ELAN - Elanco 2022 Earnings: Speculative Value With Signs Of Progress

Summary

- Elanco Animal Health, an Eli Lilly spin-off, is the second-largest pure-play in the industry.

- On February 21, Elanco reported another largely disappointing year of restructuring, reorganization and poor financial performance, but there are a few signs of progress and improvement.

- For value investors with a 3 to 5-year time horizon, Elanco provides a speculative transformation play with a possible 30% to 40% upside.

On February 21, Elanco ( ELAN ) reported another largely disappointing year of restructuring, reorganization, and poor financial performance, but there are a few signs of progress and improvement.

As a prelude, let's first consider a quote from Charlie Munger about the use of EBITDA in financial reporting:

I think that, every time you see the word EBITDA, you should substitute the word 'bullshit' earnings.

And here's Warren Buffett on "adjusted earnings:"

Too many managements - and the number seems to grow every year - are looking for any means to report, and indeed feature, "adjusted earnings" that are higher than their company's GAAP earnings. There are many ways for practitioners to perform this legerdemain. Two of their favorites are the omission of "restructuring costs" and "stock-based compensation" as expenses.

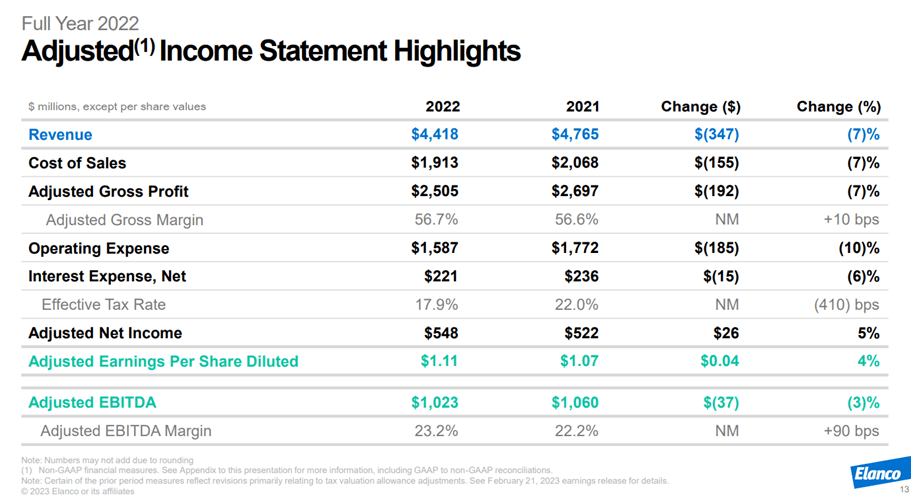

When we review slides from Elanco 2022 Fourth Quarter and Full Year Investor Presentation , there will be heavy emphasis on adjusted numbers - especially adjusted EBITDA. In fact, Wall Street analysts are estimating adjusted numbers, not GAAP, to the point where a cursory reading of some reports of Elanco's 2022 results would indicate the company was actually profitable.

What's really going on at the second-largest pure-play animal health business?

Elanco Animal Health Financial Results: 2021 vs. 2022

For 2022's fourth quarter and full year, Elanco - as it has done for every quarter and year for several years - presented investors with two complete versions of its financial performance. Here's management's preferred version:

Elanco 2022 Fourth Quarter and Full Year Investor Presentation

{kind=link}

In this version, Elanco reported adjusted net income of $548.0 million, a $26.0 million or 5.0% increase from $522.0 million in 2021. Adjusted EPS increased to $1.11 per share, 4% higher than $1.07 per share in 2021. I can only imagine the comments of Mr. Munger and Mr. Buffett.

