ET - Energy Transfer: Still A Solid 8.84% Opportunity Despite Recent Price Run-Up

2023-10-20 18:25:57 ET

Summary

- Energy Transfer LP has seen a strong performance in the market, outperforming the S&P 500 Index since early August.

- The company's cash flows are stable and not impacted by energy prices due to its long-term volume-based contracts.

- Energy Transfer is set to acquire Crestwood Equity Partners, which will enhance its presence in the natural gas space and offer synergies for both companies.

- The market seems to expect that the production of crude oil in the United States will increase, but that is not likely to happen. The real opportunity here is natural gas midstream.

- Energy Transfer has one of the strongest balance sheets in the industry and continues to be a good way to obtain an 8.84% yield.

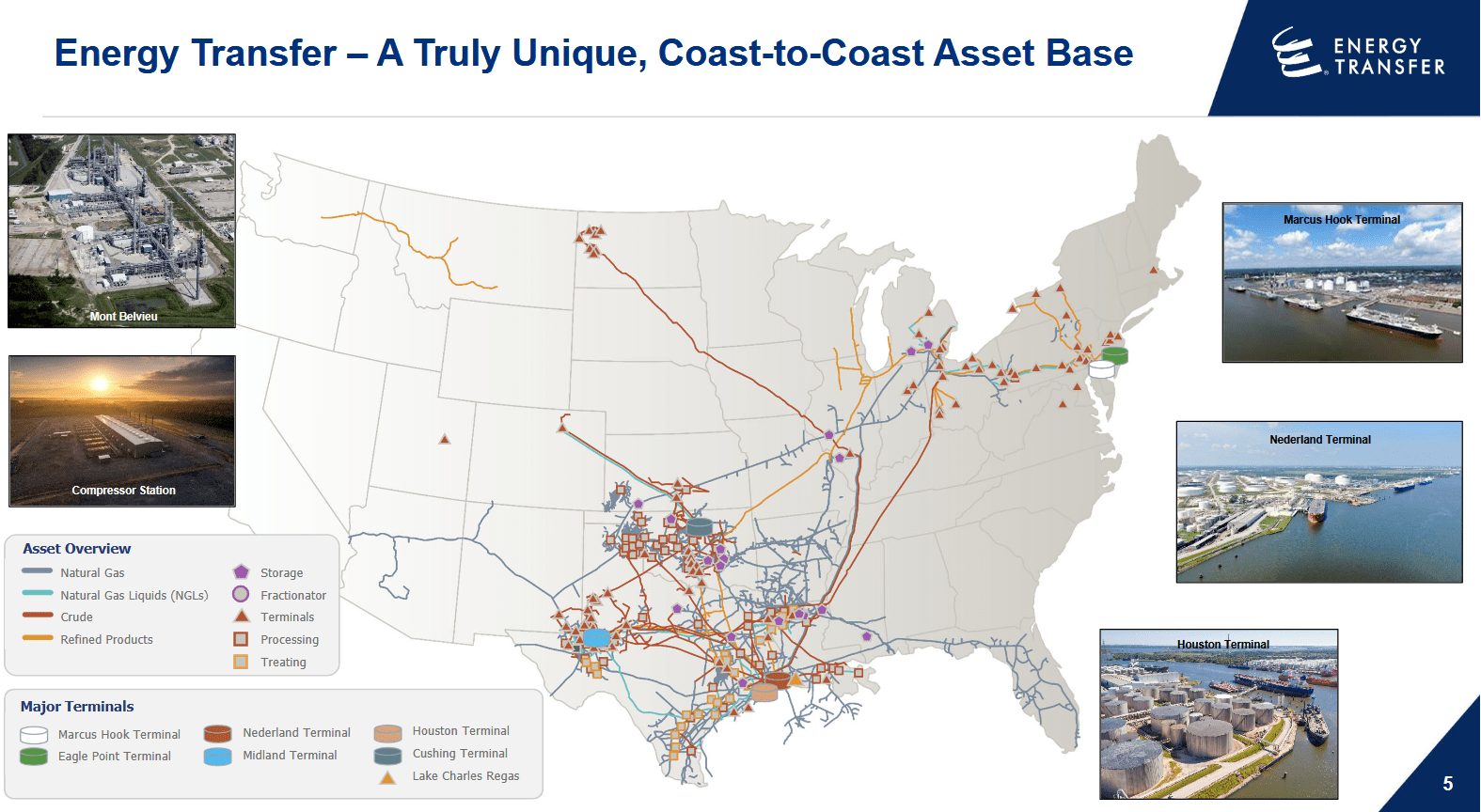

Energy Transfer LP ( ET ) is one of the largest midstream partnerships in the United States, boasting a network of pipelines and related infrastructure that stretches over most of the nation.

{kind=link}

This has proven to be a pretty good business to be in recently, as rising energy prices have generally had a positive impact on the unit price of most midstream companies. This is quite interesting, as Energy Transfer does not directly benefit from rising energy prices. In fact, its cash flows tend to be remarkably stable over time regardless of economic shocks or energy price fluctuations. I have discussed this in many previous articles on the company.

That has not prevented Energy Transfer from proving to be a very good investment for its unitholders recently, however. As regular readers may recall, we last discussed Energy Transfer in early August of this year. The company’s units have appreciated by 9.27% since that time, substantially outperforming the S&P 500 Index ( SP500 ):

{kind=link}

This may not be entirely caused by rising energy prices, although that is almost certainly a factor. As I have pointed out in various articles over the past few weeks, the mood of the market has recently changed to one of impatience. Investors are no longer willing to wait years (or decades) to earn cash flow from the assets in their portfolios. In today’s high-rate environment, their interest has shifted to those companies that boast strong cash flows and can deliver money right now. Energy Transfer currently boasts an 8.84% yield, so it certainly meets this requirement. In fact, this yield is sufficiently high to beat the yield of the S&P 500 Index as well as the yield of the Alerian MLP Index ( AMLP ).

