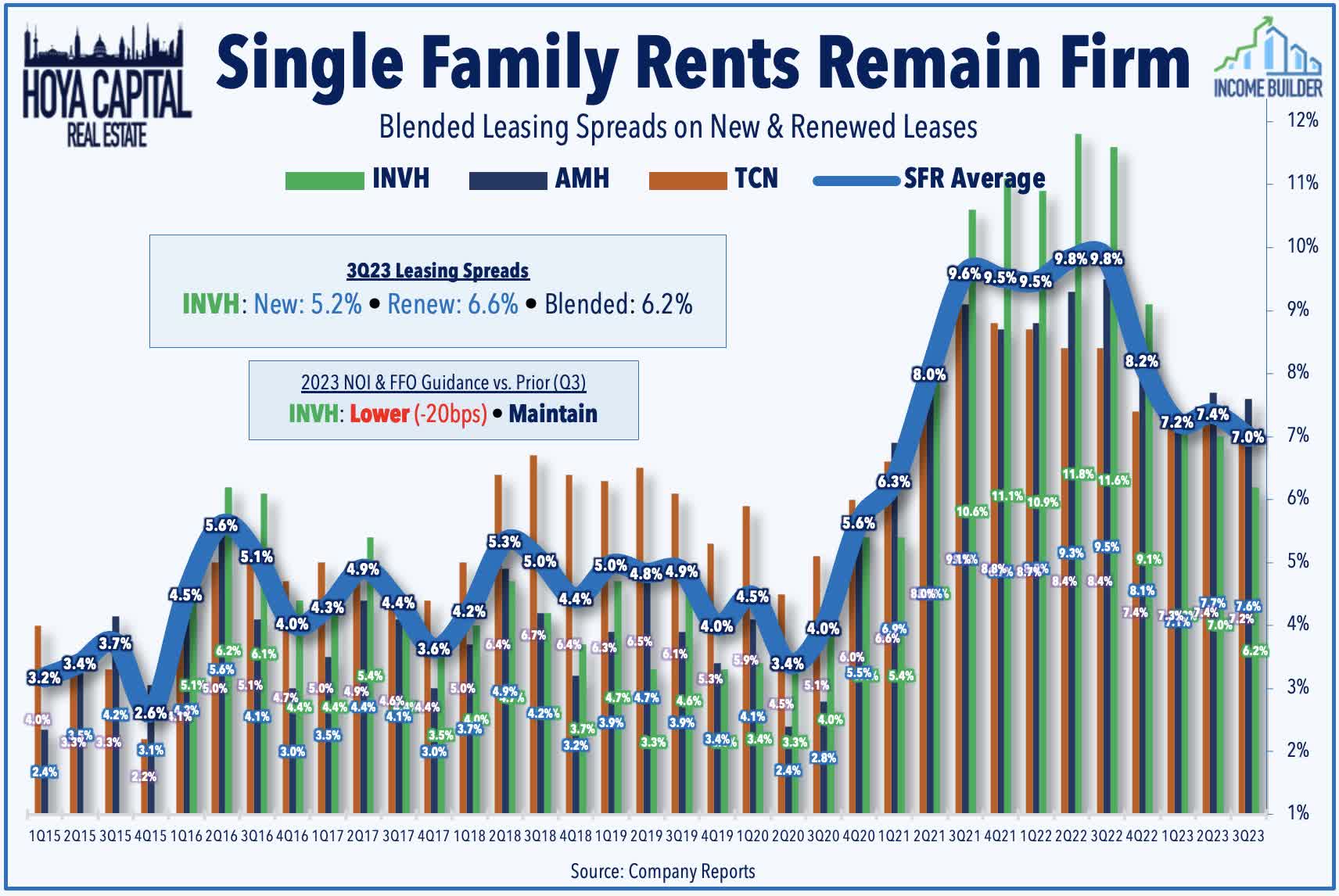

Single-Family Rental : Invitation Homes ( INVH ) - the largest single-family housing owner in the U.S. - was among the laggards this week after reporting mixed results and trimming its full-year outlook on higher property taxes and insurance expenses. INVH maintained its full-year AFFO outlook - which calls for 5.0% growth this year - but trimmed its same-store NOI guidance to 4.8% - down 20 basis points from its prior outlook. INVH now expects same-store expenses to rise 10.5% this year, and reported that property tax expense was higher by 13% year-over-year, while insurance expense was 15% higher. Leasing trends remained solid, however, with INVH recording blended leasing spreads of 6.2% comprised of 6.6% increases on renewals and 5.2% increases on new leases. While new homeowners can now expect to pay in excess of 8% on a new mortgage, INVH noted that it raised $800M in Q3 at an average interest rate below 5.5%. This cost of capital advantage facilitated a robust quarter of acquisitions, with INVH buying 2,291 homes for $854 million.