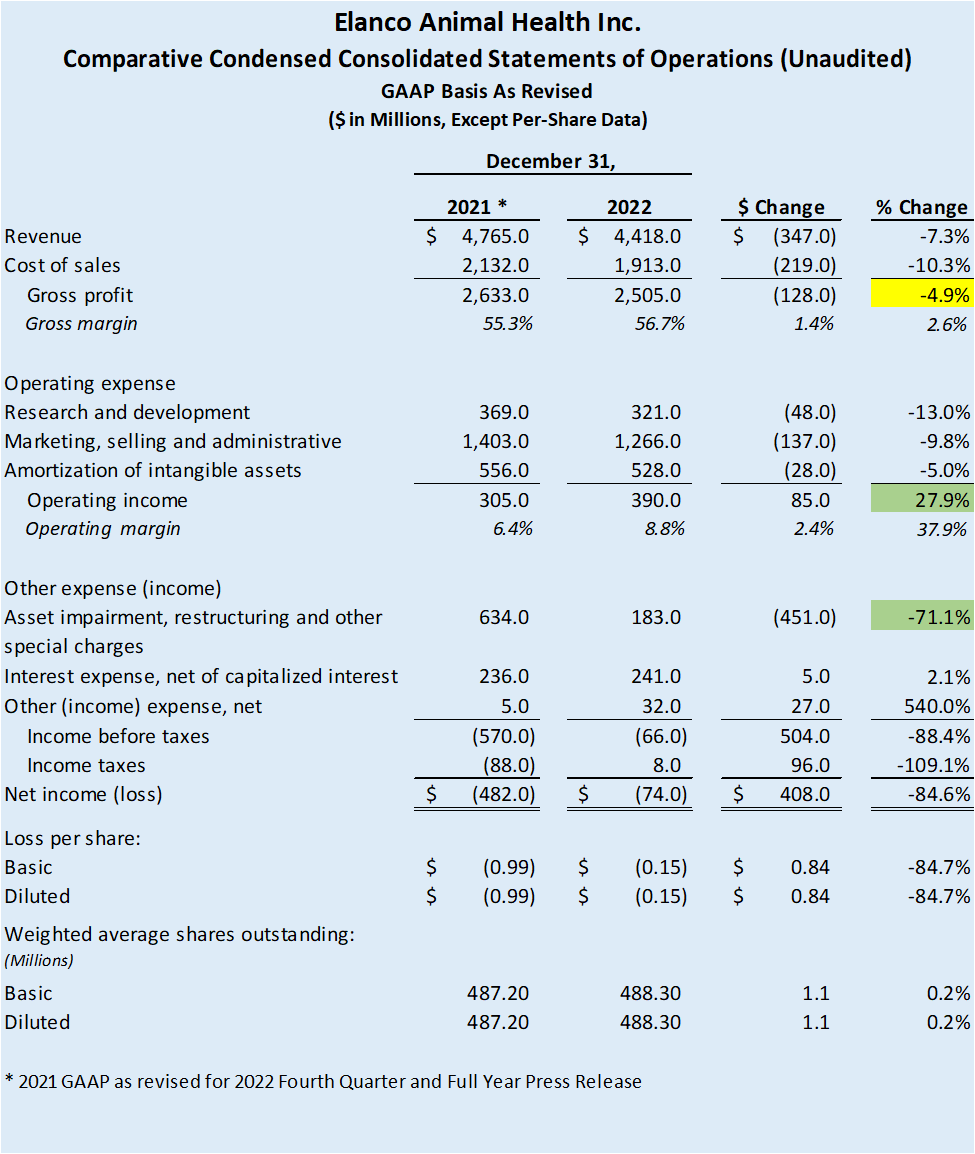

The GAAP reality, however, was not really that bad. Elanco actually reported significant improvement on its bottom line in 2022. The net loss narrowed a huge $408.0 million or 84.6% to $74.0 million - marked in green on the GAAP-basis Comparative Income Statements below, management's second version of its performance, equivalent to EPS of - $0.15 compared to - $0.99 in 2021.

