ELV - eHealth: Small Caps Are (Super) Inefficient

2023-11-16 05:48:20 ET

Summary

- eHealth, Inc. shares have been stuck in a trading channel between $7 and $10 despite positive Q3 results and encouraging leading indicators for the 2023 AEP.

- The company's business model checks many boxes for value investors in the small cap patch, including more favorable industry conditions and a highly attractive current valuation.

- The company's commissions receivable appear money good and EHTH's book value is about $18.77 vs. a current stock price of about $8.

This is an update article, as I've originally wrote on the name, back on March 9, 2023 . For historical context and industry background, please reference that article.

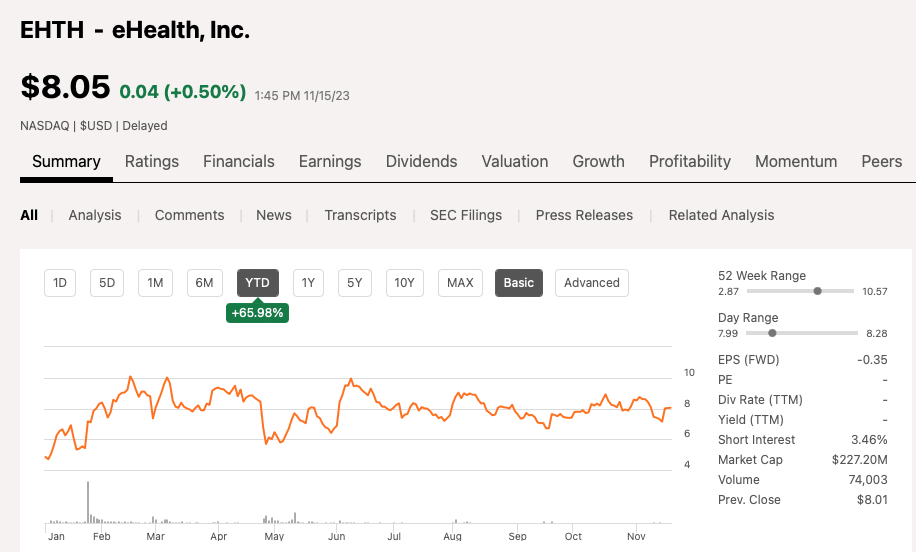

eHealth, Inc. (EHTH) is a core name I've owned throughout most of 2023. It appeared on my radar, back on January 24, 2023, when the company pre-announced markedly better than expected Q4 FY 2022 results. Since that nice leg up, off a very low baseline, the stock has been stuck in a trading channel. And notwithstanding a questionable sell side downgrade, in late April 2023, ahead of its Q1 FY 2023 results, where the stock briefly traded under $5, the channel has been mostly between $7 and $10 per share.

{kind=link}

Last week, November 8, 2023, EHTH delivered another solid Q3 and its management team held a fantastic and in depth conference call. The conference call was full of highly encouraging leading indicators, yet the algos don't seem to be able to synthesize qualitative data very well. To the end, in today's piece, I write to share an update piece, as the market seems completely asleep at the wheel here. My only logical explanation is small caps, notably companies with sub $300 million market capitalizations, tend is (super) inefficient.

The Thesis, Simply Stated

What I love about eHealth is that its checks many of the boxes when it comes to questing for value, in the small cap patch. The business and industry is moving from 'really terrible' to 'ok', the company is somewhat complicated to understand, and the starting valuation is very low when you consider the quality and strong book value relatively to its current stock price (approximately $18.77 of book value vs. an $8 current stock price). The other element that I really love here is there appears to be very compelling qualitative evidence the business is positioned to do really well during the 2023 AEP (October 15th - December 31, 2023). However, the way markets are geared, the algos can't seem to synthesize qualitative information very well, so unless/ until EHTH pre-announces better than expected Q4 results, perhaps in late January 2024, similar to last year, the algos don't appear to be pricing or on the scent of any of the positive leading indicators discussed on the Q3 call and contained within today's write up.

In this piece, my goal is to write a streamlined version of the thesis.

eHealth is an online private health insurance marketplace. The company sells health insurance plans, mostly Medicare Advantage (or other Medicare) plans, on behalf of the national carriers. The plans can be super complicated and nuanced depending on the plan type and features, and inclusive of different state and local market dynamics / policies. EHTH isn't taking any credit risks on the underlying performance of the plans, as that is borne by the insurance carriers (think UnitedHealth Group ( UNH ), Aetna ( CVS ), Elevance Health, Inc. ( ELV ) formally Anthem, Humana Inc. ( HUM ), Centene Corp ( CNC ), and The Cigna Group ( CI )).

