EMR - Emerson Electric: My Best Value Pick For Dividend Growth Investors

2023-10-23 11:15:02 ET

Summary

- A Dividend Growth Investing strategy can generate retirement income by buying and holding Dividend Champions and reinvesting into more shares over time.

- Emerson Electric is a Dividend Champion with a strong track record, including 66 consecutive years of dividend increases.

- EMR has undergone a business transformation and is well-positioned for growth in industries such as LNG, nuclear, life sciences, and mining.

As I approach my retirement years my investing style has changed from one of growth and accumulation to one that is more focused on generating income to replace my employment income that is no longer coming in. However, there is more than one way to generate income for retirement by investing in stocks. One common approach that is embraced by many experienced investors is the Dividend Growth Investing strategy or DGI. Dividend Champions are stocks that have increased their dividend for at least 25 years in a row. By buying, holding, and reinvesting the dividends into new shares over many years and as long as those shares continually increase in price over time, the total return realized from DGI investments can help build a retirement income stream.

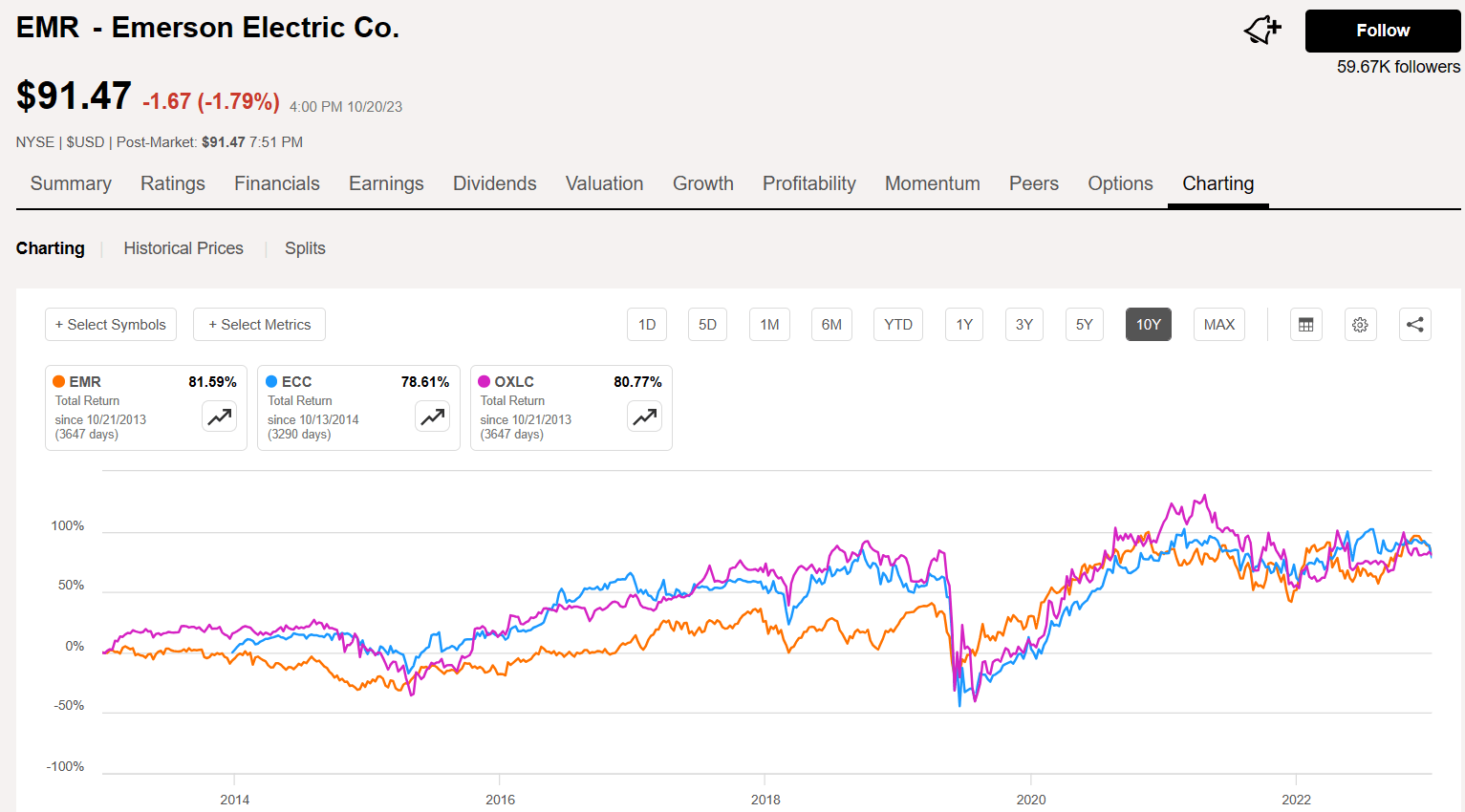

One Dividend Champion that I believe is an excellent value at the current time, is Emerson Electric (EMR). Emerson has been around for over 130 years and has increased the dividend every year for the past 66 years ! While EMR only yields about 2.27% with its current quarterly dividend of $0.52, the total return over the past 10 years when factoring in capital appreciation and dividend reinvestment has been comparable to an investment in Oxford Lane Capital (OXLC) or Eagle Point Credit (ECC), which are both high yield income-oriented investments that currently yield 19% and 18%, respectively.

{kind=link}

If you go back even further, the total return for EMR has been quite impressive. If you had invested $10,000 in EMR stock in January 1987 and reinvested the dividends received, you would now have over $380,000, which represents a CAGR of more than 10%. That means that on average, you would have increased your total return by 10.4% per year by just reinvesting those increasing dividends each year into more shares of EMR stock.

