PPL:CC - Energy Income Weekly: Guiding For Growth In 2023

Summary

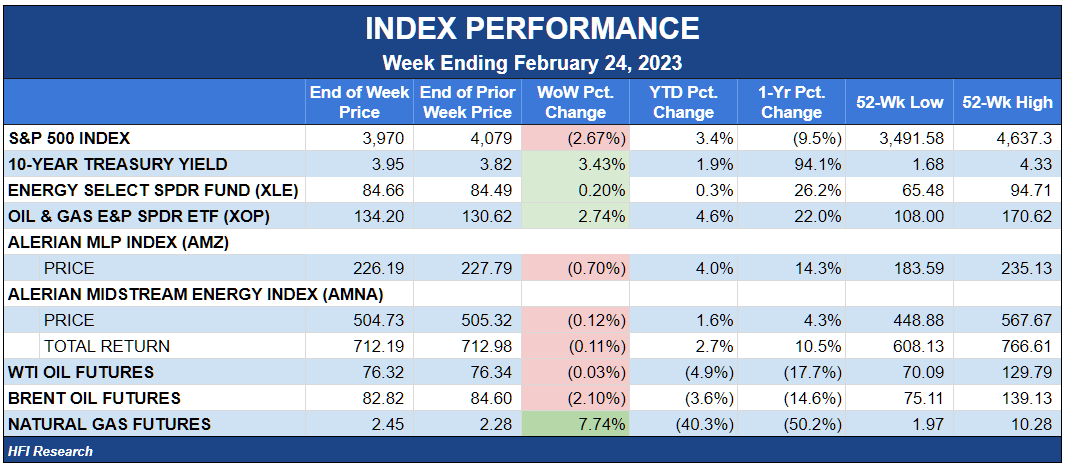

- Energy income equities were largely flat in an ugly week for the stock market.

- Fourth-quarter earnings results and forward guidance continue to come in strong.

- Cash flow growth is offsetting the headwind of rising interest rates.

Energy Income Performance

Energy income equities held up well during the worst week for the market this year. In previous weeks, the market had gotten ahead of itself in its enthusiasm that inflation had moderated. But as data has pointed to inflation persisting amid a resilient economy, interest rates rose, and market prices fell. With the Federal Reserve now likely to continue increasing interest rates, stock prices remain at risk.

{kind=link}

Energy income equities - many of which have built-in inflation resistance - are a good haven in these times. Fourth-quarter earnings have come in strong due to increasing commodity flows. Importantly, in many cases, full-year 2023 guidance has exceeded consensus expectations. With companies entering the year with rehabilitated balance sheets and guiding for higher free cash flow, the prospect of increasing dividends provides support for equity prices in an environment of rising interest rates.

Fourth-quarter earnings continue to come in strong. Most companies we cover have guided to growth in 2023, with many guiding above consensus.

This week, The Williams Companies, Inc. ( WMB ) reported Adjusted EBITDA of $6.4 billion, representing a 5% beat versus consensus. WBM’s stock price failed to react to the positive report even though there are reasons to be optimistic for WMB shares. Management guided for 3% growth in 2023, in line with expectations. However, we believe Adjusted EBITDA should get a bigger boost in 2024 and 2025 as Transco expansion projects and Gulf of Mexico add-on projects come online. Adjusted EBITDA over that timeframe should track above $7 billion, which would bode well for the share price.

In Canada, Enbridge ( ENB ) announced results at the high end of management’s guidance range and reaffirmed 2023 guidance. Pembina Pipeline’s ( PBA ) results beat expectations due to the outperformance of its marketing segment. The marketing performance was dependent on higher natural gas and NGL prices and isn’t likely to be repeated in 2023. Still, PBA's 2023 prospects are good due to increasing oil, natural gas, and NGL volumes from the Western Canadian Sedimentary Basin. PBA remains our favorite Canadian midstream equity due to its conservative management and growth prospects.

Equitrans Midstream ( ETRN ) reported $271.3 million of Adjusted EBITDA, in line with expectations. ETRN’s Mountain Valley Pipeline ((MVP)) remains in limbo, and of course, its financial prospects hinge on the pipeline’s completion, as shown in the following excerpt from its fourth-quarter earnings press release.

{kind=link}

Source: ETRN Q4 2022 earnings press release , Feb. 21, 2023.

ETRN has taken on significant debt to fund the MVP’s construction. Its cash flow will be consumed by expenses related to the MVP and debt service costs if the pipeline project is canceled.

Crestwood Equity Partners ( CEQP ) was the standout underperformer, reporting fourth-quarter results that missed expectations. The miss wasn’t surprising given the company’s vulnerability to weather-related issues. Guidance for 2023 also missed expectations.