The simplest way to think about this business is CAC, LTV, and persistence. CAC stands for customer acquisition cost, LTV stands for lifetime value, and persistence is a fancier word for churn.

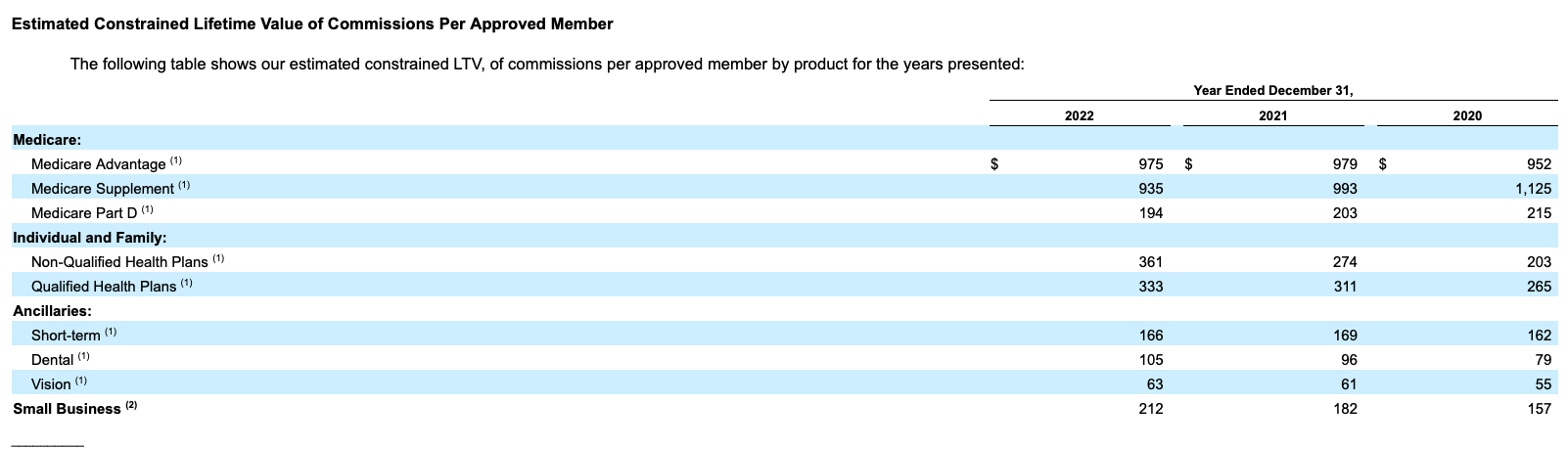

If you look at EHTH's FY 2022 10-K, we see the following:

Medicare CAC was $888 in 2022.

{kind=link}

And EHTH's LTV for Medicare Advantage and Medicare Supplement were $975 and $935, respectively.

{kind=link}

Generally speaking, and I'm just sharing directionally numbers (I'm not intending to be overly precise) the first year commission paid for a new Medicare Advantage enrollee is about $650 to $675 (and it varies by state). In the ensuing renewal years, they are paid out at a rate of about $375 to $400 per year (again, varying slightly by state).

So if you think about this business, as of FY 2022 and in the aggregate, it costs EHTH $888 upfront in the all in CAC and EHTH's LTV was about $975 (inclusive of all the different cohorts, on a portfolio level basis). So that spread, of call it $100, as of FY 2022, multiplied by roughly 600K members is the earnings power.

However, from late 2020 - early 2022, in the era of zero percent interest rates, back in days yore, when the stock market was euphoric and paying up for growth and ignoring profits, there was way too much capacity and CAC dollars chasing growth in this space. The reason was that investors were rewarding growth, in the form of higher stock prices. This led to very aggressive marketing tactics, lots of complaints by seniors, lower quality ratings and more regulation. Moreover, it led to massive operating losses by the entire industry.

Amidst the sharp peaks and valley of the cycle, from boom to bust, EHTH's board fired its former CEO and named Fran Soistman as it new CEO. I would argue that Mr. Soistman, a former CVS executive, has systematically rebuild the entire organization. To visualize it, think about taking a house down to the studs and then completely rebuilding it. Moreover, when something can't continue in its current state, i.e. the massive industry operating losses, it doesn't. The entire industry was forced to get religion. This means focusing on quality, profitability, disciplined CAC, and blocking and tackling. Because this business is highly complex, regulated, and the current daylight between the CAC and LTV isn't that attractive, a lot of capacity has left the market.

