EMR - Emerson Electric: The Buy Case Is Still Very Much In Play

2023-09-15 10:28:44 ET

Summary

- Emerson Electric Co.'s share price has grown nearly 20% due to solid sales growth and improved margins.

- The company operates in six segments, offering a wide range of innovative products and services.

- EMR is consistently posting strong free cash flow and has raised its guidance for net sales growth and earnings.

Investment Rundown

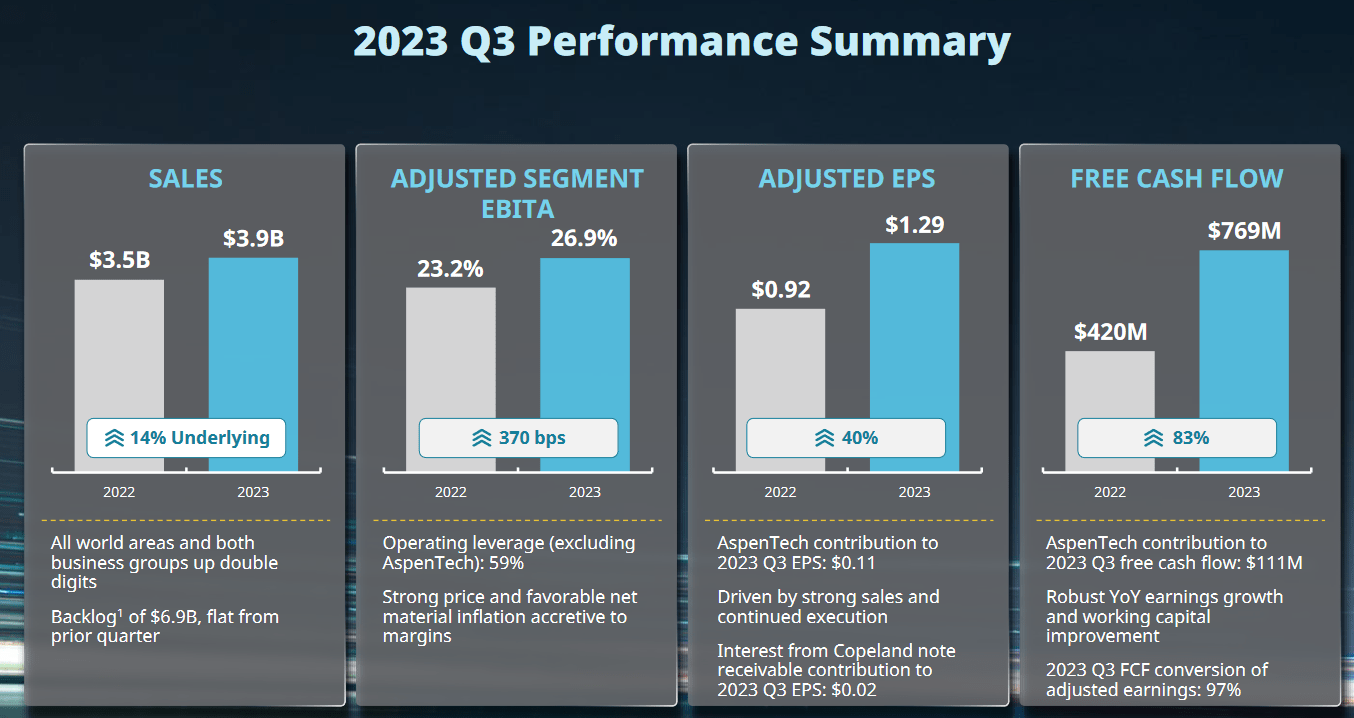

One of my better calls in the last few months has to be Emerson Electric Co. ( EMR ) as the share price has grown nearly 20% since my last coverage of the business. The last quarter showcased a solid 14% YoY growth in sales and the margins of the business continued to improve very well too on a YoY basis with an 840 bps improvement in the net margins alone. This positive news seems to have been one of the driving forces behind the share price momentum in the last few months.

From a valuation perspective, the company looks a little pricey on an earnings multiple basis as it has a premium of around 29% right now. But justifying that premium I think is the solid growth trajectory of the business and the historical performance and reliance investors have been able to have on EMR to pay out a good dividend and raise it consistently too. I liked the share price when it was 20% lower, and I still like it here. I am reiterating my buy rating for EMR right now.

