EMR - Emerson Electric: Well-Positioned For A Comeback

2023-10-20 04:33:56 ET

Summary

- EMR has showcased financial resilience and strategic foresight, with strong quarterly performances and a focus on core segments.

- EMR's third quarter earnings exceeded expectations, driven by sales growth in intelligent devices and software and control automation solutions.

- The company's proactive approach to portfolio optimization and alignment with expanding sectors like the EV market position them favorably for long-term growth.

Investment action

Based on my current outlook and analysis of Emerson Electric Co. (EMR), I recommend a Buy rating. EMR has showcased a blend of financial resilience and strategic foresight, underpinned by robust quarterly performances and forward-thinking business decisions. EMR's third quarter earnings surpassed market expectations, reflecting double-digit year-over-year sales growth. This growth is attributed to their operational excellence and a strategic focus on core segments like intelligent devices and software and control automation solutions. Their proactive approach to portfolio optimization, evident in the Copeland transaction and the anticipated NI acquisition, signals a commitment to long-term growth. Furthermore, EMR's alignment with expanding sectors, such as the EV market, and their emphasis on leveraging secular growth trends position them favorably in the evolving industrial landscape. As they navigate the fiscal year, EMR's trajectory suggests a promising blend of growth, innovation, and market adaptability.

Basic information

EMR is a global technology and engineering powerhouse, operating primarily through two pivotal segments. The Automation Solutions segment delivers products and tailored solutions for diverse industries, encompassing oil and gas, refining, and power generation, featuring measurement instruments, valves, and specialized software. Simultaneously, the Commercial & Residential Solutions segment emphasizes energy efficiency and enhanced comfort in homes and businesses, providing heating, air conditioning, and refrigeration solutions. Renowned for its innovative spirit, Emerson remains steadfast in addressing key global challenges, particularly energy efficiency and environmental sustainability.

Over the last half-decade, EMR's trajectory has been marked by both peaks and troughs. The years 2020 and 2021 witnessed a pronounced spike in demand for EMR's offerings as healthcare institutions urgently sought electronic health record systems amidst the COVID-19 crisis. Yet, as the pandemic's intensity waned in 2022, so did this heightened demand, resulting in a revenue contraction for EMR. Compounding these challenges, the global economic landscape is currently navigating through headwinds such as inflation, escalating interest rates, and the ongoing conflict in Ukraine. These factors are inducing a sense of caution among healthcare providers, making them reticent to channel investments into new technologies, including EMR systems.

Review

In the third quarter of 2023, EMR reported adjusted earnings of $ 1.29 per share, surpassing the expectation of $1.09 per share. Their net sales climbed to $3.95 billion, marking a 14% rise from the previous year, a testament to their robust segmental performance. EMR has streamlined its operations and now categorizes its business into two main segments. The Intelligent Devices segment recorded net sales of $2.98 billion, which is an 11% increase year-over-year. Meanwhile, the Software and Control Automation Solutions segment saw a notable surge, with sales reaching $983 million, a 22% jump compared to the same period last year. Overall, the company boasted an adjusted EBITA margin of 26.9%. This commendable sales growth, coupled with margin-boosting price costs and an advantageous product and project mix, highlights EMR's operational excellence.

Underlying orders saw a 3% uptick , primarily fueled by high single-digit growth in the process and hybrid sectors. While there's been a deceleration in demand within the discrete sector, the company remains optimistic. This optimism stems from robust demand and strong underlying growth catalysts, which are projected to steer full-year order growth to the mid-single digits, a result of efficient backlog conversion. This quarter, the company saw a 14% surge in underlying sales, surpassing initial forecasts. This growth was especially prominent in regions like the Americas, Europe, Asia, the Middle East, and Africa. The renewables sector was highlighted as a particular area of strength, with nearshoring driving incremental investments globally in sectors like life sciences, metals, and mining. The company is also seeing forward movement in LNG projects and an increase in customers' energy transition and sustainability budgets. Overall, the market outlook of EMR's clients appears positive, which is expected to provide favorable momentum for EMR's own outlook.

EMR has been making significant strides in its strategic priorities. The company successfully closed the Copeland transaction in May. This move is part of EMR's broader portfolio transformation to optimize its portfolio and focus on core growth areas. The sales are on course to realize annualized cost savings of $100 million by 2024. Secondly, EMR's acquisition of NI is on track to be finalized in the first half of fiscal 2024. Integration planning is underway, and NI shareholders have already given their approval. NI posted its highest-ever quarterly sales, witnessing a 5% increase compared to the previous year, complemented by robust margin performance. The demand landscape looks promising, with an anticipated recovery in the discrete and semiconductor sectors in the forthcoming quarters.

