ESMT - EngageSmart Is Well Positioned For Growth Ahead

2023-05-09 16:30:40 ET

Summary

- EngageSmart recently reported its Q1 2023 financial results, beating revenue estimates.

- The firm provides customer engagement software to organizations of all sizes.

- ESMT has grown revenue steadily, is producing increasing operating profits, has no debt, and generates plenty of free cash flow.

- For investors with a patient hold time frame, my outlook on ESMT is a Buy at around $16.50 per share.

A Quick Take On EngageSmart

EngageSmart (ESMT) recently reported its Q1 2023 financial results, beating revenue estimates and matching earnings estimates.

The firm provides customer engagement software solutions to enterprises worldwide.

ESMT appears well-positioned to withstand a downturn with its focus on health care, government and utilities, although its DonorDrive product is likely the most exposed to the negative effects of a slowdown.

For investors with a patient hold timeline, my outlook for ESMT is a Buy at around $16.50 per share.

EngageSmart Overview

Braintree, Massachusetts-based EngageSmart was founded to develop a platform that improves customer engagement tailored for certain industry verticals.

Management is headed by founder and CEO Robert P. Bennett, who has been with the firm since its inception and was previously president of Sage Payment Solutions.

The company's primary offerings include:

-

SimplePractice - Wellness

-

InvoiceCloud - Government, Utilities and Financial Services

-

HealthPay24 - Healthcare

-

DonorDrive - Non-profit and Corporate Fundraising

The firm acquires customers through its direct sales and marketing teams and through partner referrals.

Management is focused on the industry verticals of health and wellness, government, utilities, non-profits and financial services.

EngageSmart's Market & Competition

According to a 2021 market research report by Mordor Intelligence, the global market for customer engagement solutions was an estimated $15.5 billion in 2020 and is forecast to reach $30.9 billion by 2026.

This represents a forecast CAGR of 12.65% from 2021 to 2026.

The main drivers for this expected growth are a growth in technology solutions to improve the customer journey via any device they use to connect with businesses.

Also, a desire to reduce customer churn rate results in improved revenue growth, financial results and a growing stock valuation.

Major competitive or other industry participants include:

-

IBM

-

Microsoft

-

Nuance

-

Oracle

-

Salesforce

-

Avaya

-

Calabrio

-

Aspect Software

-

Genesys

-

Verint Systems

-

Nice Ltd.