But that is all "water under the bridge" if you have not been invested in EMR stock for the past 35+ years. So, let's look at what EMR is worth now and see if it still makes sense to invest in it for a future total return that represents good value for current investors. Things have changed quite a bit in the past few years and EMR is a much different company now than it was in 1987.

Emerson started in St. Louis, Missouri in 1890 as a manufacturer of electric fans and motors. Now they are a global technology solutions powerhouse. Emerson now offers products, services, and solutions for a multitude of industries.

{kind=link}

In 2021 a new CEO came on board, Lal Karsanbhai, replacing David Farr who served as CEO for 20 years. That year also saw the acquisition of OSI, Inc. for $1.6 billion. OSI is an operations technology software provider for the global power industry. In 2022, the company acquired 55% of Aspen Technology (AZPN) and combined OSI and Aspen with the Subsurface Science and Engineering business. Also in 2022, the company sold the InSinkErator business to Whirlpool Corp (WHR) for $3B. Another deal that was completed in May of this year involved the sale of the Emerson Climate Technologies business to Blackstone for $14B (now called Copeland). On October 11, the deal to acquire National Instruments (NATI) for $8.2B was completed .

NI brings a portfolio of software, control and intelligent devices that is expected to accelerate Emerson's revenue growth aligned to its 4-7% through the cycle organic growth target. NI increases Emerson's end market exposure in discrete markets, which will be Emerson's second largest industry segment, and with approximately 20% of sales in software, NI also increases Emerson's exposure to high-growth industrial software markets. NI increases Emerson's gross profit, with further adjusted EBITA margin expansion opportunities as Emerson delivers an expected $165 million of cost synergy opportunities by the end of year 5 through application of best practices from the Emerson Management System.

Other acquisitions completed in 2023 include a deal to acquire Afag from Switzerland to improve factory automation capabilities and a deal to acquire Flexim from Germany to enhance the Emerson intelligent devices portfolio.

Q3 2023 Earnings Results

The company reported strong performance results with 14% underlying sales growth, 59% operating leverage, and 40% adjusted EPS growth. They closed the Copland transaction resulting in ~$8B in after-tax proceeds plus expected future proceeds of about $4B. Free cash flow of $769 million was up 83% YOY and 47% YTD.