This strong recent performance does not necessarily mean that the units have gotten ahead of themselves, however. Let us investigate this and see if buying Energy Transfer still makes sense today.

About Energy Transfer

As stated in the introduction, Energy Transfer is one of the largest midstream master limited partnerships in the United States, boasting a network of pipelines, storage facilities, natural gas liquids fractionators, natural gas processing plants, and terminals. The company even has a liquefied natural gas regasification plant. Overall, its infrastructure can be found in many states in the eastern and central states, although it is somewhat less common along the Pacific Coast.

This is not especially surprising, as there are very few midstream companies with operations in California. This is mostly due to California regulations requiring a special formulation of refined products for sale in the state. As a result, there are no crude oil or refined products pipelines going into the state, and most midstream companies have just shunned the entire Pacific Coast as a result.

As mentioned earlier, it is quite possible that the strong performance of Energy Transfer’s units in the market over the past few months has been at least partially driven by strengthening energy prices. This chart shows the cash price of West Texas Intermediate crude oil against Energy Transfer’s unit price since August 3, 2023:

{kind=link}

We can obviously see a correlation here, as the two charts move almost in lockstep. However, Energy Transfer’s cash flows have very little to do with oil prices. As I explained in my last article on Energy Transfer:

Energy Transfer has very little exposure to the market prices of either of these commodities (crude oil and natural gas) due to the business model that the company employs. In short, Energy Transfer enters into long-term (usually five to fifteen years in length) contracts with its customers under which the company provides transportation for the company’s hydrocarbon products using its network of pipeline infrastructure. In exchange, the customer compensates Energy Transfer based on the volume of resources that the partnership handles, not on their value. This provides a great deal of protection against price fluctuations of either crude oil or natural gas.