-

OpenText

-

Pegasystems

-

Others

ESMT's Recent Financial Trends

-

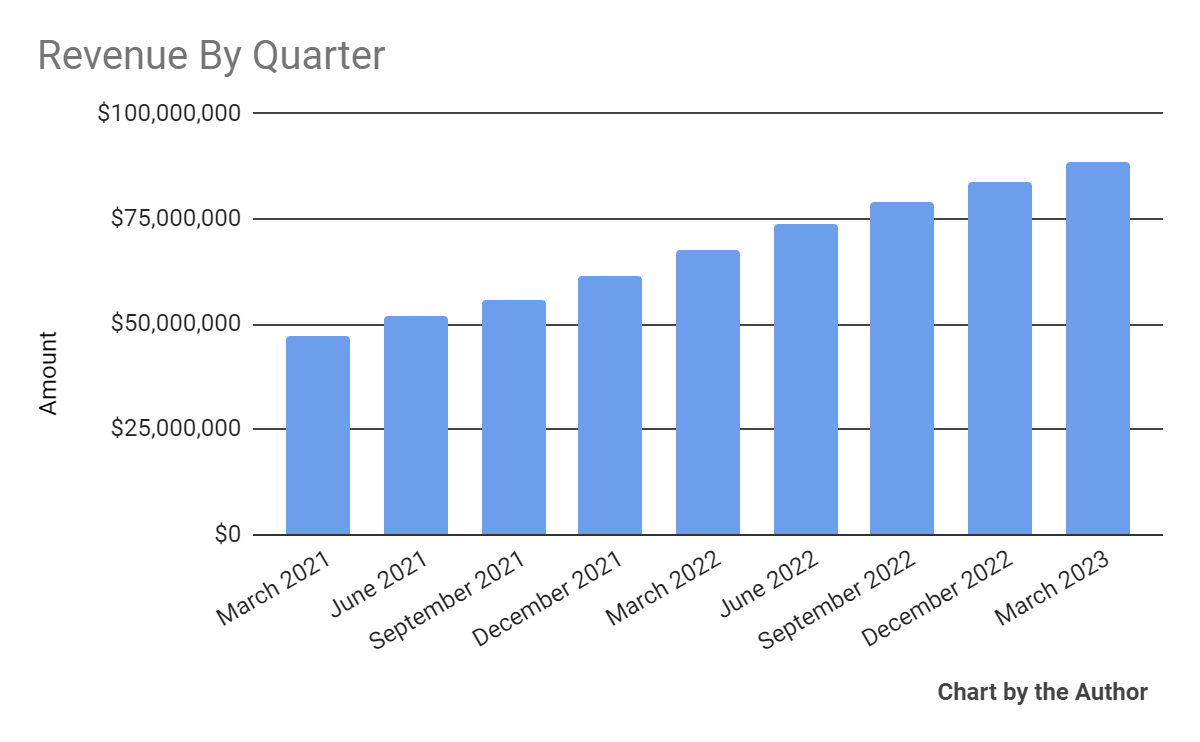

Total revenue by quarter has risen steadily per the chart below

{kind=link}

-

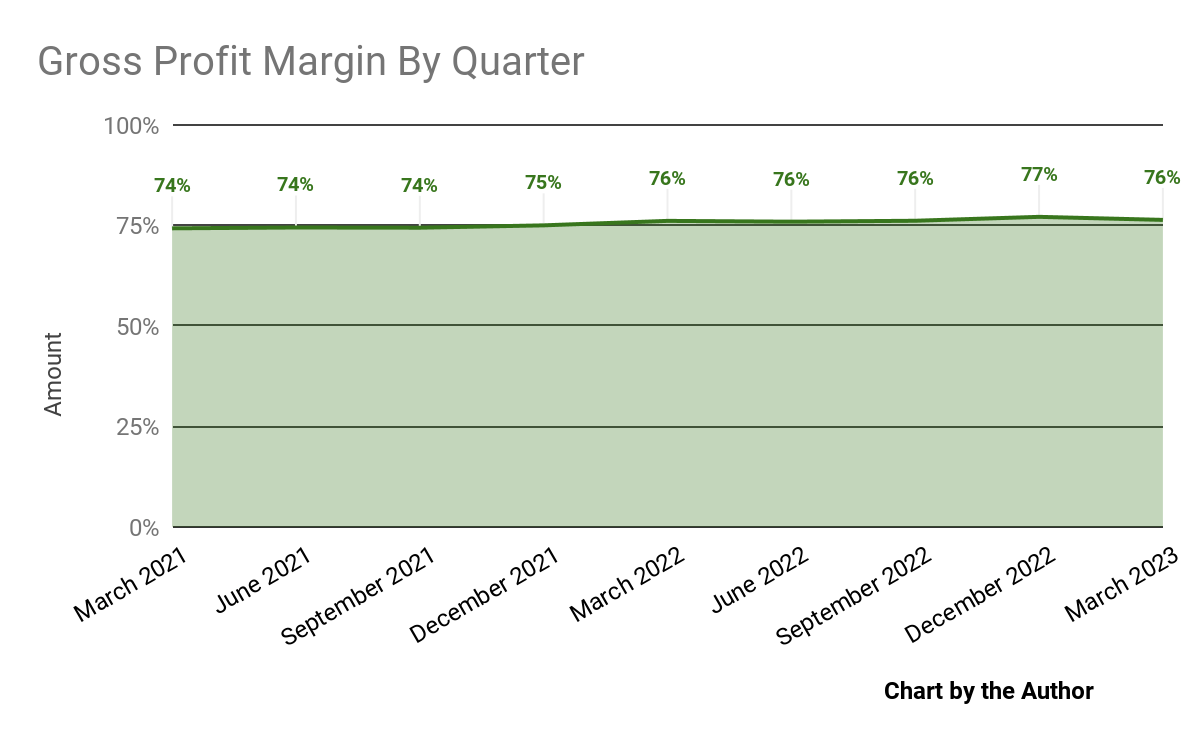

Gross profit margin by quarter has trended slightly higher over time:

{kind=link}

-

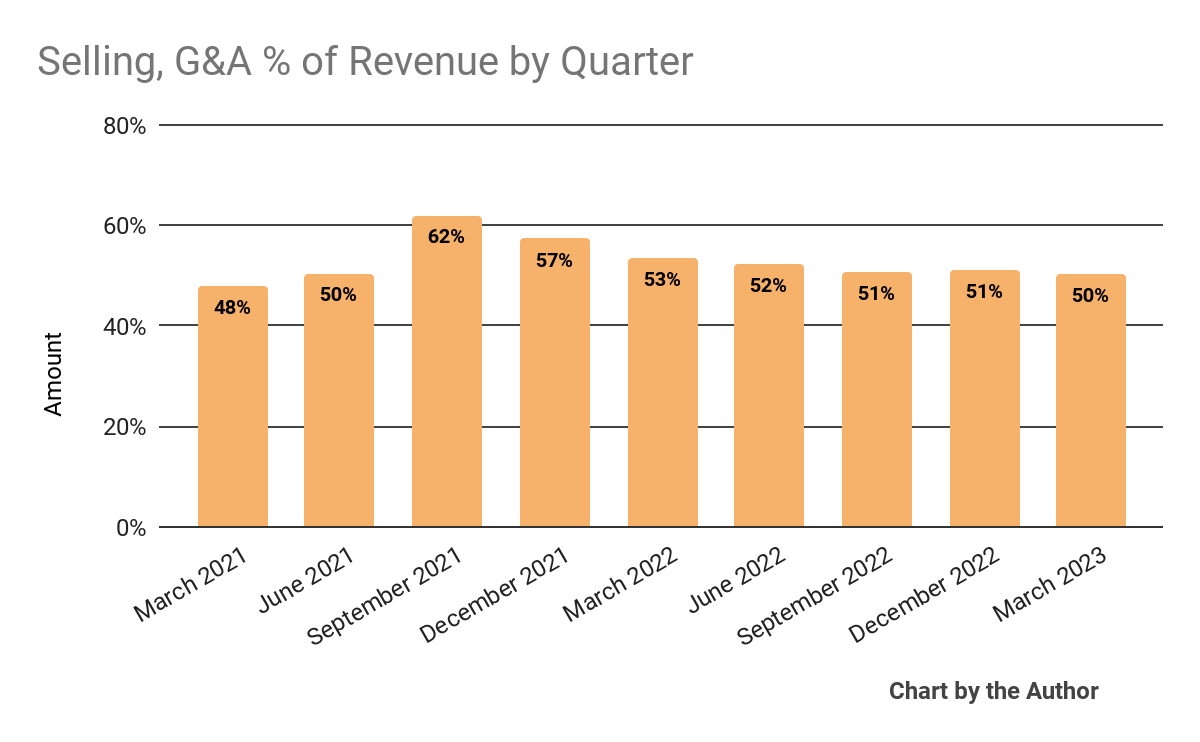

Selling, G&A expenses as a percentage of total revenue by quarter have fallen in recent quarters:

{kind=link}

-

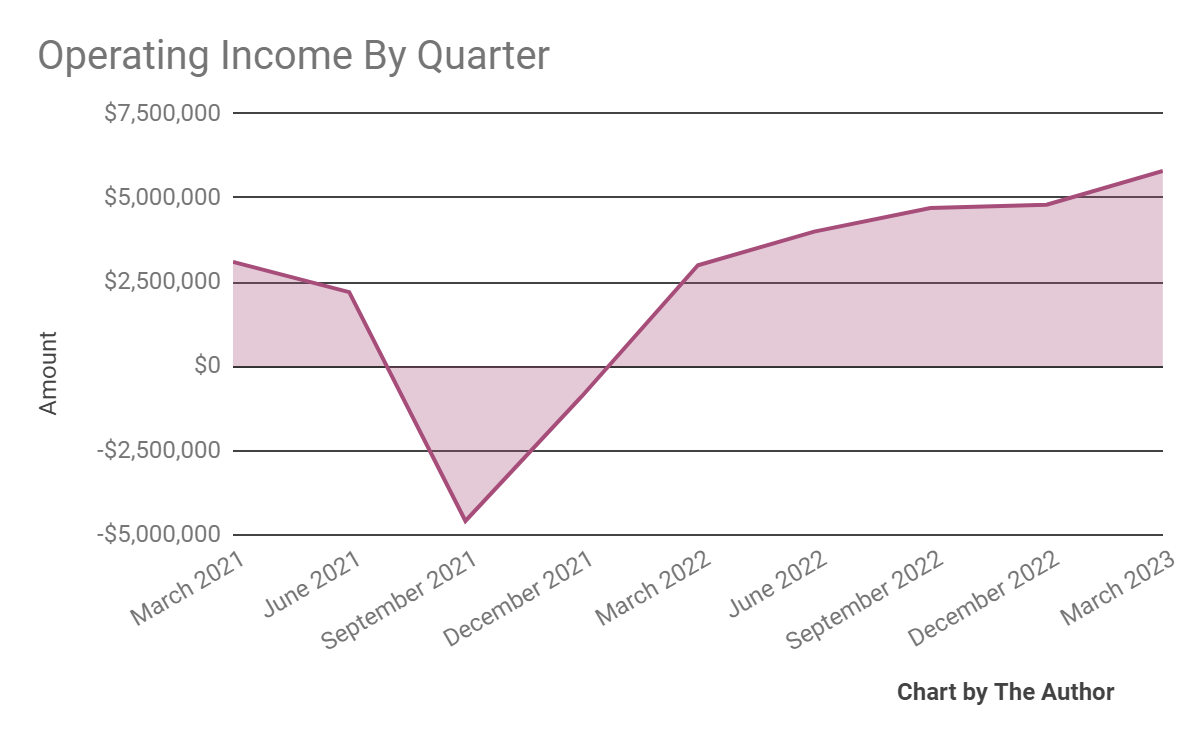

Operating income by quarter has trended higher in recent quarters:

{kind=link}

-

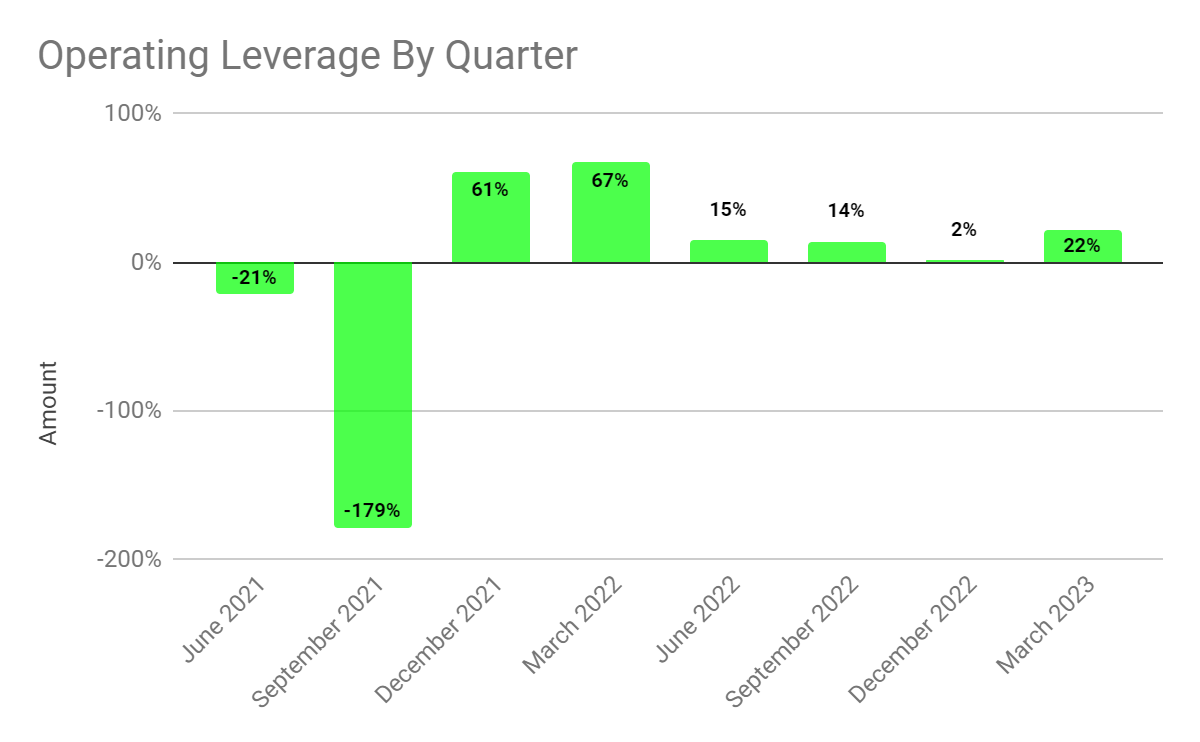

Operating leverage remained positive in several quarters recently:

{kind=link}

-

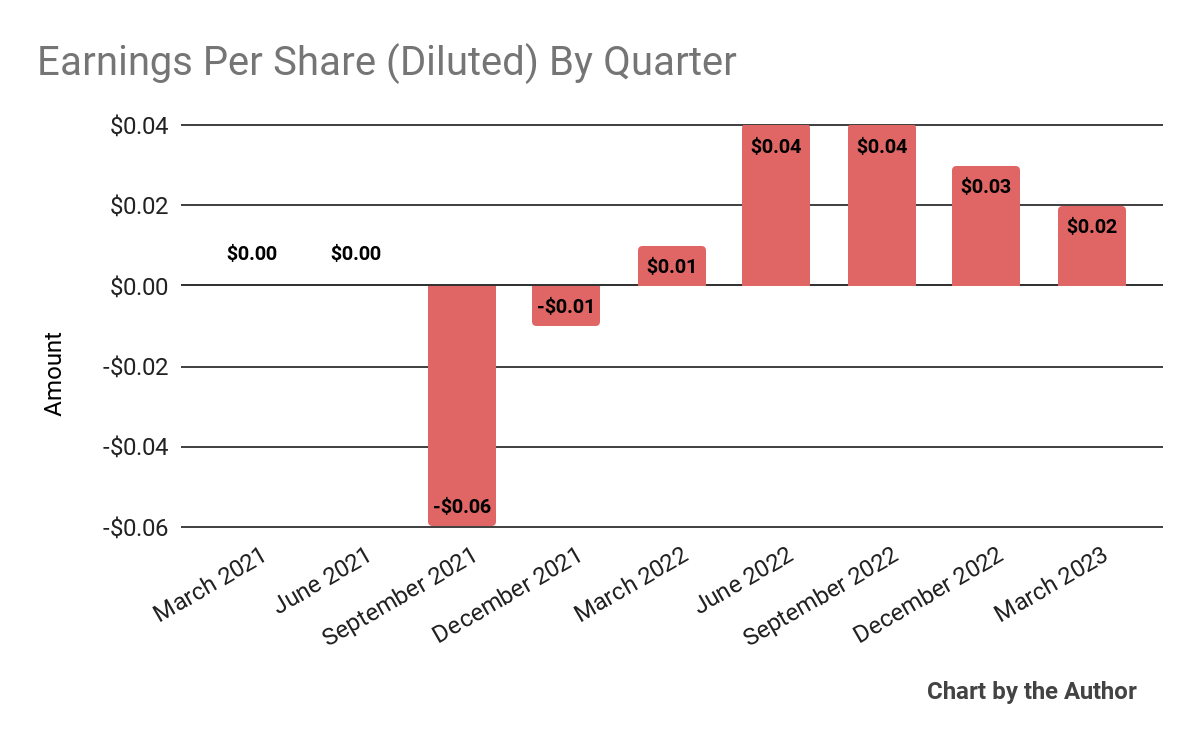

Earnings per share (Diluted) have been positive in each of the last five quarters:

{kind=link}

(All data in the above charts is GAAP)

