EDR:CC - Endeavour Silver: More Share Dilution At Multi-Year Lows

2023-11-14 14:08:47 ET

Summary

- Endeavour Silver reported a sharp decline in Q3 production due to lower grades at its Guanacevi Mine.

- The company's costs soared year-over-year while AISC margins flipped negative, and we saw ~8% share dilution from August to November due to ATM sales.

- In this update we'll dig into the Q3 results, the stock's valuation, and whether this dip is worth buying after a disappointing Q3.

Just six months ago, I wrote on Endeavour Silver (EDR:CA)(EXK), noting that there was no way to justify owning the stock above US$3.50 given that grades were likely to normalize after multiple quarters above reserve grades and catch-up in sustaining capital which would pressure unit costs. Simultaneously, the sharp rise in the Mexican Peso was not helping the H2 margin outlook, and the stock wasn't offering any margin of safety with the stock trading at ~1.1x P/NAV. In the update, I noted that Capri Holdings (CPRI) was the better bet at US$37, trading at barely 6x forward earnings. Since then, Endeavour's share price has plunged 40% and Capri Holdings has gained 45%, but EXK's valuation has not improved as much as it should have given that we've seen continued share dilution at unfavorable prices. In this update we'll dig into the Q3 results, the stock's valuation, and where the stock's updated buy zone sits.

