ET - Energy Transfer Offers High Yielding Vehicles For All Investors

2023-11-10 11:34:27 ET

Summary

- Energy Transfer trades at a relative discount to its peers and offers a massive 9.40% dividend yield with preferred yielding over 10%.

- The company has made recent acquisitions, including Lotus Midstream and Crestwood Equity Partners, to expand its pipeline network and customer base.

- Energy Transfer has a strong position in NGL transportation and services and is a major player in hydrocarbon transportation, with over 30% of domestic transport and 40% of export capacity.

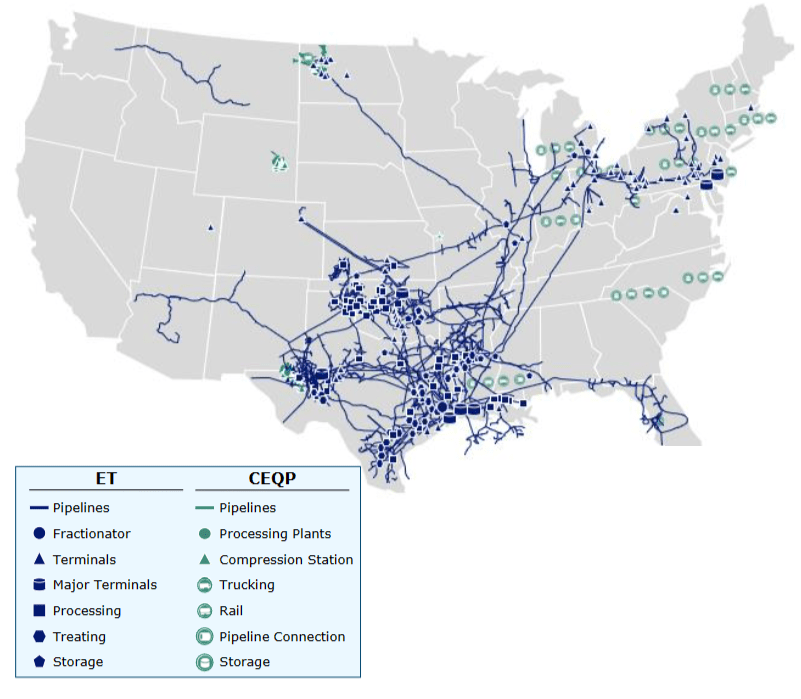

Energy Transfer (ET) is a $90b in enterprise value MLP midstream company with operations all across the US in the gathering and processing of oil, natural gas, and NGLs, midstream services, long-haul intrastate and interstate pipelines, and commodity exports. Much of their business comes from NGL transportation and services and midstream operations. Growing through acquisition, Energy Transfer has become the epitome of hydrocarbon transportation boasting over 30% of domestic transport and 40% of export capacity. Throughout this report, I will discuss recent acquisitions, new market opportunities, and a variety of trading options. I give ET units a BUY recommendation with a price target of $16.06/unit. I also provide a BUY recommendation on their perpetual preferred shares, both series C (ET.PR.C) and series D (ET.PR.D), a buy recommendation at par with a yield of 10.14%.

Acquisitions

Energy Transfer acquired Lotus Midstream on May 2, 2023, for $1.5b, split between $930mm in cash and $574mm in ET units. Lotus Midstream owns the Centurion Pipeline System, a 3,000-mile crude oil gathering and transportation pipeline that extends from southeast New Mexico, through the Permian Basin in West Texas, to Cushing, Oklahoma. This pipeline system's gathering lines extend Energy Transfer's network and provide additional connections to major hubs including Midland, Colorado City, Wink, and new connections in Cushing and Crane.