{kind=link}

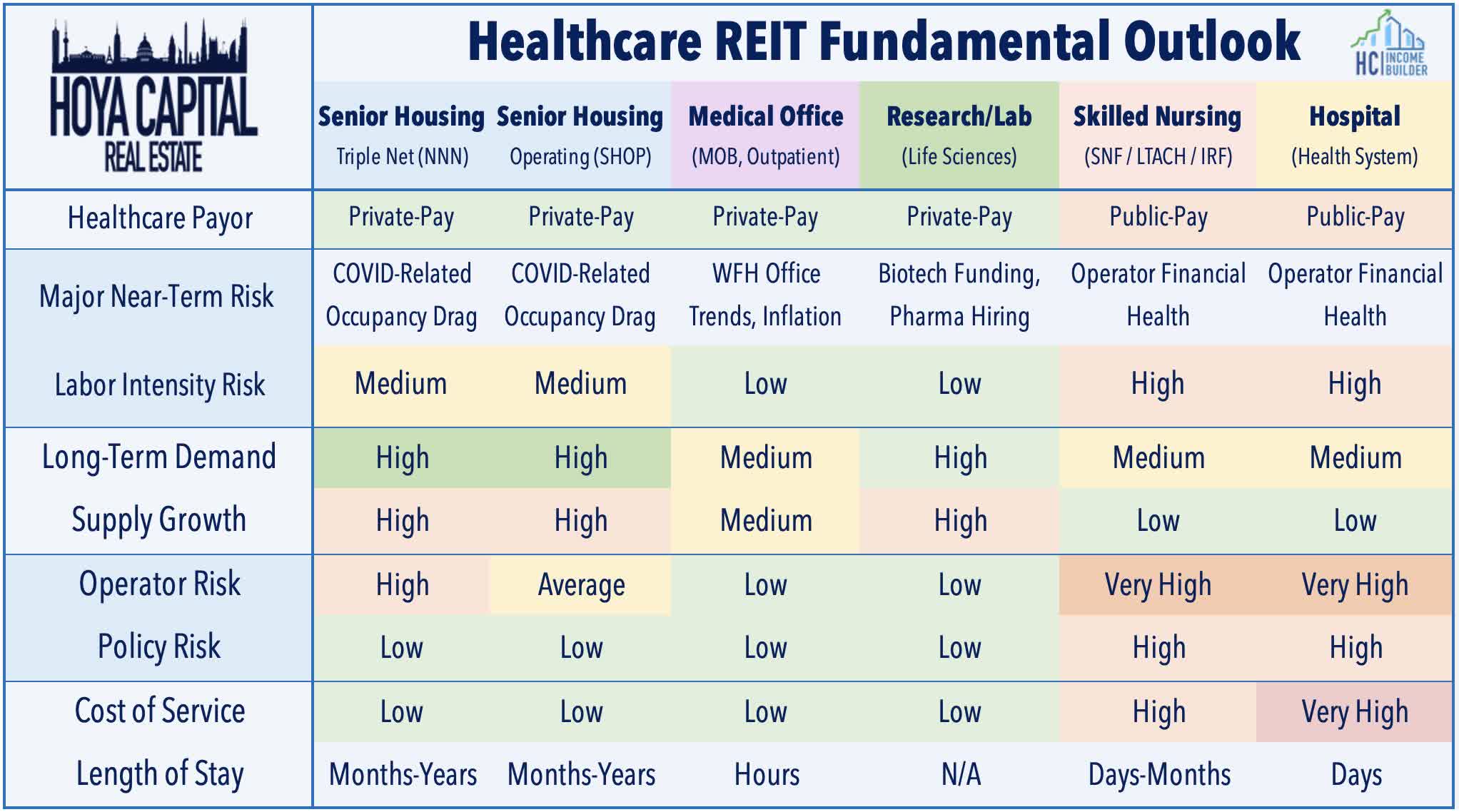

Healthcare : Embattled hospital owners Medical Properties Trust ( MPW ) - which has plunged over 65% since the start of 2022 amid rent collection issues from a handful of struggling hospital operators - advanced 4% this week after reporting decent results and raising its full-year outlook. MPW now expects its full-year FFO to decline 13.7% - a 110 basis point improvement from its prior outlook. Importantly, MPW noted that it resumed collecting cash rent payments in September and October from Prospect Medical, which had been struggling to pay rent. MPW - which had slashed its dividend by about 50% earlier this year - also detailed its new capital allocation strategy to raise $2B in new liquidity over the next year through asset sales and limited secured debt financing options. Lab space owner Alexandria Real Estate ( ARE ) declined 3% this week despite reporting solid results and raising the midpoint of its full-year FFO outlook. ARE - which has been among the laggards within the REIT sector this year on concern of sluggish lab space demand and oversupply in several major markets - now expects full-year FFO growth of 6.7%, up 30 basis points from its prior guidance. Leasing activity remained sluggish in Q3, as expected, with total volume of 867k square feet - its lowest since Q1 of 2020 - and down from 1.3M in Q2 and 1.2M in Q1.

