CRSP - Editas Medicine: A Mispriced Contender In The Gene Editing Arena

2023-10-11 11:07:37 ET

Summary

- Editas Medicine specializes in gene editing, targeting a range of serious illnesses, with a unique platform that covers over 95% of the human genome.

- EDIT's collaboration with Bristol-Myers Squibb aims to revolutionize cancer treatments, especially in cancer immunotherapy.

- EDIT faces competition in the gene therapy race for Sickle Cell Disease from Bluebird Bio and CRISPR Therapeutics, with BLUE and CRSP being more advanced in their clinical trials.

- My valuation analysis suggests EDIT is undervalued with a potential upside of approximately 124%, but BLUE and CRSP might be better investment alternatives.

Editor's note: Seeking Alpha is proud to welcome Myriam Alvarez as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Editas Medicine ( EDIT ) stands as a significant contender in gene editing, aiming to address a range of severe diseases through its innovative gene-editing platform. The industry is burgeoning with potential, yet EDIT is trailing behind Bluebird Bio, Inc. ( BLUE ). Nonetheless, given BLUE's ongoing transition into its production phase, there still appears to be ample space in the market for both BLUE and EDIT to coexist and thrive. In this review, I will detail EDIT's strategic direction, ventures into genetic medicine, and financial health. I will also take a closer look at EDIT's endeavors to tackle ocular conditions, Sickle Cell Disease, beta-thalassemia, and solid tumors. It's noteworthy that EDIT's partnership with Bristol Myers Squibb (BMY) represents a pivotal step towards leveraging collective expertise with the potential to redefine cancer therapies. Lastly, my valuation comparison of EDIT's market position will be juxtaposed against BLUE and CRISPR Therapeutics (CRSP). I assign a "Strong Buy" rating on EDIT as I believe the stock is significantly undervalued and has a potential upside of 124%, based on my calculations. That said, when I compare EDIT's market position with that of BLUE and CRISPR, I conclude that although EDIT might be undervalued, BLUE and CRSP could present more compelling opportunities for those looking to invest in gene editing.

Editas Overview

Editas Medicine ((EDIT)), formerly Gengine, specializes in gene editing and is creating potentially groundbreaking gene editing treatments for various serious illnesses. Their unique gene editing platform enables gene editing for over 95% of the human genome. EDIT holds exclusive licensing rights for the Cas9 and Cas12a patent estates from the Broad Institute and Harvard University, specifically for human medicinal applications.

Revenue streams are primarily pinned on developing and commercializing in vivo and ex vivo gene-edited and cellular therapy medicines. EDIT-101 is in a phase 1/2 clinical trial for treating blindness due to Leber Congenital Amaurosis 10 (LCA10, a CEP290-related retinal degenerative disorder). The results show safety and efficacy data from 14 patients (12 adults and two pediatric patients). Unfortunately, these trials have been paused due to the high price of the treatment and the limited number of patients.

Branching into cellular therapy, especially with engineered NK cells targeting solid tumors, showcases EDIT's broader vision, given the grave impact of over 1.6 million new solid tumor cases annually in the U.S. EDIT-202's preclinical success in ovarian cancer models hints at potential new cancer treatment modalities, reflecting a diversified approach to combatting cancer beyond just ex vivo realms. Furthermore, the alliance with BMS in optimizing engineered alpha-beta T cell therapies is a collaborative stride towards expanding the horizon of treatable cancers. I believe this collaboration melds the expertise of two formidable entities aiming to push the envelope in cancer therapy. The ongoing programs targeting a range of tumor types, including HPV-associated tumors, underscore the extensive potential of gene editing in revolutionizing cancer immunotherapy.

Heating Gene Therapy Race for Sickle Cell Disease

Another costly ex vivo gene-edited cell treatment targets the severe and prevalent inherited blood diseases beta-thalassemia and Sickle Cell Disease ((SCD)), with a key program entering Phase 1/2 clinical trials for treatment. EDIT-301 possibly cures these diseases, but it has a long road ahead, with an expected finish date in August 2025 . After that, phase 3 still would take approximately two years before the candidate is approved and starts commercialization. EDIT's main competitors in the race to commercialize gene therapy for SCD are Bluebird Bio and CRISPR Therapeutics.

