ET - Energy Transfer Acquiring Crestwood Equity Partners Will Rally The Bears But It's A Strong Move

2023-08-17 09:00:00 ET

Summary

- Energy Transfer has agreed to acquire Crestwood Equity Partners in a deal valued at $7.1 billion.

- This will be Energy Transfer's 16th acquisition since 2004 and its fourth since the pandemic.

- The deal expands Energy Transfer's assets and sets the stage for a potential larger acquisition in the future.

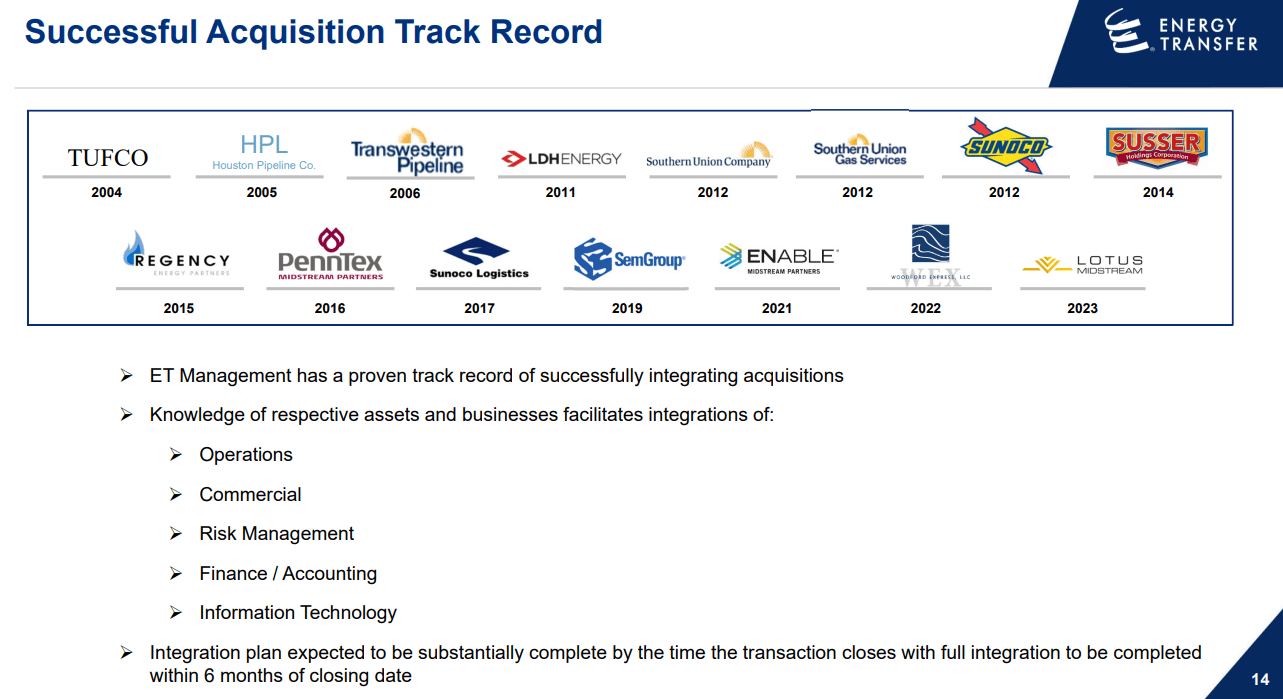

On Wednesday, 8/16/23, news broke that Energy Transfer (ET) agreed to acquire Crestwood Equity Partners (CEQP) deal valued at $7.1 billion. This deal is likely to rally the bears, as I fully expect to see many comments and possibly some articles discussing how Kelcy Warren is back to his old ways. ET has a long history of growing its company through acquisitions, and the CEQP deal will mark its 16th acquisition since 2004. This will be the 4th company since the pandemic that ET has acquired as CEQP will join Enable Midstream, Woodford Express, and Lotus Midstream under the ET umbrella. Looking back to 5/12/21, Kelcy Warren stated that he felt consolidation in the oil industry would accelerate, and that consolidation must occur if companies are going to thrive. This deal shouldn't be a surprise, especially after ET, as management has continued growing through acquisitions while repairing the balance sheet. I am supportive of this deal, as I am looking toward the future. I think this was a setup move for ET as they took a strategic piece off the table and are setting their sights on a much bigger deal in the future.

