ET - Energy Transfer Announces Rock-Solid Earnings

2023-11-02 17:07:01 ET

Summary

- Energy Transfer LP reported strong Q3 performance and record volumes in NGL transportation, fractionation, and exports.

- The company updates its financial guidance with adjusted EBITDA of $13.55 billion and massive discounted cash flow of $2 billion for the quarter.

- Energy Transfer's diversified asset portfolio and ongoing capital spending support its ability to drive strong shareholder returns.

Energy Transfer LP (ET) is one of the largest midstream companies in the world and recently released its earnings for the third quarter. The company has a market capitalization of almost $40 billion and a yield of more than 9%. Despite all that, as we'll see throughout this article, the company has the financial strength to drive even higher shareholder returns despite its debt.

Energy Transfer Updates

The company had strong performance as it's continued to focus on its overall business.

{kind=link}

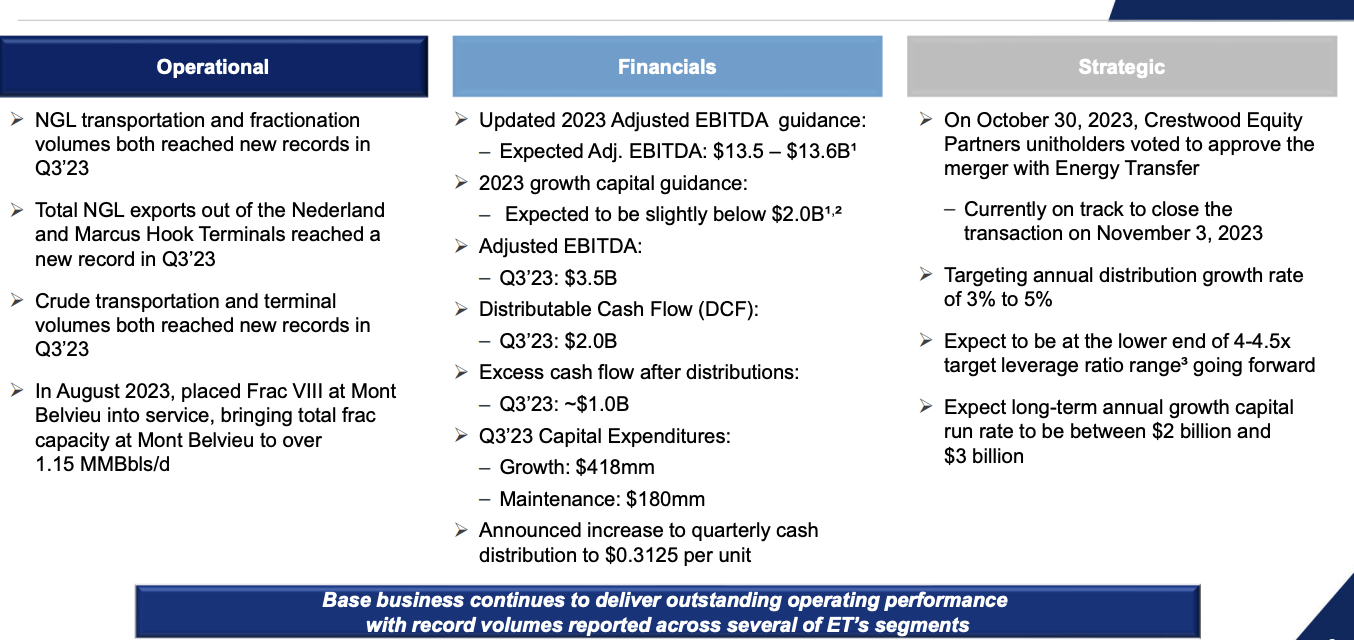

The company's NGL transportation and fractionation volumes reached new records. The company has worked to own every step of the value chain. NGL exports also hit a new record for the company, along with crude transportation and terminal volumes. Mont Belvieu has become a massive development with total fractionation capacity at more than 1.15 million barrels / day.