The company's strategy to shift business away from traditional energy, power, and chemical industries and win more projects in LNG, Nuclear, Renewables, Metals/Mining, Clean Fuels, and Energy Transition businesses has been successful thus far with several new wins in LNG, Lithium and Copper Mining, Battery Manufacturing, etc. The current environment is improving based on growing demand for Process and Hybrid solutions, supply chain improvements, and price-cost benefits from effective inflation management.

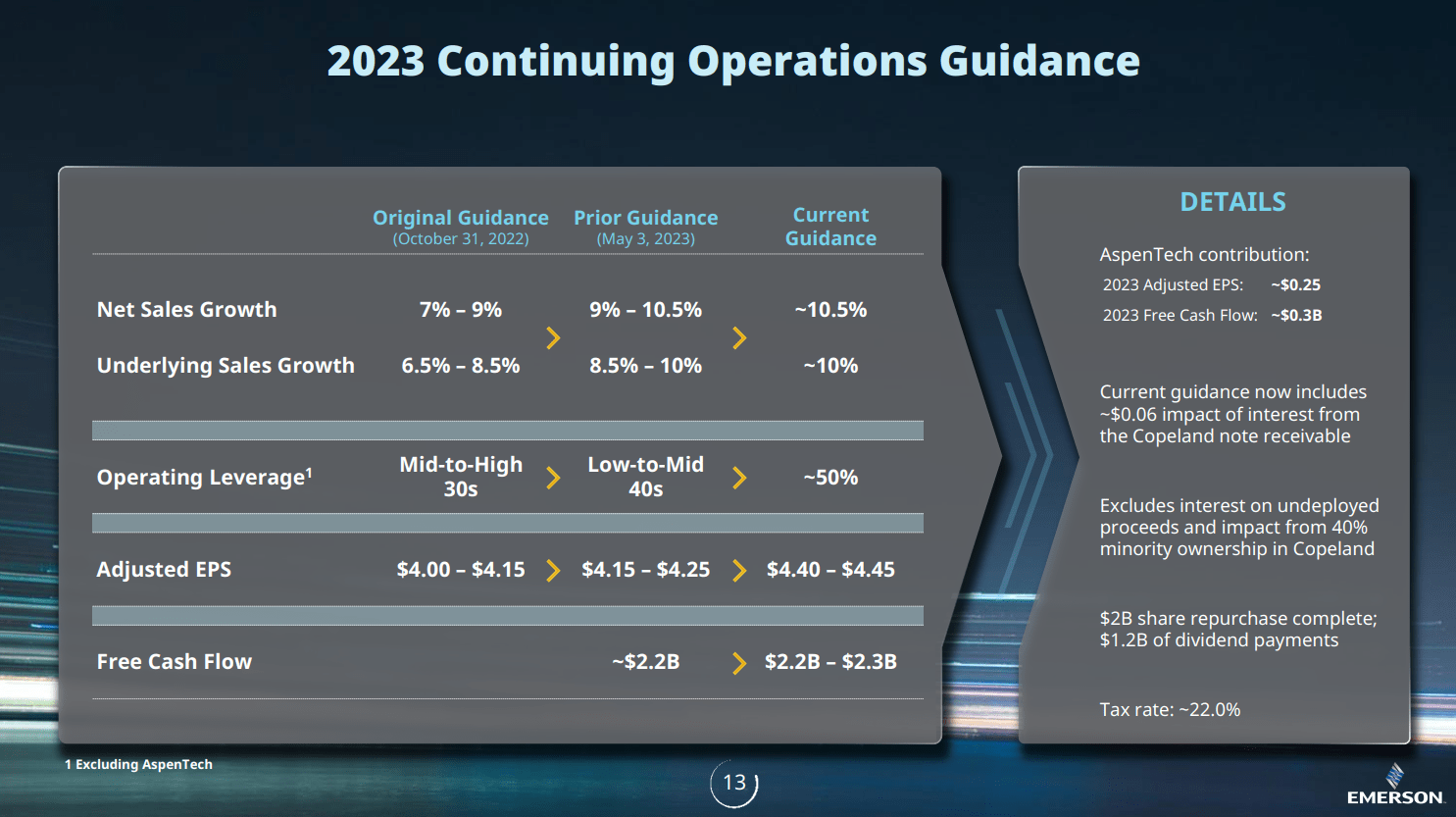

Key growth drivers for the business include the Energy Transition leadership opportunities, nearshoring with stimulus investments in mining, life sciences, and the battery value chain, and software growth from AI and sustainability trends. Guidance for sales growth, EPS growth, operating leverage, and free cash flow for FY2023 is improving as illustrated in this slide from the Q3 presentation.

{kind=link}