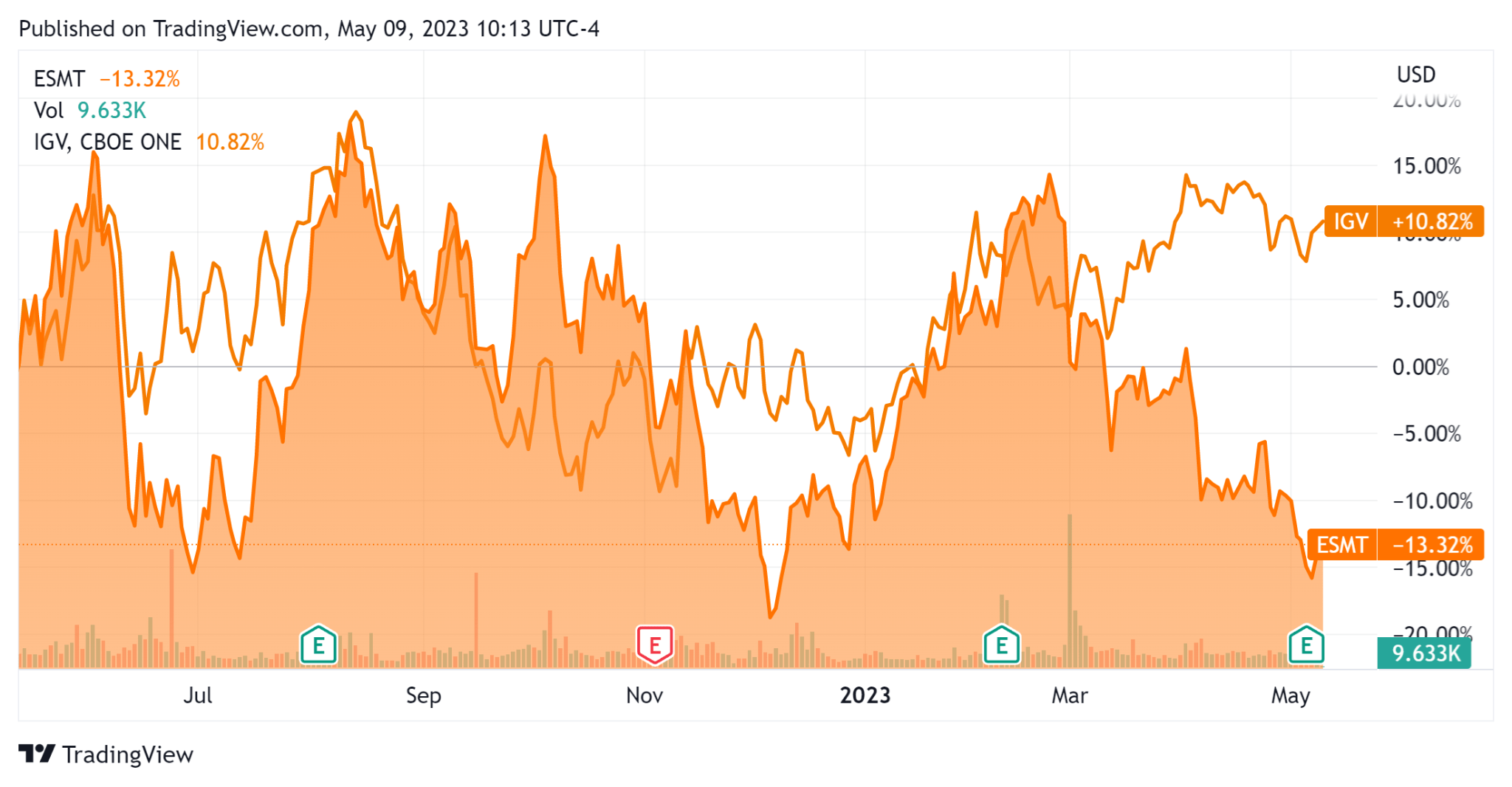

In the past 12 months, ESMT's stock price has dropped 13.32% vs. that of the iShares Expanded Technology-Software ETF's (IGV) rise of 10.82%, as the chart indicates below:

{kind=link}

For the balance sheet, the firm ended the quarter with $318.3 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was $50.9 million, of which capital expenditures accounted for $7.5 million. The company paid $16.1 million in stock-based compensation in the last four quarters, the highest figure in the past eleven-quarter period.

Valuation And Other Metrics For EngageSmart

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 7.3 |

| Enterprise Value / EBITDA |

| 62.1 |

| Price / Sales |

| 8.1 |

| Revenue Growth Rate |

| 37.6% |

| Net Income Margin |

| 7.0% |

| EBITDA % |

| 11.8% |

| Market Capitalization |

| $2,670,000,000 |

| Enterprise Value |

| $2,380,000,000 |

| Operating Cash Flow |

| $58,410,000 |

| Earnings Per Share (Fully Diluted) |

| $0.13 |

(Source - Seeking Alpha)