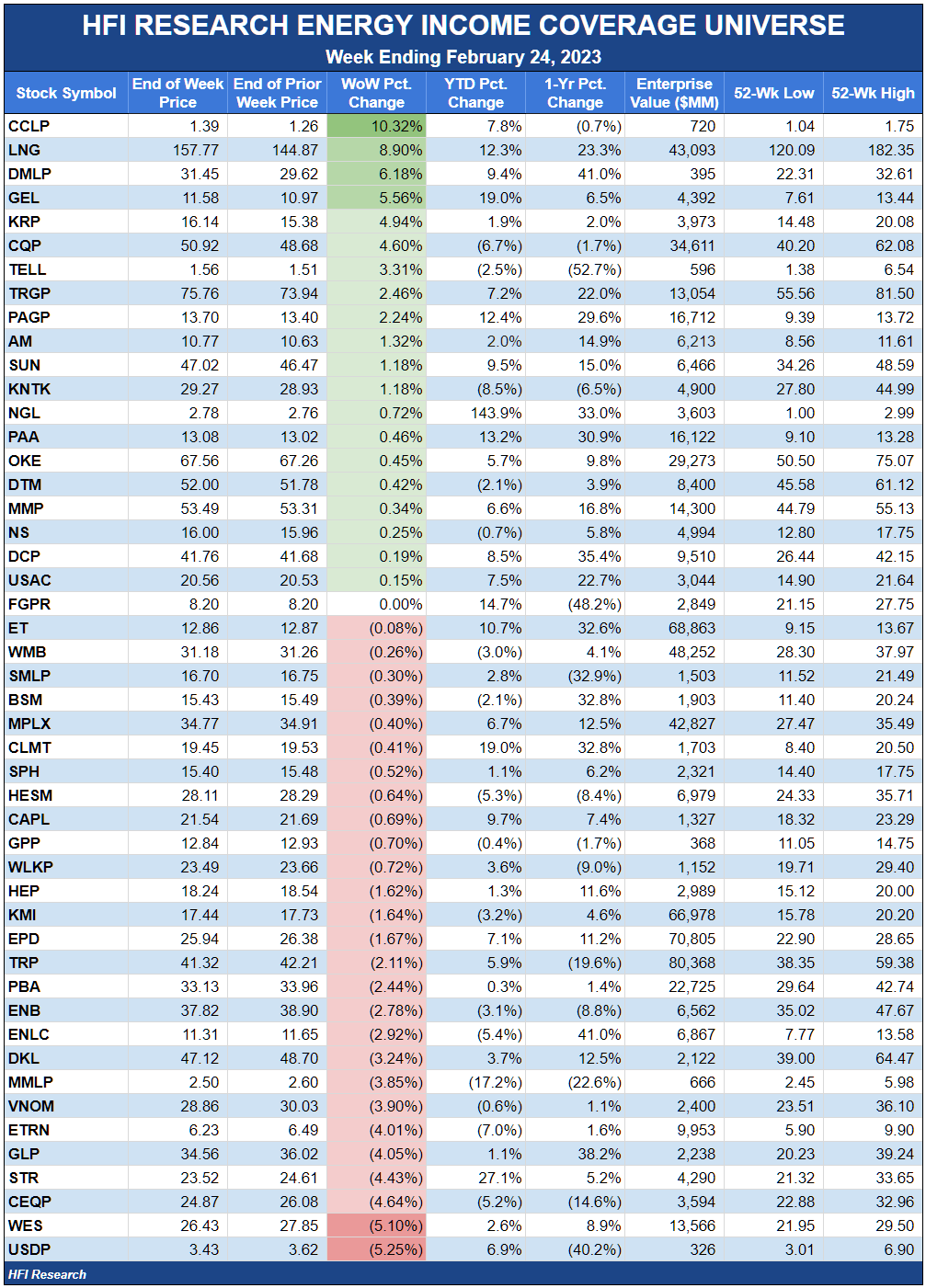

Weekly HFI Research Energy Income Portfolio Recap

It was a busy week for our portfolio, with five of our holdings reporting fourth-quarter results. We cover each in turn below.