{kind=link}

This is what Energy Transfer is getting from the Crestwood acquisition, and I think this is a setup move for a bigger acquisition

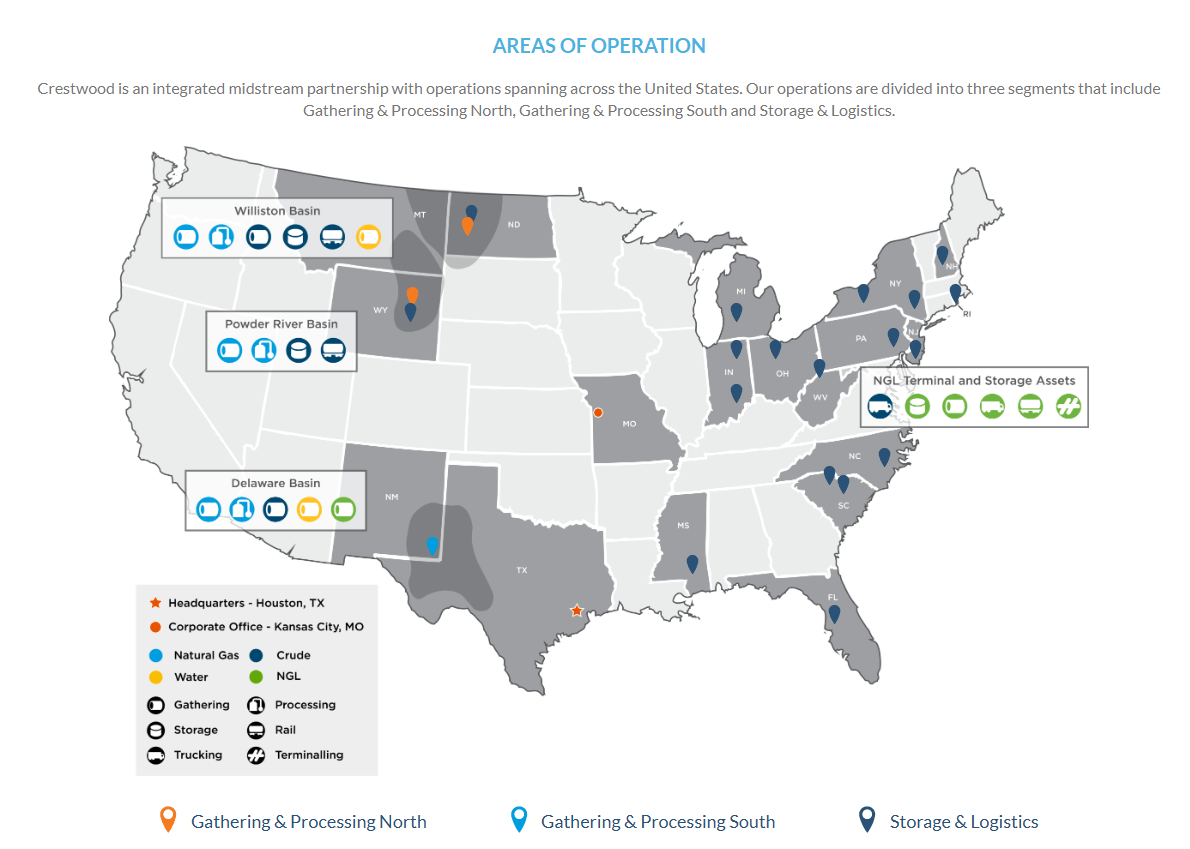

CEQP is an MLP that operates fee-based assets within the energy infrastructure space. CEQP provides solutions across the value chain to accommodate the needs of large-scale upstream producers in the major basins. CEQP owns and operates a large array of assets tied to natural gas liquids (NGLs), crude oil, and natural gas and provides produced water gathering, storage, disposal, and transportation to its partners. These are fundamental needs for any upstream producer.