And all of this growth is happening without the additional revenues from NI and the other recent acquisitions. Once those new business additions begin to add to the bottom line the numbers should improve even more. For reference purposes, consider that NI reported $1.66 billion in revenues in 2022, operating in 40 countries and serving approximately 35,000 customers.

The industry outlook for the Emerson business lines is optimistic. The spending on the global energy transition continues to accelerate. There is continued momentum for power and renewables demand in the US. LNG continues to gain momentum in North America and the Middle East. Reshoring trends are driving life sciences and lithium and battery metals activity, especially in Mexico, Australia, and the US. Battery manufacturing investments are increasing in the US and Asia. There is some slowing in factory demand automation but still a large addressable market, especially on the software side with AI and IoT device integration.

Valuation and Ratings

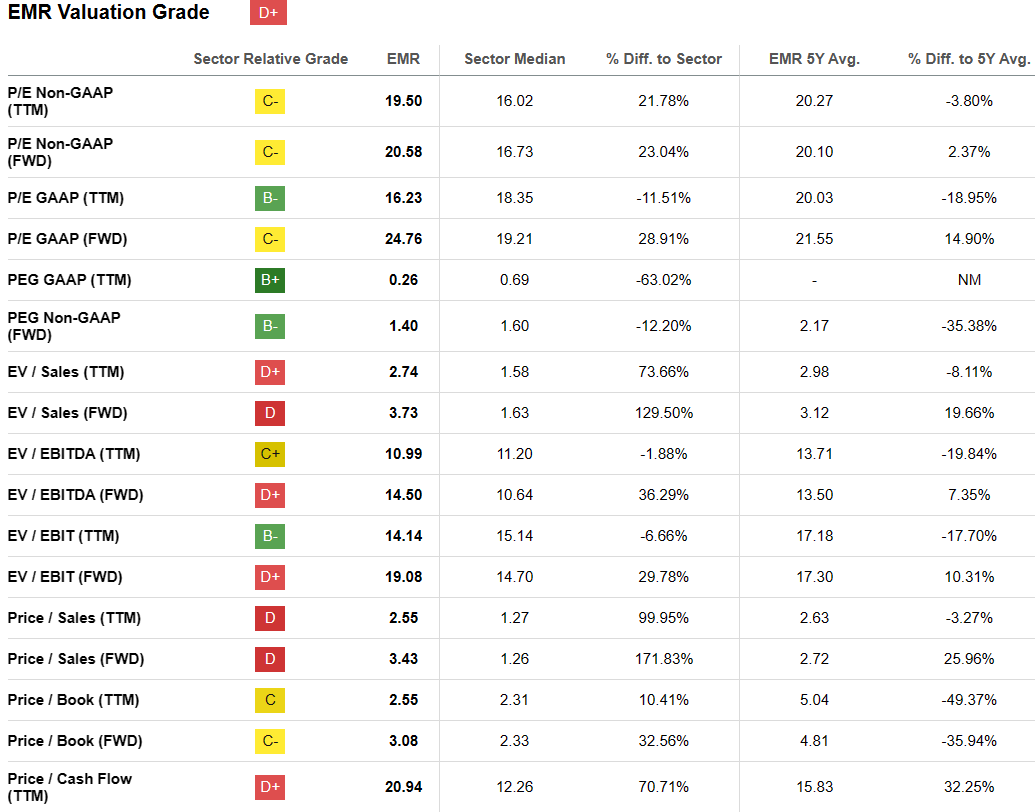

For what it's worth, the SA Quant system gives EMR a D+ for Valuation.