{kind=link}

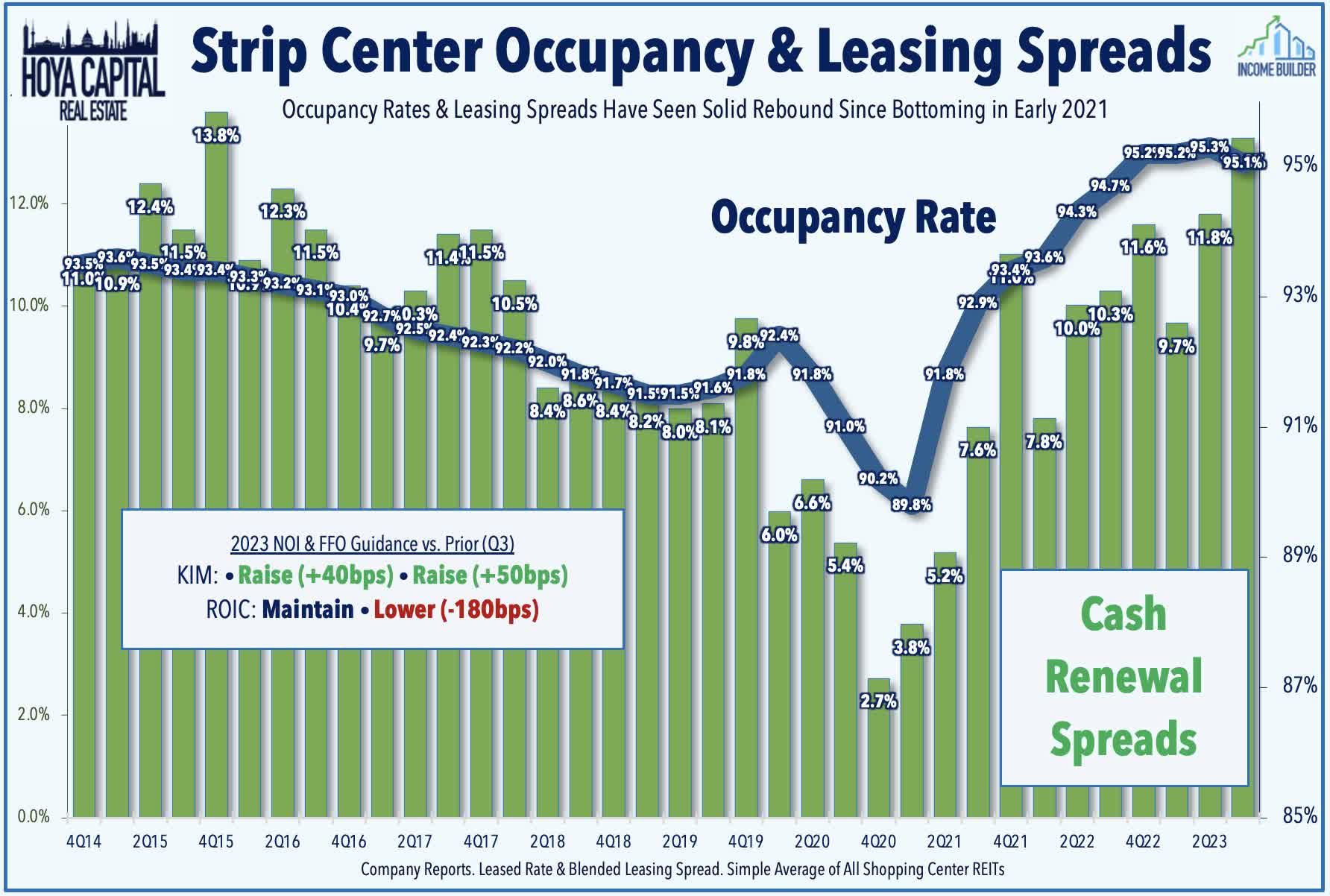

Strip Center : Two strip center REITs reported results this week. Kimco ( KIM ) - the largest strip center REIT - gained 1% this week after reporting strong results and boosting its full-year outlook and dividend. KIM now expects its full-year FFO to decline 0.9% at the midpoint of its range - a 40 basis point improvement from last quarter - and expects NOI growth of 2.0%, up from 1.5% last quarter. Demand remains robust for well-located strip center space, as KIM noted that it leased 2.1M square of space in Q3, achieving blended rent of 13.4%, the highest level of combined leasing spreads in six years. Pro-rata portfolio occupancy ended the quarter at 95.5%, increasing 20 basis points year-over-year. Additionally, Kimco became the 70th REIT to raise its dividend this year, hiking its payout by 4.3% to $0.24/share (5.9% dividend yield). Retail Opportunity ( ROIC ) dipped 6% this week, however, after reporting mixed results and lowering its full-year FFO outlook on higher interest expense. ROIC now expects its full-year FFO to decline 3.6% - a 180 basis point downward revision. Property-level fundamentals remained strong, as ROIC maintained its same-store NOI growth at 3.5%, achieving impressive rent spreads of 36.0% on new and renewed leases in Q3, resulting in a 7.2% overall increase in base rents. ROIC commented, "demand continues to be consistently strong with a broad range of new tenants actively seeking space."