Terronera Project - Company Website

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q3 Production & Sales

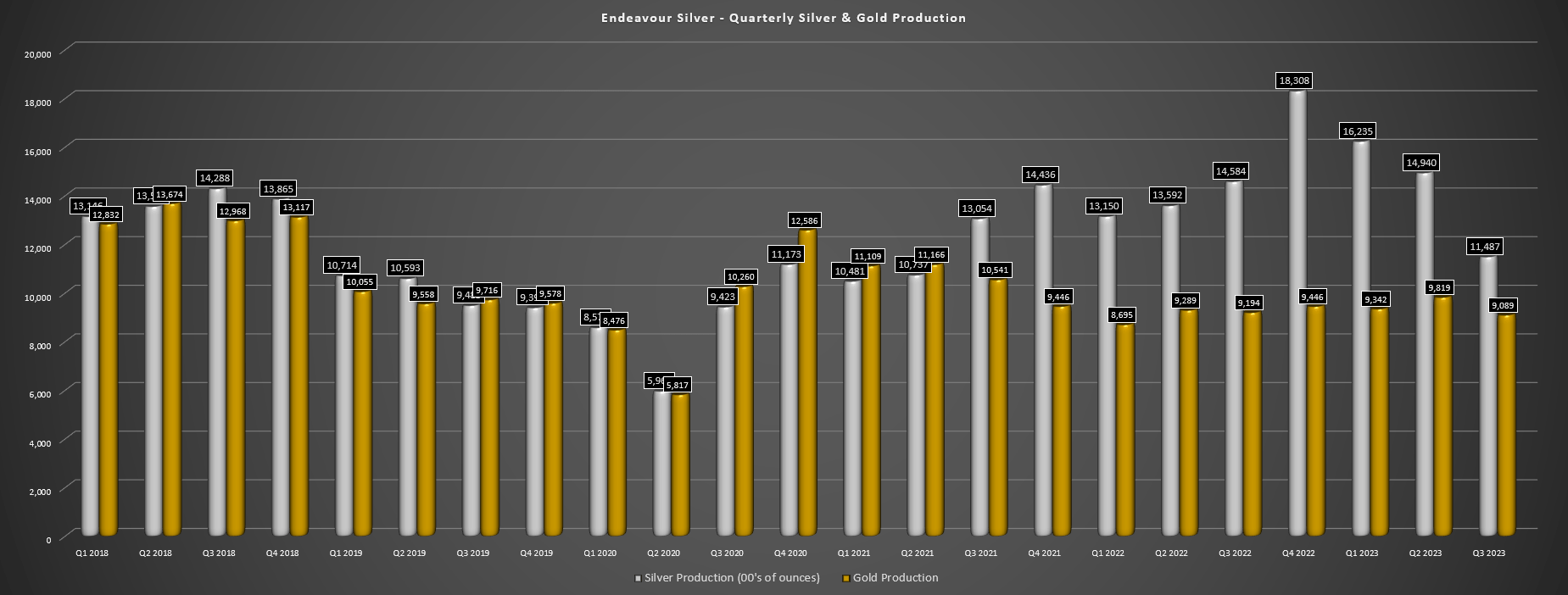

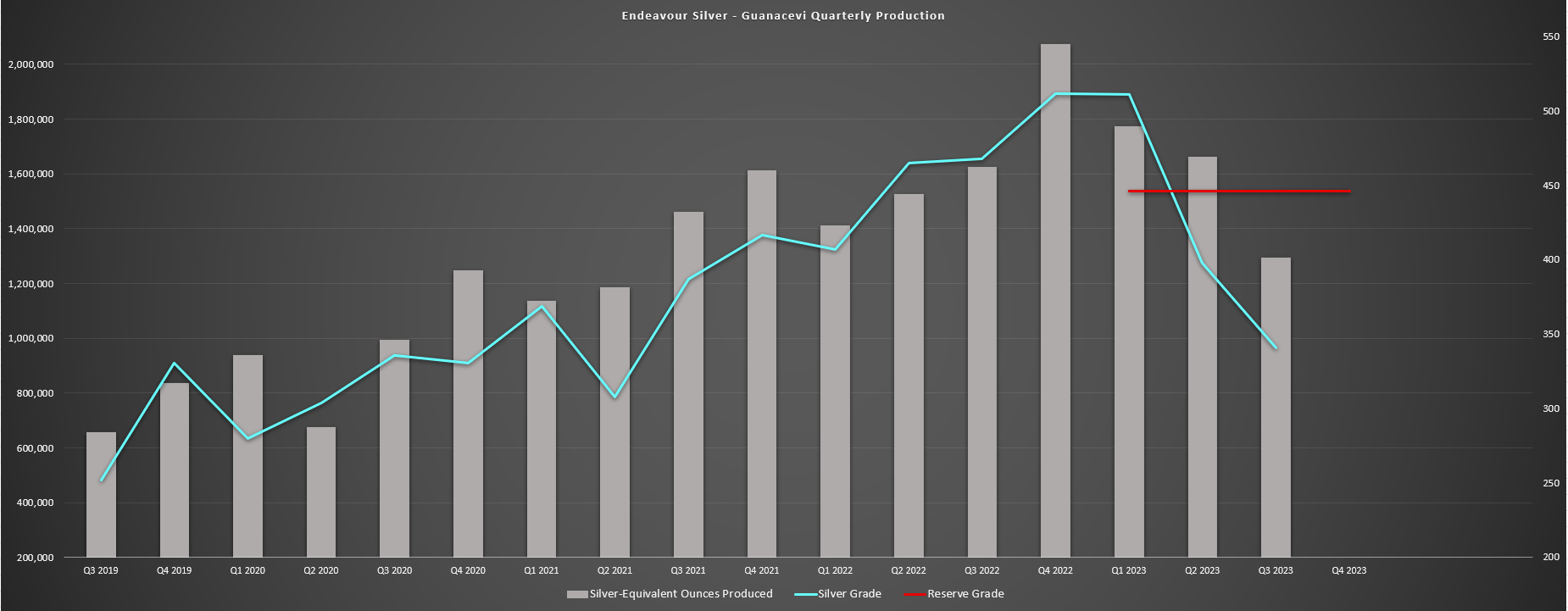

Endeavour Silver ("Endeavour") released its Q3 results last week, reporting quarterly production of ~1.15 million ounces of silver and ~9,100 ounces of gold, translating to a 21% and 1% decline in production year-over-year, respectively. The bulk of this production decline can be attributed to the company's larger Guanacevi Mine, where silver-equivalent ounce [SEO] production plunged 20% due to sharply lower grades (341 grams per tonne of silver vs. 468 grams per tonne of silver in Q3 2022) after an already tough Q2 due to not being able to mine one of its high-grade stopes. This result was especially disappointing given that the company has guided for grades to stabilize in Q3 and Q4 and be "slightly below Q1" . However, due to mine sequencing changes to make progress in improving working conditions (better ventilation and water management with higher water inflow than planned into El Curso), grades actually came in 33% below Q1 levels.