Company Segments

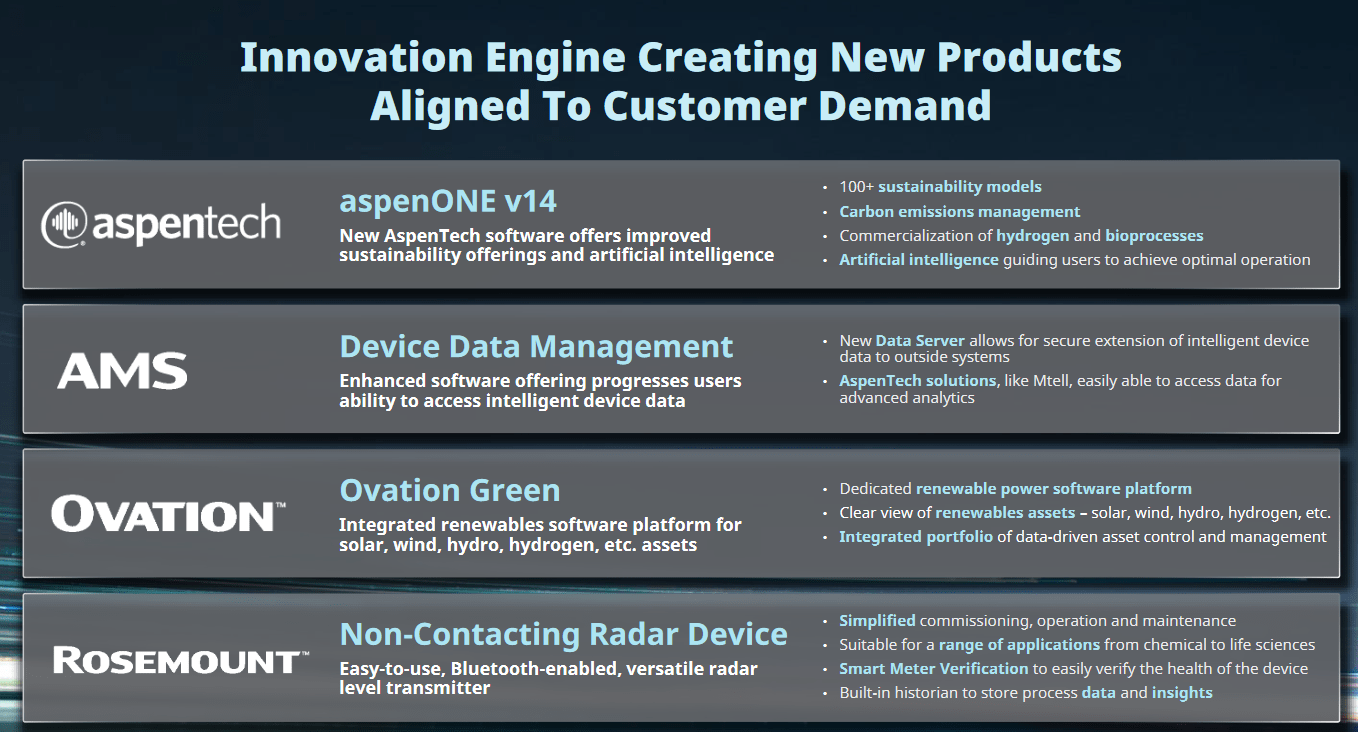

EMR is a technology and engineering firm, that delivers a diverse set of solutions to clientele spanning industrial, commercial, and consumer sectors across the Americas, Asia, the Middle East, Africa, and Europe. The company's operations are segmented into six distinct categories: Final Control, Control Systems & Software, Measurement & Analytical, AspenTech, Discrete Automation, and Safety & Productivity. This multifaceted approach enables Emerson Electric to offer a wide spectrum of innovative products and services, serving as a testament to its commitment to excellence and adaptability in today's ever-evolving markets.