{kind=link}

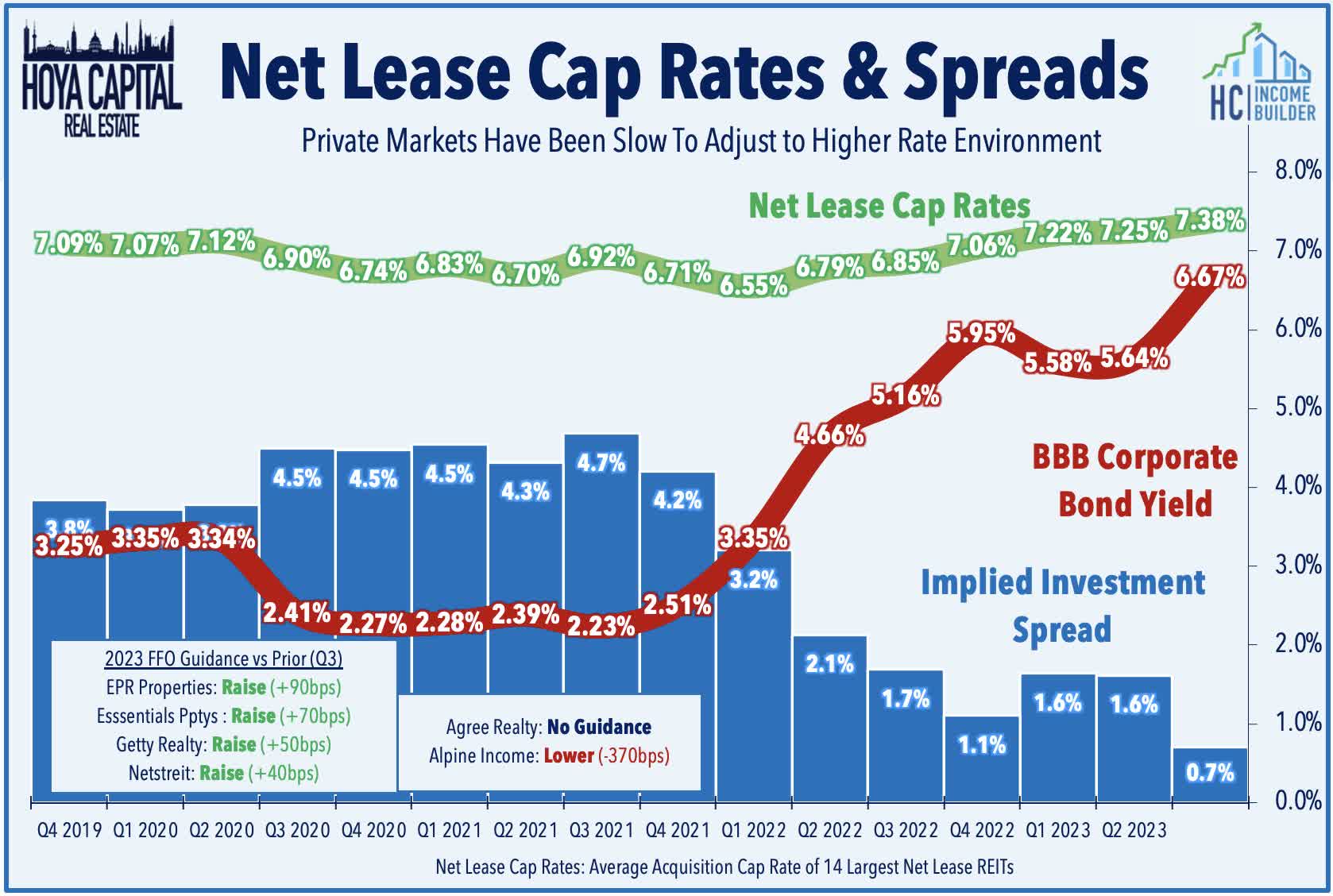

Net Lease : Results from five net lease REITs this week - four of which raised their full-year FFO outlook - showed that these REITs are among the few active buyers left across the real estate industry amid the surge in financing cost. Among the seven net lease REITs that have reported results thus far, acquisition cap rates have trended higher by only 20 basis points from last quarter, pressuring the implied net investment spread to below 1%. Essential Properties ( EPRT ) gained 1% after it boosted its full-year FFO growth guidance to 7.5% - up 70 basis points - and provided initial 2024 guidance calling for FFO growth of another 5.4%. EPR Properties ( EPR ) was little-changed after it raised its full-year FFO growth guidance to 9.6% - up 90 basis points - driven by "significant deferral collections" and the improved outlook related to its restructured master lease agreement with movie theater operator Regal. Netstreit ( NTST ) was little-changed despite raising its full-year FFO growth outlook of 5.2% - up 40 basis points. Getty Realty ( GTY ) - declined 1% despite boosting its full-year FFO growth target to 4.9% - up 50 basis points - while also boosting its dividend by 4.7% to $0.45/share (6.8% dividend yield). Agree Realty ( ADC ) also declined 1% after maintaining its full-year outlook for $1.3B in total acquisition volume.