Endeavour Silver - Quarterly Silver & Gold Production - Company Filings, Author's Chart Guanacevi SEO Production - Company Filings, Author's Chart

{kind=link}

{kind=link}

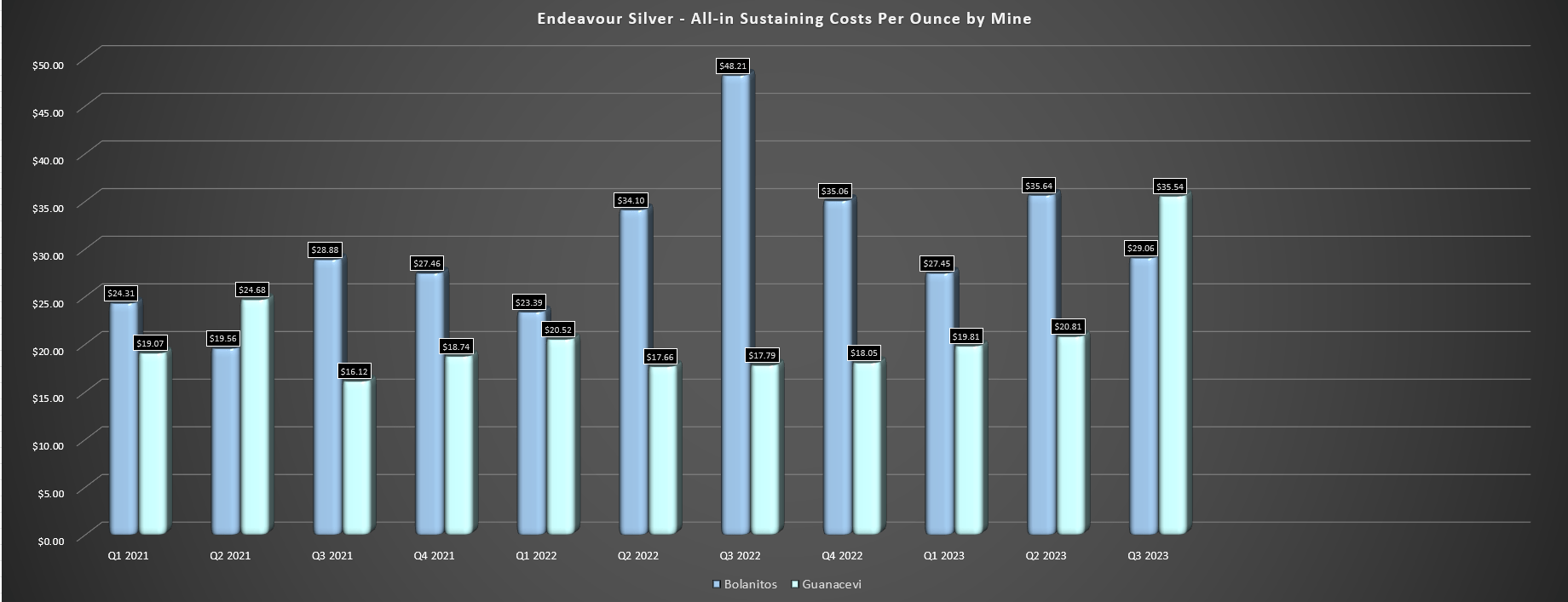

Not surprisingly, the lower grades had a significant impact on overall production and unit costs, with production coming in at ~1.29 million SEOs, a 20% decline from the year-ago period. Meanwhile, all-in sustaining costs [AISC] at the mine soared to $29.06/oz (+63% year-over-year) despite the benefit of lower sustaining capital in the period. On a positive note, these changes should improve mine productivity longer-term at Guanacevi, and the company has already seen an improvement in mine productivity in Q4. According to the company, work completed in Q3 and into Q4 should allow for a consistent throughput of 1,200 tonnes per day next year, up from an average throughput of ~1,160 tonnes per day year-to-date. However, from a negative standpoint, direct operating costs per tonne at Guanacevi continue to rise and are sitting over 11% above 2022 costs year-to-date, which is lapping a 15% increase in costs last year.