{kind=link}

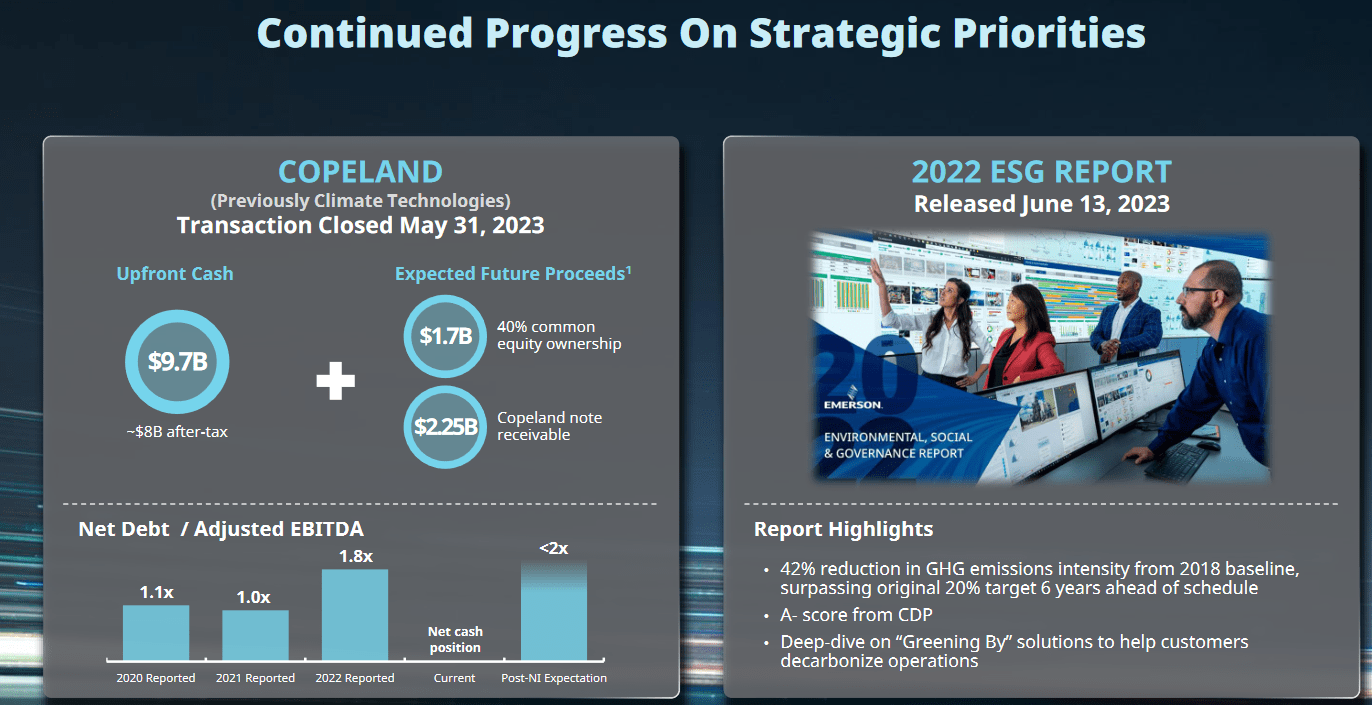

The company has been able to grow very well through the years thanks much to the aggressive sense of acquiring growing business. AspenTech was a significant one last year and the most recent one for 2023 was Copeland which is expected to add additional value to the portfolio of EMR.