See Fran's commentary from last week's Q3 FY 2023 (November 8, 2023) conference call :

With respect to the Medicare distribution sector, we see the competitive environment as favorable. Throughout the past 12 months, we have observed exits and financial distress leading to bankruptcies, reorganization, and divestitures, along with capacity reductions from several of our competitors.

And we will likely see more as new Medicare marketing regulations put strain on industry players that are not able to adjust their practices timely and cost effectively. Additionally, in the current financial environment, it's increasingly difficult for small private organizations to access capital. As brokers adapt to the changing environment, they are increasingly focused on profitability and enrollment quality as opposed to growth at all costs. We believe this is a major positive for the industry.

At the same time, we are seeing limited innovation in the sector in terms of consumer facing technology tools and omnichannel capabilities. In addition, telebroker industry marketing messaging remains largely generic. This sets eHealth apart as we see ourselves as the strongest true omnichannel platform with a distinct brand. This creates an opportunity for us to build deeper relationships with consumers and carriers.

As you can see directly above, Fran captured it very nicely.

The Other Key Nuance - ASC 606

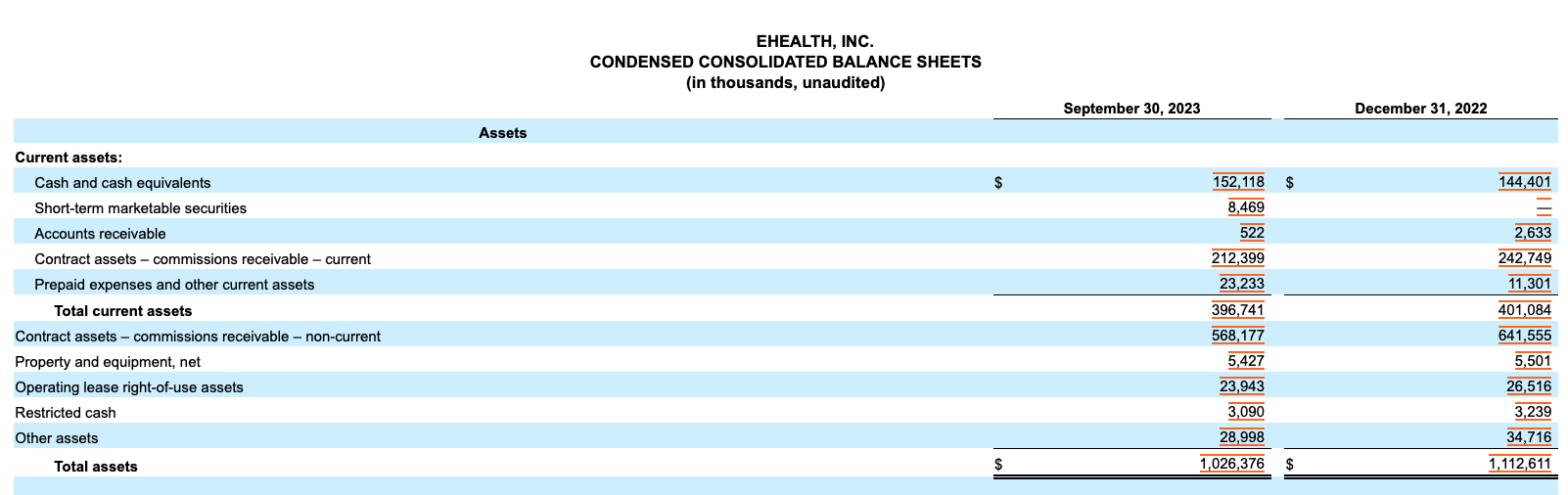

If you look at EHTH's balance sheet, please note the following:

$160.5 million of cash, current commissions receivable of $212.4 million, and longer term commissions receivable of $568.2 million.