Guanacevi & Bolanitos - All-in Sustaining Costs - Company Filings, Author's Chart Guanacevi Annual Operating Costs Per Tonne - Company Filings,

{kind=link}

{kind=link}

Digging into costs at Guanacevi a little further, year-to-date costs at Guanacevi are considerably higher at ~$187/tonne, up from ~$166/tonne in the same period last year and ~$168/tonne in FY2022. Some of this can be attributed to the production shortfall of ~400,000 ounces vs. the annual mine plan, but this is also despite Q1 benefiting from very elevated grades relative to reserves (511 grams per tonne) and also benefiting from the MXN/USD being above 18/1 for nearly all of Q1 vs. lower rates currently. This is not ideal when it comes to reporting reserves next year and could create a higher hurdle, given that current resource/reserve cut-off grades are between 207 to 254 depending on the zone which doesn't leave much wiggle room relative to direct operating costs per tonne of $180.00+. Hence, it's tough to be optimistic about reserve growth at Guanacevi this year.

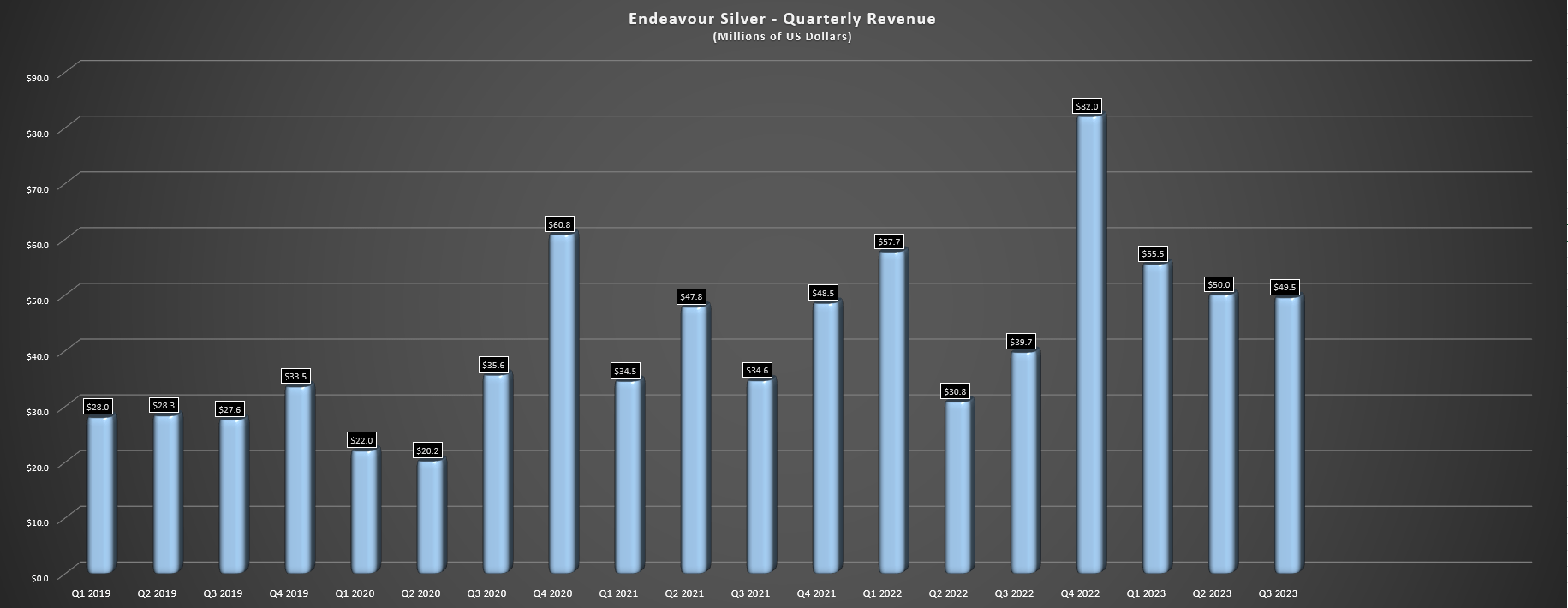

EXK Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Moving over to the company's financials, Endeavour reported a 24% increase in revenue to $49.5 million, but this was entirely driven by help from metals prices. Unfortunately, operating cash flow sunk to $3.3 million in the quarter and the company reported an adjusted net loss of $7.3 million. Worse, cash flow and revenue per share will be impacted going forward on a per share basis due to ~8.2 million shares sold under the company's ATM in the quarter at US$2.85, with an additional ~6.8 million shares sold at US$2.44 subsequent to quarter-end. The only silver lining is that Terronera continues to progress well (38% complete, engineering at 97%) and with this future mine set to be a free cash flow machine (~4.0 million ounces of silver per annum at sub $6.00/oz AISC even when incorporating inflationary pressures), the continuous share dilution might finally be in the rear-view mirror once it's closer to first production.