Corporate Reports

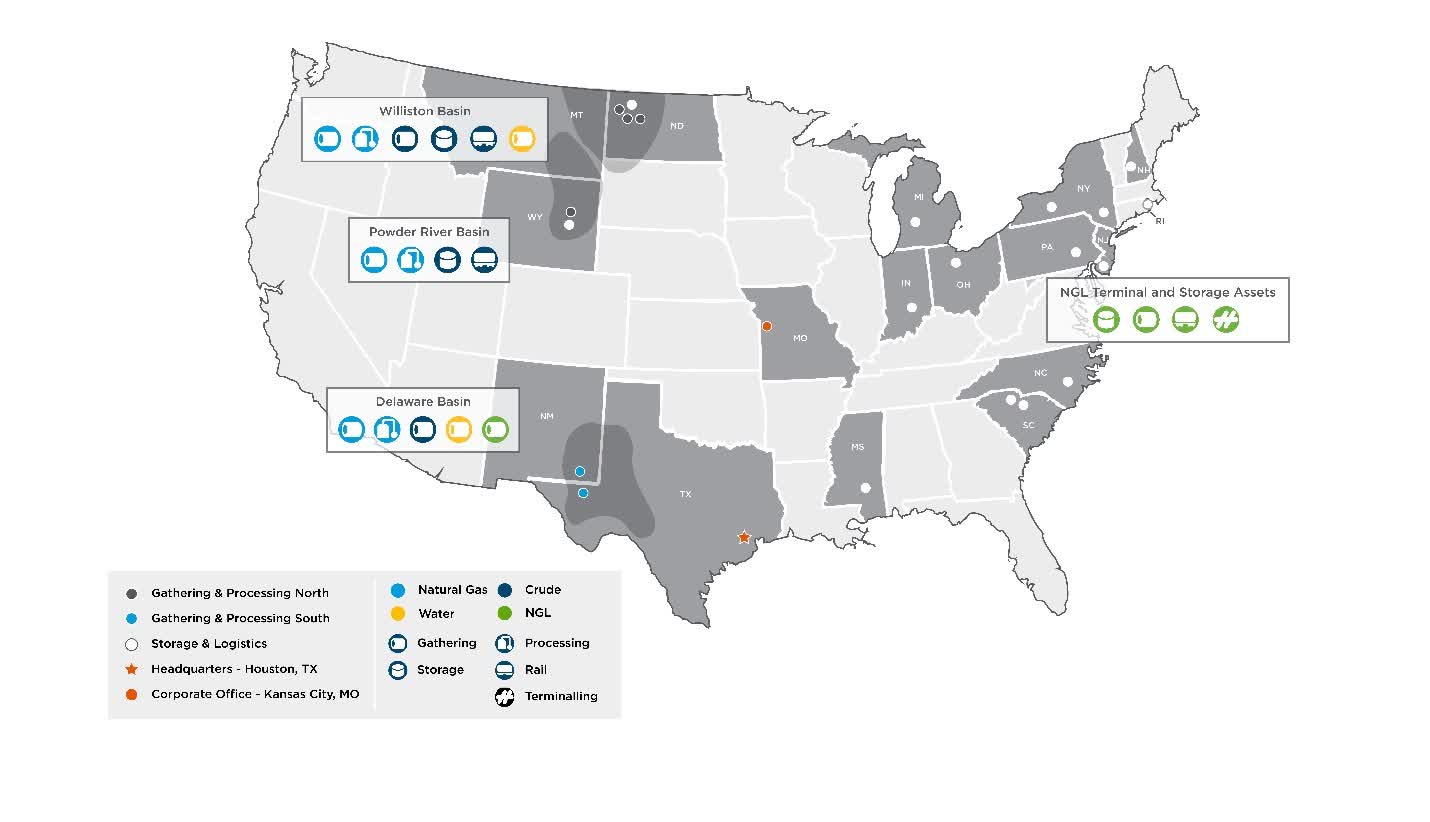

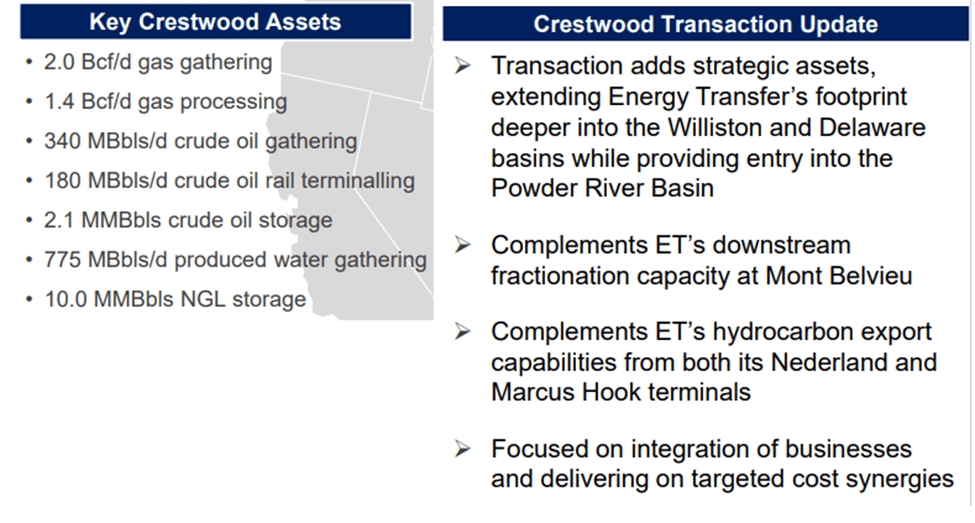

On August 16, 2023, Energy Transfer announced the acquisition of Crestwood Equity Partners ( CEQP ) for 2.07 units for each CEQP unit outstanding, summing to $2.8b at announcement. The deal closed on November 3rd, 2023, with all CEQP shares being converted to ET shares. Crestwood's business focused on gathering and processing (G&P) in the Williston, Delaware, and Powder River basins. The Crestwood acquisition comes with some strong customers across their basin outlays, including Exxon Mobil ( XOM ) and Devon Energy ( DVN ) in the Williston Basin, ConocoPhillips ( COP ) and Marathon Oil ( MRO ) in the Delaware Basin, and Occidental Petroleum ( OXY ) and Continental Resources in the Powder River Basin.