Seeking Alpha

Digging a little deeper, we can see that the forward GAAP P/E is a bit on the high side relative to its peers. Also, the EV/Sales ratio is on the high side as is the Price to Cash Flow ratio. But most of the factors are below the 5-year average, so I would not consider these indicators to be all that reliable, especially considering that growth is picking up again now that the Covid pandemic effects are fading into the distance.

{kind=link}

When you consider that Revenue and Earnings revisions are picking up considerably now that the NI acquisition is complete, I believe that the current value is well below the future fair value of the stock.

{kind=link}

Wall Street analysts give EMR a Strong Buy rating. Over the past few weeks, I have seen price targets raised by several analysts to $120, about a 30% increase from the current share price of $91.

Seeking Alpha

Even UBS, who downgraded the stock to Hold offered an increased price target of $104.

UBS raised its price target on Emerson to $104 a share from $97 a share previously, based on a sum-of-the-parts analysis that implies a multiple of 12 times the estimated Ebitda for 2025.

According to TipRanks, the average price target is $110 and the lowest is $95 in the last month.

Business Transformation is Succeeding

The reason why I chose EMR as my Best Value Pick is due to the incredible transformation that the business is undergoing. As explained by CEO Karsanbhai at the Morgan Stanley Laguna Conference , the global energy business is undergoing a transition and Emerson is positioning itself to take advantage of the trends they are seeing in near-shoring, energy security, affordability, sustainability, and digital transformation.

No, look, a lot of positive momentum in our business at this point in time; we've undergone, over two and a half years, a fundamental transformation at Emerson, disposing the Copeland business, the InSinkErator business, TOD, a few oil-centric assets and replacing those with AspenTech, National Instruments and creating a cohesive automation portfolio with that.

In energy, the trends that he sees as opportunities for EMR include LNG and Nuclear:

We're talking about gas, liquefied natural gas, which is in a period of investment, an investment wave that is unprecedented. It's driven in three key geographies around the world. It's the Gulf Shore of the Gulf of Mexico here in the United States, it's Qatar and it's Mozambique. That's where the core investments will occur over the next three to seven years.

We are in the early innings of a resurgence in nuclear power. And that comes in two ways, the first being, of course, the smaller reactors, the SMRs. These are basically your nuclear sub-reactor used in a commercial way. But the second is the extension of life of nuclear power plants.

The other industries that EMR is targeting include life sciences, and mining and metals. This is what he had to say about those opportunities:

Life sciences, the perspective there is that just about every country, industrialized country on the planet is bringing the life science capacity onto their shores. On a recent trip to Australia, where 9 out of 10 meetings that I hold with customers are related to the mining industry, the first set of meetings were with Moderna and BioNTech, who are replicating their capacity from the Northeast and in Belgium into Melbourne for vaccine manufacturing.

So, nearshoring is very important for us as it relates to the life science industry and then metals and mining. We have quietly put together a $450 million, $500 million metals and mining business, but very relevant as it moves today for us from what was traditional production into the processing and now into the packaging, particularly as it relates to batteries and EVs.

And then there is the additional opportunity of integrating NI with the current business lines, opening up new markets from existing NI customers in semiconductors, aerospace, defense, EVs, and other technology markets that EMR has not already penetrated. The CEO expects that the NI acquisition will result in $165 million in cost synergies while adding 30 points to EBITDA. It may take a few quarters to get there, but that is the expectation going forward.

