ET - Energy Transfer: Prepare To Buy

2024-01-19 11:23:57 ET

Summary

- In my last note on Energy Transfer, I had a 'Neutral/Hold' stance, missing out on +5.83% alpha over the S&P 500. Now I am more bullish but maintain my stance:

- Crestwood is a good acquisition to bolster ET's portfolio as it solidifies the latter's existing market position and enables entry into new basins. The purchase is also not pricey.

- ET is well-set to capitalize on US NGL exports, which are expected to increase in 2024. ET is a beneficiary here as it has a 40% market share.

- Currently, ET is trading near its 5-yr median 1-yr fwd price to cash flow per unit multiple; I prefer a valuation discount to become a buyer.

- Technical analysis also suggests there may be an opportunity to accumulate at lower prices to have a better chance of maximizing total shareholder return.

Performance Assessment

In my last update on Energy Transfer ( ET ), I had a 'Neutral/Hold' rating on the security. Since then, ET has delivered a total shareholder return of +24.98% compared to the S&P 500's +19.15%, corresponding to a missed opportunity for +5.83% alpha:

Performance since Hunting Alpha's last coverage of Energy Transfer (Seeking Alpha)

Thesis

I am more bullish on Energy Transfer now, but I am waiting for a better discount for buys. It is a close call though between 'buy' and 'wait'. For now, I maintain a 'Neutral/Hold' stance as I note the following:

- Crestwood is a good acquisition to bolster ET's portfolio

- ET is well-set to capitalize on NGL export trends

- I prefer a valuation discount to become a buyer

Crestwood is a good acquisition to bolster ET's portfolio

I find ET's rationale for purchasing Crestwood Equity Partners' ( CEQP ) business to be clear. That's important for an M&A or spinoff decision. Generally, when a company's capital market transaction rationale is not glaringly obvious and obvious, it has undermined my positivity in the stock. For example, TC Energy ( TRP ) ( TRP:CA )'s spinoff of their liquids pipeline business is an example of a muddy rationale.

