ET - EnLink Midstream: Not The Best Yield But Still Worth Buying For Growth

2023-05-01 10:36:57 ET

Summary

- EnLink Midstream, LLC is a rather unknown and underfollowed midstream company with significant forward growth potential.

- The company enjoys remarkably stable cash flows that are resistant to economic fluctuations and tend to grow with time.

- The company is positioned to deliver substantial growth in its carbon capture solutions business over the coming few years.

- The company has a very strong balance sheet.

- The yield is not as high as we would like, but it is respectable and sustainable.

EnLink Midstream, LLC ( ENLC ) is a midsized midstream company that operates in a few basins in the southcentral part of the United States. This company’s infrastructure includes a few regions that few other companies do, which is nice as it provides us with a certain level of diversification benefits. The fact that the company operates in different areas than many of its peers is not necessarily a problem for us, though, as it still enjoys many of the same characteristics as its larger peers, such as incredibly stable cash flows over time. This has allowed EnLink Midstream to pay out a significant portion of its cash flows in the form of distributions, which has given the company a 5.10% yield at the current price.

EnLink Midstream, LLC is not without growth prospects, however, and Citigroup ( C ) recently highlighted the company’s opportunities in carbon capture solutions ("CCS") and storage in a ratings upgrade. Overall, there could be some reasons to consider buying membership units of EnLink Midstream today, despite the fact that the company’s yield is not as high as we usually look for here at Energy Profits in Dividends.

About EnLink Midstream

As stated in the introduction, EnLink Midstream is a midsized midstream company with a market capitalization of $4.62 billion at the current price. This makes the company significantly smaller than many of the other major companies in the industry:

| Company |

| Current Market Capitalization |

| EnLink Midstream |

| $4.62 billion |

| Energy Transfer ( ET ) |

| $39.86 billion |

| Enterprise Products Partners ( EPD ) |

| $57.21 billion |

| MPLX ( MPLX ) |

| $35.03 billion |

| Crestwood Equity Partners ( CEQP ) |

| $2.60 billion |

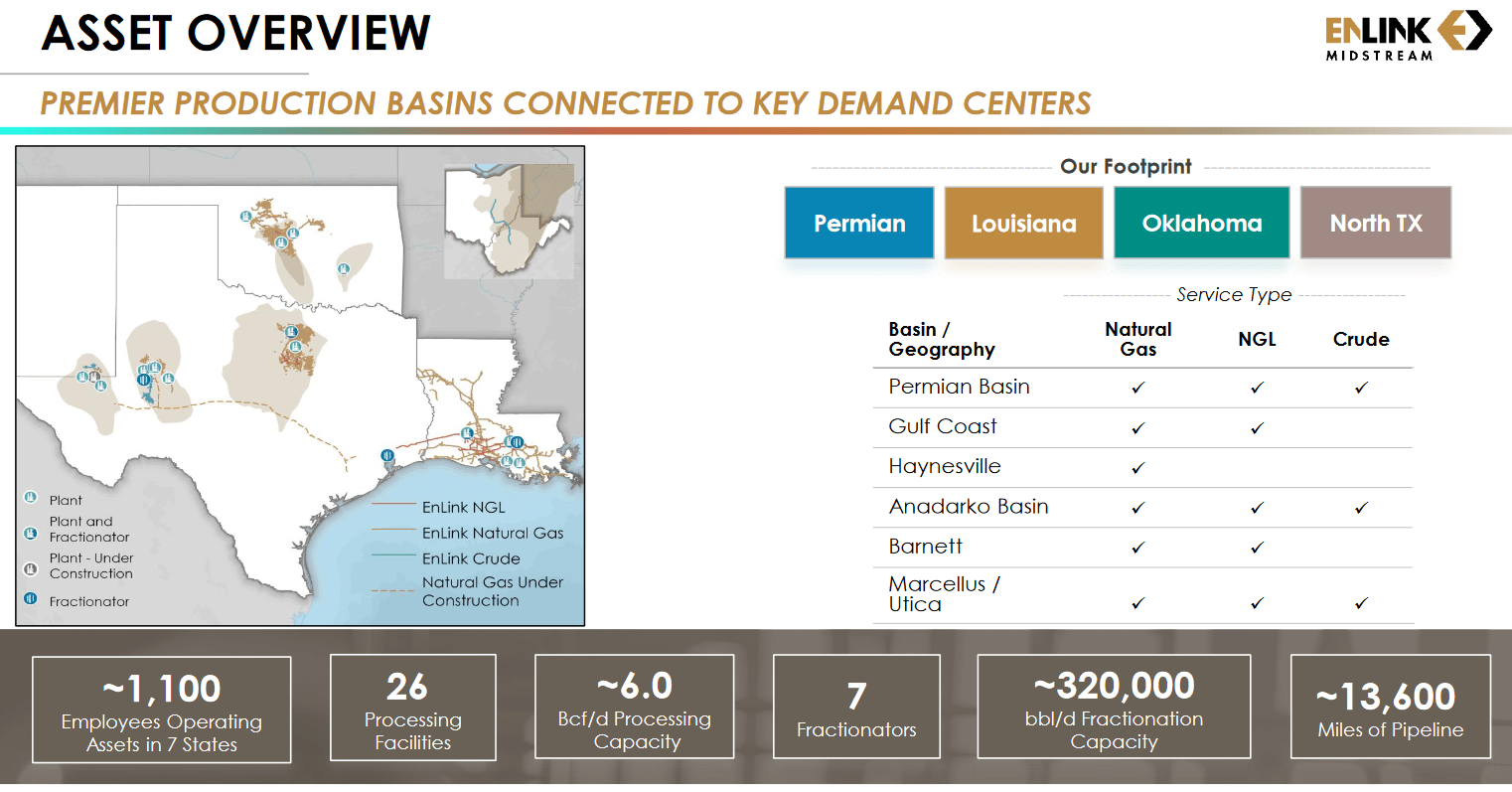

As might be expected from the company’s small size compared to some of the giant firms in the industry, EnLink Midstream’s reach only extends to a handful of basins. The company primarily operates in the Permian Basin, the Anadarko Basin, Haynesville Shale, and Barnett Shale. It also has a small operation in the Marcellus Shale:

{kind=link}

As we can easily see above, the company’s operations are primarily focused on providing midstream services for natural gas and natural gas liquids. This includes natural gas gathering and processing services as well as natural gas liquids fractionation. The company also has some intrastate pipelines in both Texas and Louisiana that are capable of carrying resources over longer distances than most gathering pipelines. These large pipelines are something that most companies of this size do not have. The fact that EnLink Midstream’s operations are mostly in natural gas and natural gas liquids is something that is quite nice to see as the fundamentals for these products are much stronger than the fundamentals for crude oil. I have discussed this in various previous articles, but it is mostly because natural gas turbines are being run along renewable power plants in those areas that are attempting to drive the developed world to electricity as a replacement for fossil fuels. All of the forward demand growth for crude oil comes from emerging markets as developed nations try to reduce their own consumption. It remains to be seen if this process will proceed as quickly as some politicians and environmental activists desire, but it cannot be denied that natural gas has a much stronger future.