CRISPR's exa-cel program could treat beta-thalassemia and SCD, and it is in phase 3. The Food and Drug Administration (FDA) is set to decide on the approval of exa-cell treatment for SCD in early December. Furthermore, a decision on approval for beta-thalassemia is anticipated to be made by the FDA in the first quarter of 2024.

Bluebird launched Zynteglo , a one-time cure therapy for beta-thalassemia, in August 2022. However, it is limited as it can only be administered to 1,300 to 1,500 patients, leaving room for CRISPR's treatment in the market. Bluebird's gene therapy for Sickle Cell Disease ((SCD)), lovo-cel, is slated for FDA review in late December.

Therefore, Editas is a little behind in this specific race. However, the demand from patients requiring treatment outstrips the supply capacity of competitors to produce the medicine. This situation creates an opportunity for EDIT to cater to the unmet needs of those patients still requiring therapy.

EDIT's Corporate Presentation

EDIT is carving a niche in the expansive domain of genetic medicine. Their ventures reflect innovation, strategic collaboration, and a diversified approach to addressing genetic disorders and cancers. Each endeavor, tackling ocular conditions, SCD, beta-thalassemia, and solid tumors, embodies a step towards a future where the enigma of genetic diseases could be unraveled and rectified. The collaboration with BMS amplifies the potential achievements in cancer immunotherapy. However, these therapies' long-term success and translational efficacy from bench to bedside remain to be observed.

EDIT-301 trials data update, June 2023

Portfolio Valuation and Comparison

A deep dive into EDIT's financials paints an intriguing picture of its fiscal trajectory within the dynamic biotech sector. By mid-2023, the firm's liquidity surged to $220.8 million, up from $141.5 million at 2022's close. This uptick could be attributed to savvy fundraising efforts or judicious cash flow management. Such financial resilience underscores EDIT's strategic prowess and investment appeal. Yet, it's juxtaposed with a widening deficit , ballooning from $1.08 billion to $1.17 billion in a mere half-year. This underscores the inherent volatility and challenges in the biotech arena.

Moreover, a notable shift is the reduction in R&D expenditures, dropping year-on-year from $81.6 million to $67.6 million. On the surface, this might be perceived as a strategic cost containment. However, for a trailblazer like EDIT, where groundbreaking innovation is at its core, curbing R&D could potentially hamper forward momentum. Striking the right equilibrium between fiscal prudence and relentless innovation becomes imperative for EDIT, especially in light of its reported net loss of $89.3 million during the first six months of 2023.