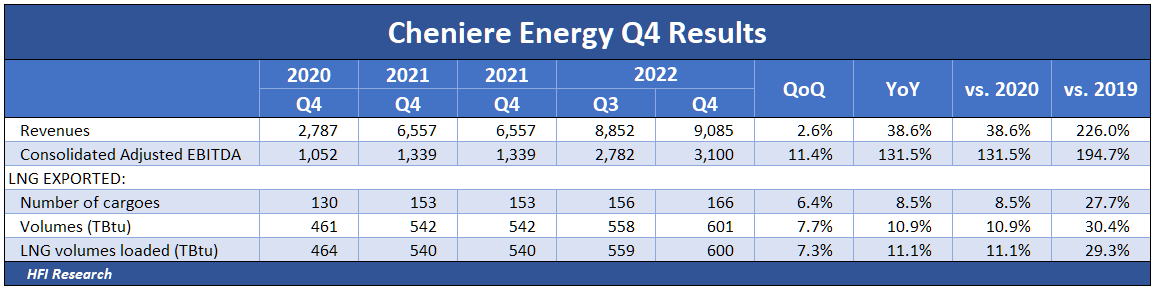

Cheniere Energy: Beat

Cheniere Energy ( LNG ) is the gift that keeps on giving on both the operating and financial fronts. Cheniere announced fourth-quarter Adjusted EBITDA of $3.10 billion versus analyst consensus expectations for $3.02 billion, for a 2.6% beat. During the quarter, the company paid down $2.2 billion of debt and repurchased 4.4 million shares for $700 million. It also won an investment grade rating of BBB from Standard & Poor’s in November.

{kind=link}

The news helped send Cheniere’s stock up 8.9% for the week, the best gain among our holdings.

Full-year 2023 guidance was for $8.25 billion versus Adjusted EBITDA of $11.6 billion in 2022. The guidance shows the company’s financial resilience amid plunging LNG prices.

The big surprise was management’s announcement of expansion programs for Cheniere’s Sabine Pass and Corpus Christi liquefaction facilities. Management had alluded to the possibility of further expansion in previous earnings conference calls but is now taking concrete steps toward contracting and development. The Sabine Pass expansion involves 20 million tons per annum (mtpa) to the facility’s current capacity of 30 mtpa. The Corpus Christi expansion involves an additional 10 mtpa of capacity to its existing 15 mtpa.

Genesis Energy: Beat

Genesis Energy ( GEL ), our newest holding, reported earnings as well. The units were our portfolio’s second-best performer, up 5.6% during the week. We increased our position earlier in the week, as detailed here . GEL beat consensus Adjusted EBITDA of $171 million for the fourth quarter with Adjusted EBITDA of $180.2 million, though management had pre-reported a result in that ballpark. Management noted that fourth-quarter Adjusted EBITDA was negatively impacted by $10 million during the quarter due to unplanned downtime for a Gulf of Mexico customer.

Full-year 2022 was a barn-burner for GEL, with management having raised its Adjusted EBITDA guidance three times and the company’s final $717.1 million full-year result beating management’s most recent upward revision. GEL’s leverage ratio ended the year at a multi-year low of 4.14-times, due in large part to Adjusted EBITDA gains.

Full-year 2023 guidance was 4% above consensus expectations. Management guided to Adjusted EBITDA of $795 million at the midpoint of its range, representing year-over-year growth of 10.9%. Despite the healthy beat, guidance was conservative as management assumed that a global recession will materialize and hurt results throughout 2023. Absent a recession, results should be better than guided.

Management expects to complete its Granger expansion project in 2023. It locked in sales prices for 85% of soda ash sales volumes for the year. It expects to complete GEL’s CHOPS expansion projects in 2024. It expects to keep leverage below 4.0-times and pay down debt with incremental free cash flow.

GEL’s units are likely to remain volatile throughout 2023, but if management can execute as per its guidance, we believe a steady uptick in the units is likely as Adjusted EBITDA increases and leverage comes down. We also believe higher oil prices will be a catalyst for a higher unit price. By the latter months of 2023, as the stock market begins to look to 2024, we expect the unit price to get more traction as capex will fall off dramatically in 2024, accelerating debt reduction and increasing the onset of higher distributions. The timing of both will hinge on management being disciplined with regard to capital allocation.

Black Stone Minerals: Beat

Black Stone Minerals ( BSM ) reported $131.7 million of Adjusted EBITDA, up 7% from the previous quarter and above analyst consensus expectations of $108 million by an impressive 19.4%. The beat was attributable to higher-than-expected production volumes. BSM’s 42,000 boe/d of production during the quarter was a 5% increase over the previous quarter. The company had 108 rigs operating across its acreage, 17% more than were operating in the third quarter. Oil volumes increased due to production in the Bakken and Delaware basins, while natural gas increases were driven by wells coming online in BSM’s Shelby Trough acreage.

Interestingly, BSM saw an improved contribution from its Austin Chalk wells. The company has 18 wells online and has more on the way. Management hasn’t divulged many details about its Austin Chalk activity other than pointing well that had an initial production rate of 1,500 barrels of oil per day. However, management indicated that it had brought in producers on terms more that were unusually favorable for the producers, who were taking a risk on developing the prospective acreage. As producers prove up BSM’s Austin Chalk acreage, it will presumably stimulate additional activity that BSM can develop on better terms for its own unitholders. Management has significant holdings of common units, so we don’t doubt its intention to improve returns to common unitholders. The Austin Chalk offers the advantage of being an oilier play than BSM’s other acreage, which in aggregate was 74% natural gas by production but only 56% natural gas by royalty revenue in 2022. The new play could move the needle in a big way for the company’s profitability if well results remain strong.