{kind=link}

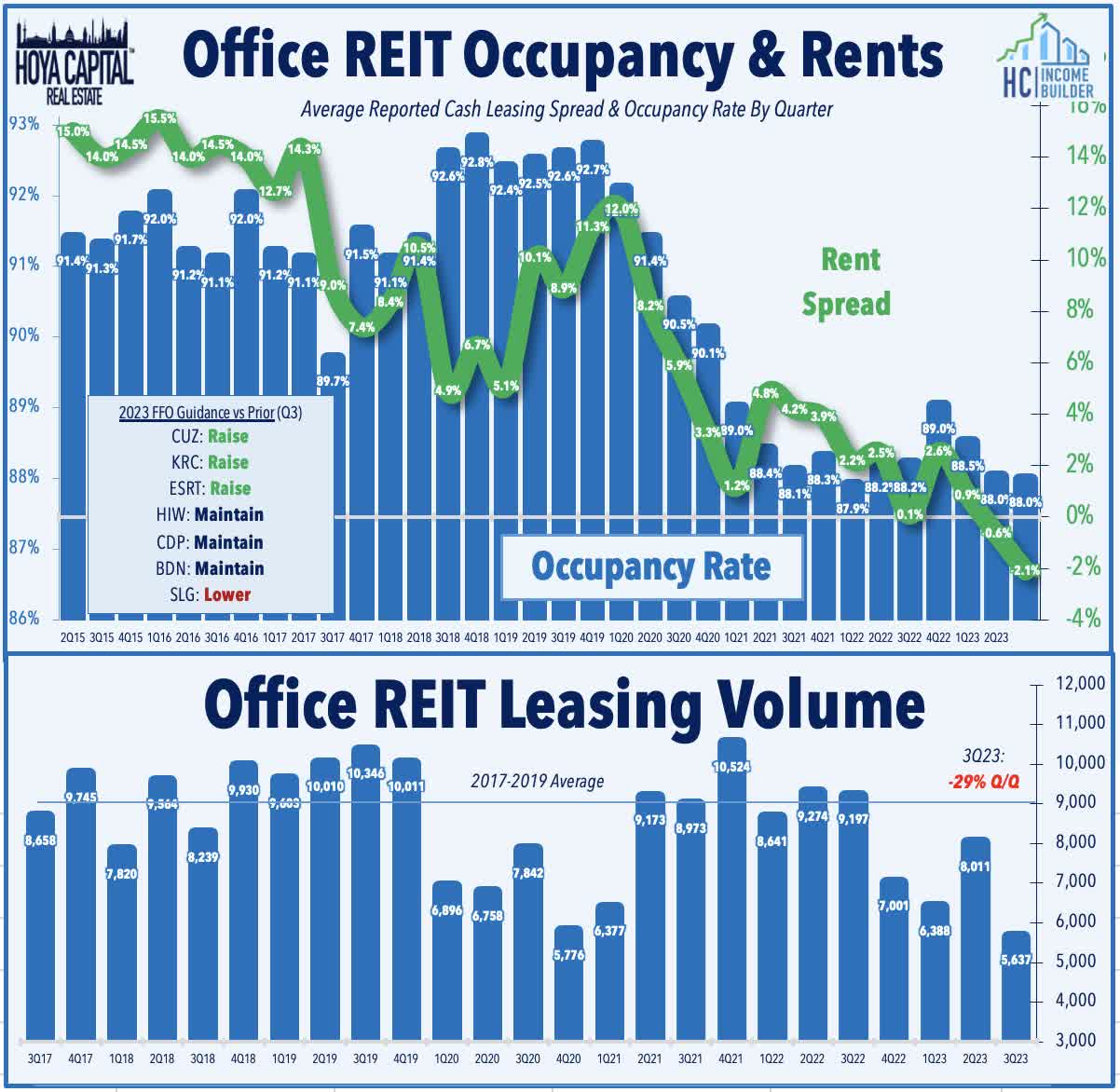

Office : Unsurprisingly, results this week from office REITs showed continued demand headwinds, but Sunbelt markets continue to exhibit notable - and underappreciated - outperformance over clearly-troubled coastal markets. Sunbelt-focused Cousins ( CUZ ) was also among the leaders after reporting decent results and raising its full-year outlook. Bucking the trends, CUZ reported an acceleration in leasing activity in Q3, recording 548k square feet of activity and achieving rent growth of 9.8% on renewed leases. Comparable occupancy also improved to 88.0%, up 70 basis points. Driven by favorable property tax adjustments, CUZ now expects its full-year FFO to decline 3.7% this year - a 70 basis point improvement from the prior quarter. Cousins is one of three office REITs to raise its full-year FFO outlook this quarter, joining Empire State Realty ( ESRT ) and Kilroy ( KRC ). On the downside, Philadelphia-focused Brandywine ( BDN ) declined 4% after reporting soft leasing volume at 351k SF, down from 411k in the prior quarter. Cash leasing spreads remained barely positive at 0.8%, while its comparable occupancy rate declined 110 basis points. Among the seven office REITs to report results this far, leasing activity has averaged 22% below last quarter, while occupancy rates - already at historic lows - have been roughly flat.