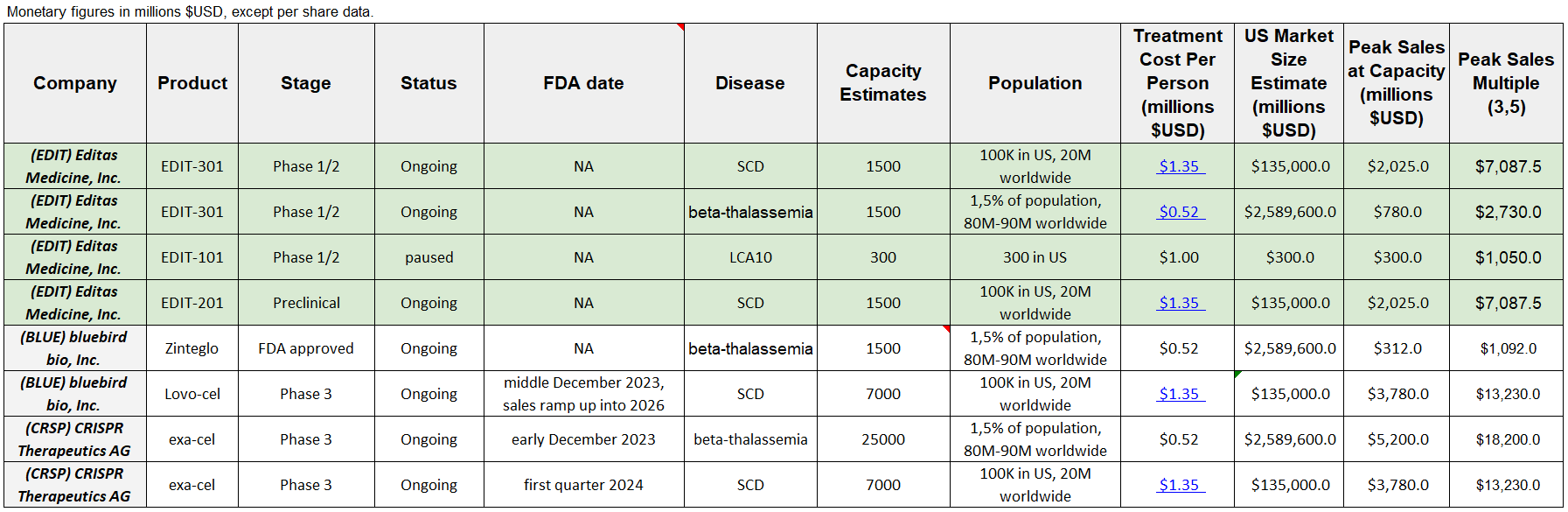

Table 1. (Author's elaboration and public company data)

{kind=link}

Indeed, EDIT is in a complex financial situation, yet the FDA's Orphan Drug Designation for EDIT-301 stands out as a significant milestone. This designation validates EDIT's research and suggests a quicker route to commercialization. However, it's crucial to approach this with a balanced perspective. While the potential of EDIT-301 is promising, its success hinges on continuous positive clinical outcomes, especially given the stringent FDA approval processes. Financially, EDIT faces challenges, but its robust liquidity could be its strategic advantage. This financial buffer might allow EDIT to navigate the costly drug development phase and transition to commercialization. The market sentiment, underscored by Stifel's upgrade from Hold to Buy, indicates growing confidence in EDIT. This suggests that investors might be underestimating EDIT-301's potential, which could become more apparent as further clinical data emerges and FDA approval draws nearer.

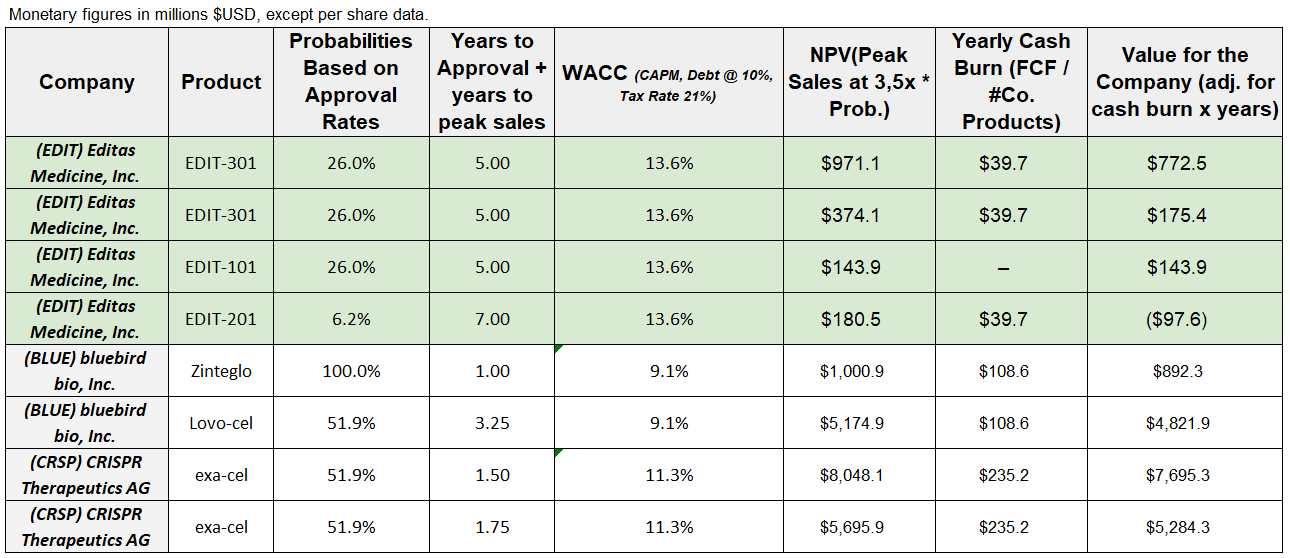

Table 2. (Author's elaboration and public company data)