{kind=link}

Crestwood's assets in the Willison and Delaware basins are well positioned to work in conjunction with Energy Transfer's long-haul pipelines, downstream fractionation capacity at Mont Belvieu, and their hydrocarbon export capacity from their Nederland terminal and Marcus Hook complex in Texas and Pennsylvania. The deal is expected to generate $40mm annual run-rate cost synergies in addition to other benefits from the combination.

{kind=link}

These acquired assets significantly complement Energy Transfer's pipeline systems and improve their G&P exposure in the Bakken Basin.

{kind=link}

Operations & Financials

Energy Transfer manages operations across multiple segments, including intrastate, interstate, midstream, NGL & refined products, crude oil, and disaggregated investments in Sunoco and USAC. Interstate transport and midstream services are their highest-yielding segments with each earning an aEBITDA margin of 80% and 78% for FY22, respectively. Midstream services are those transporting hydrocarbons from the wellhead to the larger vein pipeline, whether interstate or intrastate. Interstate transportation and storage, as the name suggests, hauls natural gas on its long-haul pipeline system to trading hubs, including Cushing and the Henry Hub. Midstream and interstate services earned Energy Transfer $3,210mm and $1,753mm in aEBITDA for FY22. Aggregate aEBITDA came in at $13,093mm for FY22 with management guiding FY23 ending between $13,500 - $13,600mm, a modest 3-4% increase. Management guided estimates up from a month ago in the September guidance pre-Crestwood acquisition, with the remaining two months being inclusive.

Operations were significantly impacted in q3'23 by a $625mm non-operating litigation-related loss, resulting from legal matters (covered below). Overall operations performed exceptionally well within management's expectations for the year. On a trailing basis, Energy Transfer is in line to meet management's aEBITDA estimates of $13.5 - $13.6b. Much of this is attributable to significant increases in volumes. For the first 9 months of FY23, intrastate experienced a 3% increase in natural gas volumes transported through their Enable Oklahoma Intrastate Transmission system and Texas system as well as higher gas volumes out of Haynesville Shale. Crude oil also experienced higher transport volumes, moving 5.6mmbbl/d compared to 4.6mmbbl/d from the same period last year. Much of these volumes resulted from more flow through the Texas pipeline systems, the Bakken Pipeline, as well as the acquisition of the Lotus assets, and the Centurion Pipeline System that extends through the Permian from New Mexico to Cushing, Oklahoma.