{kind=link}

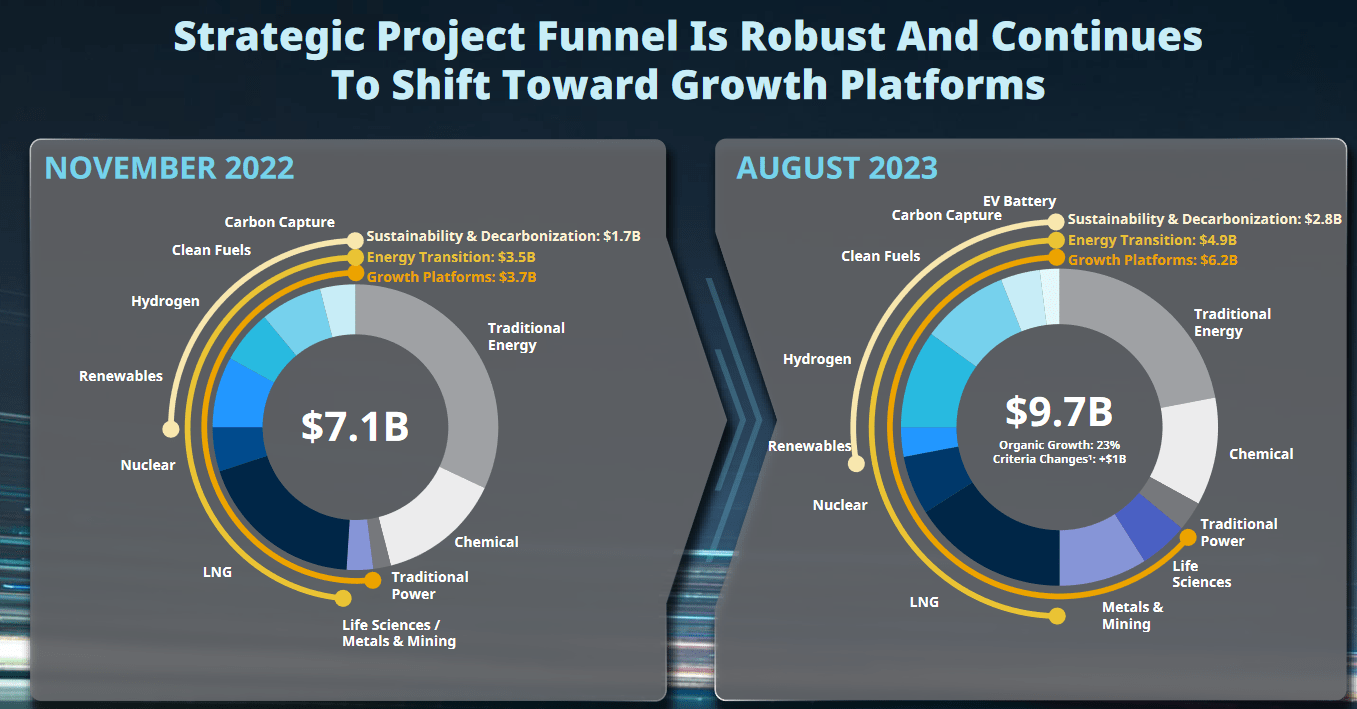

The last quarter's presentation showcased the commitment that EMR has toward growing the investments in the business. The management is sticking with its shift towards growth platforms to expand. Sustainability and decarbonization are becoming an ever larger part of EMR and I think the time is right for it now too.

Earnings Highlights

{kind=link}

As was mentioned in the earlier part of the article, EMR is growing the top and bottom line at an impressive rate as margins expand and so do the cash flows. I think that EMR is heading towards consistently posting FCF at nearly $1 billion quarterly. The expansion over the last few years and successful acquisitions as been a key driver for this I think. AspenTech for example added $111 million in FCF for the last quarter alone. The FCF conversion rate also further improved to 97% of adjusted earnings.