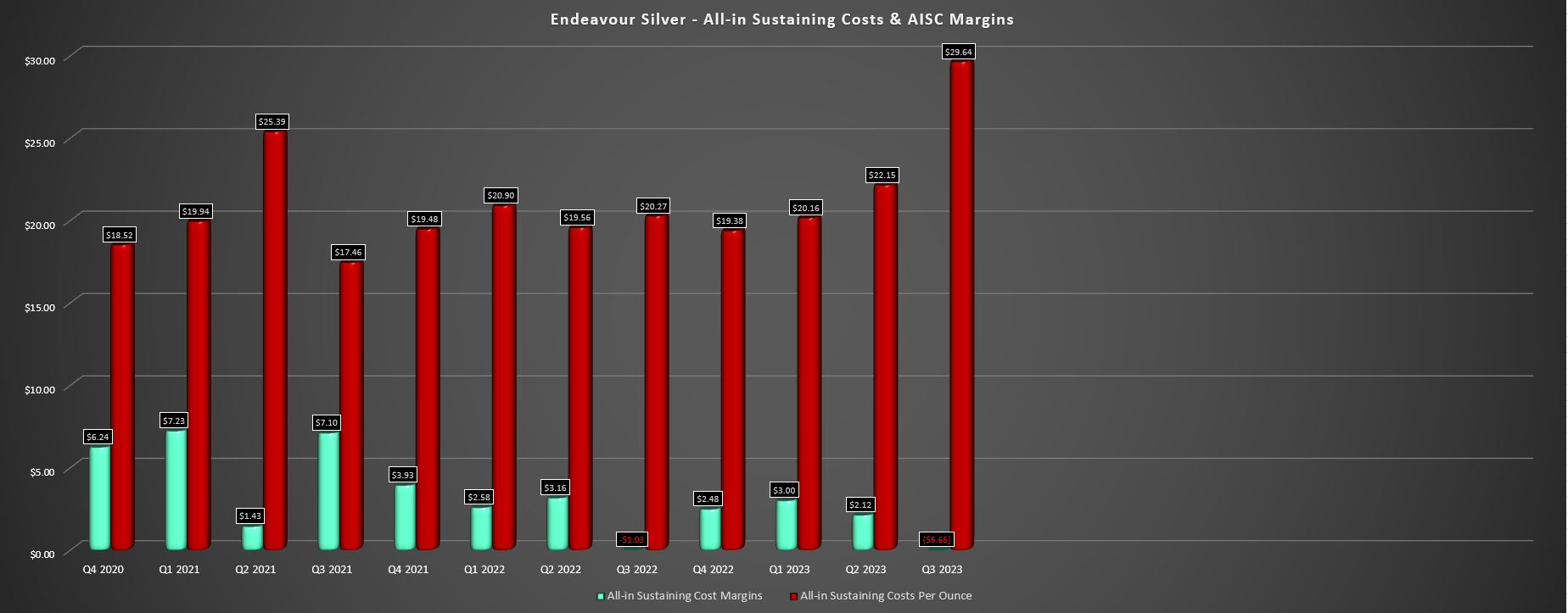

Costs & Margins

Unfortunately, the impact of a lower denominator put a severe dent in Endeavour's costs and margins, with the company reporting a 46% increase in all-in sustaining costs and a 70% plus increase in cash costs to $29.64/oz and $17.94/oz, respectively. Endeavour attributed the soaring costs to increased mine development, elevated third-party ore purchases, lower productivity and higher repair costs, plus higher labor/consumables costs relating to the impact of the stronger Mexican Peso. The result was that despite lapping easy comparisons because of depressed metals prices last year that contributed to negative AISC margins in Q3 2022 ($1.03/oz), AISC margins actually worsened year-over-year to -$5.65/oz. And while costs will improve sequentially after a kitchen sink Q3, I would be surprised to see FY2024 AISC below $21.50/oz next year if the USD/MXN continues to hang out below 18/1.