Energy Transfer expects that approximately 90% of its 2023 adjusted EBITDA (a proxy for pre-tax cash flow) will come from these volume-based contracts:

Energy Transfer

Thus, the company’s financial performance is largely dictated by the volume of resources that it transfers, not their value. As such, its cash flow is not really impacted by energy prices. We can see this cash flow stability by looking at the company’s adjusted EBITDA over the past few years:

| FY 2020 |

| FY 2021 |

| FY 2022 |

| YTD 2023 |

| Adjusted EBITDA |

| $10,531 |

| $13,046 |

| $13,093 |

| $6,555 |

(all figures in millions of U.S. dollars.)

It cannot be denied that oil prices were all over the place during those years. In particular, the average price of West Texas Intermediate was $39.68 per barrel in 2020, $68.17 per barrel in 2021, and $94.53 per barrel in 2022. The year-to-date average for 2023 is $77.90 per barrel and Energy Transfer’s annualized adjusted EBITDA is $13.110 billion. Thus, we can immediately see that energy prices have virtually no impact on the company’s adjusted EBITDA despite what the market seems to believe.

With that said, there could be some optimism that the volume of resources that the company transports will increase as energy prices do. After all, there is a certain logic behind the belief that American shale producers will increase their production in order to take advantage of rising energy prices. However, as I have discussed in a few recent posts to Energy Profits in Dividends, it is unlikely that this will be the case. As the Wall Street Journal explains :

Some oil executives said most of the shale industry plans to stand pat even as global oil prices increase further. Most shale companies have vowed to hand over their winnings from high energy prices to investors via share buybacks and dividends. They also face pressure from inflation and high interest rates.

I pointed this out in a few articles published over the past two years in various shale companies as well. Basically, due to investor complaints about the industry’s underperformance over most of the past decade, shale companies are largely opting to simply keep their production stable and pay out the majority of their cash flows to investors. Thus, it is unlikely that Energy Transfer’s volumes will increase substantially due to shale producers increasing their output along with energy prices.

This does not mean that Energy Transfer has no near-term to mid-term growth opportunities, just that the company will probably not see the volume growth that the market expects. For example, there are still significant growth opportunities in the natural gas space, as energy producers are constructing an enormous amount of liquefied natural gas production capacity over the next few years. Indeed, the nation’s consumption of natural gas is expected to increase by 20 billion cubic feet per day by 2027, approximately 14 billion cubic feet of which comes from new liquefied natural gas production facilities that are scheduled to come online over the period:

{kind=link}

Energy Transfer is engaged in some growth projects to take advantage of this situation. For example, the company stated recently that it is investigating the possibility of constructing a new natural gas processing plant in the Permian Basin due to strong customer demand.

This is in addition to the 200 million cubic feet-per-day Bear processing plant that the company brought online in June. The company also has a number of natural gas pipelines under construction that are meant to increase its ability to meet the growing demand for natural gas domestically, as numerous utilities are replacing coal power plants with renewables supplemented by natural gas plants.

After all, wind and solar are not capable of meeting electric demand on their own with current technology (and batteries are nowhere near sufficient to provide sufficient backup capacity). It is fortunate that Energy Transfer is reasonably well diversified and has long had a substantial presence in the natural gas space to allow it to take advantage of this growth potential. Indeed, as we can see here, the company’s cash flows are quite well diversified between crude oil, natural gas, and natural gas liquids:

Energy Transfer

Most of its forward growth will almost certainly come from the natural gas and natural gas liquids segments, but that is okay as the company should still have much greater growth potential than some other midstream companies that exclusively focus on crude oil or refined products.

Acquisition of Crestwood Equity Partners

Energy Transfer could soon increase its presence in the natural gas space significantly by acquiring Crestwood Equity Partners ( CEQP ). The company announced on August 16, 2023, that it is planning to acquire Crestwood Equity Partners in an all-stock deal. From the press release:

Under the terms of the agreement, Crestwood common unitholders will receive 2.07 common units for each Crestwood common unit. The transaction is expected to close in the fourth quarter of 2023, subject to the approval of Crestwood’s unitholders, regulatory approvals, and other customary closing conditions. Upon closing, Crestwood common unitholders are expected to own approximately 6.5% of Energy Transfer’s outstanding common units.