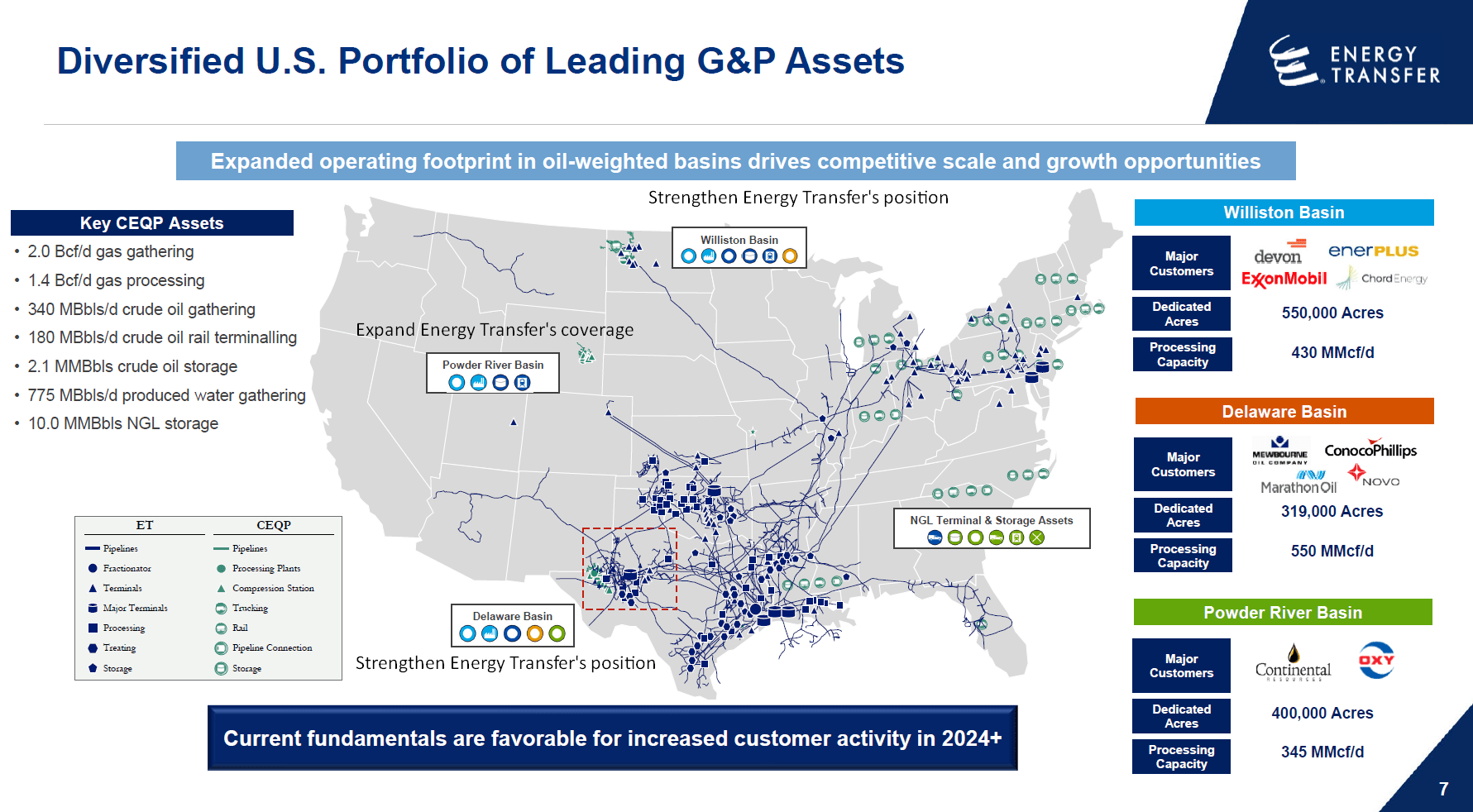

Pro-forma Asset Portfolio (Energy Transfer M&A Presentation, Author's Annotations)

{kind=link}

In this case, the combined portfolio will strengthen ET's existing positioning in the Williston and Delaware Basins and help them expand coverage and enter the Powder River Basin. The company expects $40 million of annual cost saving synergies generated due to the close overlap of the businesses. Moreover, the deal is accretive to FCF, which is particularly important for yield-focused investors.