The three main basins that CEQP focuses on are the Williston, Powder River, and Delaware basins. In the Williston Basin , CEQP provides 420 MMcf/d of natural gas gathering capacity, 250 MBbls/d crude gathering capacity, 421 MBbls/d of water gathering, and 430 MMcf/d of natural gas processing capacity. In the Powder River Basin, they provide 398 MMcf/d of natural gas capacity and 345 MMcf/d of processing capacity. In the Delaware Basin , they provide 1.1Bcf/d natural gas gathering, 90MBbls/d crude gathering, 354 MBbls/d water production, and 613 Mmcf/d of processing capacity. CEQP's NGL assets are mainly on the east coast, with some located in the south. In total CEQP has 13 liquified petroleum gas terminals offering 10 MMBbls of contracted storage and pipeline capacities providing integrated supply and logistical services to producers and refiners. They also have 13 trucking and rail terminals, 500 NGL truck & trailer units, 1,100 railcars, and pipeline capacity to domestic and international markets.

{kind=link}

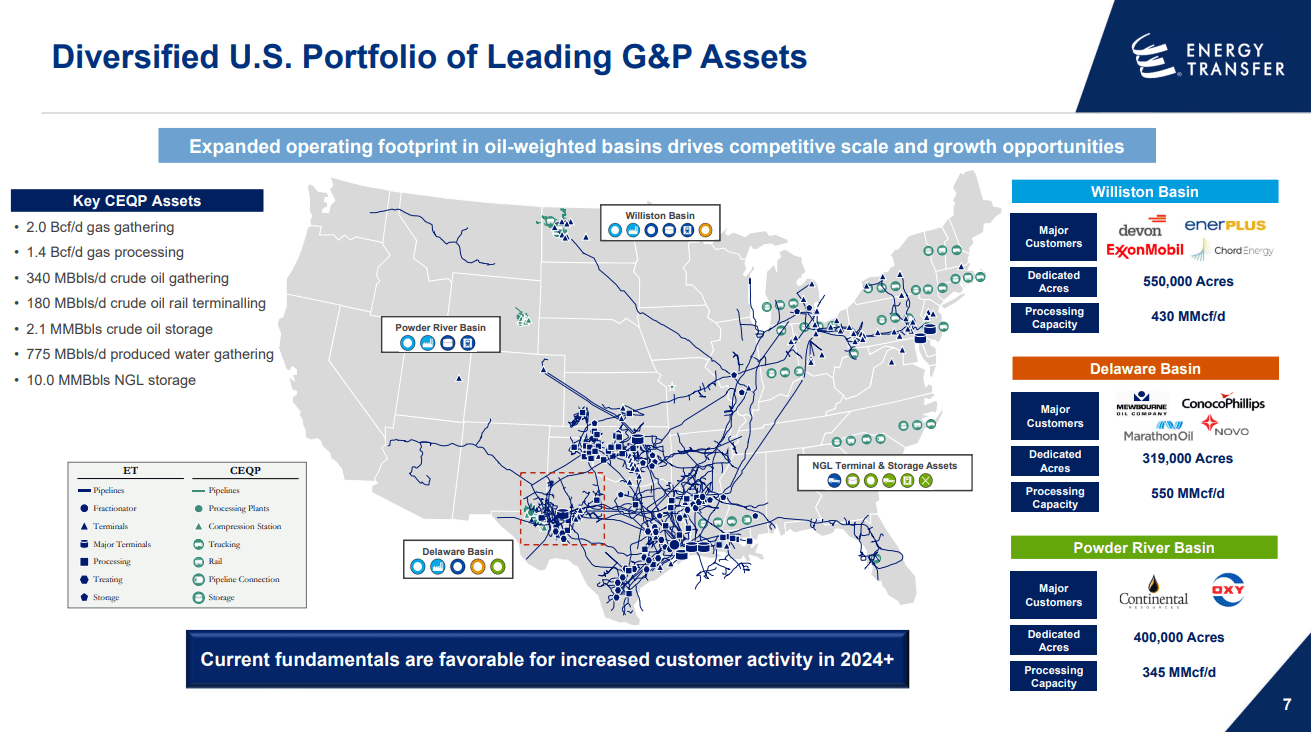

Unlike ET's previous acquisitions, when you overlay CEQP's assets with ET's assets, this is more of an expansion than complimentary. The Lotus Midstream deal provided ET with 3,000 miles of gathering pipelines to its Permian pipeline network and 2 million barrels of storage in Midland Texas. The Enable Midstream deal added significant pipeline mileage in the mid-continent region and made ET the largest processor in the region and the largest transporter by pipeline miles.

Normally we see ET complement its current assets and expand its pipeline extensions. This deal is different as there is a mix of complementary and outright expansion into new areas. ET will complement and strengthen its asset mix in the midcontinent region, and add significant assets in the Williston Basin and in Central America. This deal is opening up new opportunities through expansion as ET will now operate in the Powder River Basin, expand its presence upward throughout the northeast, and establish a foothold in the mid-south.