{kind=link}

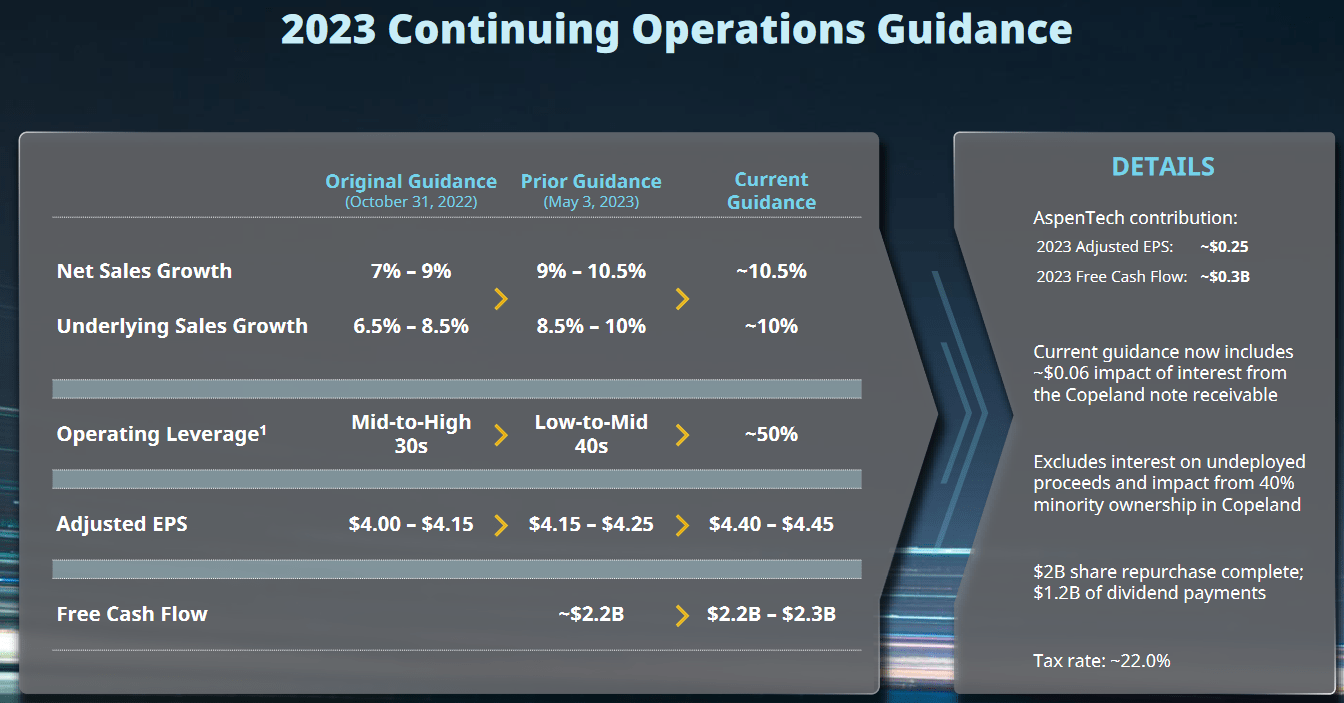

The guidance for the company is also improving and they now see the net sales growth being at 10.5%, the upper end of the previous guidance that was provided. Apart from that, the higher operating leverage seems to have trickled down to EMR raising the EPS estimates for 2023 which now sits at $4.4 - $4.45, and the FCF is raised to $2.2 - $2.3 billion. A comparison of the FCF to 2021 is a slight decline, but I think we can now have a reliable FCF of over $2 billion as the addition of AspenTech seems to have ensured this.

Risks

A significant concern for EMR at present revolves around its ability to sustain profit margins. The acquisition of AspenTech, while intended as a growth opportunity, has recently faced challenges that could lead some investors to perceive it as a potential liability. If such sentiment persists in the market, there is a risk of a notable decrease in the company's stock price, reflecting the prevailing pessimism regarding the acquisition and its impact on EMR's overall performance. Ensuring that the integration of AspenTech aligns with EMR's growth strategy and delivers anticipated benefits will be critical in addressing this risk and maintaining investor confidence. So far it seems that the margins are trending upwards and that is reassuring me that the buy case is still in order.

Net Margin (Macrotrends)

One notable risk factor for EMR, in my assessment, pertains to the effectiveness of their acquisitions and divestitures. The key question here is whether these strategic moves will indeed yield the anticipated growth in the future. Ineffectual acquisitions or divestitures can result in prolonged periods of stagnation for the company, potentially affording competitors a competitive edge. While a slightly higher acquisition price may not be a significant concern over the long term, the paramount consideration lies in the acquired businesses' ability to foster growth and innovation.

{kind=link}

Ensuring that these strategic actions align with the company's growth objectives and translate into tangible benefits will be crucial in mitigating this risk and sustaining EMR competitiveness in the market. What I think will characterize EMR in the next decade is making solid acquisitions based on the market needs and for its clients. AMS for example offers new device data management services and software offerings grew as well.

Final Words

EMR continues to be a very interesting company, as the FCF is expanding quickly and aiding the management in continuing its strategic path of acquiring more and more companies. The quality of the company has been showcased in my opinion and even though there is an earnings premium of around 29% to the rest of the sector, I think the reliability of earnings growth for EMR is justifying this. The company has a decent dividend yield and a good history of buying back shares too. The share price has grown very well since my last article, and despite that, I remain equally if not more bullish on EMR still and will be reiterating my buy.

For further details see:

Emerson Electric: The Buy Case Is Still Very Much In Play