Risks and Competition

Some of the biggest risks to the business emanate from the global economy and potential impacts on renewable energy investments, inventory buildup and slowing demand due to geopolitical conflicts in the geographies in which the company operates, the slowing economy in China, and a slowdown in spending on EV battery manufacturing or other end markets like lithium production.

Most of the businesses that are generating the majority of profits for EMR are going strong with LNG in the Middle East not currently impacted and renewables in Europe still going strong, at least through the 3rd quarter of 2023. The CFO, Michael Baughman summarized the prospects by geographies at the Laguna conference:

Reading through the geographies. I mean, start in North America, our biggest business is about 50%. We'll exit the year, with about 10% growth driven by a lot of what Lal talked about with LNG, energy, metals and mining, life science is all strong.

Moving to Europe, we'll exit that business in the high single digits. Liquid natural gas, re-gasification, renewables driving in that area. A lot of discussion around China, the headline discussion around commercial residential doesn't really read through in our business, though we're seeing some discrete softness. Chemical is very strong. That's a nearshoring effort as well.

Rest of Asia, high single digits as we exit the year. And then Middle East, Africa, a region that's just been growing really nicely. We'll add over $100 million in growth this year in LNG, chemical and traditional energy, so everything Lal was talking about really reading through nicely in the numbers.

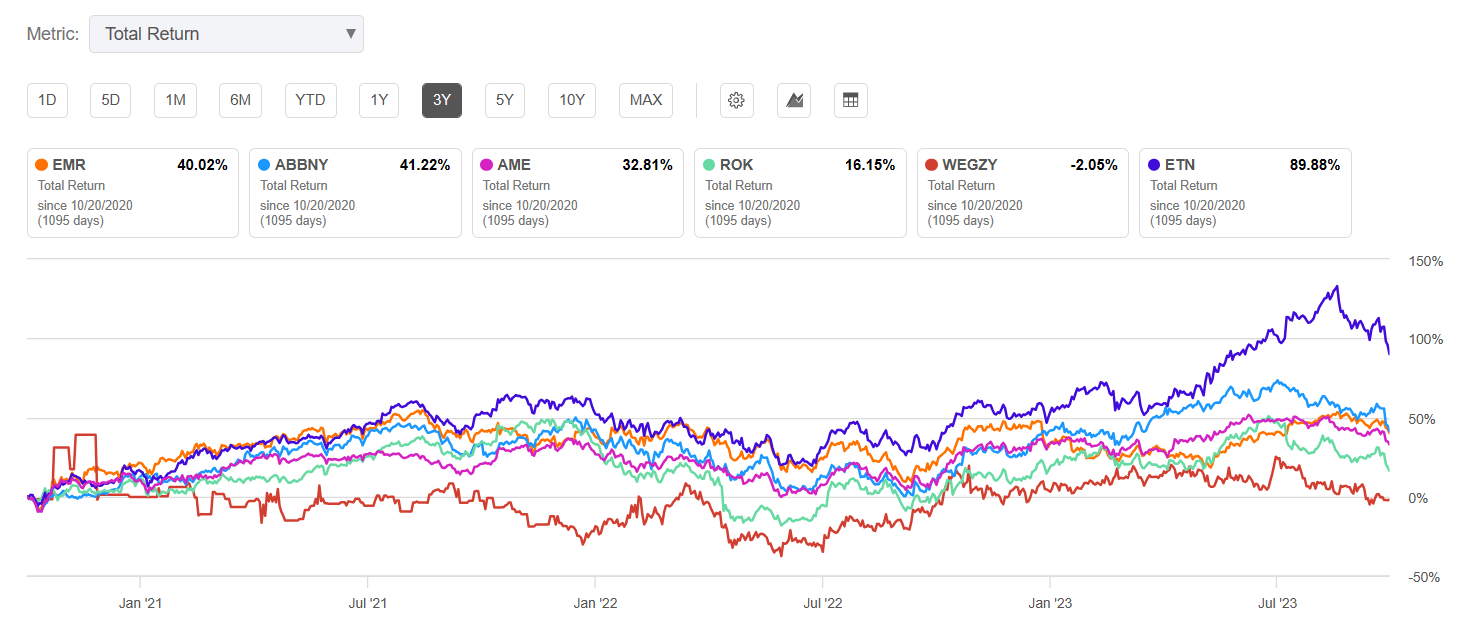

Peers and competitors include Rockwell Automation (ROK), Eaton (ETN), AMETEK (AME), and ABB (ABBNY).