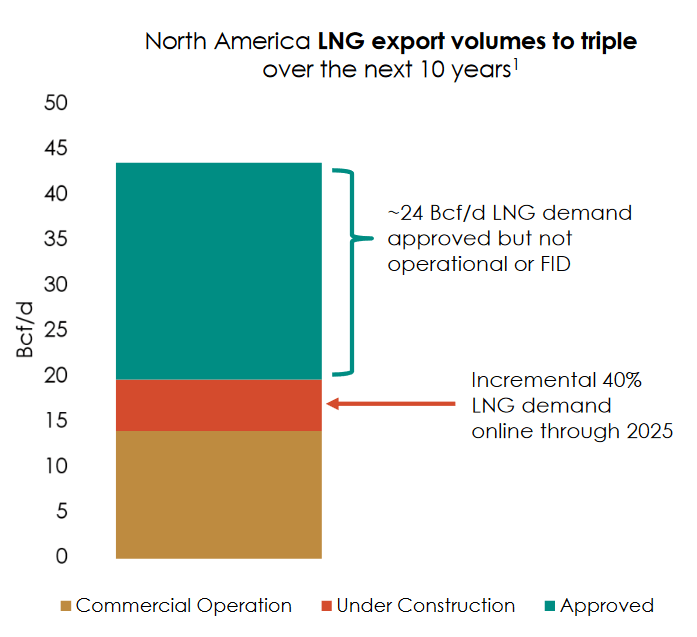

We can clearly see the strong future for natural gas by looking at the emerging North American liquefied natural gas industry. This industry is constructing a number of new facilities along the East and Gulf Coasts that will convert natural gas into a liquid state so that it can be exported. As I have pointed out in a few previous articles, the demand for natural gas from these facilities is expected to triple over the next decade:

{kind=link}

This benefits EnLink Midstream because its business model is based on transported resource volumes. In short, the company enters into long-term (typically five to ten years in length) contracts with its customers. Under the terms of these contracts, EnLink Midstream moves a customer’s natural gas, natural gas liquids, and crude oil through its network of pipelines and other infrastructure. In exchange, the customer compensates EnLink Midstream based on the volumes of resources that are transported. This provides the company with a great deal of insulation against volatile energy prices. This can be both a blessing and a curse as it protects the company against steep declines in energy prices like what happened in the second half of 2022 or in 2020 after the imposition of the COVID-19 lockdowns. However, it also prevents the company from being able to benefit from periods of strength in resource pricing, like what happened following the outbreak of hostilities between Russia and Ukraine. Rather than having performance that varies with resource prices, EnLink Midstream’s cash flows are remarkably stable. As we can see here, the company’s cash flows were almost entirely unaffected by any macroeconomic events:

{kind=link}

(all figures in millions of U.S. dollars)

As we can clearly see, the company’s cash flows exhibited remarkable stability along with some growth over the past ten years, despite the fact that energy prices were all over the place during that period. This is exactly the kind of thing that we like to see in an income play since stable and growing cash flows provide a great deal of support for the distribution that the company pays out. After all, it is much easier to budget for a large dividend when management can be certain that the company will earn a similar amount of money next year. It is also rather nice for more conservative investors since we do not have to suffer from stress worrying about how changes in energy prices could affect the companies that are in our portfolios.

EnLink Midstream is well-positioned to grow its cash flow going forward. As just discussed, the demand for natural gas from a number of natural gas liquefaction plants is expected to surge over the coming ten years. Although there are a few places where these plants are being constructed, a significant percentage of them are in Louisiana, where EnLink Midstream has a significant intrastate presence. We can see this on the map above. As the demand from these facilities increases, someone will need to transport the natural gas to the facilities to meet this demand. EnLink Midstream’s substantial operations should allow the company to benefit from higher volumes transported as this scenario plays out. As EnLink Midstream’s cash flows are directly correlated to the volume of resources that it transports, this should result in cash flow growth for the company going forward.