Elanco 2022 Fourth Quarter and Full Year Press Release, Herding Value Analysis

{kind=link}

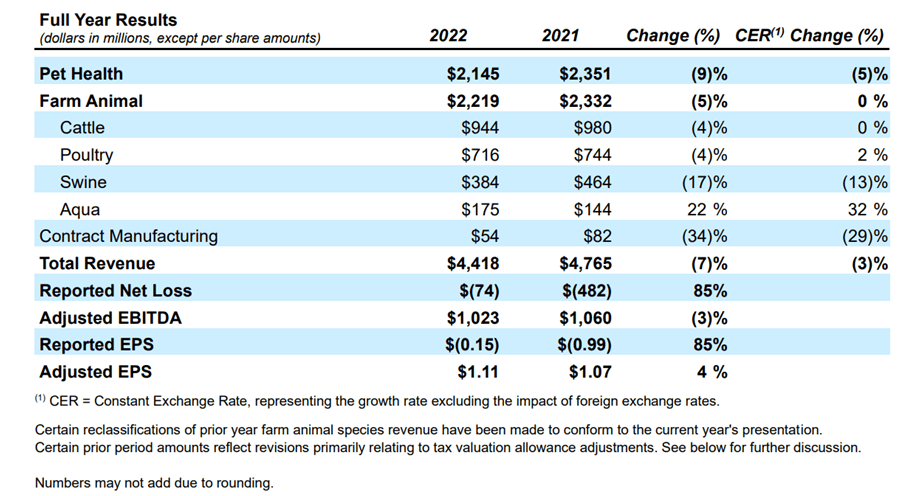

Unfortunately, the improvement did not come from gross profit which suffered from a particularly disappointing 7.3% decline in revenues - marked in yellow in above. The table below shows that the decline in revenue hit every segment of the company's business except drugs for aquatic purposes.

Elanco 2022 Fourth Quarter and Full Year Press Release

{kind=link}

Management blamed " environmental and competitive pressure " for declining revenue, but competitor Zoetis ( ZTS ) was able to report a 4% increase in revenue for 2022. Elanco's primary revenue issue is an aging drug portfolio. This is especially obvious in the Pet/Companion Animal Health segment, where Zoetis reported an 11% increase in revenue in 2022, compared to a 9% decline for Elanco.

On the plus side, cost of sales declined 10.3% - even more than revenue - but not enough to prevent gross profit from declining $128.0 million or 4.9% to $2.5 billion from 2021's $2.6 billion. The decline in cost of sales probably results from the continuing push for productivity from synergies with acquired companies, most notably Bayer Animal Health. President and CEO Simmons made the following comment on cost-savings and productivity during the 2022 Elanco Fourth Quarter and Full Year Conference Call :

Finally, on productivity. We delivered savings in cost avoidance despite significant inflation and product mix pressure, allowing for a slight expansion of gross margin in 2022.

The gross margin increased 140 bps from 55.3% in 2021 to 56.7% in 2022 on a GAAP basis. On a non-GAAP basis, however, the adjusted gross margin increased a lower 70 bps based on an adjusted gross margin of 56.6% in 2021 due to the removal of certain GAAP amortization amounts from cost of sales.

The declines in the ongoing business-related categories of operating expense; research and development - down 13.0%, marketing, selling and administrative - down 9.8%, indicate that post-acquisition costs from the purchases of Aratana for $234.0 million 2019, Bayer Animal Health for $6.9 billion in 2020 and Kindred Biosciences for $444.0 million in 2021 are finally being brought under control. It has required almost three years, for example, to integrate Bayer's IT and other systems. Solely due to this new-found cost-control, Elanco was able to report an $85.0 million or 27.9% increase in operating income to $390.0 million from $305.0 million in 2021.