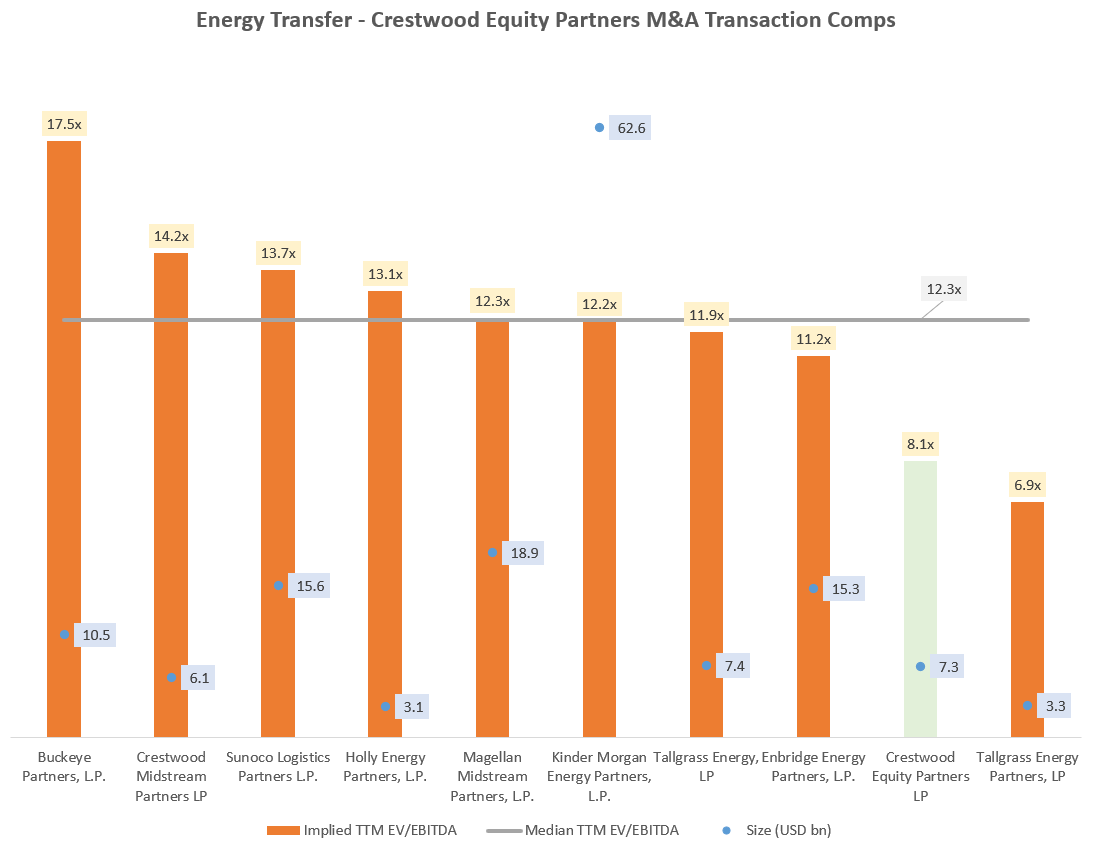

Energy Transfer - Crestwood Equity Partners EV/EBITDA Transaction Comps (Capital IQ, Author's Analysis)

{kind=link}

It is also favorable that this acquisition is not too large at only $7.3 billion and not pricey compared to similar M&A transaction multiples; the ET - CEQP deal occurred at a TTM EV/EBITDA of 8.1x, which corresponds to a 34% discount to the median transaction multiple of 12.3x. Hence, I believe the risk of overpaying is relatively reduced here.

ET is well-set to capitalize on NGL export trends

According to the US Energy Information Administration, US exports of hydrocarbon gas liquids is expected to increase in 2024:

US Net Trade of Hydrocarbon Gas Liquids (US Energy Information Administration, Short Term Energy Outlook January 2024)

Natural gas liquids ((NGL)) fall under the hydrocarbon gas liquids category.

This is a tailwind for ET as it has a 20% global market share in NGL exports and 40% market share in US NGL exports. ET's co-CEO Thomas Long also noted strong growth in this business in the Q3 FY23 earnings call :

Total NGL export volumes grew more than 20% over the third quarter of 2022, setting a new partnership record. This was primarily driven by increased international demand for NGLs .

The numbers also show strong growth in this segment over the last few quarters and years:

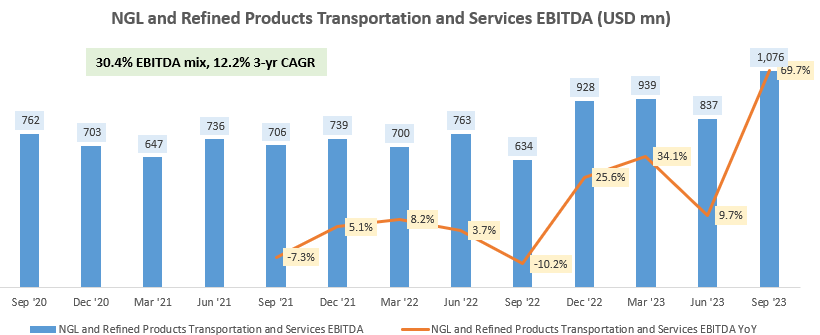

NGL and Refined Products Transportation and Services EBITDA (USD mn) (Company Filings, Author's Analysis)

{kind=link}

This division makes up 30.4% of overall EBITDA for ET.

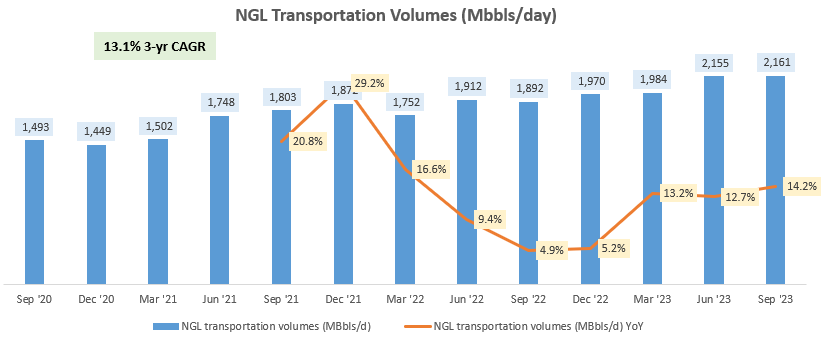

NGL Transportation Volumes (Mbbls/day) (Company Filings, Author's Analysis)

{kind=link}

The numbers also show that NGL transportation volume growth has been accelerating in 2023. Given the bullish outlook, I anticipate this trend to continue.