{kind=link}

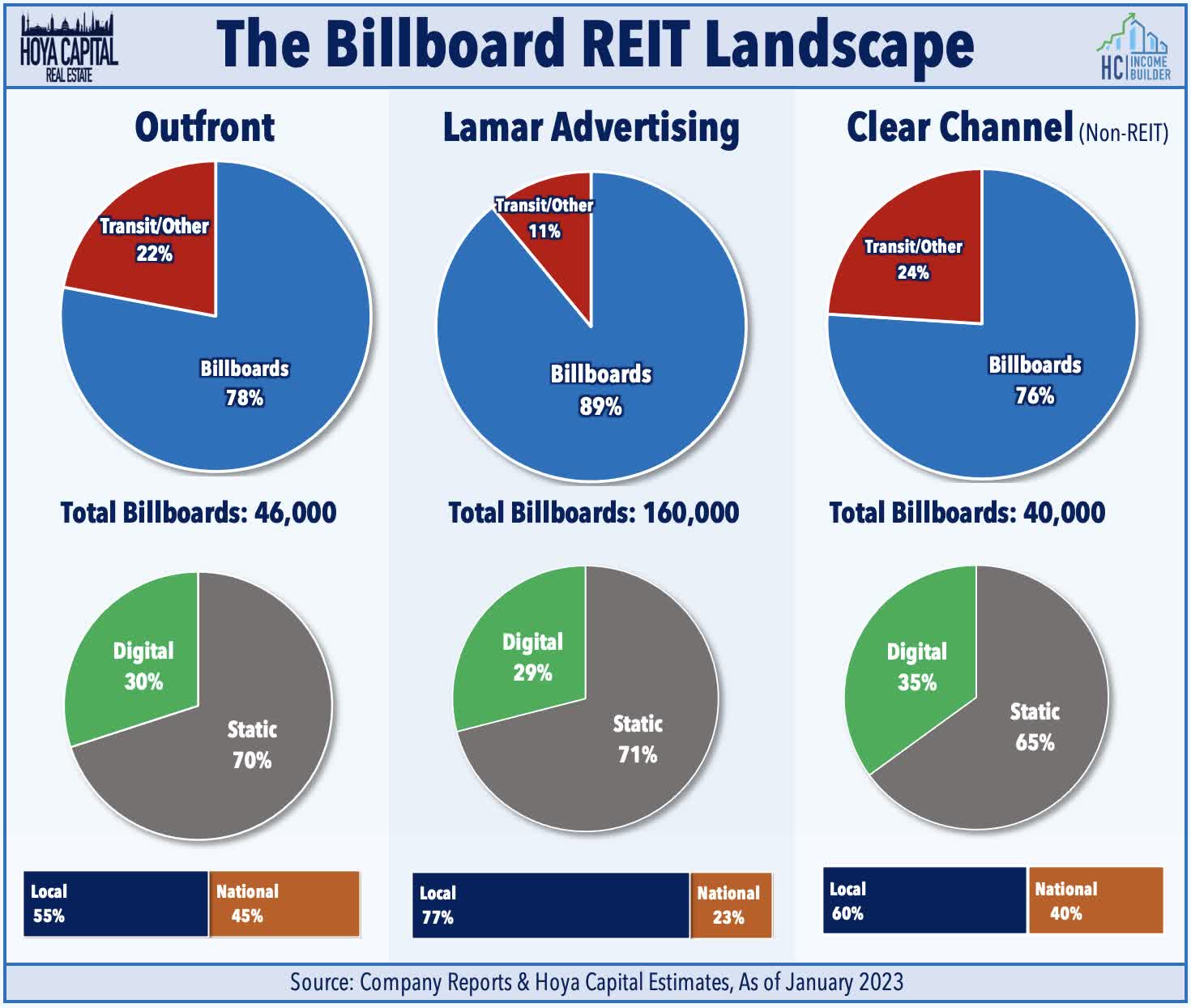

Billboard : Last but not least, Outfront Media ( OUT ) - among the weaker-performing REITs this year - rallied 6% this week after it reached a deal to sell its Canadian billboard business to Bell Media for $299M USD (CAD 410M). Outfront's Canadian business is comprised of 9,325 total billboard and transit displays and generated revenues of $91.9M during full year 2022, representing roughly 5% of Outfront's portfolio. Bell Media - a subsidiary of BCE Inc ( BCE ) - is one of Canada's largest communications companies, owning roughly 50 TV stations and 103 radio stations in Canadian markets, along with the Astral out-of-home ("OOH") advertising network. The all-cash deal is expected to close in 2024, and OUT will presumably use the proceeds to pay down its relatively elevated level of variable-rate debt, which comprises roughly a quarter of OUT's total debt. OUT has dipped nearly 40% since reporting disappointing second-quarter results in which it significantly lowered its full-year outlook and booked a $500M non-cash impairment on its New York MTA transit segment, an ill-timed 15-year deal signed two years before the pandemic that has proven to be a substantial drag on its otherwise solid billboard business.