The final element in 2022's improvement in financial performance was the immense $451.0 million or 71.1% drop-off in impairment, restructuring and other special charges to $183.0 million from $634.0 million in 2021. Since 2019, Elanco has reported more than $1.6 billion in these "non-recurring one-time charges," about 21% of the total purchase price for all acquisitions during that period. It is highly likely that Elanco stockholders would like to see the end of these extraordinary expenses.

Speaking of Elanco's Expenses…

Facing an aging product pipeline, competitive pressures, difficult acquisition integration and earnings challenges in 2022, management decided…to allocate $100.0 million to build a brand-new six-story headquarters with adjoining labs on a 40-acre site in Indianapolis, Indiana.

Elanco April 12, 2022 Press Release

Centralization of offices and labs might help Elanco over time, but building a new office tower in 2022 with the company challenged on so many fronts was a very bold - and expensive - move.

Debt

Elanco has paid the price for achieving scale with debt. As of the end of 4Q 2022, the company carried $5.9 billion in long-term debt against a $5.5 billion market cap. In comparison, much larger competitor Zoetis carried $8.0 billion in long-term debt against a $78.7 billion market cap. At the end of 4Q 2022, Elanco's net leverage ratio was 5.4 x adjusted EBITDA, unchanged from 2021, in spite of the paydown of about $501.0 million in debt. Although Elanco's net leverage ratio is high, maturities are limited until 2027 and net leverage covenants are 7.7 x adjusted EBITDA.

Management is committed to continuing to pay down debt. Elanco's corporate family ratings are non-investment grade; BB from S&P and Ba2 from Moody's. With an expected increase in EBITDA, an acquisition halt and some debt paydowns, Elanco's debt should be manageable but will bear watching.

The Pipeline

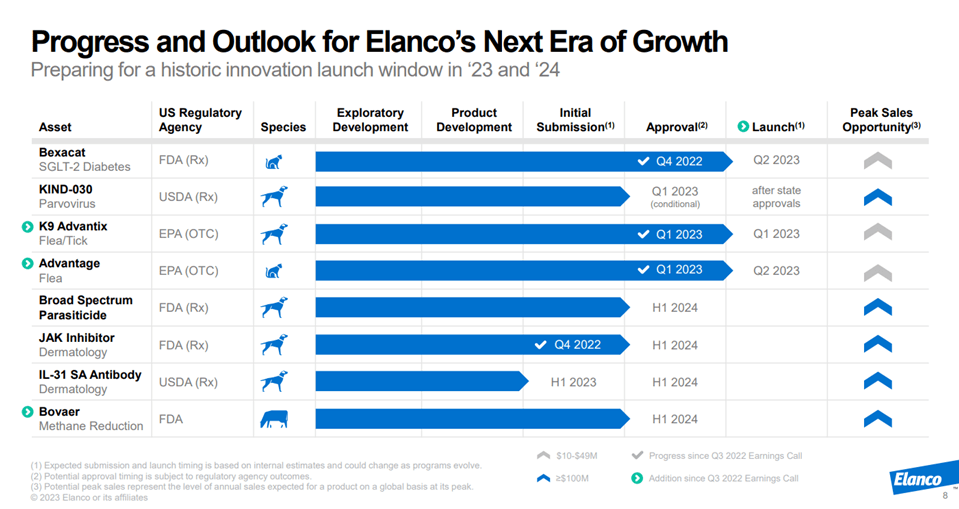

The future of any drug company depends on its pipeline of new and/or reformulated products. Declining 2022 revenue put Elanco's product pipeline in sharp focus. Here are the highlights:

Elanco 2022 Fourth Quarter and Full Year Investor Presentation

{kind=link}

According to President & CEO Simmons on the 2022 Elanco Fourth Quarter and Full Year Conference Call :

Also, our late-stage innovation is on track, and we continue to see a path towards U.S. approval of 5 potential blockbuster products by the first half of 2024. And today, very importantly, after close collaboration with the FDA, we are pleased to announce we now anticipate a first half 2024 U.S. approval and launch of Bovaer, a methane reducing product for cattle. This adds another potential blockbuster to our suite of late-stage innovation and adds to our confidence in 2024 and beyond.

