ETN - Eaton: Solid Growth Prospects

2023-10-10 05:23:58 ET

Summary

- Eaton Corporation's revenue is expected to benefit from strong order rate and backlog levels, supported by solid end market demand and secular demand drivers.

- The company has seen good growth in revenues post-Covid, driven by organic sales growth and notable sales growth in the Aerospace segment.

- Eaton's margins are expected to improve due to operating leverage and strong pricing, supported by robust demand for its products.

Investment Thesis

Eaton Corporation plc's (ETN) revenue is poised to benefit from strong order rate and backlog levels supported by solid end market demand across its Electrical and Aerospace segments in the near term. In the long run, secular tailwinds from reshoring, investments in grid modernization, ramp up in A-320 and BA-737 programs and government stimulus funding should help revenue growth. The company's margins should benefit from operating leverage as well as strong pricing, considering the robust demand for its products. While the valuation is trading at a premium compared to its historical levels, I believe the stock is a good buy given the potential for upward revision in estimates and exceptionally strong end-market demands which has resulted in a backlog that is multiple times its pre-Covid levels providing a good visibility on revenue growth and margin expansion.

Revenue Analysis and Outlook

The company has seen good growth in revenues post-Covid with strength seen across the business segments. In the second quarter of 2023, the company achieved a solid 12.5% year-over-year (Y/Y) increase in net sales, reaching $5.866 billion. This growth was driven by a 13% Y/Y increase in organic sales, which benefited from robust performance in the end-markets of both the Electrical Americas and Electrical Global business segments. Additionally, there was notable sales growth in both the commercial and military OEM and aftermarket sectors within the Aerospace business segment. Furthermore, pricing adjustments to address inflationary pressures also contributed to the positive results.

ETN's Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, the company is poised to see a good growth in both near as well as long term given its strong backlog as well as megatrends like reshoring and infrastructure spending which should result in good end market demand for the next several years.

The company ended last quarter with a backlog of $9.1 bn for Electrical business and $3 bn for Aerospace business. This is meaningfully higher than pre-COVID levels and the order pace is still strong with a book-to-bill ratio of 1.2x in Q2 2023.

ETN's Backlog Growth (Company's Earnings Presentation)

This strong order book provides a good visibility on the company's future growth not only for the second half of FY23 but also for the next year.

The U.S. industrial projects continue to benefit from the Federal government stimulus under Inflation Reduction Act (IRA) and CHIPS and Science Act and the company's Electrical segment has a good exposure towards these projects which should help Eaton's sales. There has been a significant increase in government credit and incentives under IRA as well as mega project ($1 bn+) announcements in the recent quarters.

IRA Government Spending (Company's Earnings Presentation)

Mega Project announcements (Company's Earnings Presentation)

Now the interesting thing is that it takes some time from a project getting announced and ETN seeing orders from it. Most of these recently announced projects are still in initial stages and as the work on them continues to ramp up, Eaton should see order rate strengthening further from here.

In addition to Federal stimulus, there are also secular drivers which are driving the demand in specific-end markets. For example, increased use of renewables and electric vehicles is driving investments in grid modernization and ensuring enhanced reliability and safety which is helping Eaton's utility business. Also, increased use of artificial intelligence and machine learning is driving investment in data centers resulting in increased demand for Eaton's electrical products.

There are secular long term drivers in Eaton's Aerospace business as well. The increase demand for civilian aircrafts with Airbus ( EADSF ) expected to increase production of A320 from 45 to 50 per month currently to 75 per month by 2026 and Boeing ( BA ) expected to increase production of Boeing-737 from 31 per month currently to 50 per month by 2025-26 is expected to meaningfully increase the sales of Aerospace segment. Further, with geopolitical tension increasing significantly in the recent period, the government spending of defense aircraft should also increase. In addition to end-market demand, the company is also well-positioned to benefit from its increased content per aircraft on the new models. For example, according to management , on Bell V-280 Valor aircraft, which replaces the Black Hawk helicopter, Eaton has five times more content and is actively pursuing additional opportunities through bidding.

Overall, the company is poised to deliver strong growth for the next several years. If we look at the current consensus estimates for revenues, the sell-side is expecting double-digit revenue growth in the current year and mid-single digit growth from next year. However, given the company is still in initial stages of benefiting in surge in demand from trends like reshoring, government stimulus funding, investment in grid modernization and ramp up in A-320 and BA-737 programs, I believe the Y/Y revenue growth can continue to remain in low double-digit even beyond FY23. So, there is a good chance of Eaton beating sell-side and expectations in the coming years.