Carbon Capture Potential

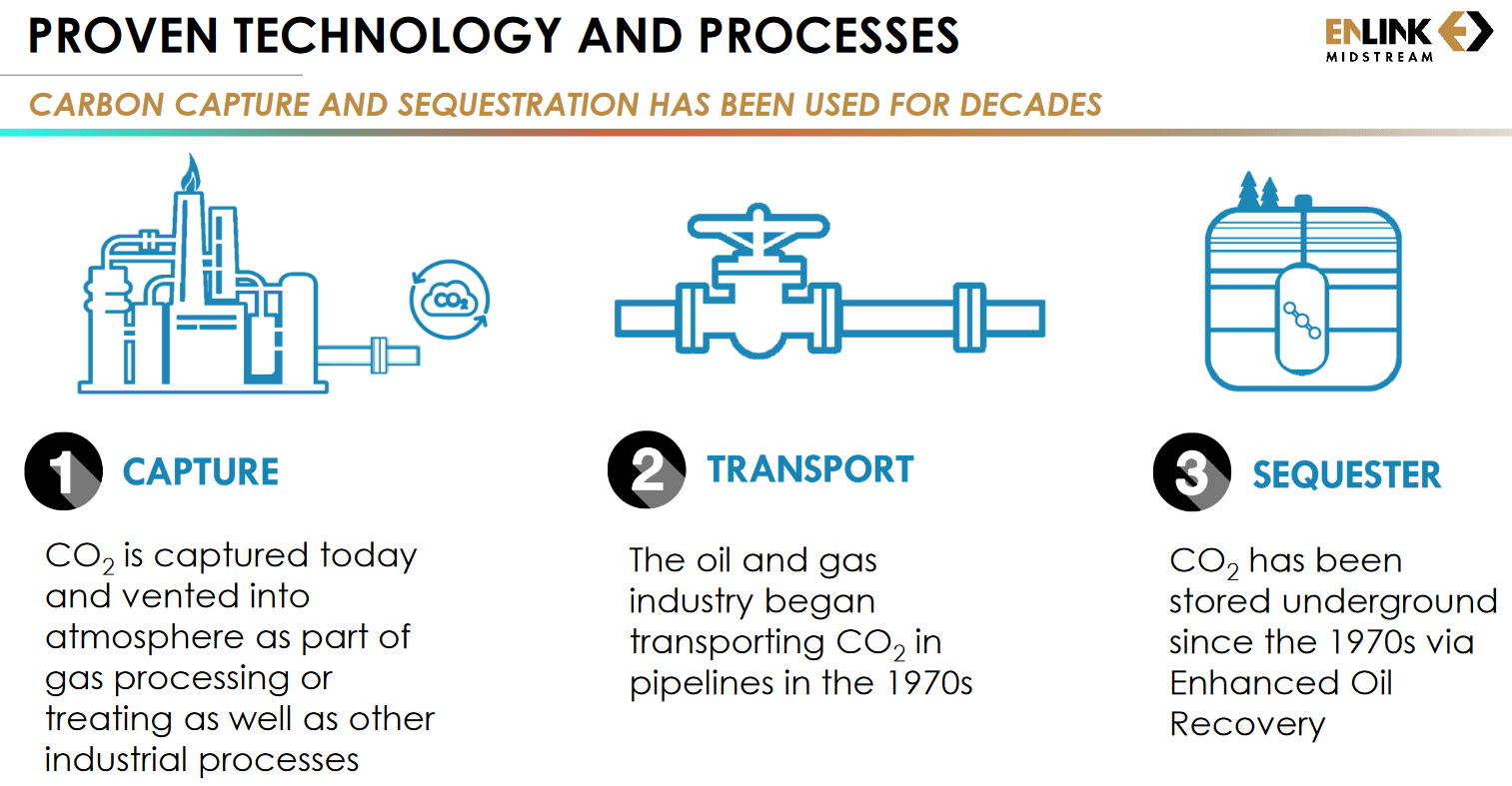

As mentioned in the introduction, Citigroup recently upgraded EnLink Midstream to a buy because the current stock price is not taking the company’s opportunities in carbon capture solutions into account. Carbon capture and storage refers to the process of capturing carbon dioxide emissions from industrial sources, such as a refinery or factory, and transporting it to a place where it can be stored instead of being vented into the atmosphere. Although this is something that is advertised as a new process, it has actually been used since the 1970s:

{kind=link}

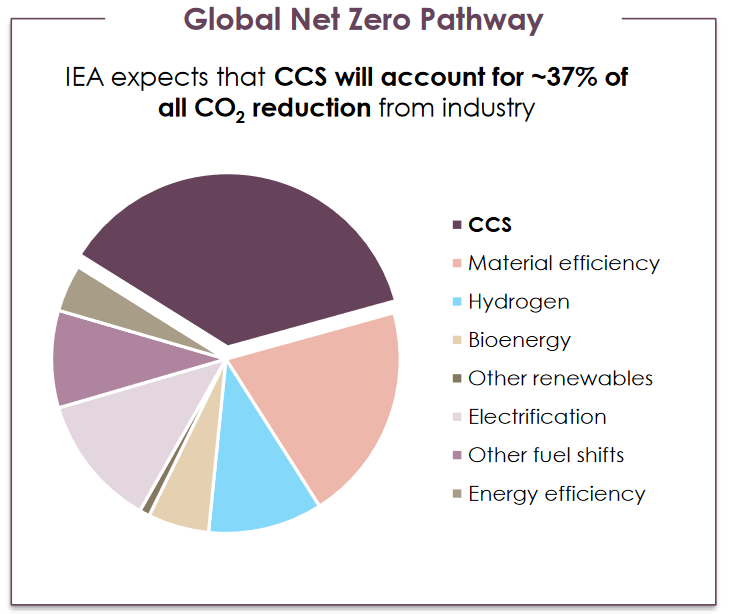

Although the technology has been used by the fossil fuel industry for decades, it has seen increasing popularity in the past ten years or so due to rising pressure from environmental groups and “stakeholder-focused” institutional investors. The International Energy Agency expects that carbon capture technology will account for 37% of the total required emissions reductions required for the world to achieve net-zero carbon emissions by 2050:

{kind=link}

That works out to carbon capture technologies being used to capture 7.6 billion tons of carbon dioxide emissions annually in 2050, which is a fairly dramatic increase from the forty million tons annually that these technologies are currently collecting.

