EBS - Emergent BioSolutions: Meaningful Debt But Narcan Should Grow

2023-11-23 08:10:13 ET

Summary

- Emergent BioSolutions produces NARCAN nasal spray, traveler's package vaccines and other vaccines periodically stockpiled by the government.

- NARCAN is experiencing substantial growth due to demand from the opioid epidemic and has received OTC approval to further drive access.

- The company is facing financial challenges, including negative income, high debt, and rising interest costs. They are implementing cost savings measures to improve profitability.

- In all, the multiple isn't that high, but it's also uncertain due to volatile operating outcomes. Moreover, underlying cash generation could be better.

- While meaningful demand will come online again, underlying cash generation isn't that strong and combined with debt we have too many concerns to like it.

Emergent BioSolutions ( EBS ) produces NARCAN, the infamous nasal spray used to treat opioid overdoses, in addition to some other products and live vaccines with substantial but lumpy US Government demand. While multiples on guidance are not too high, lumpy economics and periodic cash burn are an issue, as well as weak underlying cash generation in the face of pretty substantial debt and rising interest costs. We think there are simply better businesses out there for cheaper multiples than EBS.

Products

Emergent BioSolutions is the company which tends to be a “medical shield” for people through the products which they make. They have extensive pipeline of products (which are commercially in use), as well as product candidates (which are in clinical trials) at the time of making this article.

Main focus of the story should be the products which make the most money for the company and additionally are important from a medical need perspective too. These are NARCAN nasal spray, Vaxchora and the Vivotif vaccines.

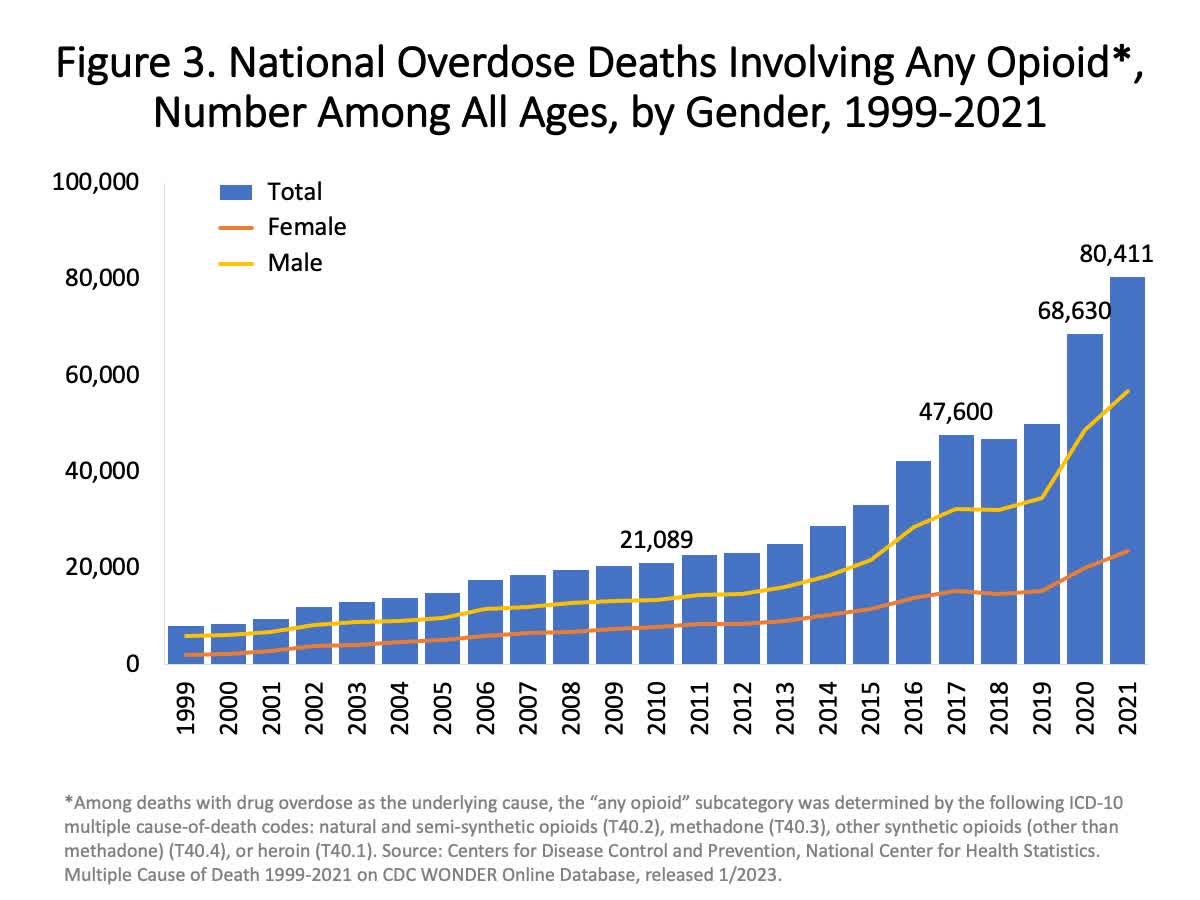

NARCAN nasal spray is a form of naloxone drug adapted for intranasal application which company made in cooperation with pharma company (called Adapt Pharma). Naloxone is the essential substance of mentioned product and it is clinically used in opioid overdoses (since naloxone binds to opioid receptors in a human body and respectively blocks and counters the opioid effect). Nasal application of the drug is smart choice, because our nasal mucosa has amazingly rich web of blood vessels, which ensure fast absorption and action of the drug. This drug has real significance, considering the large number of deaths every year caused by opioid overdoses in the US, a cause of death that is actually noticeably affecting trends in US mortality.