With luck, these drugs should finally enable Elanco to turn the corner on profitability. KIND-030, in particular, if successful, will vindicate management's acquisition of Kindred Bio spending to acquire genetic engineering capabilities.

Seresto: Waiting for the EPA

A March 2021 USA Today article, followed by lawsuits, claimed that there had been 1,700 pet deaths linked to the Seresto flea collar. Elanco, generally supported by the veterinary industry, disputed the article's findings as no scientifically valid investigative work was performed prior to publication. Subsequently, in June 2022, the Subcommittee on Economic and Consumer Policy of the House Committee on Oversight and Reform released a report recommending the recall of the collar after finding that about 2,500 pet deaths were anecdotally attributed to the collar - out of about 34 million collars sold, or about 0.01% of pets using the collars - without conducting a scientific evaluation and despite the collar being approved in 80 jurisdictions around the world.

Subsequently the EPA , which regulates pesticide-containing pet collars, decided to expand its oversight and "request enhanced incident reporting and sales data for pet products, including collars." Regarding Seresto, per the 3Q 2022 10-Q , Elanco is "vigorously defending" its position that the collars are safe. President & CEO Simmons, during the 2022 Elanco Fourth Quarter and Full Year Conference Call noted "a very constructive positive dialogue" with the EPA. He also expected an EPA "outcome" in 2023 and reiterated that Seresto, the company's second-largest product line with $352.0 million in 2022 sales, was "a key product that will help drive the strength and profile of this company."

ELAN Stock Valuation

As the graph below indicates, investors have perhaps grown tired of waiting for an inflection point in Elanco's financial performance.

What's Elanco worth?

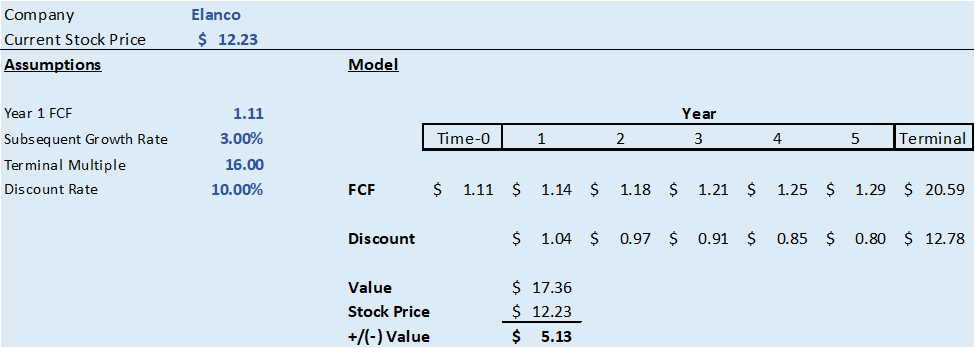

I updated my DCF model by calculating a starting point of $1.11 per share of free cash flow per 2022's results, assuming 3.00% annual growth, a long-term S&P 500 market multiple of 16 as the exit multiple and discounted at my personal 10.00% hurdle rate to derive a surprising per share value of $17.36. This compares well with the current Morgan Stanley price target of $17.00 per share.

Seeking Alpha, Elanco 2022 Fourth Quarter and Full Year Investor Presentation, Herding Value Analysis