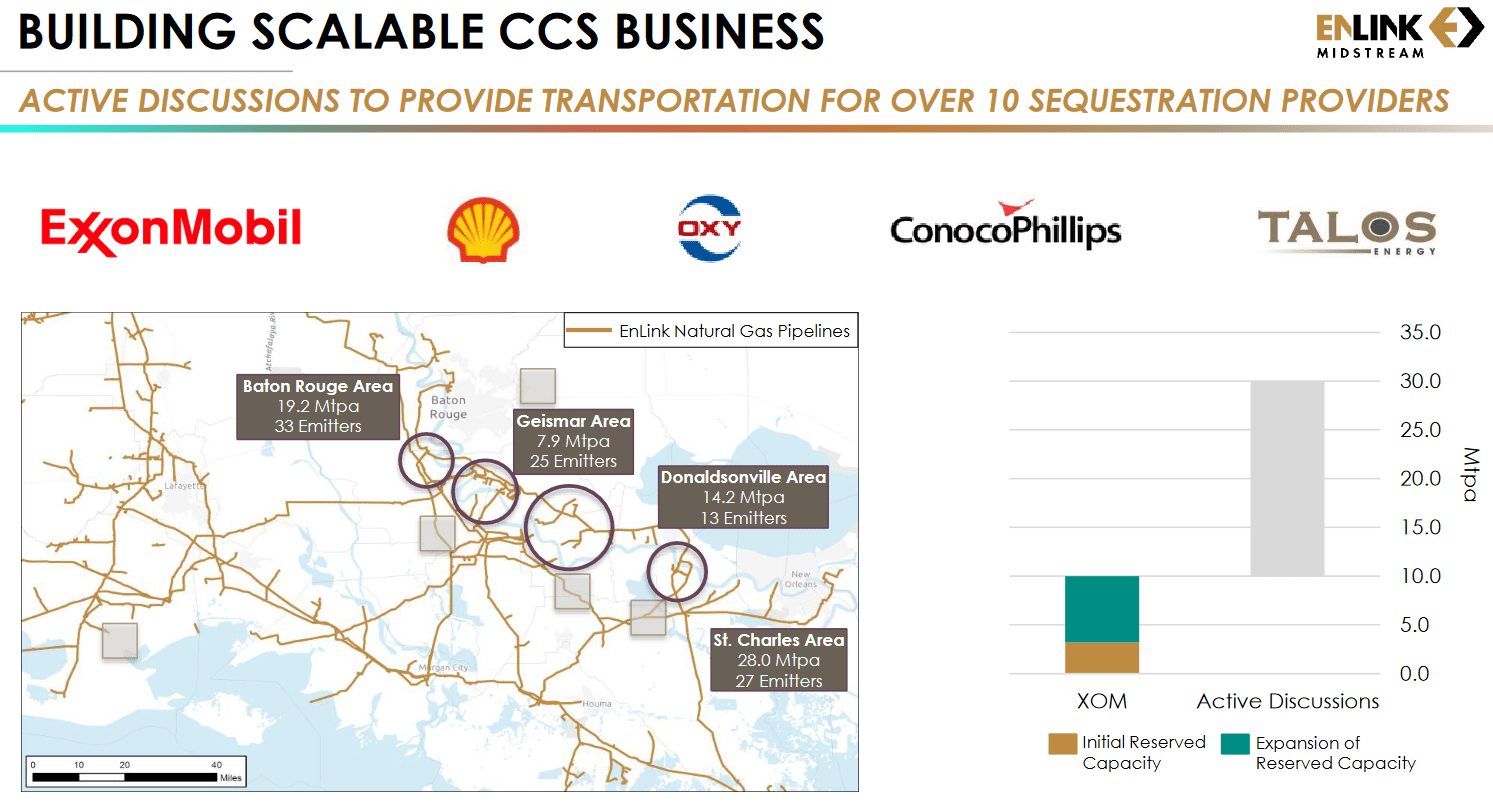

EnLink is working to deploy carbon capture technologies in Louisiana, which is the second-largest industrial carbon-emitting state in the United States. The state’s various industries produce 135 million tons of carbon emissions every year, with the Mississippi River Corridor alone producing 80 million tons of carbon emissions annually. It is the Mississippi River Corridor that EnLink Midstream considers to be its target market as its existing pipelines can be used to transport any carbon collected to underground storage facilities. As we can clearly see, the opportunity here is huge as this corridor produces twice the carbon emissions as were collected by all carbon capture technologies globally in 2020.

EnLink Midstream is currently moving to take advantage of this situation. As Citigroup notes in its report, the company is currently in discussions to enter into a long-term contract to collect twenty million tons of carbon dioxide per year in the corridor. This would triple the size of its business, as the company is currently only collecting about ten million tons per year today.

{kind=link}

As we can clearly see, the company clearly is positioned to transport far more than the thirty million tons that it would have after the current discussions conclude with a contract in place. Its current footprint includes a number of companies that are currently emitting significant levels of carbon that could become customers of EnLink Midstream’s carbon capture and storage business. As these contracts would work much like its midstream contracts in that they provide stable cash flows based on volumes transported, we can see the potential for significant improvement in the company’s cash flows on a permanent basis. This will obviously benefit investors in the company.

Financial Considerations

It is always critical that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and then using the money to repay the maturing debt. This can cause a company’s interest expenses to increase following the rollover depending on the conditions in the market. As of the time of writing, interest rates are at the highest level that we have seen since 2007 so that could be a very real concern today. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes its cash flows to decline could push it into financial distress if it has too much debt. Although midstream companies like EnLink Midstream tend to have remarkably stable cash flows, this is still a risk that we should not ignore.

The usual metric that we use to evaluate a midstream company’s debt level is the leverage ratio, which is also known as the debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it would take the company to completely repay all its debt if it was to devote all its pre-tax cash flow to that task. As of December 31, 2022, EnLink Midstream had a leverage ratio of 3.4x based on its trailing twelve-month adjusted EBITDA. This is a reasonable ratio that is relatively in line with the best companies in the industry. As I have pointed out before, Wall Street analysts usually consider anything under 5.0x to be acceptable for a midstream company. However, many companies in the sector have been working to get their ratios down under 4.0x ever since the pandemic, and that is also where I like to see it in order to add a margin of safety to the investment. EnLink Midstream is clearly in that range and as such the company appears to be running with a reasonable financial structure right now.