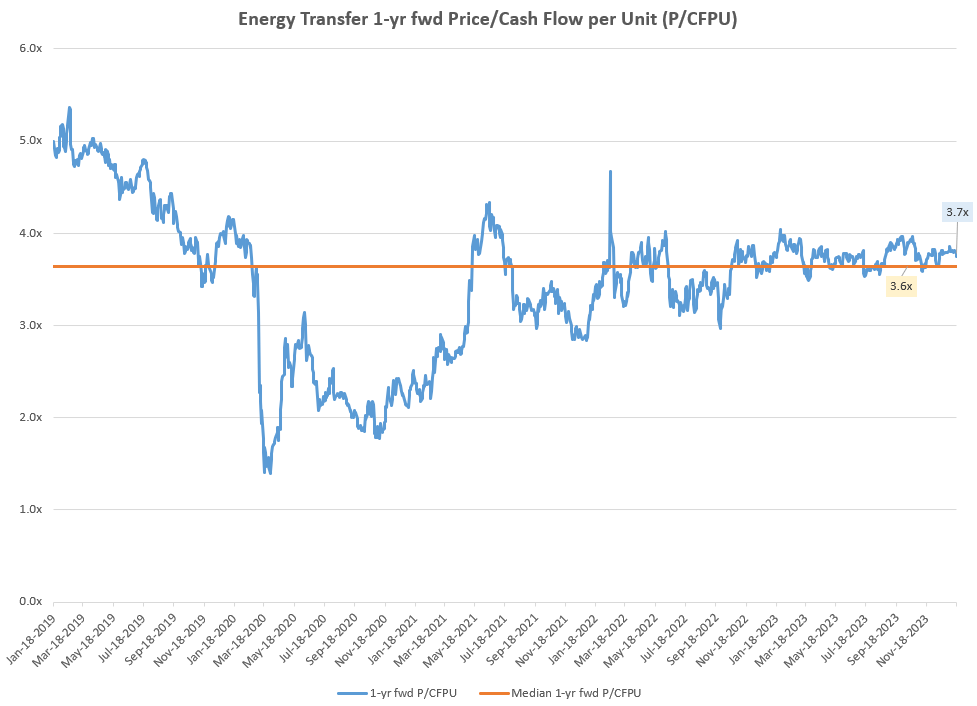

I prefer a valuation discount to become a buyer

Energy Transfer 1-yr fwd Price/Cash Flow per Unit (Capital IQ, Author's Analysis)

{kind=link}

As ET does not have very high variability in cash distributed to unitholders, I believe it is appropriate to use a cash flow multiple to assess the valuation multiple. Currently, ET trades at a 1-yr fwd P/Cash Flow per Unit (P/CFPU) of 3.7x; just a touch over the 5-yr median of 3.6x.

I believe buys are acceptable in this range, but personally I would wait for a bit of a discount especially after considering the technicals:

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post , which explains how and why I read the charts the way I do.