"If we can maintain our production profile, it will allow us to meet guidance from a cost standpoint, and our all-in sustaining cost is expected to be between $19 and $20 this year. That's probably going to be a little bit higher next year because of the inflation factors, but we'll come out with that guidance in January."

- Endeavour Silver CEO, Dan Dickson, Q3-23 Conference Call

EXK AISC & AISC Margins - Company Filings, Author's Chart

{kind=link}

While the recent quarterly results were certainly discouraging, Terronera will be a game-changer for the company from a margin standpoint, and the company hopes to be nearly half-complete from a construction standpoint by year-end. In fact, Endeavour will own one of the highest-margin silver mines for 2026 in its first year of full production, helping to drag down company-wide AISC. That said, and as I've highlighted in past updates, we may be inching closer to the first pour, but the ramp-up won't happen overnight, meaning that the real benefits in the financial results will show up starting in Q2 2025, not Q4 2024 when first pour is expected. Let's look at the stock's valuation below and see where the stock's updated low-risk buy zone lies after another quarter of share dilution.

Valuation

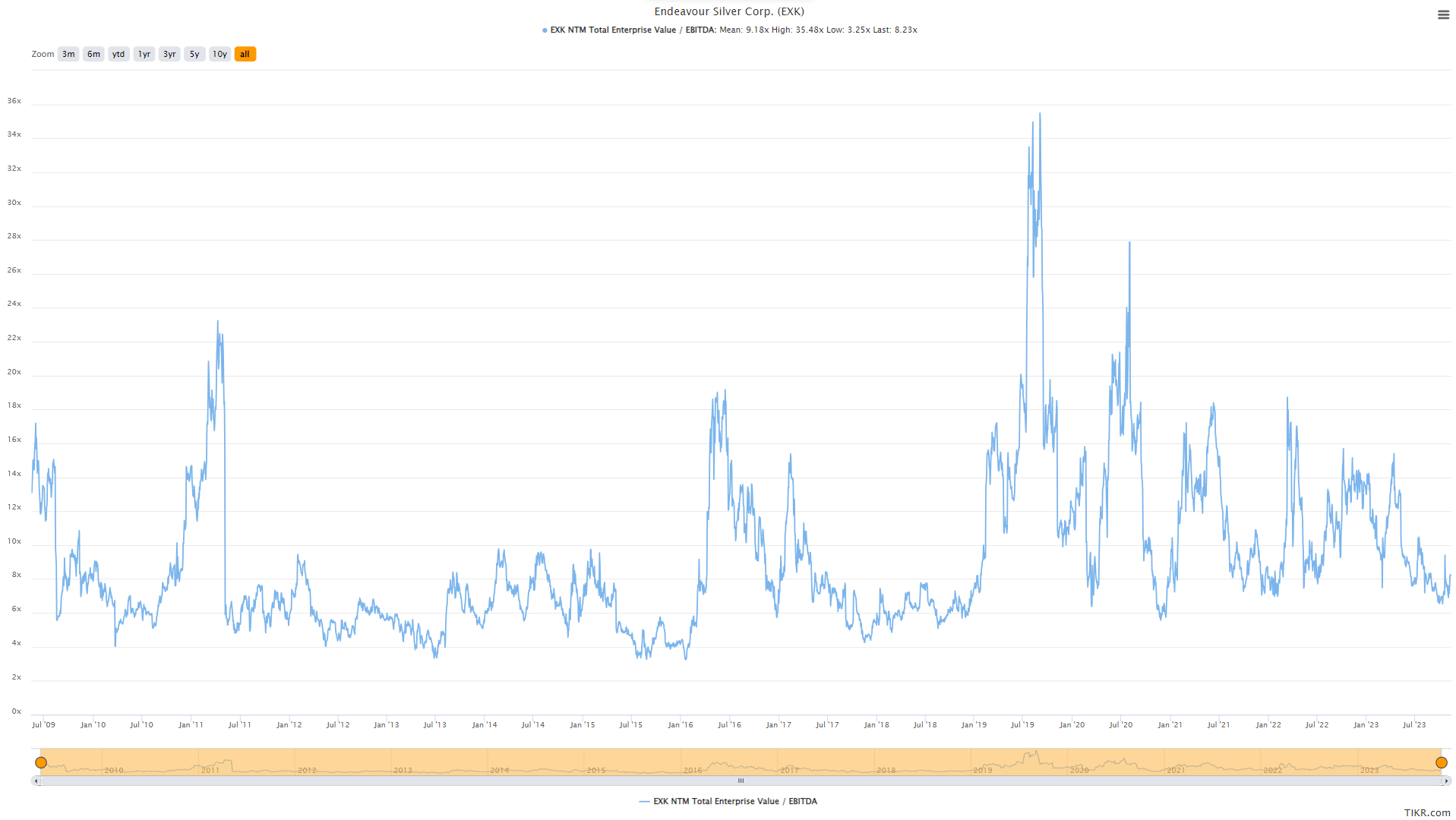

Based on ~212 million fully diluted shares and a share price of US$1.98, Endeavour trades at a market cap of ~$420 million and an enterprise value of ~$390 million, comparing favorably to an estimated net asset value of ~$550 million. This leaves the stock trading at 0.76x P/NAV, which is one of the largest discounts to net asset value that the stock has traded at in years, which can likely be attributed to the declining investment attractiveness for Mexico, some potential loss in confidence from investors because of consistent share dilution, and the multiple compression we've seen sector-wide due to negative sentiment. In fact, while EXK may be cheap on an absolute basis vs. its historical multiples, I still don't see it as cheap relative to what else is available, with names like i-80 Gold (IAUX) trading at less than ~0.35x P/NAV at a higher discount rate in a top-3 ranked jurisdiction (Nevada). Meanwhile, in the royalty/streaming space, Sandstorm Gold (SAND) trades at a similar multiple with superior diversification and margins (~80% gross margins).

Endeavour Silver - EV/EBITDA Multiple - TIKR.com

{kind=link}