{kind=link}

Using a peak sales ratio of 3.5, commonly applied to early biotech products, and considering the implied yearly cash burn for EDIT , BLUE , and CRSP , we can attempt to gauge the value of each product for these companies. EDIT-201 has a negative value for Editas because of the implied necessary investments over time and the long time until it gets a possible FDA approval, along with its associated low probability. I believe BLUE will likely expand its patient base for the Lovo-cel treatment by 2025-2026. Drawing from Bluebird's earnings call, they've pinpointed over 20,000 U.S. individuals as potential candidates for gene therapy for severe sickle cell disease. Their research indicates that 70% of these individuals, amounting to 14,000, might opt for the treatment. If Lovo-cel manages to secure a conservative 50% of the market, this could mean a reach of around 7,000 patients. However, I believe this number is an optimistic ceiling, given the challenges tied to operational capacity and the scaling of their qualified treatment centers (QTCs). On the other hand, I infer that CRSP might penetrate the market faster, given its more extensive scale and capacity.

Stock Valuation Process

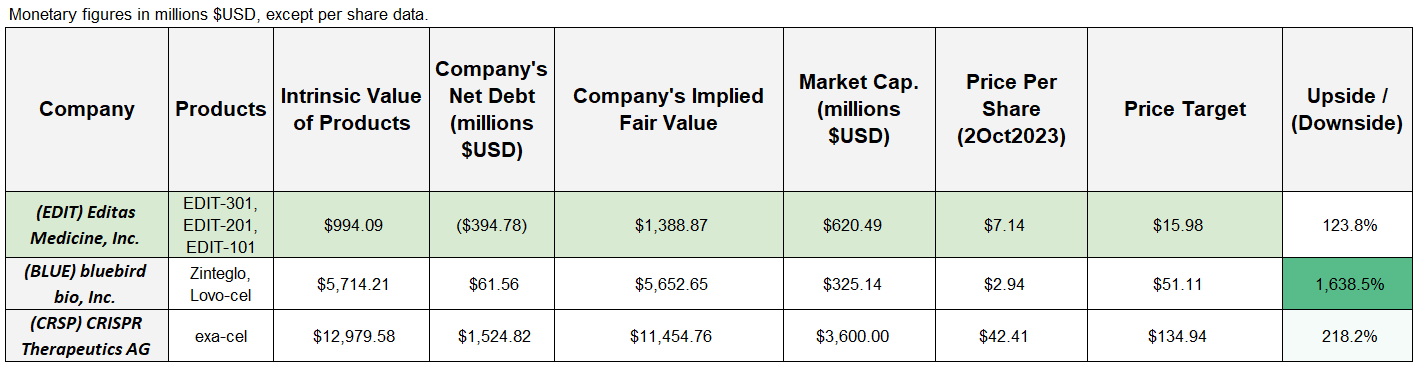

The valuation summary below (Table 3) presents the combined intrinsic value of EDIT's products, which represents the potential future worth of EDIT's portfolio. I then adjust this value by the EDIT's net debt, resulting in the company's implied fair value. This fair value indicates the company's worth based on its product lineup and financials. The upside is calculated as the difference between the current market cap and my fair value estimate, and that percentage upside is then used to estimate the price target.

Table 3. (Author's elaboration and public company data)

{kind=link}

Earlier, Table 2 delved deeper into EDIT's products' valuation metrics. Each product's value is first gauged by its approval probability, indicating the likelihood of it reaching the market. This potential value is then adjusted for the time it'll reasonably take for the product to gain approval and reach its peak sales, which I then discounted at the implied Weighted Average Cost of Capital (WACC). Table 2 also calculates the net present value at peak sales, incorporating the approval probability, and adjusts the product's value for the company's yearly cash expenditures. I estimate the peak sales with a conservative multiple of 3.5, the approval probability based on historical approval rates depending on each phase, and the cash expenditures based on each EDIT's current negative FCF run rates.