Distribution Analysis

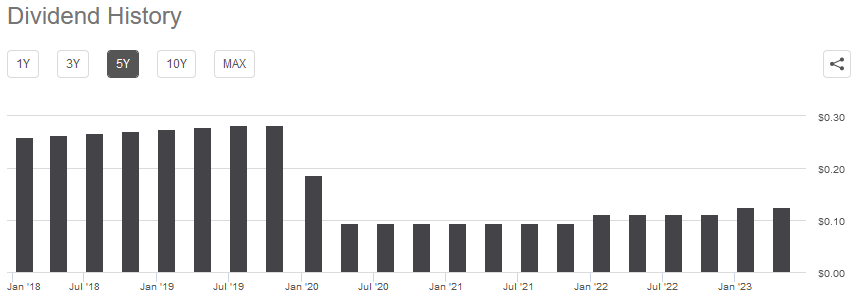

One of the biggest reasons why investors purchase units of midstream companies like EnLink Midstream is the very high distribution yields that these companies typically possess. This comes from the fact that they have relatively low growth rates, so they pay out a significant percentage of their cash flows to investors in order to provide an acceptable return. These companies also tend to not be assigned very high multiples by the market, so the distribution ends up being a sizable percentage of the share price. For its part, EnLink Midstream yields 5.48% at the current price. This is certainly a respectable yield, but EnLink has unfortunately not been very consistent about its distribution in the past:

{kind=link}

As we can clearly see, the company cut its distribution twice in 2020, which was a reversal of the increasing payouts that it had prior to that time. This is a major disappointment and will likely reduce the appeal of the company in the eyes of some investors. However, it is important to keep in mind that EnLink Midstream was hardly alone in its actions during this year. As we can all recall, the energy industry in general faced a great deal of uncertainty in 2020 as the pandemic-induced lockdowns caused people to severely curtail travel and reduce their demand for crude oil. This caused prices to fall and numerous upstream producers to scale back on their drilling plans. EnLink Midstream’s cash flows held up just fine, but the reduced drilling activity meant that some of the planned growth was no longer likely. It also became difficult for anything related to the fossil fuel industry to raise capital. As a result, several midstream companies cut their distributions to reduce debt and become financially independent. It was a smart move, even though investors got punished at the time. Fortunately, though, anyone buying today will not be affected by the events of the past and will receive the current distribution and yield. As such, the most important thing for us today is determining the company’s ability to maintain its current distribution.

The usual metric that we use to evaluate a midstream company’s ability to maintain its distribution is the distributable cash flow. Distributable cash flow is a non-GAAP measure that theoretically tells us the amount of cash that was generated by a company’s ordinary operations that is available to be distributed to the unitholders. Curiously, EnLink Midstream did not report a distributable cash flow for 2022, although the company stated that it expects to have $915.0 million in distributable cash flow during 2023. That would be more than sufficient to cover the $235.0 million that the company intends to pay in distributions this year.

However, we are concerned with 2022 and the company did not report a distributable cash flow during that year. We can look at its free cash flow, though. Free cash flow is the amount of cash that was generated by a company’s ordinary operations that is left over after it pays all of its bills and makes all necessary capital expenditures. This is the money that can be used to reduce debt, buy back units, or pay a distribution to investors. Over the full-year 2022 period, EnLink Midstream had a levered free cash flow of $517.0 million and paid out $221.4 million in distributions. It, therefore, appears as though the company was able to easily cover its distributions with quite a lot of money left over that can be used for other purposes. The distribution appears to be quite safe right now and we do not need to worry.

Conclusion

In conclusion, EnLink Midstream, LLC is a somewhat underfollowed midstream firm that has a great deal of potential in the emerging carbon capture solutions industry. This could ultimately be a source of growth for the company that would allow it to continue on its historic trajectory of delivering year-over-year cash flow growth during most periods. The company boasts a very solid balance sheet and an attractive, sustainable distribution. Admittedly, the yield is not as high as some other midstream companies, but EnLink Midstream makes up for this with growth potential. The company appears to be worth buying right now in light of this.

For further details see:

EnLink Midstream: Not The Best Yield, But Still Worth Buying For Growth