Fortunately, Endeavour Silver is progressing towards a transformation with its Terronera Project nearly 40% complete, and I don't think it's unreasonable to expect the stock to trade at 1.2 P/NAV or higher (still a discount to its historical multiple) once the mine comes online in Q4 2024. So, even if we assume a higher share count of 220 million shares (this assumes more share dilution until Terronera moves into commercial production), I see a fair value for the stock of US$2.65. That said, I am looking for a 40% discount to fair value to justify starting new positions in high-cost producers, and while Endeavour may be set up for an eventual upside re-rating, investors may have to wait until Terronera construction is complete and could see the negative news of more share dilution in the interim. Hence, I would need a pullback below US$1.60 to become interested in the stock from a swing-trading standpoint.

Given this downgrade in the low-risk buy zone from my previous update (related to continued share dilution and potential for further share dilution in Q4), I exited my position last week at US$2.07 for break-even from my entry at US$2.07.

Summary

Endeavour Silver had a rough Q3 operationally, made worse by significant share dilution. This was evidenced by nearly 8% share dilution from August to November (~191.5 million shares to ~206.5 million shares), and it's hard to rule out further share dilution between now and commercial production at Terronera, especially if the silver price remains below $24.00/oz. Meanwhile, the sharp increase in costs year-to-date is not ideal and could affect reserves at Guanacevi, with the current cut-off grades looking quite low given the sharp increase in operating costs per tonne year-over-year with little help from the silver price. Finally, while Guanacevi will be back on track in 2024, EXK has noted that costs could be negatively impacted next year because of inflation factors, suggesting there could be several weak margin quarters left on deck until Terronera ramps up to commercial production in Q2 2025. Hence, I wouldn't expect a meaningful improvement in sentiment unless the silver price can get back above $26.00/oz and stay there.

So, what's the good news?

For investors willing to be patient, EXK has better days ahead even if we could see more share dilution in the near term, and this means that any pullbacks below US$1.57 could provide a solid entry into the stock for the eventual turn in sentiment when Terronera comes online. Obviously, there's no guarantee that the stock will drop this low, but I prefer to pay the right price or pass entirely, and I continue to see more attractive bets elsewhere in the sector for now. To summarize, I remain neutral on EXK short term, but I would strongly consider going long the stock on any pullbacks below US$1.60.

For further details see:

Endeavour Silver: More Share Dilution At Multi-Year Lows