{kind=link}

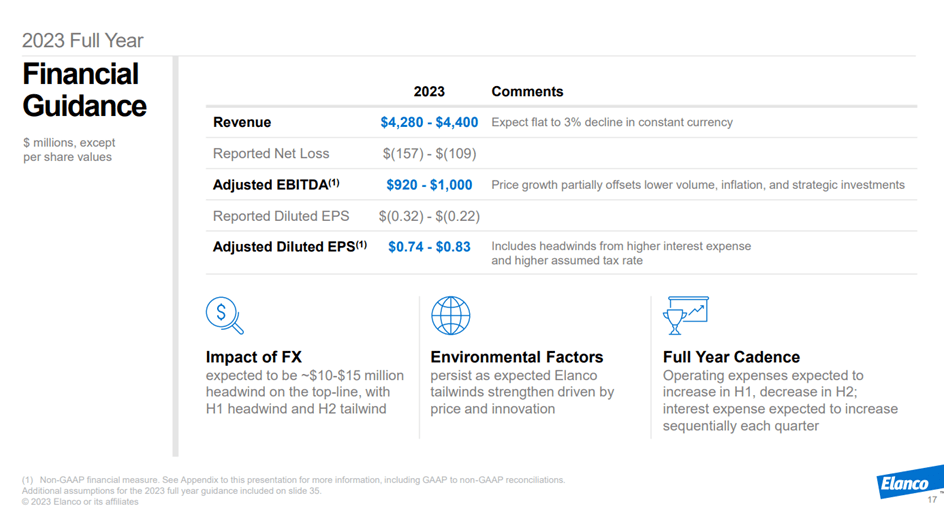

In terms of multiples, Elanco appears to be trading off adjusted EPS. Management's 2023 guidance is for adjusted midpoint EPS of $0.79 and GAAP EPS of -$0.22 to - $0.32. At February 22, 2023's $12.23 per share, the implied adjusted PE is 15.6. Analysts are looking for 2023 to be another year of muddling through with an adjusted consensus $0.83 per share EPS estimate. With no multiple expansion, we get a share value of $12.95 at the adjusted 2023 EPS midpoint.

Most analysts see 2024 as the year when management's vision for the company begins to become reality with consensus estimates of $1.02 in adjusted EPS. Applying the same current multiple to be conservative provides an estimate of $15.91 per share.

If we regard 2023's value as an outlier, an investor could justify a per share price in the range of $16.00 to $17.00, a potential gain of 30% to 40%. This might be what interested the value investors at Dodge & Cox.

Conclusion

With exceedingly weak 2023 guidance from management, however, in the near-term Elanco has almost become an option on its own drug pipeline.

Elanco 2022 Fourth Quarter and Full Year Investor Presentation

{kind=link}

The guidance for GAAP revenue, net loss and EPS are all worse than the corresponding 2022 reported results. Even the adjusted guidance is worse than "actual" adjusted 2022 results. Larger competitor ZTS is expecting increases in all areas - and making no concessions to a possible 2023 recession. As always, there are merits and considerations:

Merits :

- Animal health is a growing and somewhat recession-resistant industry.

- ELAN is the second-largest pure play in the industry.

- Management has transformed the company with an expanded product offering and pipeline.

- Management is committed to rationalization of operations.

- Dodge & Cox acquired 86.0 million shares in 4Q 2022 and owns about 18.0% of Elanco's stock.

Considerations :

- Elanco has not reported GAAP net income since 2019, its first full year as an independent company.

- Elanco carries a lot of debt due to its acquisitions, hampering financial flexibility.

- A dark cloud still hangs over Seresto, the company's second-largest product.

- At 3Q 2022, Sachem Head Capital Management owned 28.6 million shares or 6% of Elanco's stock, but sold 88% of its position and owned just 3.4 million shares at year-end 2022.

My advice regarding Elanco remains much as it has been for several quarters. Investors with shorter time horizons and smaller portfolios should pass. This is a company that has been just about to turn the corner for a few years; it's going to take time. Buy "best-in-breed" ZTS instead and forget about the complications of Elanco.

If, however, you're a value investor with a 3 to 5-year time horizon looking for a speculative transformation play for a small portion of your portfolio, consider Elanco, there is the possibility of a 30% to 40% gain here.

For further details see:

Elanco 2022 Earnings: Speculative Value With Signs Of Progress