{kind=link}

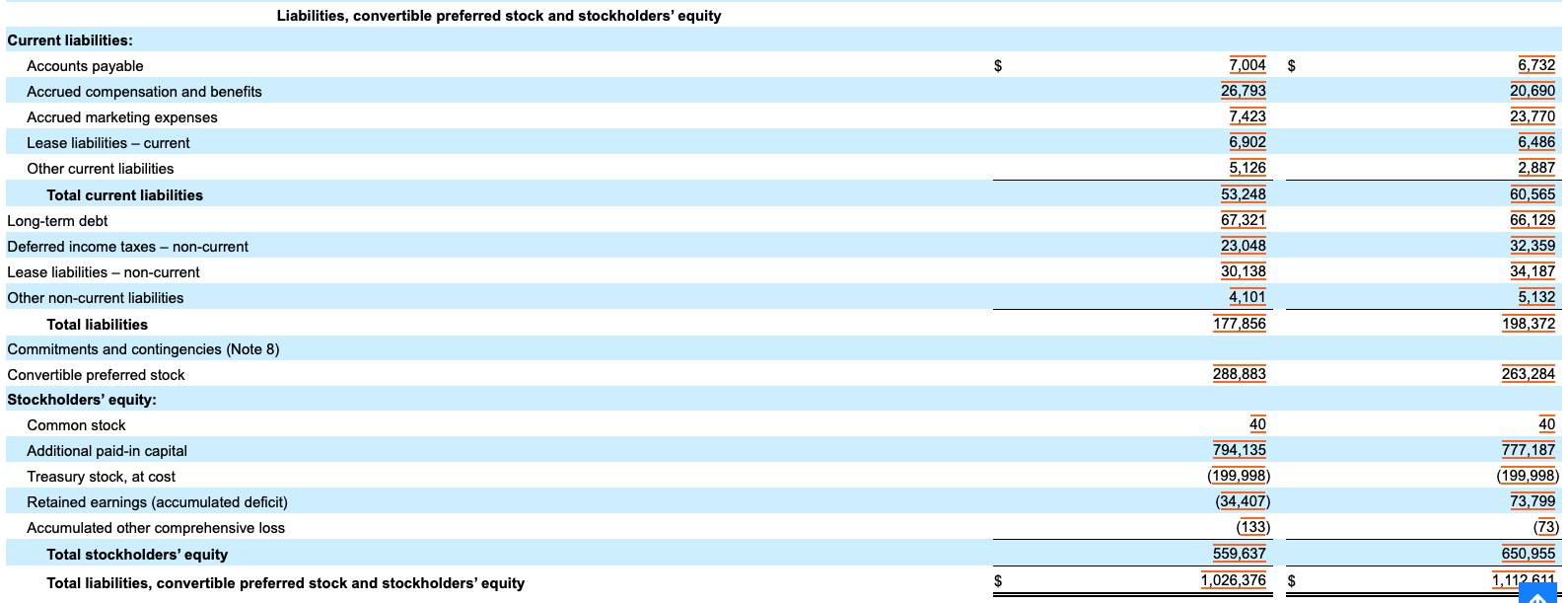

On the liability side, EHTH has $288.8 million in a busted convertible that has an 8% coupon and that has been PIK status. As of April 30, 2023, the annual interest expense is now 6% paid in kind and 2% paid in cash. However, if there was a change of control, there is a provision in the convertible that the preferred has to get taken out at 130% of par. Admittedly, this is a big poison pill. In addition, EHTH has $67.3 million on its credit line at quarter end Q3 FY 2023.

{kind=link}

So if we add up cash, and the near term and longer term commissions receivable, we arrive at $941 million. Then we have $289 million in convertible preferred debt and $67.3 million of net, or $356.3 million. The difference between the major assets and liabilities is $585 million. Next, we need to reduce that value by about $50 million, to capture other liabilities, and you get about $535 million of balance sheet book value. $535 million / 28.5 million shares equals $18.77 vs. a current price of about $8 per share.

In other words, Mr. Market is saying "we don't believe the value of the commissions receivable" or that they think the on-going business has negative $10.77 per share of value.

Yet, if anyone has actually been paying attention here, or even if they simply listened to last Wednesday night's call, they would quickly workout that since ASC 606 was instated, EHTH has had $186 million in positive tail revenue releases, since 2018!

Our Q3 results include positive tail revenue of 12.2 million. eHealth's cumulative net favorable revenue adjustments 2018, when ASC 606 was initially implemented, is now up to 186 million. I can't emphasize the importance of this metric enough.

(Source: EHTH's Q3 FY 2023 Conference Call)

So unlike some of the other players in the space, whom had negative ASC 606 adjustments (they overstated the value of their commissions receivables), this more or less proves that EHTH's underwriting and actuarial assumptions, so to speak, are more conservative!!

This is in contrast with other industry players that have gone through substantial commission receivable impairments over the past 2 years. Our consistently positive net adjustment revenue could be interpreted as conservatism within eHealth's initial revenue estimates and that is a fair observation given our recent results. While we continue to work on refining our initial revenue estimates, eHealth believes investors are better served with the conservative posture eHealth has employed.