{kind=link}

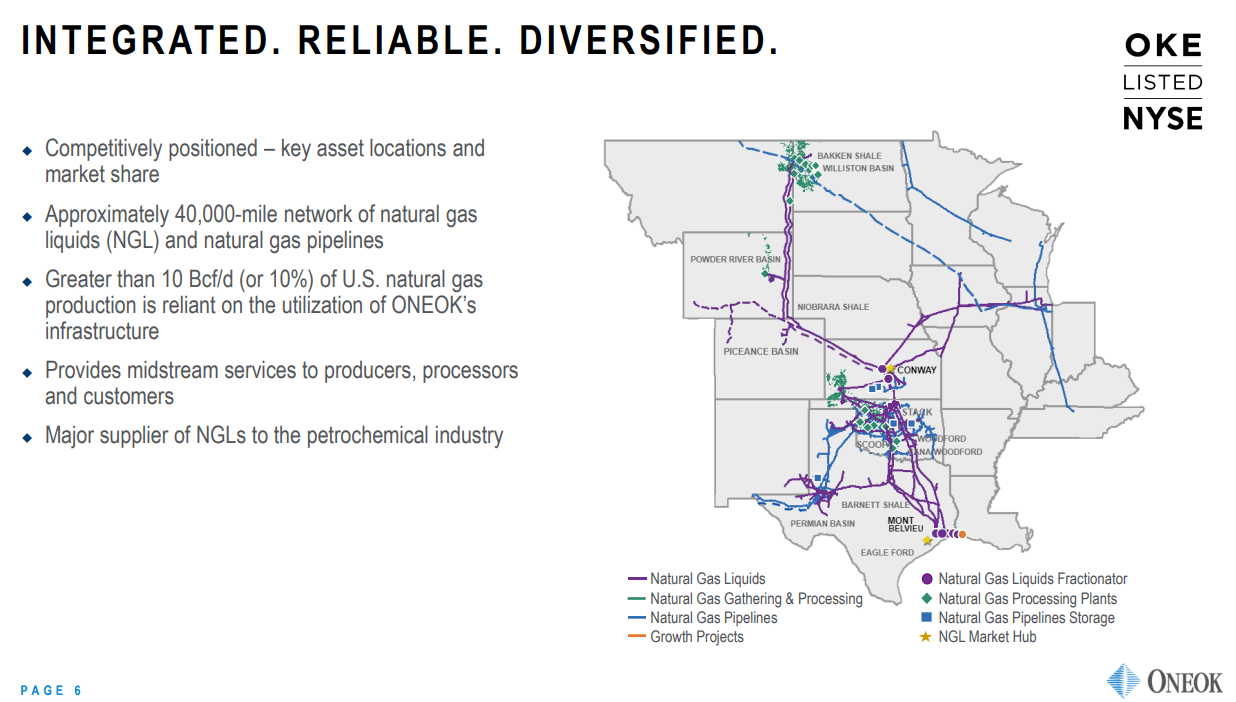

This deal doesn't make sense to me from an asset perspective unless ET is looking to fill out connectivity throughout the east coast or Middle America. From an asset standpoint, this deal is a much larger expansion than we have normally seen, as ET typically has stuck to complementary assets. We know that Kelcy Warren has a track record of growing through acquiring, and has publicly said that companies will need to expand to thrive. I think this deal is a stepping stone for a much larger future deal. I have no knowledge, but I would speculate that if the ONEOK (OKE) and Magellan Midstream Partners (MMP) deal falls through, they will try to acquire OKE. MMP is holding a special meeting to vote on the deal on 9/21/23, and as I outlined in my article on the deal ( can be read here ), there has been a lot of opposition, especially from Energy Income Partners , who own roughly 3% of MMP.

When I look at the combined asset map from ET and CEQP, and then I look at OKE's assets below, it would be a strong strategic move. ET just increased its presence in the Williston Basin and established operations in the Powder River Basin. By acquiring OKE, ET would gain a 40,000-mile network of NGL and natural gas pipeline, but more importantly, significant takeaway capacity from the Williston Basin and the Bakken Shale Basin. ET would also gain much-needed infrastructure for its new assets in the Powder River Basin. I don't think ET is done, and I have a feeling that the CEQP deal is a stepping stone to a large-scale deal that will shock the energy infrastructure space.

{kind=link}

Looking at the numbers from the Crestwood deal

ET has entered into a definitive agreement to acquire CEQP at a $7.1 billion enterprise valuation in an all-equity deal. This deal dilutes unitholders, but ET isn't utilizing any of its cash. While ET is projected to issue 219 million units, they are also adding $3.3 billion of debt to their balance sheet as they assume CEQP's debt in the transaction. The unitholders from CEQP will get 2.07 units for every 1 unit of CEQP in the deal, and it's expected to close in Q4 2023.