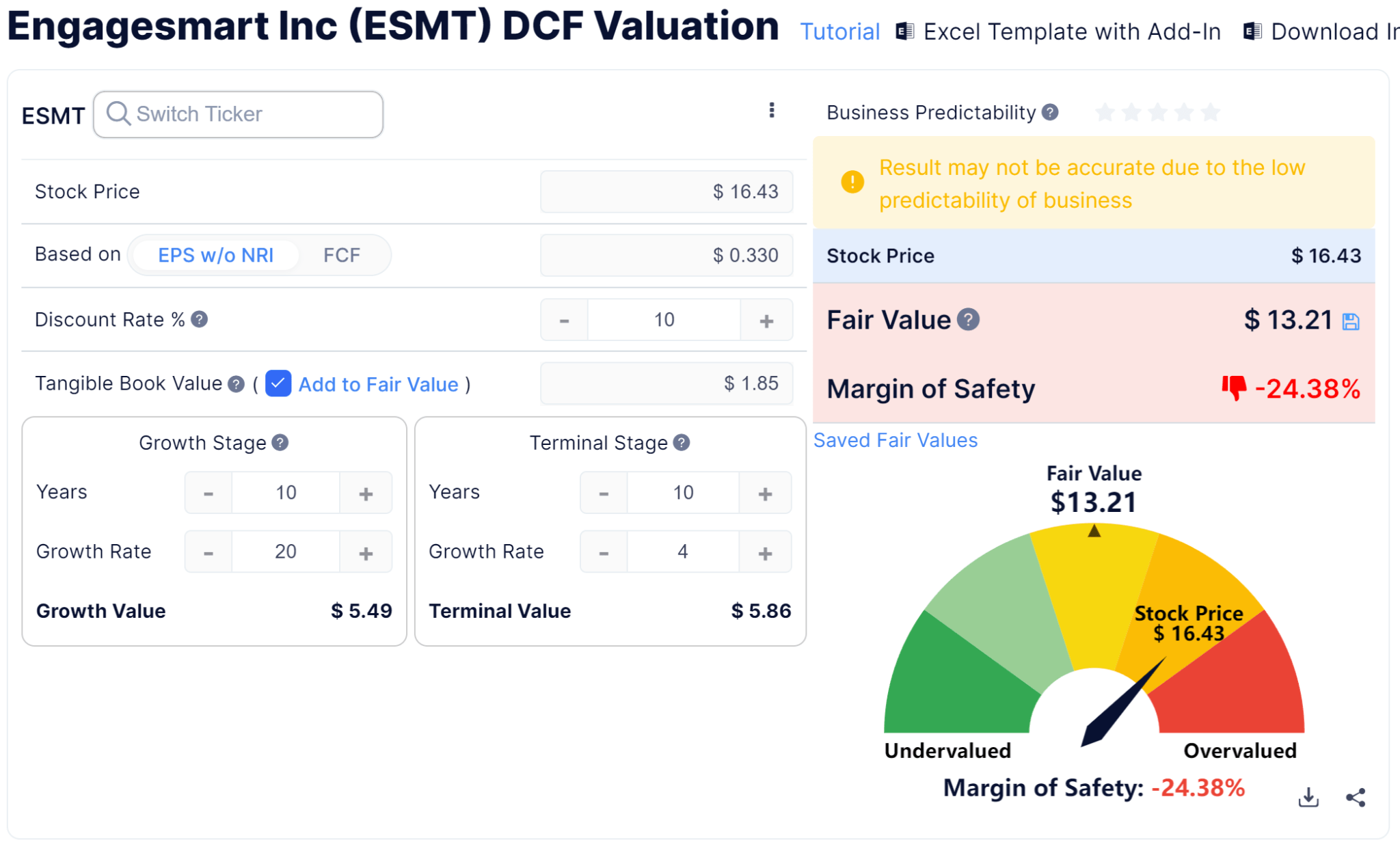

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm's projected growth and earnings:

{kind=link}

Assuming generous DCF parameters, the firm's shares would be valued at approximately $13.21 versus the current price of $16.43, indicating they are potentially currently overvalued, with the given earnings, growth, and discount rate assumptions of the DCF.

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

ESMT's most recent Rule of 40 calculation was 49.4% as of Q1 2023's results, so the firm has performed impressively in this regard, per the table below:

| Rule of 40 Performance |

| Calculation |

| Recent Rev. Growth % |

| 37.6% |

| EBITDA % |

| 11.8% |

| Total |

| 49.4% |

(Source - Seeking Alpha)

Commentary On EngageSmart

In its last earnings call (Source - Seeking Alpha), covering Q1 2023's results, management highlighted the growth of its SMB segment, growing 36% versus 25% for its enterprise segment.

The company's core vertical, mental health, saw increased demand due to rising mental health disorders amid therapist supply constraints.

Notably, management has been increasing its investment in creating communities for its products and initial results in its health care centric verticals have been 'enormous… In fact, we received over 10x the number of applications that we had room for'.

For its Enterprise segment, which focuses on government, utilities, non-profits and financial services, the company continues to develop strategic alliances to augment its direct efforts.

Management did not disclose any company or customer retention rate metrics other than to characterize their customer retention rates as 'excellent.'

Total revenue for Q1 2023 rose an impressive 31.2% year-over-year while gross profit margin edged up on 0.2%

SG&A as a percentage of revenue fell three percentage points, a positive sign of increasing efficiency and operating income continued to rise.

Looking ahead, management guided full-year 2023 revenue growth to be 26% with adjusted EBITDA of $70 million.

The company's financial position is very strong with ample liquidity, no debt and solid free cash flow generation.

Regarding valuation, the market is valuing ESMT at an EV/Sales multiple of around 7.3x.