{kind=link}

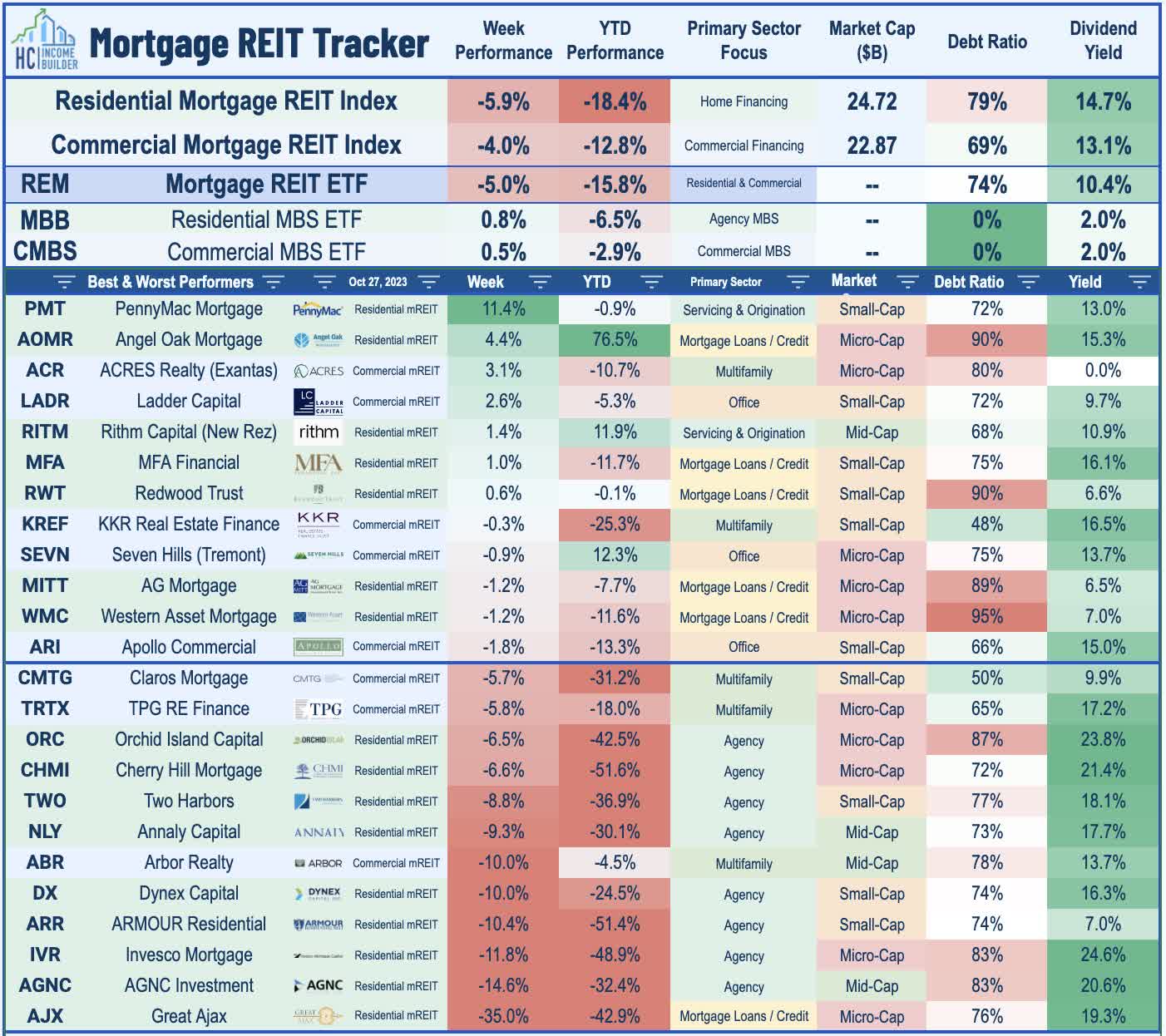

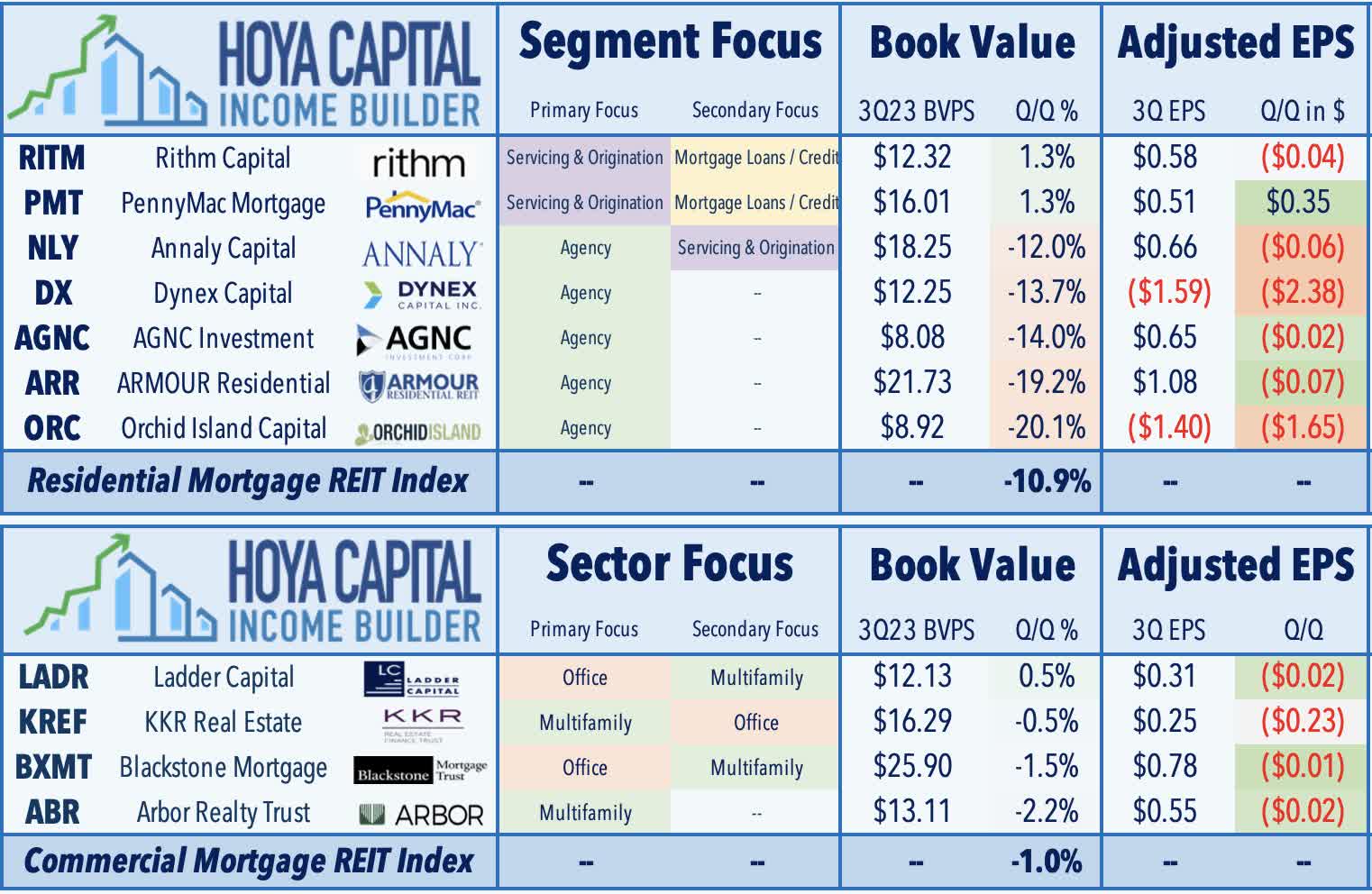

Mortgage REIT Week In Review

Declining in five of the past six weeks, the iShares Mortgage REIT ETF ( REM ) slid another 5% this week as the first wave of earnings results showed that the resurgence in benchmark interest rates resulted in a significant deterioration in book values for some mREITs. On the downside, AGNC Investment ( AGNC ) - a pure-play agency mREIT - dipped 15% after reporting that its tangible Book Value Per Share ("BVPS") dipped 14% in Q3, and estimated that its current BVPS as of last week had dipped another 14-15%. Annaly Capital ( NLY ) - the largest residential mortgage REIT - dipped 9% after reporting that its BVPS dipped 12% in Q3. Armour Residential ( ARR ), meanwhile, reported that its BVPS dipped 19% in Q3, while Orchid Island ( ORC ) reported that its BVPS dipped 20%, and Dynex Capital ( DX ) reported a 14% decline in BVPS. Also among the laggards this week, Great Ajax ( AJX ) plunged 35% after Ellington Financial ( EFC ) called off its deal to acquire AJX, which had initially been announced in July.

{kind=link}

Not all residential mREITs were negatively impacted by the surge in interest rates. PennyMac ( PMT ) - which focuses on the inversely-rate-senstive Mortgage Servicing Rights ("MSR") business - surged 11% this week after reporting very strong results, noting that its BVPS increased by 1.2% in Q3. Fellow services-focused mREIT, Rithm Capital ( RITM ) - which we own in the Focused Income Portfoli o - was also a notable upside standout after it reported that its BVPS increased 1% while recording comparable EPS of $0.58 - far exceeding consensus estimates and easily covering its $0.25/share dividend. Rithm also announced that it again increased its bid to acquire hedge fund Sculptor Capital ( SCU ) to $12.70/share - up 13.9% over Rithm’s original bid of $11.15, a deal that won the approval of the competing shareholder group that had sought to block the earlier agreement.

{kind=link}

Results across the commercial mREIT space were mixed. Ladder Capital ( LADR ) - which focuses on office and residential lending - rallied 3% after reporting that its BVPS increased 0.5%. KKR Real Estate ( KREF ) - which focuses on residential and office lending - was also an outperformer after recording comparable EPS of $0.25 - topping the $0.11 consensus. On the downside, multifamily-focused lender Arbor Realty ( ABR ) dipped 10% after it reported an uptick in delinquency rates, noting that it now has twelve non-performing loans with a carrying value of $137.9M, up from seven loans with a carrying value of $122.4M last quarter. Blackstone Mortgage ( BXMT ) - the largest commercial mortgage REIT - declined 3% after reporting an uptick in delinquency rate on its office loans - which comprise about a third of its portfolio - and noted that it has increased its CECL reserve on its office assets by more than 10X in the past year, implying an average decline of over 50%. Elsewhere, small-cap Sachem Capital ( SACH ) declined 5% after it reduced its dividend by 15%, becoming the second commercial mREIT to lower its dividend this year and 29th REIT overall.