Management guided to a 5% increase in production volumes for full-year 2023 versus 2022, though the risk remains that volumes disappoint if natural gas prices remain at today’s sub-$3 levels. Volumes will depend a great deal on the production response to lower prices by Aethon, BSM’s operating partner on its Shelby Trough acreage.

We were pleasantly surprised to hear management guide to a flat $0.475 quarterly distribution in 2023. We expected the distribution to fall, even with BSM being well-hedged for the year. Roughly half of its oil production is hedged at $80 per barrel versus today’s $76. Slightly less than half of its natural gas production is hedged at around $5.15 per mcf versus today’s $2.45.

We were also pleased to hear management all but swear off acquisitions in today’s seller’s market for mineral and royalty interests. BSM had been a very active mineral interest acquirer in previous years when commodity and acquisition prices were low. Today, management is planning on harvesting the value of those acquisitions until asset prices fall back to reasonable levels. Chairman and CEO Tom Carter mentioned that it’s hard to find anything out there with an IRR that approximates BSM’s 12% yield, so they’d rather build up liquidity instead of splurging on an overpriced acquisition.

Targa Resources: Beat

Targa Resources ( TRGP ) reported Adjusted EBITDA of $840 million, a 2.6% beat relative to consensus of $819 million. Full-year guidance of $3.60 billion was above expectations of $3.43 billion.

The biggest news was a 43% increase in TRGP’s dividend, from $0.35 per quarter to $0.50. The significant payout hike leaves excess capital available for funding management’s capital allocation plans, which we suspect involves further expansion. TRGP’s management has proven itself by executing superbly to grow TRGP’s operation in gathering, processing, fractionation, and exporting. It has simplified the company’s balance sheet and reduced leverage to low levels. TRGP management is one of the few in the midstream sector whose expansion initiatives we support.

The dividend hike will probably limit the amount of capital allocated toward share repurchases. This is not a concern for shareholders as we expect TRGP’s shares to trade around their intrinsic value as the market becomes attuned to the company’s growth prospects.

We rate TRGP units a Buy with an $81 price target, but we’d add that our price target is probably too low as it assumes that 2023 Adjusted EBITDA will be $3.0 billion versus management’s guidance of $3.6 billion. We try to make conservative valuations to ensure that our analytical conclusions are sound. In TRGP’s case, we bought our shares at a price that we believe would have generated attractive investment returns if 2023 EBITDA was significantly lower. Fortunately, management has executed above our expectations, and we will circle back and revisit our TRGP valuation shortly.

We plan to hold our shares as long as TRPG management continues to increase intrinsic value for shareholders.

Western Midstream Partners: Miss

Of our 12 holdings that have reported fourth-quarter results, Western Midstream Partners ( WES ) was the only one reporting fourth-quarter results that missed our expectations. WES reported fourth-quarter Adjusted EBITDA of $515.8 million, which also missed consensus estimates of $528 million by 2.3%. WES units were the second-worst performer in our portfolio during the week, down 5.1%.

WES’s main disappointment was management’s guidance for flat Adjusted EBITDA in 2023. We had expected an increase due to the prospect of the company’s anchor customer, Occidental Petroleum ( OXY ), increasing its production activity on WES’s DJ Basin acreage. We expected WES’s full-year 2023 DJ Basin volumes to be flat. Instead, management guided to a decline in WES’ DJ Basin volumes. The volumetric decline will be a drag on Adjusted EBITDA in 2023. However, the negative impact from lower DJ Basin volumes will be offset by higher volumes from WES’s Delaware basin acreage, making for flat Adjusted EBITDA overall.

On the positive side, WES’s board of directors is considering a one-time special distribution of $0.36 per unit, payable to unitholders in May. Another positive was that the company ended 2022 with its leverage ratio at a low 3.1-times.

Fourth-quarter results and guidance indicate that WES units may tread water in 2023. Still, assuming it makes the $0.36 special distribution on top of its $2.00 base distribution, WES units currently trade at an attractive 8.9% distribution yield and remain undervalued. We maintain our $32 price target, which implies 21.1% upside from the units’ $26.43 closing price.

News of the Week

Feb. 21. Crestwood Equity Partners and Brookfield Infrastructure Partners ( BIP ) announced the sale of their Tres Palacios natural gas storage facility for $335 million. The $167.5 million net to CEQP will be used to pay down debt.

Capital Markets Activity

None.

{kind=link}

For further details see:

Energy Income Weekly: Guiding For Growth In 2023