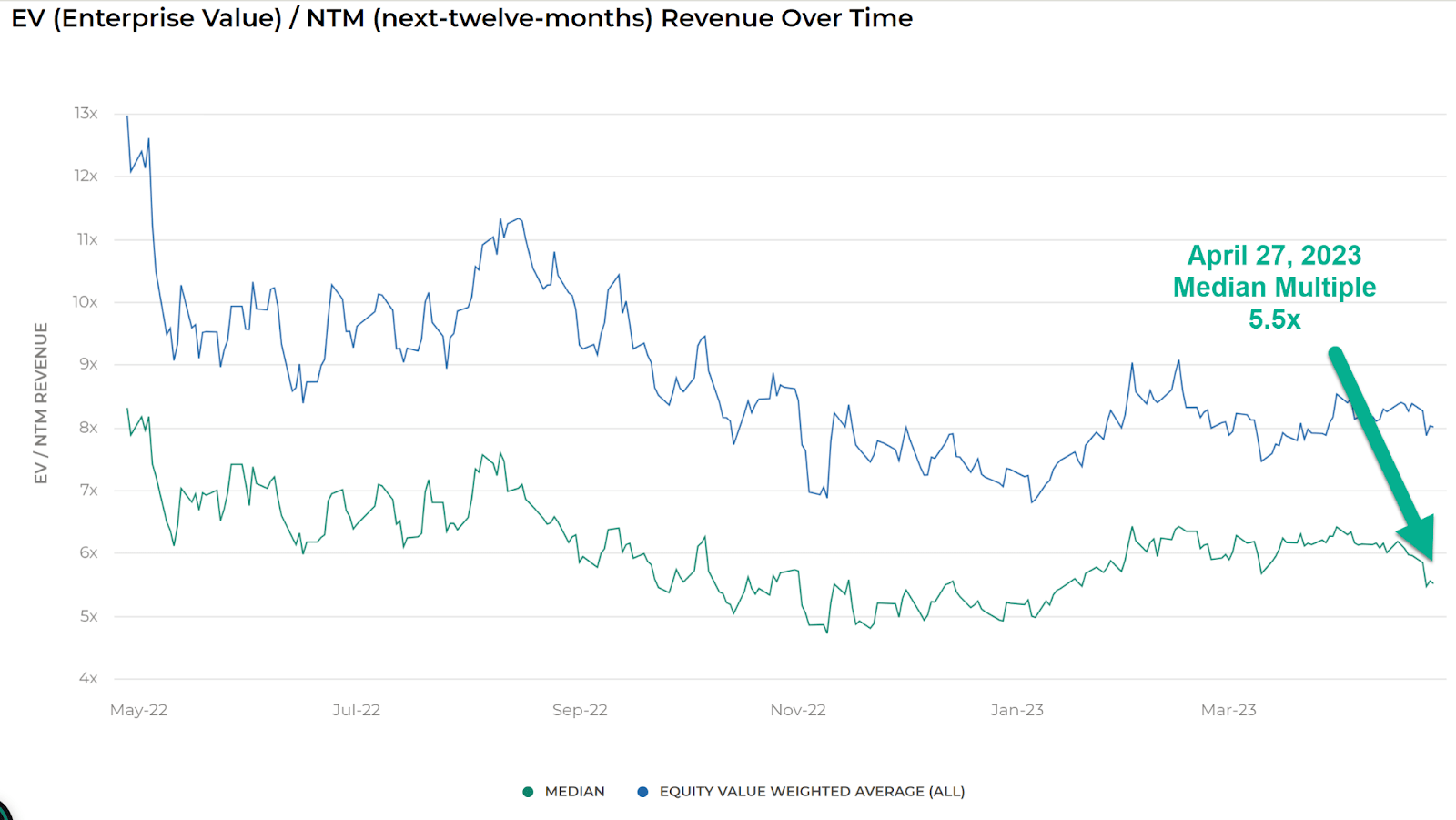

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.5x on April 27, 2023, as the chart shows here:

{kind=link}

So, by comparison, ESMT is currently valued by the market at a premium to the broader Meritech Capital SaaS Index, at least as of April 27, 2023.

The primary risk to the company's outlook is a macroeconomic slowdown that appears to be already underway, with tightening credit conditions that may affect customer spending plans and lengthening sales cycles that could reduce its revenue growth trajectory.