Margin Analysis and Outlook

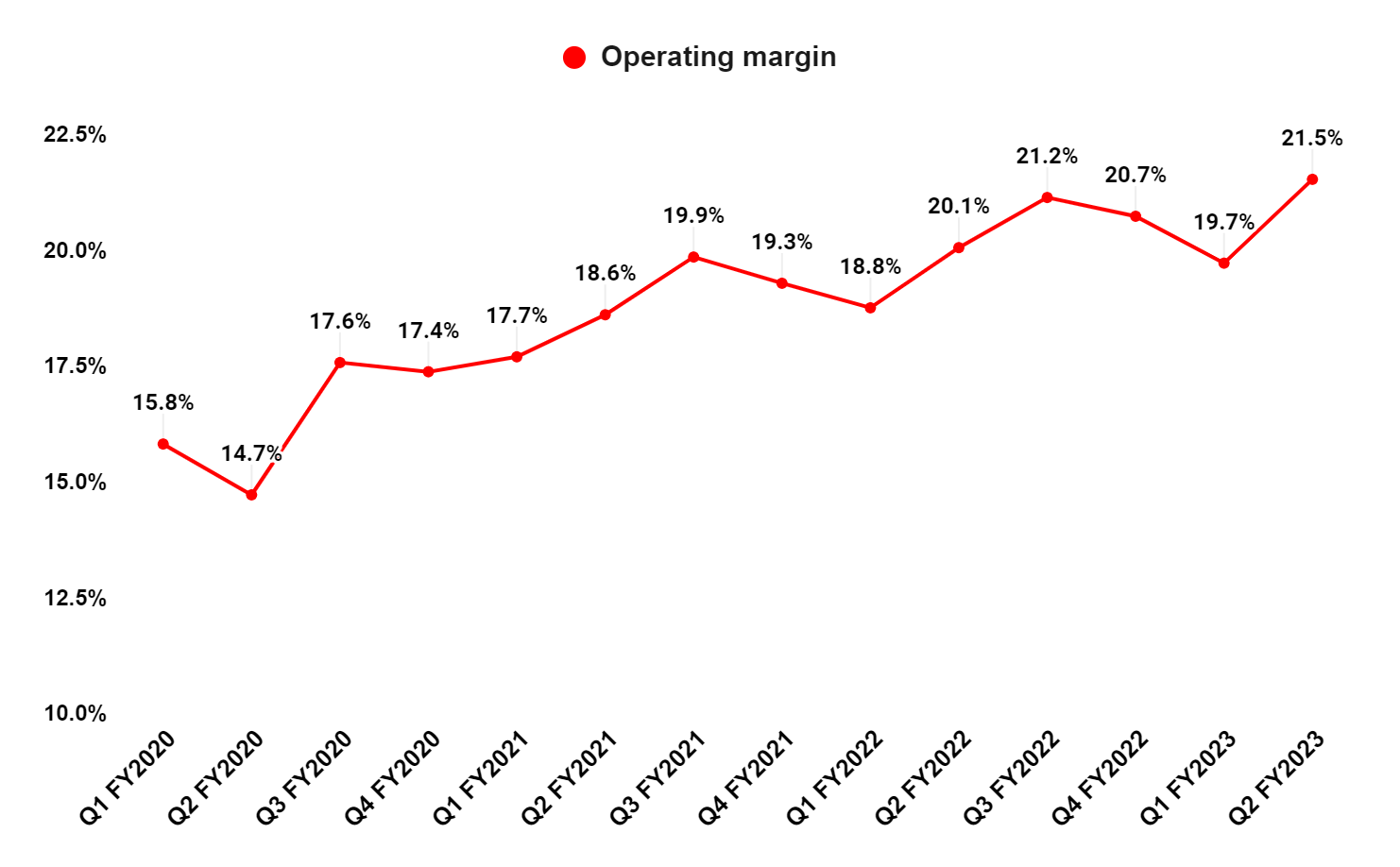

In Q2 2023, the company's total segment operating margin improved by 140 bps YoY to 21.5%, driven by higher sales volumes and pricing increases. These factors more than offset wage and commodity inflation, as well as an unfavorable product mix.

ETN's Operating margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I expect the company's margins to continue improving from the current levels. Last quarter, the company reported incremental margins of 33% and, with good revenue growth prospects, the company should continue to benefit from strong operating leverage. Also, given the extraordinarily strong demand, I expect the company to have good pricing power in the coming years, which should help margins. So, while the company's margins are at record highs, I am optimistic about further margin expansion prospects.

Valuation and Conclusion

ETN's stock is trading at a ~21.67x FY24 EPS estimates of $9.70 which is at a premium compared to its 5-year average forward P/E of 20.35x.

While the valuation is slightly high compared to its historical averages, I like the stock given the company's solid growth prospects, good visibility from strong backlog, and potential to post higher growth compared to what sell-side consensus is currently modeling. Considering the solid growth opportunities driven by secular trends like reshoring, government stimulus funding, investment in grid modernization and ramp-up in A-320 and BA-737 programs, I have a buy rating on the ETN's stock.

Risks

While the Electrical Americas business has good visibility due to significant increase in new project activity, there is some risk in the Electrical Global business if the global industrial market weakens further due to the high interest rate environment. In this case, the revenue should still be up, but may miss my double-digit Y/Y growth forecast. In addition, the company's international exposure can also result in headwinds from adverse FX movements. Further, there is also an execution risk associated with how fast the company can ramp up its production to benefit from increased end-market demand and, in case there are execution issues, the growth may turn out to be lower than my expectations.

For further details see:

Eaton: Solid Growth Prospects