Financially, the company has updated its guidance to a midpoint adjusted EBITDA of $13.55 billion. Growth capital is expected to come in a hair below $2 billion. The company's adjusted EBITDA for the quarter is at almost $14 billion annualized and discounted cash flow ("DCF") was a massive $2 billion for the quarter, despite the company's interest obligations.

It's worth noting at current interest rates, refinancing the company's debt could add hundreds of $ millions of interest obligations per quarter. The company ended with $1 billion in excess post-distribution cash flow for the quarter, and increased dividends . Capital spending came it at $180 million maintenance and $418 million growth.

Strategically, the company is working to complete its merger with Crestwood Equity Partners (CEQP). The acquisition was financed with all stock, technically, but ~40% of it was debt. It expects it to be closing around now. The company expects to be at the lower end of its leverage ratio going forward, supported by its growing EBITDA while it keeps long-run growth capital high.

Energy Transfer Footprint

The company continues to maintain an incredibly diversified and strong footprint of assets.

{kind=link}

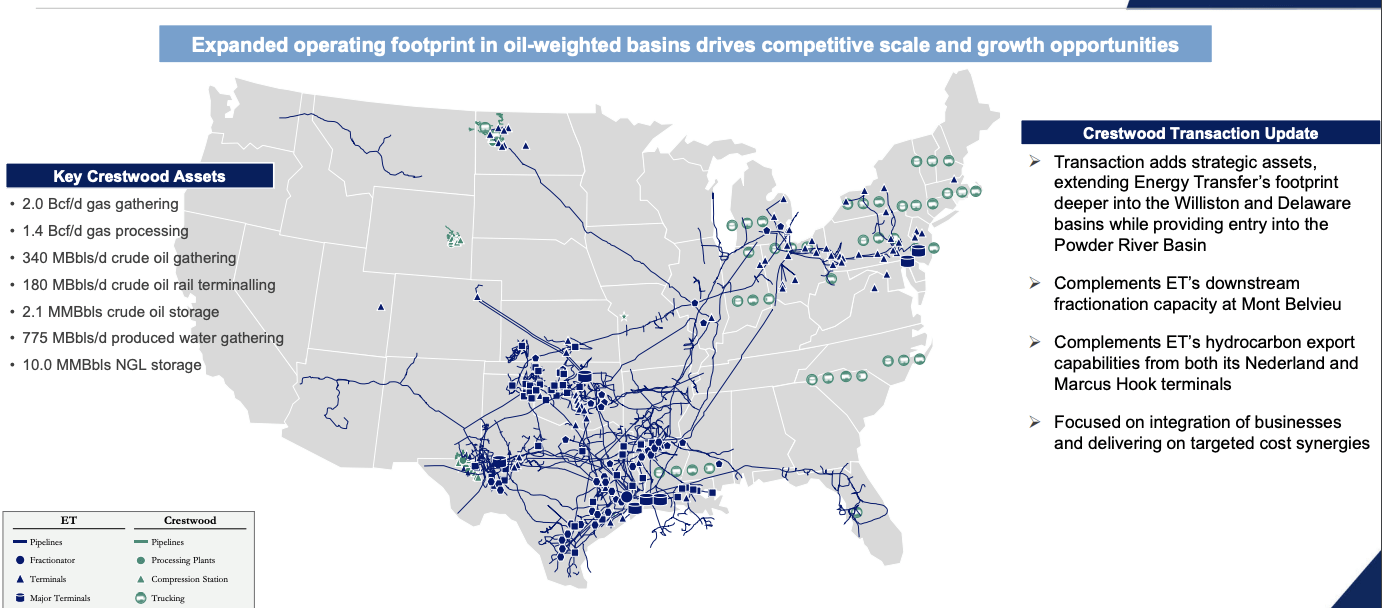

The company's acquisition of Crestwood integrates well with its existing asset footprint. Crestwood has Bcf/day of gathering and processing assets along with substantial crude oil and storage assets. The company's integrated assets here enable strong synergies and higher margins for its existing portfolio of assets.