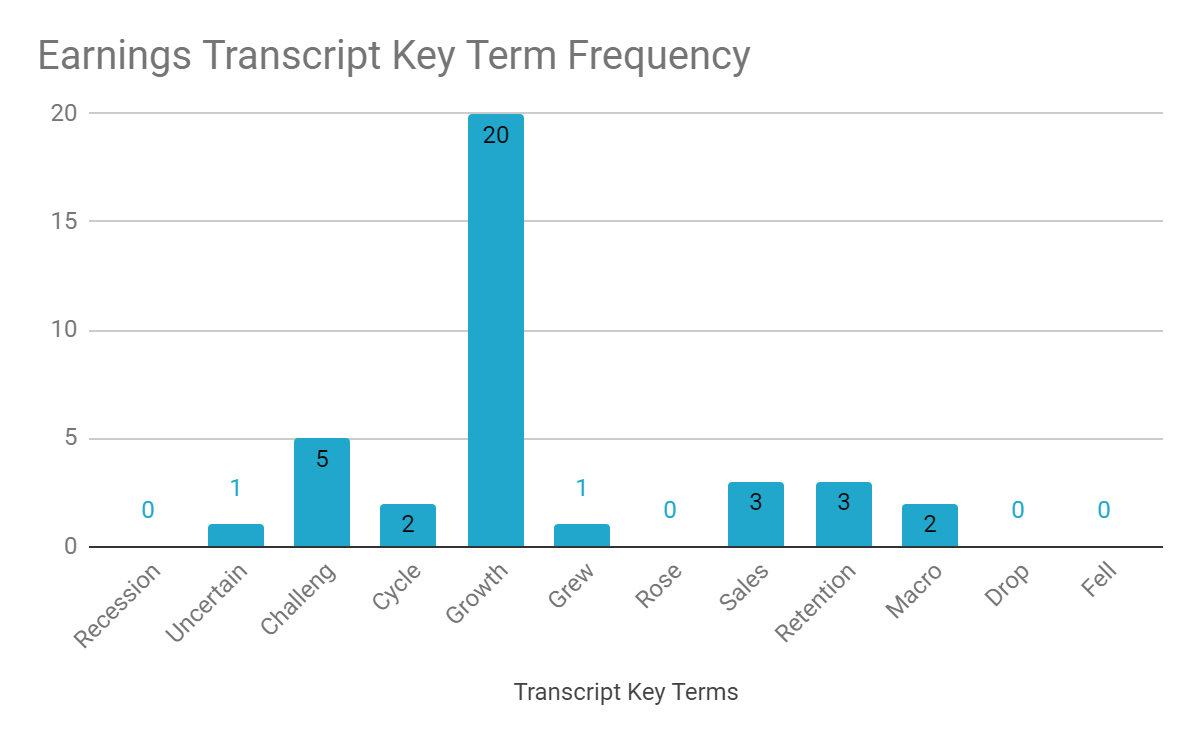

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

{kind=link}

I'm most interested in the frequency of potentially negative terms, so management cited 'Uncertain' one time, 'Challeng[es][ing]' five times, and 'Macro' two times in various contexts.

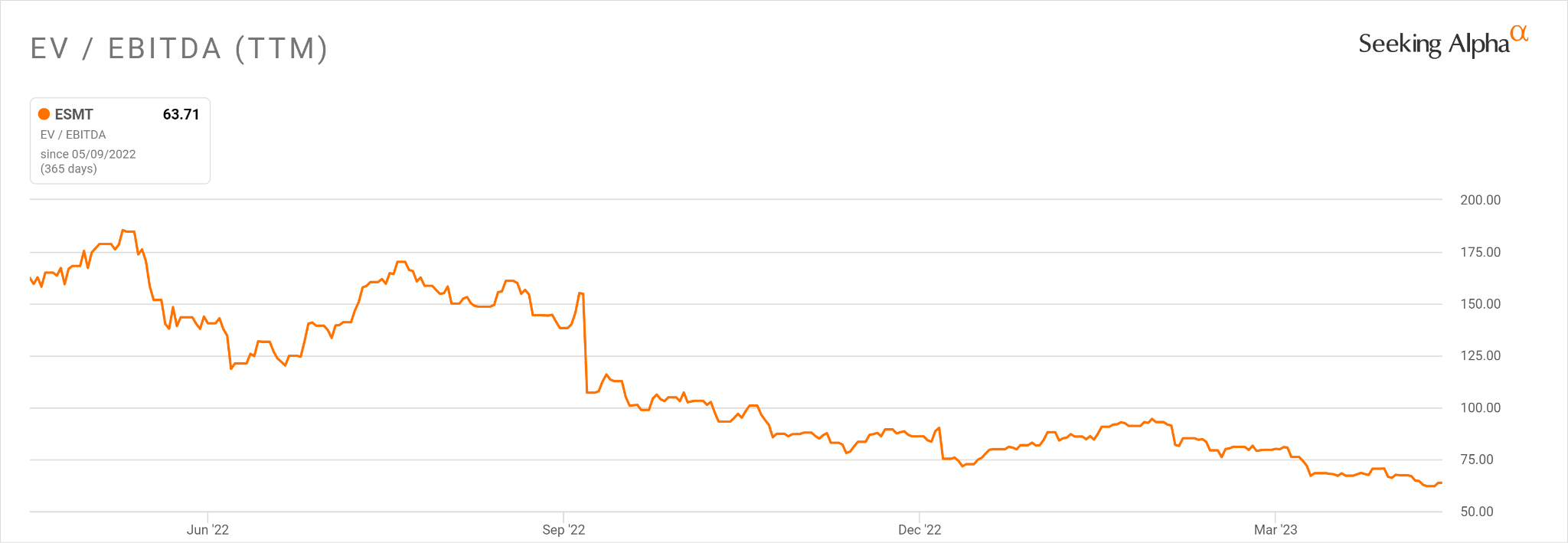

In the past twelve months, the firm's EV/EBITDA valuation multiple has fallen from a high of around 185 to its current 63.7x, as the chart from Seeking Alpha shows below:

{kind=link}

A potential upside catalyst to the stock could include a shallow economic downturn and pause on interest rate hikes, reducing downward pressure on its stock price multiples.

While I'm concerned about an economic rough period ahead, ESMT appears well-positioned to withstand a downturn with its focus on health care, government and utilities, although its DonorDrive offering is likely the most exposed to the negative effects of a slowdown.

For investors with a patient hold timeline, my outlook for ESMT is a Buy at around $16.50 per share.

For further details see:

EngageSmart Is Well Positioned For Growth Ahead