EMR was awarded a significant project with a leading German EV manufacturer to automate the battery cell assembly process. The company's hardware and software solutions are pivotal in R&D, testing, and validation of batteries and vehicles. EMR is poised to expand its factory automation business by leveraging relationships with major EV and battery manufacturers globally. According to recent data , the electric vehicle market is set to achieve a revenue of $561.3 billion in 2023. With an anticipated annual growth rate of 10.07% from 2023 to 2028, the market's value is projected to reach $906.7 billion by 2028. Furthermore, unit sales in the EV market are forecast to hit 17.07 million vehicles by 2028. Given the accelerating and robust growth of the EV sector, EMR's strategic collaboration places them in a prime position to seize a significant market share, potentially enhancing their future revenue.

The expectations for FY2023 have been increased based on the operational execution, with a projection of double-digit underlying sales growth, about 50% operating leverage, and over 20% adjusted EPS growth for FY2023. EMR now anticipates approximately 10.5% year-over-year net sales growth and earnings per share of $3.54 to $3.59. EMR aims to leverage secular growth trends like energy affordability and security, sustainability and decarbonization, digital transformation, and near-shoring. Over 30% of their sales are aligned with these trends, and the company is well positioned with highly differentiated technology and solutions in these areas.

Valuation

I believe EMR can grow at double-digit rates over the next two years, a perspective that aligns with both management guidance and market consensus. Several driving factors bolsters this belief. A noticeable uptick in underlying orders has been observed, and given EMR's optimistic stance on sustained demand and their adeptness at efficient backlog conversion, this upward trend seems poised to continue. The expected surge in the renewables and LNG sectors further amplifies the positive trajectory for EMR. On top of that, the sale of Copeland is projected to yield cost savings by the next fiscal year. As EMR intensifies its focus on core business areas, it's likely to see heightened investments, pushing revenues even higher. The rapid, double-digit ascent of the EV market cannot be overlooked either. With EMR's strategic partnership with a leading EV manufacturer, they are well-positioned to harness the expansive opportunities of this rapidly growing sector.

{kind=link}

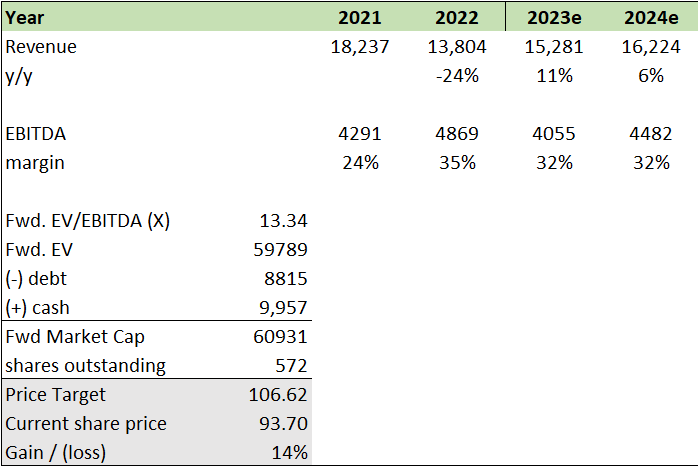

EMR is presently trading at approximately 13.34x forward EV/EBITDA, while its peers Rockwell Automation ( ROK ) and Ametek ( AME ) have a median trading multiple of 17.07x. When it comes to EBITDA margins, EMR stands out with approximately 28%, surpassing its peers' average of around 26%. Furthermore, EMR's anticipated revenue growth rate for the next 12 months is 11%, which is notably higher than its peers' 9%. However, a point of concern is EMR's net margin, which, at about 13%, lags behind its peers' average of approximately 17%. Given that profitability is an important metric for shareholders, it holds significant weight in this analysis. Considering these factors, I believe EMR's current forward EV/EBITDA valuation is justified. My price target for EMR is approximately $106, indicating a potential upside of 14%. Consequently, I recommend a buy rating for EMR. If EMR can enhance its net margins to align with its peers, its forward EV/EBITDA is likely to gravitate towards the industry average, especially given its superior growth prospects and EBITDA margin.

Risk and final thoughts

A potential downside risk to my buy recommendation for EMR is the possible underperformance of the NI acquisition. At present, NI is grappling with supply chain challenges, leading to a 17% decline in sales. Should this trend persist or deteriorate, the acquisition could weigh down on EMR, potentially exacerbating its net margin issues. This could, in turn, lead to a decline in the share price.

In the most recent quarter, EMR showcased strong financial and operational performance, outpacing expectations and demonstrating resilience amidst challenges. Their strategic decisions, including the Copeland transaction and the impending NI acquisition, underscore a commitment to optimizing their portfolio and capitalizing on growth areas. The company's expansion into the rapidly growing EV market, especially their collaboration with a leading German EV manufacturer, positions them advantageously in a sector poised for strong growth. Furthermore, EMR's alignment with secular growth trends, such as energy sustainability, digital transformation, and near-shoring, ensures they are tapping into areas of high demand and potential. With over 30% of sales resonating with these trends and a forward-looking strategy, EMR is well-poised for sustained growth and market leadership. Their upward trajectory in sales, strategic collaborations, and focus on core growth areas make a compelling case for EMR's promising future. Therefore, I recommend a buy rating for EMR.

For further details see:

Emerson Electric: Well-Positioned For A Comeback