{kind=link}

Both of the vaccines (Vaxchora and Vivotif) are live vaccines against serious intestinal infections (Vaxchora against cholera infection, Vivotif against typhoid infection). Symptoms of these infections, such as extensive vomiting, high fever and severe diarrhea can lead to dangerous dehydration (in extreme cases even can cause even death). We can say that these vaccines play really important role specially as a “traveler package” vaccines in areas with high incidence such as Africa and some parts of Asia. If anyone wonders about side effects of these products, they are pretty rare and really mild if they eventually occur.

Bottom Line

The results are as follows. The other products, containing the traveler's package vaccines, are seeming pretty resilient following a trough during COVID-19. They are in line to produce more or less the same results as last year according to the guidance .

NARCAN is growing substantially thanks to continued demand from the opioid epidemic ravaging the continent. Moreover, they have moved forward with OTC approval, and due to the severity of the crisis there is bipartisan support in maximising access to NARCAN. The OTC NARCAN hit shelves in September of this year .

{kind=link}

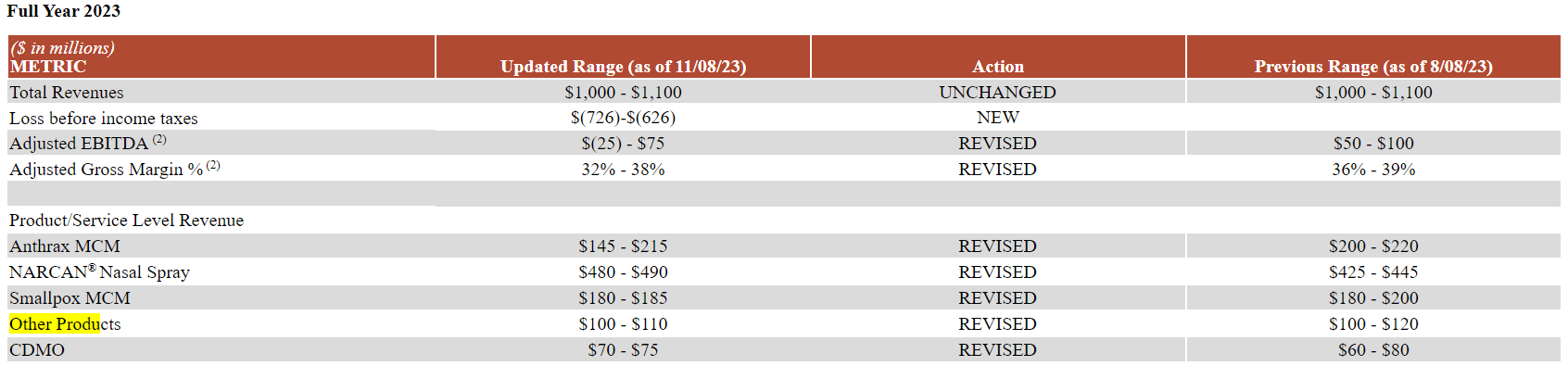

A financial view is important here, because EBS has been going through some issues. In 2021 there was massive demand from the US governmen t in exercising contract options to shore up emergency reserves of vaccines like those of smallpox. These purchases are not that frequent and they have created negative comp effects. The come down from this has brought the company into negative income territory as some programmes have since generated no revenue, but while timing remains uncertain, both the demand for more smallpox vaccines and anthrax vaccines are possible to generate some positive upside. In the meantime, the uncertainty has led to widening and lowering of guidance ranges, including of EBITDA from a max of $100 million to a max of $75 million.

They are planning on de-emphasising contract manufacturing and trying to generate savings that they expect will amount to $100 million annualised by Q1 2024. This should in principle bring them out of operating unprofitability, and would put the adjusted EV/EBITDA multiple at around 10x in the more optimistic outcomes. If they could hit $100 million in adjusted EBITDA, their pre-revision best case scenario, the multiple would be 8x based on current market cap. It's not high but it's not low either considering the suboptimal economics.

Despite the attractiveness of NARCAN in terms of growth, another concern around interest expenses probably has us looking elsewhere for now. The higher for longer environment will impact the results substantially. Interest expense will rise more than 2x and this matters for shareholders. Net income losses are going to stay pretty substantial in our opinion. While the company is addressing the situation with cost savings, it may not be enough and actually turns the company into a cash burning proposition. In fact, cost savings are mostly going to be offsetting the higher interest costs in the bottom line. Also there is quite a lot of leverage which compounds problems, around $700 million net debt to the $100 million in market cap. While NARCAN will continue to expand, the bottom line is a concern, as is underlying profitability in the expansion. Despite the safe bet of NARCAN expansion, we just think the story gets a little too complex considering cash burn and pre-existing leverage, it can be quite dangerous. At least most of the debt comes due in 2028, and there is $600 million in cash to cover around 4 years of current negatives in FCF of around $150 million roughly, depending on CAPEX, with scope that the cash burn declines substantially on NARCAN scale as well as repeat demand from the US Gov't for anthrax and smallpox vaccines. The 4 years staying power is not a charitable figure given that live vaccine demand could come online. Still, not very attractive proposition on account of debt and interest costs.

For further details see:

Emergent BioSolutions: Meaningful Debt, But Narcan Should Grow