The company's strong and integrated asset portfolio is the source of both its reliable and growing cash flow.

Energy Transfer Capital Spending

The company's capital spending remains massive, to the tune of roughly $2 billion / year. The company has stopped cutting growth capital and is guiding for long-term growth capital even higher than 2023.

{kind=link}

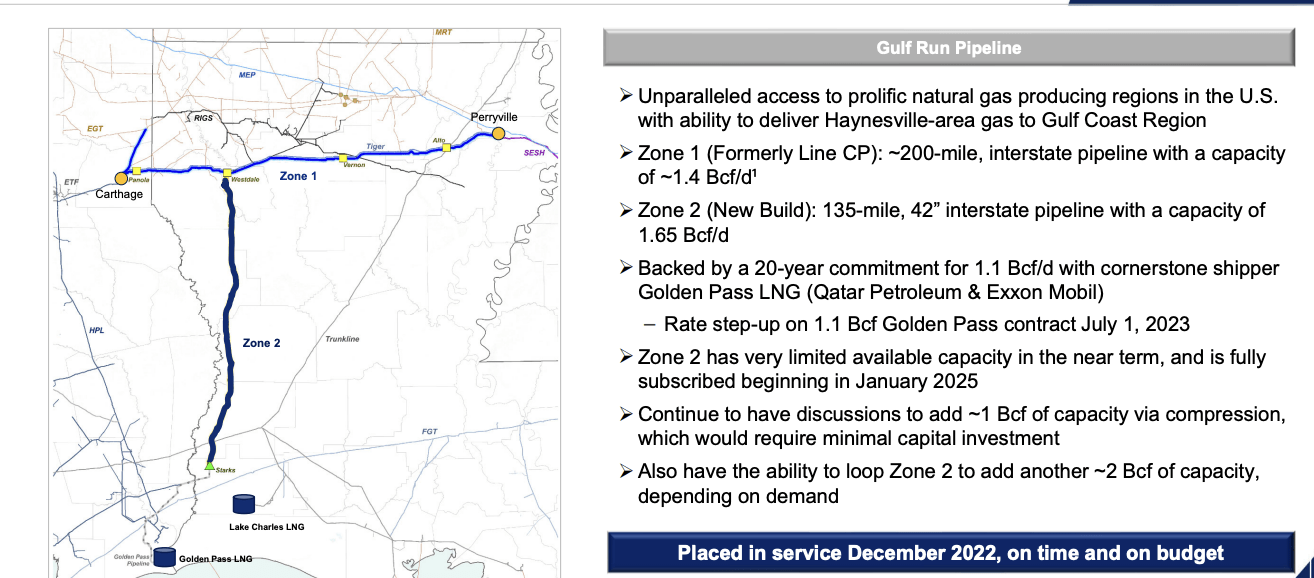

An example of the company's continued growth capital spending is the Gulf Run pipeline. The focus on this asset is to deliver Haynesville area gas to processing centers on the coast. The former line has a new 135-mile 42" pipeline added on with Zone 2. Capacity is expected to be a massive 1.65 billion cubic feet / day.

Almost 70% of that capacity is backed by a 20-year commitment with Golden Pass LNG which just saw a rate step up. Starting January 2025, the pipeline is fully subscribed, and the company is seeing demand high enough that it's investing additional bolt-on capacity additions for 1-2 billion cubic feet / day in extra capacity.

This is high-margin capacity that takes advantage of the company's assets.