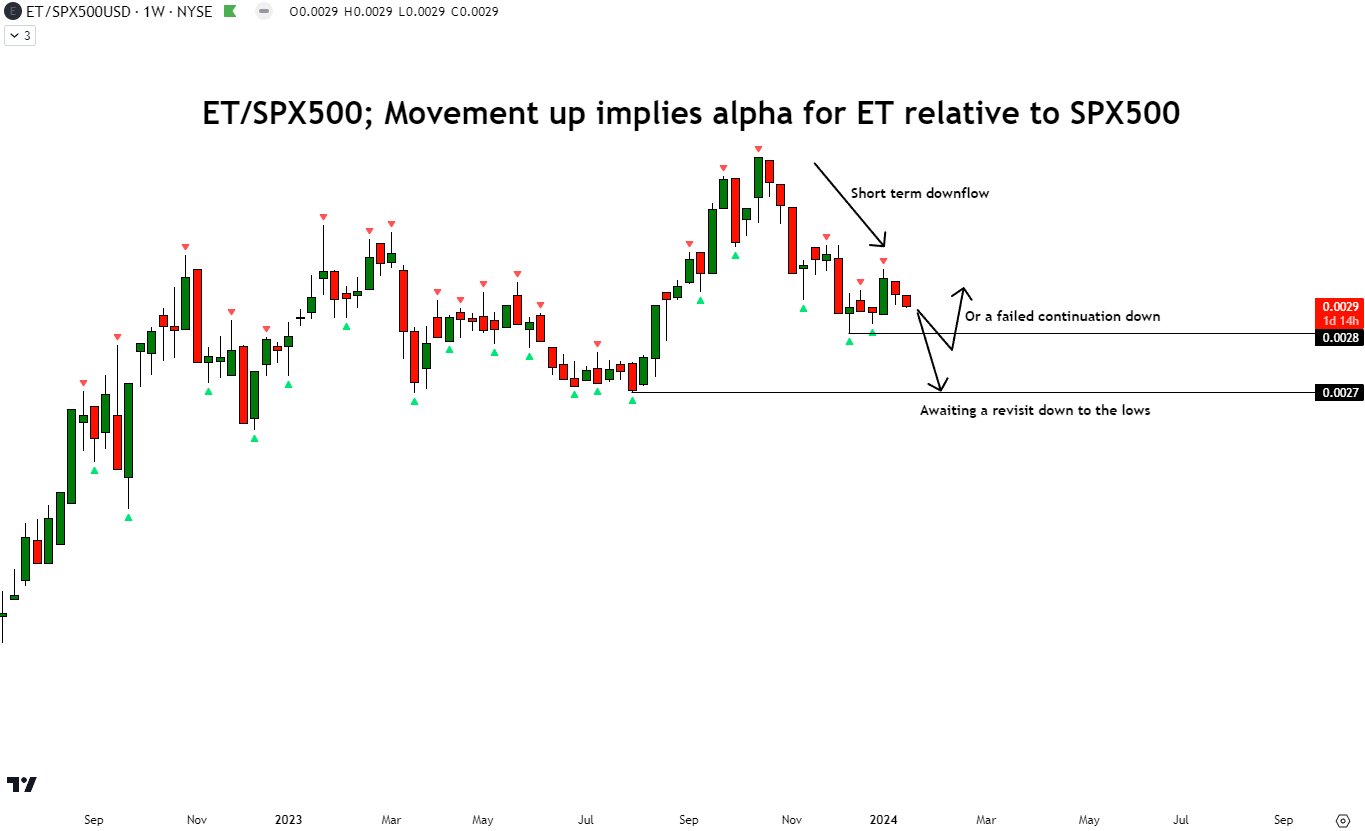

Before getting into the analysis of the technicals, why even look at it in the first place, especially for an MLP that is likely to be a longer-term investment? The answer is to maximize chances of getting the best deal possible; the 8.99% dividend yield and alpha generation over the S&P 500 ( SPY ) ( SPX ). Readers familiar with my work will know that I view every investment relative to its alpha potential vs the S&P 500.

Relative Technical Analysis of ET vs S&P500 (TradingView, Author's Analysis)

{kind=link}

On the relative weekly chart of ET/SPX500, a movement up corresponds to ET making alpha over the S&P 500. I observe a short-term downflow currently due to a sequence of lower highs (red arrows) and lower lows (green arrows). I identify two scenarios for technical alignment of buys:

- At a revisit back down the lows made in August 2023

- After a failed continuation down below the lows made in December 2023

These are the scenarios I am waiting for to become a buyer of ET.

Leverage Risks

ET's net debt/EBITDA stands at 3.6x as of Q3 FY23. And the company is targeting to be in the lower-end of 4-4.5x going forward. I think leverage risk is reduced if there are going to be rate cuts in 2024 . Fitch Ratings also views this favorably , granting ET a BBB- credit rating.

Takeaway

In my last update on Energy Transfer, I had a 'Neutral/Hold' stance, making me miss out on +5.83% alpha over the S&P 500 ((SPY)) ((SPX)). Now, I am a bit more bullish but just not enough to buy just yet (although it is a close call).

I think ET's acquisition of Crestwood Equity Partners ((CEQP)) makes clear strategic sense as it would solidify existing market positioning and pave the way for entry into new basins. The transaction also occurred at a reasonable multiple below the median of comparable transactions, reducing the risk of a capital allocation blunder.

From an operations perspective, I see the main highlight to be a bullish growth outlook for US NGL exports, for which ET has 40% market share. Valuations-wise, ET is trading at close to its 5-yr 1-yr fwd price to cash flow per unit multiple. Given that the technicals also suggest there may be an opportunity to accumulate at lower prices, I am holding off on the buys and waiting a little longer for now. But it is a close decision; I think buys are also acceptable.

Stance: 'Neutral/Hold'

How to interpret Hunting Alpha's ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

For further details see:

Energy Transfer: Prepare To Buy