{kind=link}

Over the past 3 years, Eaton has had the best total return but appears to be losing their edge over the past couple of months. I have not done an in-depth analysis of Eaton stock, but it may be worth further investigation if you are interested in the industrial sector. Eaton also beat on both the top and bottom lines with 12.5% YOY revenue growth when they reported Q2 FY23 results on August 1 and raised guidance for the rest of the year.

{kind=link}

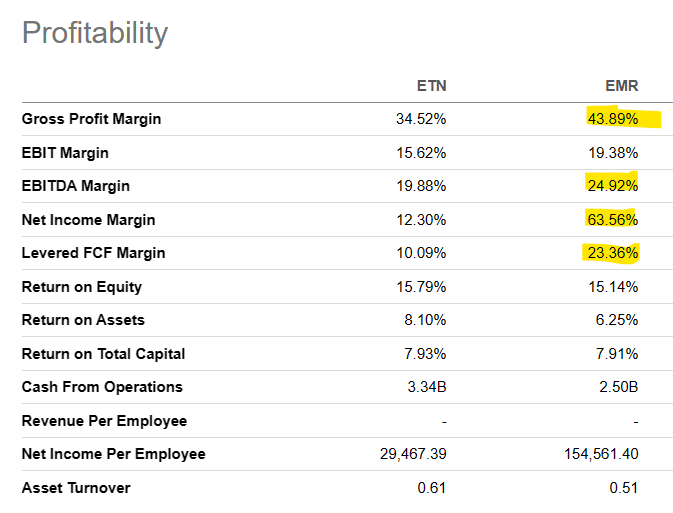

EMR does have a better valuation, better growth, and slightly better profitability than ETN.

{kind=link}

Summary

Emerson Electric is a Dividend Champion, paying out a quarterly dividend that has been continually increasing for 66 years now. The EMR stock currently trades at a TTM P/E of 16.45 (according to Yahoo Finance) and yields 2.27%. The average 1-year target estimate is $110. The last closing price as of October 20, 2023, was $91.47. I rate the stock a Buy at the current price and a Strong Buy at a price below $85.

With recent M&A activity and the pending absorption of National Instruments, there is plenty of opportunity for EMR to grow market share in a variety of industries and continue to increase margins while managing costs due to a strong balance sheet and healthy FCF. More than 76% of shares are held by institutional investors.

A recent blog from Zacks Investment sums up the Buy thesis:

Emerson Electric Co. has been benefiting from healthy demand across end markets. Strong demand across the process and hybrid markets are driving EMR's underlying sales. The successive deals to acquire Afag and Flexim spark optimism. Emerson Electric's $8.2 billion deal to acquire National Instruments holds promise. EMR's bullish guidance for fiscal 2023 is encouraging.

Emerson Electric has an expected revenue and earnings growth rate of 5.4% and 10.6%, respectively, for the current year (ending September 2024). The Zacks Consensus Estimate for current-year earnings has improved 1.4% over the last 30 days.

There is some risk to pricing pressure if the global economy experiences a slowdown due to ongoing conflicts in Ukraine and now Israel, or if additional conflicts arise in the coming months that further disrupt demand. EMR is due to report Q4 earnings on November 7, and I expect that a solid earnings beat will be announced, which is likely to drive the price higher. Meanwhile, there could be some price volatility and I would be looking to add shares if the price dips below $90 for a long-term hold.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Emerson Electric: My Best Value Pick For Dividend Growth Investors