(Source: EHTH's Q3 FY 2023 Conference Call)

Lastly, qualitatively, EHTH's business has never looked better and stronger, in terms of its go-to-market strategy and the quality of the product it is putting out on the field. In fact, on October 10, 2023, and I would argue as a show of its confidence, EHTH made the unusual step of issuing a press release ' Highlighting Key Milestones and Achievements ' reached ahead of the 2023 AEP.

Let me synthesize and explain:

I would argue Fran understands that to win in this business, you need to do the following: have the highest quality interactions with customers (whether that be online, via the telephone agents, or a hybrid of online with telephone assistance). The highest possible quality, with the most knowledgeable and reputable agents, that have the right incentives to focus on quality, should ultimately translate into lower future churn and its Medicare quality ratings should remain or trend higher. The big health care insurance companies want high quality metrics and happy customers.

Secondly, as mentioned in the October 10, 2023 press release, EHTH's management has invested aggressively on both the technology and people sides of its business, with the goal of demystify the process, making it less painful, and to help seniors get the best curated plans, for their specific needs.

As referenced, in the October 10, 2023 press release, eHealth created a well-crafted new ad spot , that was rolled out in anticipation of the AEP (which kicked off on October 15, 2023).

Enclosed below are a few more excerpts from the Q3 FY 2023 conference call:

Our Q3 results also reflect important investments in support of our Medicare annual enrollment period objectives, including the successful scaling of our telesales organization. This included the expansion of our national and local market teams of licensed agents or benefit advisors, as well as the addition of customer care specialists as part of our ongoing commitment to enrollment quality and superior member experience that leads to improved customer persistency. We also ramped our advisor force supporting our dedicated carrier arrangements.

During the quarter, we finalized our preparations for the AEP across all key areas of our organization entering Q4 in a strong position to deliver on our financial and operational goals. Importantly, the organization is now significantly more agile than we have been in prior enrollment seasons, allowing us to course correct as we go, leaning into channels and markets that are outperforming expectations, while shifting spend out of underperforming areas.

(Source: EHTH's Q3 FY 2023 Conference Call)

And taking a step back, this industry has very favorable demographics for another five to seven years, in terms of the number of new and eligible people that qualify for Medicare. based on their age. Moreover, there is CBO data that Medicare Advantage plans are performing well.

Before discussing operational developments during the third quarter, I'll first offer some comments on dynamics we are observing within the Medicare market. First and foremost, the Medicare Advantage market remains as attractive as ever, aided by demographic trends, bipartisan support for the program, a significant value proposition relative to traditional Medicare, and robust plan selection offered by carriers.

The Congressional Budget Office, the CBO, projects that the share of all Medicare beneficiaries enrolled in Medicare Advantage plans will rise from the current levels of 51% to 62% by 2033. Looking ahead to 2024, health plans continue to feature core and supplemental benefits that seniors find attractive, including zero-dollar premiums and added value services.

(Source: EHTH's Q3 FY 2023 Conference Call)

Putting It All Together

The serious money can be made when you buy a what was formerly a 'terrible' business/ industry and that morphs into an 'ok' business / industry. The reason is expectations and valuations tend to be low, driven by recency bias and negative perceptions. In the case of EHTH, the company has made significant investments in its technology and hired telephone agents. These agents have been hired and trained in advanced of the AEP, so agents could get up to speed and find their sea legs before the higher stakes and more robust call volumes of AEP kicked off, back on October 15 2023. Moreover, the company has invested in its technology and hybrid offerings with the express goals of making the shopping experience better and easier for seniors. The focus of the organization has moved to quality and higher persistency (lower churn).

Further, as the medicare rules and regulations are complex, and tend to change each year, and this is a capital intensive business, as the CAC need to be spent first and the pay-off in the term of LTV are spaced out in lump sum payments, one year at a time, notwithstanding churn. Said differently, the breakeven payback period, from CAC to LTV isn't until late in second half of year two. In addition, investors need to consider the expensive cost of capital, and then they might quickly understand why capacity has left the market. Over the course of the cycle, at this stage, this should significantly benefit EHTH as there is more market share up for grabs and this creates favorable conditions for continued increases in LTVs, as churn lessens. Lastly, this industry has very favorable demographics for at least another five years. And oh yeah, did I mentioned that EHTH's book value is about $18.77 compared to a current stock price of $8?

In closing, I hope this provides readers with additional context and helps them in their overall research process of eHealth, Inc.

For further details see:

eHealth: Small Caps Are (Super) Inefficient