{kind=link}

2023 Performance Recap & 2022 Review

Through ten months of 2023, the Equity REIT Index is now lower by 13.6% on a price return basis for the year (-10.2% on a total return basis), while the Mortgage REIT Index is lower by 13.3% (-7.3% on a total return basis). This compares with the 7.4% gain on the S&P 500 and the 4.0% decline for the S&P Mid-Cap 400 . Within the real estate sector, just one property sector is still in positive territory on the year - Data Center REITs - while Cell Tower, Office, and Specialty REITs have lagged on the downside. At 4.85%, the 10-Year Treasury Yield has surged by 97 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April. Following the worst year for bonds in decades, the Bloomberg US Bond Index is lower again this year, producing total returns of -2.5% thus far. WTI Crude Oil - perhaps the most important inflation input - is higher by 11.8% this year.

{kind=link}

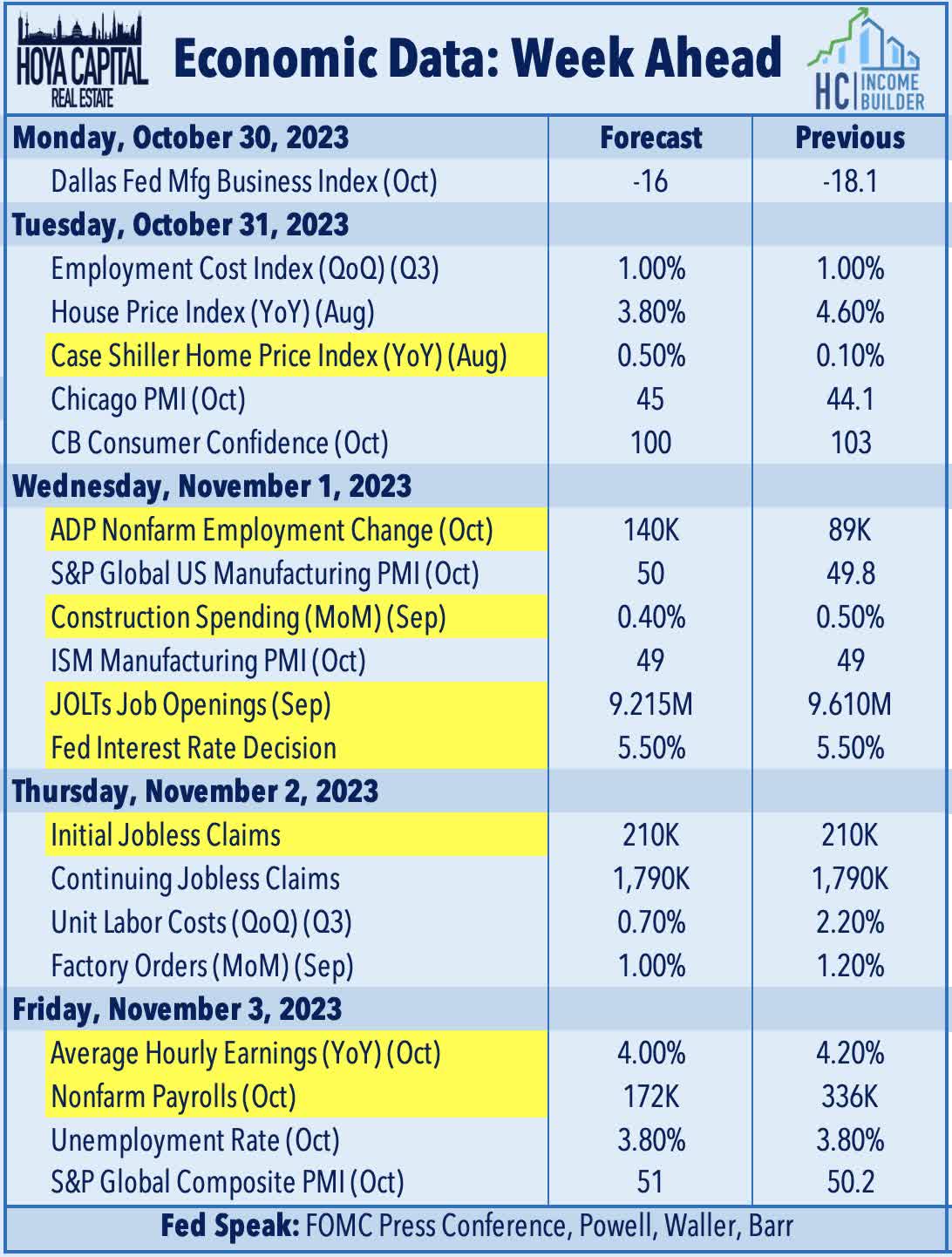

Economic Calendar In The Week Ahead

Central banks are in the spotlight in the week ahead. The Fed's two-day policy meeting concludes with its Interest Rate Decision on Wednesday, and while the Fed is all but certain to maintain the Fed Funds rate at its current 5.50% upper bound in this meeting, the focus will be on the outlook for future rate hikes. Employment data highlights another critical week of economic data in the week ahead, headlined by the JOLTS report on Tuesday, ADP Payrolls data on Wednesday, Jobless Claims data on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 170k in October, which follows a very strong month of September in which the economy added over 300k jobs. The closely-watched Average Hourly Earnings series within the payrolls report - which is the first major inflation print for August - is expected to show a cooldown in wage growth to 4.0%. 'Good news is bad news' will likely remain the theme of these reports as several Fed officials have pinned their decisions to pivot away from aggressive monetary tightening on a long-awaited cooldown in labor markets. We'll also be watching the Case Shiller Home Price Index report on Tuesday, Construction Spending data on Friday, and a flurry of PMI data throughout the week.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Earnings Can't Cure Gloom