As of right now, Crestwood Equity Partners’ common units are trading at $28.60 each and Energy Transfer’s units are at $14.06 per share. Thus, the proposed ratio assigns a value of $29.10 to Crestwood’s common units. That is a 1.75% premium today, which is not really much, but the premium was higher when this deal was announced.

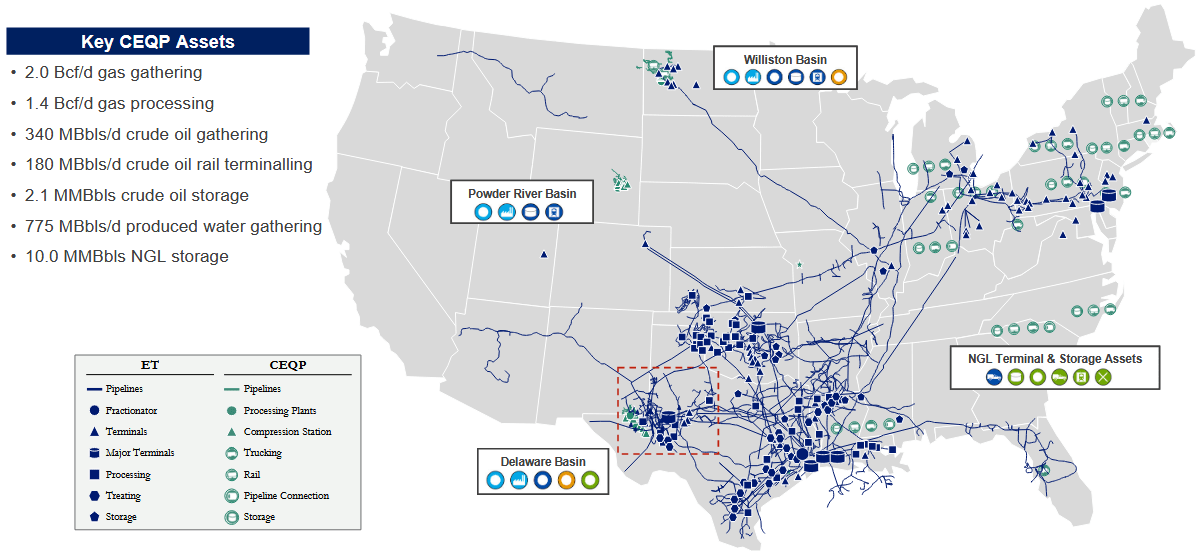

This deal will certainly enhance Energy Transfer’s capabilities in the Bakken Shale, as Crestwood Equity Partners is one of the largest midstream operators in that region. Crestwood Equity Partners also has a gathering and processing business in the Powder River Basin, which is an area in which Energy Transfer currently has no presence at all:

{kind=link}

Energy Transfer, meanwhile, has the takeaway capacity and long-haul pipelines that Crestwood Equity Partners lacks. Overall, I can certainly understand why Energy Transfer wants to do this deal. Ultimately, it could work out quite well for the company as it allows the combined firm to offer a “one-stop service” for customers in the Bakken Shale. Crestwood’s substantial gathering and processing operation in that region can handle that need for the customers and then Energy Transfer’s long-haul pipelines can move it to where it is needed.

As separate entities, neither company can offer both services to customers. Crestwood Equity Partners is also more natural gas-focused than Energy Transfer, so this acquisition should weight Energy Transfer’s business a bit more towards gas. As that is where the strongest growth is, that is certainly a positive thing.

Unlike my rather scathing view on ONEOK’s ( OKE ) acquisition of Magellan Midstream Partners, this one has some clear synergy and will probably benefit Energy Transfer. The only real downside for Crestwood Equity Partners unitholders is that Energy Transfer has a lower yield so they could lose some income. Hopefully, Energy Transfer’s growth will be stimulated enough by this acquisition that it can raise its distribution to compensate for the loss, but that is not certain. For the most part, though, this deal should work out to the benefit of both parties.