Here is what ET is gaining from a numbers' aspect. In the TTM, CEQP has generated :

- $5.52 billion revenue

- $778.1 million Adjusted EBITDA

- $533.3 million distributable cash flow ((DCF))

In the TTM ET as a standalone company has generated:

- $80.76 billion revenue

- $13.08 billion Adjusted EBITDA

- $8.47 billion in DCF

ET has $48.91 billion in total debt on the books, and when they assume CEQP's debt , the total debt will increase to $52.2 billion, which is the same amount of debt ET had in 2020. If the two were a combined entity today, their TTM numbers would look like the following:

Steven Fiorillo, Energy Transfer, Crestwood

ET would increase its revenue by 6.84%, its Adjusted EBITDA by 5.95%, and its DCF by 6.93%. Its margins would decrease by a small fraction, as Adjusted EBITDA would still represent over 16% of revenue and DCF would represent over 10.40% of revenue. ET's total debt to Adjusted EBITDA ratio would slightly increase from 3.74x to 3.77x based on the TTM numbers.

Conclusion

I think the bears will disapprove of this acquisition, and we will see a lot of negative comments on this article and future articles written about ET. From my perspective, I like the deal, and think it's a smart move. ET is assuming the debt and issuing units to fund the remaining portion of the deal and not touching its cash. While the debt will increase on the balance sheet, ET's total debt to Adjusted EBITDA, when looking at ET and CEQP as a combined entity on a TTM basis, doesn't really change much. ET would still be under a 4x ratio, which is a better ratio than we have seen in the past. ET is taking another piece off the table, and I think this is setting the stage for a large-scale deal in the future. ET once again has expanded its relevancy and widened its moat in the midstream space. I think this deal will help change the market's perception and maybe bring a more realistic valuation to units of ET as they continue to be significantly undervalued.

For further details see:

Energy Transfer Acquiring Crestwood Equity Partners Will Rally The Bears, But It's A Strong Move