{kind=link}

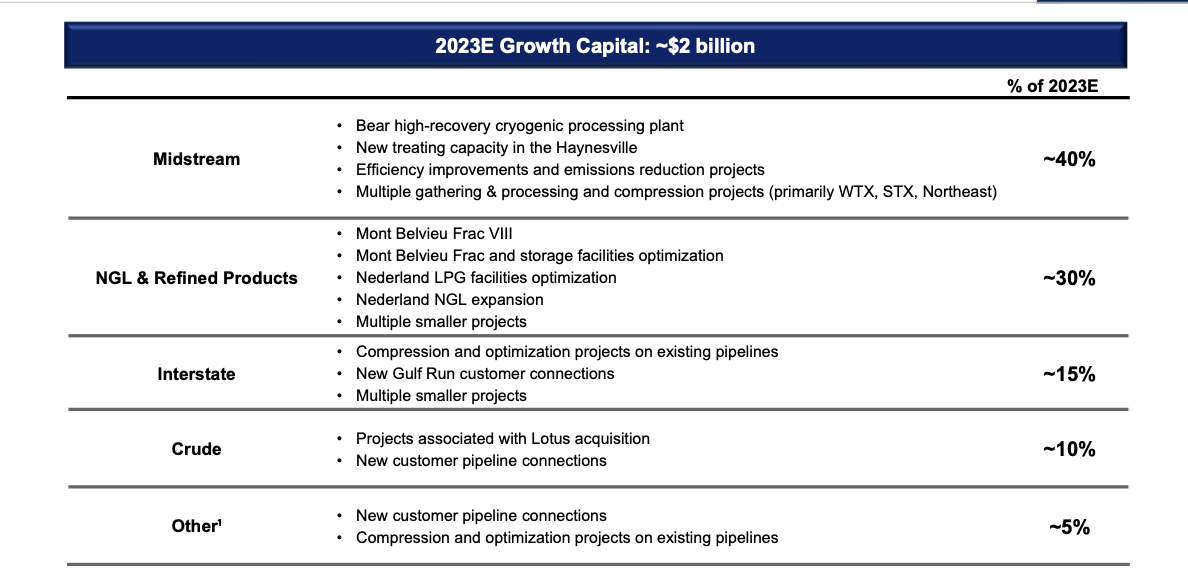

Overall, the company has $2 billion in growth capital. 40% is expected to be allocated towards midstream, while the rest will be allocated to a variety of NGL, refined products, and interstate production. That growth capital is heavily bolt-on capital spending for the company. That will all be projects that have strong margins.

Energy Transfer Shareholder Return Potential

The company has the ability to drive strong shareholder returns from its asset portfolio.

The company has a high debt load despite its strong portfolio of assets. The company's EBITDA based on Q3 annualized is almost $14 billion, and the company is spending heavily on growth capital, to the tune of ~6% of its market capitalization annualized. Even if shareholders don't directly see it, that's long-term growth.

At the same time, only half of its DCF goes towards its dividend yield of more than 9%. That's a comfortable dividend yield that the company is committed to growing at 4% in the long run, which it can comfortably afford. Together, that means that the company can continue to provide shareholders with strong double-digit returns.

Thesis Risk

The largest risk to our thesis is climate change. Energy Transfer is more insulated than most due to its focus on natural gas versus crude oil, which has more staying power. However, that's still expected to change over the upcoming decades, and when it does it could hurt the company's ability to drive cash flow and shareholder returns.

Conclusion

Energy Transfer has once again announced rock-solid earnings. The company's Crestwood Equity Partners acquisition is expected to close soon, helping it out even more. Normally we're not a fan of a heavy equity acquisition, but the debt portion helps to make it up. The company is continuing to pay a dividend of more than 9% and invest in growth.

Together, with the company's 4% long-term dividend growth, 9% dividend, and 6% capital spending, the company is guiding to almost 20% in long-term shareholder returns. Surprisingly, it can comfortably afford those returns. Rising interest rates and climate change present a risk, but we expect the company to navigate that.

For further details see:

Energy Transfer Announces Rock-Solid Earnings