Lastly, Table 1 provides a detailed overview of each product's development status and market potential. It outlines the current development phase, my projected FDA approval dates, the targeted diseases, and my estimated treatment costs. When integrated with the data from Table 2, this information forms the overall company valuation shown in Table 3, which determines EDIT's price target. While I've made certain estimates, such as approval timelines and treatment costs, I believe they are reasonable. I encourage you to refer to the respective tables and adjust your viewpoint if necessary. In essence, my valuation for EDIT combines the product pipeline's potential, the financial implications of market entry, and the anticipated market size and revenue for each product. This valuation methodology is also applied to BLUE and CRSP to provide a comprehensive perspective.

Note that, in my analysis, I estimate EDIT's capacity could be approximately 1,500 patients, aligning with BLUE's Zynteglo. This estimation is conservative, serving as a foundational figure for my model. Then, I discounted each company's potential revenues at their respective WACCs. The data suggests that EDIT might be undervalued, pointing to a price target of $14.82 per share. This presents a potential upside of approximately 124%, consistent with Stiefel's price target of $17.00 per share. Thus, I believe EDIT is mispriced at its current levels, given these assumptions.

However, my valuation suggests BLUE and CRSP present even greater value. BLUE's advanced stage compared to EDIT heightens its prospects for success, elevating its anticipated value. On the other hand, CRSP's broader scope and potential for diverse applications strengthen its valuation. While EDIT is attractive in valuation, BLUE and CRSP could be even more promising investment opportunities using the same logic. Yet, within the gene-editing portfolio, EDIT stands out as a good "Strong Buy" at its current levels, considering its positioning in the sector.

Inherent Risks

Editas Medicine shows promise in the gene-editing sector. However, its growth trajectory is subject to multiple variables. Regulatory bodies, notably the FDA, maintain rigorous approval standards. Any unforeseen challenges in EDIT's clinical trials could result in delays or rejections. Drug development typically spans extended periods, and treatments like EDIT-301 might take years to realize significant revenue. This could lead to a greater cash expenditure than initially projected. Even if operations proceed without issues for Editas, they will likely require further financing to bolster R&D or expand production capabilities. The company's current cash runway is projected to last until the second half of 2025, so EDIT shareholders might experience further dilution . Conversely, suppose the company opts to issue debt instead. Given the prevailing high interest rate environment and the speculative nature of the company's operations, it's likely to come with a steep interest rate.

Moreover, competitors like Bluebird Bio and CRISPR Therapeutics, who are making swift progress, indicate that EDIT could face challenges in securing a significant market share. This belief is because, in fast-evolving sectors, companies that innovate slowly can quickly find themselves overshadowed by more agile competitors. My analysis suggests that the market is big enough for all three companies, but readers need to know that EDIT's market share is not guaranteed.

Lastly, operational challenges in increasing production, changes in scientific methods, and potential legal disputes over patents are some factors that make EDIT's path complex. The gene-editing sector is in a state of flux, and it's possible that new technologies could arise that challenge EDIT's existing platform and ongoing research. While the potential rewards in this field are significant, the risks are equally substantial. This is why the best approach is likely to add EDIT, BLUE, and CRSP together so that investors get a diversified approach to the gene editing sector.

Final Reflections and Investment Implications

Editas Medicine has made significant strides in addressing genetic disorders, from vision-related conditions to Sickle Cell Disease. Their strategic alliance with Bristol-Myers Squibb underscores a deliberate move aiming to revolutionize oncology treatments by tapping into the collective prowess of both entities. From an investment perspective, EDIT's market positioning appears to undervalue its inherent worth, hinting at a potential growth opportunity for astute investors and a possible upside of roughly 124%.

However, EDIT doesn't quite lead the pack when placed alongside industry stalwarts like Bluebird Bio and CRISPR Therapeutics. While this assessment is centered on EDIT, it's essential to understand that BLUE and CRSP are included merely as comparative benchmarks, not as primary subjects. Given the investment landscape and the potential of gene editing, diversifying one's portfolio across these three players might pave the way for a harmonized risk-reward dynamic. In summation, EDIT's foray into gene editing presents a compelling investment narrative, with the prospect of delivering substantial value in the long run for enterprising investors.

For further details see:

Editas Medicine: A Mispriced Contender In The Gene Editing Arena