Export Capacity

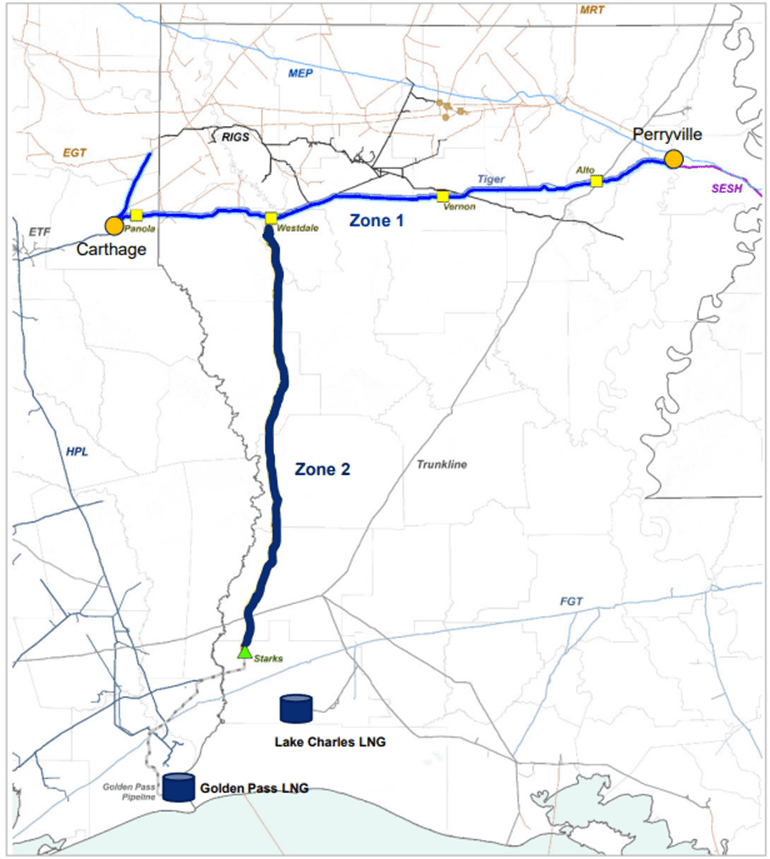

Energy Transfer's Gulf Run Pipeline was placed into service at the end of FY22. This 42", 1.65bcf/d capacity pipeline transports natural gas from the Haynesville basin through Louisiana down to the Gulf Coast for LNG export. The Gulf Run Pipeline already has 1.1bcf/d 20-year committed capacity offtake to Golden Pass LNG, the JV between QatarEnergy and Exxon. The pipeline is fully subscribed beginning in 2025 when the Golden Pass LNG export terminal commences operations and Energy Transfer has the option to add an additional 1bcf/d capacity through gas compression. Management can loop the Gulf Run Pipeline, adding an additional 2bcf/d of capacity. For those that have read my previous work on natural gas producers, Comstock ( CRK ) Southwestern ( SWN ), and Chesapeake ( CHK ) are heavily investing in the development of natural gas production in the Haynesville/Bossier Basin. In total, Energy Transfer is responsible for 20% of the global NGL export capacity and 40% of the US NGL export capacity.

{kind=link}

Debt

As of q3'23, Energy Transfer holds $48.08b in debt obligations with an aggregate annual rate of 5.25%. Net debt/aEBITDA currently sits at 3.53x using trailing figures. Energy Transfer is starting to feel the effects of our higher rates market as debt extinguished at the beginning of November held a rate of 4.50% and new debt was issued to cover repayment of current maturities along with covering their credit facility. Energy Transfer issued $4b in new issuances in October with an average rate of 6.33%.

{kind=link}

Looking ahead to 2024, Energy Transfer will be faced with $5,175mm in debt maturities spread throughout the year.

{kind=link}

The average rate on the debt rolling off their balance sheet in the next year averages to ~5.20%, significantly lower than the debt being issued to replace these issuances. Total aggregate debt owed by Energy Transfer net of subsidiaries costs ~4.60%, not including recent issues. New issues will raise the aggregate rate to 5.26%. Bear in mind that this does not include subsidiary and equity investments, only debt designated directly to Energy Transfer. It's clear that as rates set by the Fed remain higher for longer, businesses like Energy Transfer that rely on debt for growth and capital investments will find themselves in a more challenging business climate.

Management is actively paying off their revolver with a portion of the new issuances. As of their q3'23 report, the firm has $2.85b in outstanding borrowings on their five-year credit facility, of which $1.55b consists of commercial paper. The average cost of these outstanding borrowings equates to 6.29%, slightly below the average cost of their new issuances. My presumption is that management is being proactive in refinancing their credit facility to hedge the risk of another rate increase.

Both Sunoco and USAC have outstanding $647mm and $813 borrowings on their respective credit facilities. Rates are significantly higher than Energy Transfer's at 7.34% and 7.99%, respectively.

How To Trade

{kind=link}

Owning ET units comes with a lot of benefits but can come with some challenges for those using taxable accounts. Because the units are partnership units, dividends are taxed as ordinary income and inadvertently will increase your reportable annual income. My recommendation will be to hold these units in a tax-advantaged account such as a ROTH/Traditional IRA or an equivalent vehicle. Aside from owning the standard units that yield 9.40% at the time of this writing, Energy Transfer has a substantial listing of preferred shares outstanding that offer rich benefits with de minimis volatility or dilution.

Starting with common units, ET has consistently increased its dividend distribution and is now back to its pre-pandemic level of $0.31/unit. This yields 9% on a trailing annualized basis. On average, this is at the higher end of the spectrum for midstream companies.

{kind=link}

Given the firm's robust growth through acquisition and its dividend growth target of 3-5%, we can insinuate some pricing expectations to accommodate for future growth. Using a 4% dividend growth rate and a 12% discount rate, we can price ET units at $16.06/unit. I provide ET with a BUY recommendation.

{kind=link}

The alternative option is to purchase preferred shares. At this time, the series C and series D perpetual preferreds have transitioned to their floating rate which yields well over their fixed rate at 10.14% and 10.35%, respectively.

{kind=link}

The nominal payout for this should come out to ~$2.50/share at the current rate. The floating rate is dependent on the 30-day SOFR rate which now stands at 5.35%. As the spreads over SOFR stand, the breakeven SOFR rate to match the fixed rate will be 2.60%, well below the current federal funds rate. Depending on where we're at in the economic cycle and if the Federal Reserve keeps rates higher for longer, this perpetual preferred can pay handsomely in a fixed-income portfolio. As it stands, I provide the series C and series D perpetual preferreds a BUY recommendation.

Corporate Reports - sensitivity analysis

{kind=link}

For further details see:

Energy Transfer Offers High Yielding Vehicles For All Investors