Financial Considerations

As I pointed out in my previous article on Energy Transfer:

It is always important that we analyze the way that a company finances its operations before investing in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. As new debt is issued with an interest rate that corresponds to the market interest rate at the time of issuance, this can cause a company’s interest expenses to go up following the rollover. That is an especially big concern today because interest rates in the United States are at the highest levels that we have seen since 2001.

Energy Transfer has been slowly seeing its interest expenses tick up recently, although it has not been nearly as bad as companies in some other areas of the economy. We can see this here:

{kind=link}

As we can clearly see, the company’s training twelve-month interest expenses have been gradually ticking up over the past few years, although it has only been a relatively slow increase. Certainly, this is a less worrying trend than we have seen among utilities or a few other sectors. One of the biggest reasons for this is that the market has not been friendly towards midstream companies for quite some time, and Energy Transfer started focusing on strengthening its balance sheet following the COVID-19 pandemic. We still see that the company’s interest expenses have been trending up, however. Thus, we should not ignore the company’s balance sheet.

One metric that we can use to evaluate a company’s financial structure is its net debt-to-equity ratio. As of June 30, 2023, Energy Transfer had a net debt of $48.632 billion compared to $41.457 billion of partners’ equity. This gives the company a net debt-to-equity ratio of 1.17. Here is how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| Energy Transfer |

| 1.17 |

| Enterprise Products Partners ( EPD ) |

| 1.03 |

| MPLX ( MPLX ) |

| 1.53 |

| Kinder Morgan ( KMI ) |

| 0.98 |

| The Williams Companies ( WMB ) |

| 1.68 |

| ONEOK |

| 1.76 |

As we can see here, Energy Transfer compares quite well to its peers in this respect. In particular, MPLX, which has long been one of the best-financed companies in the midstream sector, actually employs more leverage than Energy Transfer. This is a clear sign that Energy Transfer is not employing too much leverage right now.

As I have pointed out in various articles, a midstream company’s ability to carry its debt is much more important than its overall financial structure. The usual way that we judge that is by looking at the company’s leverage ratio, which is also known as the debt-to-adjusted EBITDA ratio. During the twelve-month period that ended on June 30, 2023, Energy Transfer had an adjusted EBITDA of $13.080 billion.

This compares to a total debt of $48.962 billion as of June 30, 2023. That gives the company a leverage ratio of 3.74x, which is very reasonable. As I have pointed out before, Wall Street analysts usually consider anything below 5.0x to be reasonable. However, most companies have been working to reduce their leverage since the crash in energy prices in 2020. As such, most midstream companies now have a leverage ratio that is below 4.0x, which is the maximum level that I typically like to see. As we can clearly see, Energy Transfer easily meets this criterion.

When we consider that the company’s net debt-to-equity ratio compares reasonably well to its peers and that its leverage ratio is very attractive, we can quickly see that the company enjoys a very strong balance sheet. There is really not very much for us to worry about here. The company’s finances are quite strong.

Conclusion

In conclusion, Energy Transfer continues to be a good holding for those investors who desire to earn a high level of income from their portfolios while still enjoying some growth potential. Admittedly, it is somewhat unlikely that the nation’s upstream energy producers will deliver growth that is anywhere close to what some market participants expect, but there are still sufficient opportunities in the natural gas space for Energy Transfer to deliver volume growth.

The pending acquisition of Crestwood Equity Partners is interesting, and it should significantly enhance Energy Transfer LP’s potential to deliver natural gas midstream growth to the unitholders. The company continues to maintain relatively strong finances and pays a very attractive 8.84% distribution yield. Overall, this company looks like a very solid purchase today.

For further details see:

Energy Transfer: Still A Solid 8.84% Opportunity Despite Recent Price Run-Up