TSLA - Enphase: No Time To Waste Consider The Stock Now

2023-09-11 14:02:57 ET

Summary

- Enphase has been out of favor, due to interest rate headwinds and higher inventory levels.

- Still, the company is well-positioned to benefit from the growing demand for solar energy, which is expected to grow at a CAGR of 18% by 2030.

- International expansion and new product launches are expected to fuel further growth, while the multiple contraction has created a great opportunity for value investors.

- The company is trading at the highest free cash flow yield in years at 4.86%, is highly profitable with an industry-leading profit margin of 20% and has an average ROIC of 14% over the last 5 years.

- The superb cash flow generation made it possible to reinvest heavily in the business and stop the dilution of shareholders with share buybacks.

Enphase ( ENPH ) is beaten up year-to-date and down more than 50%. I have been amazed by the business in the past years, but the stock was out of reach for me based on valuation. However, the multiples have gone down, the business is more profitable than ever before and the dilution of shares has stopped. Therefore, I think Enphase requires more attention and could be a great investment to ride the secular solar trend.

Business Overview

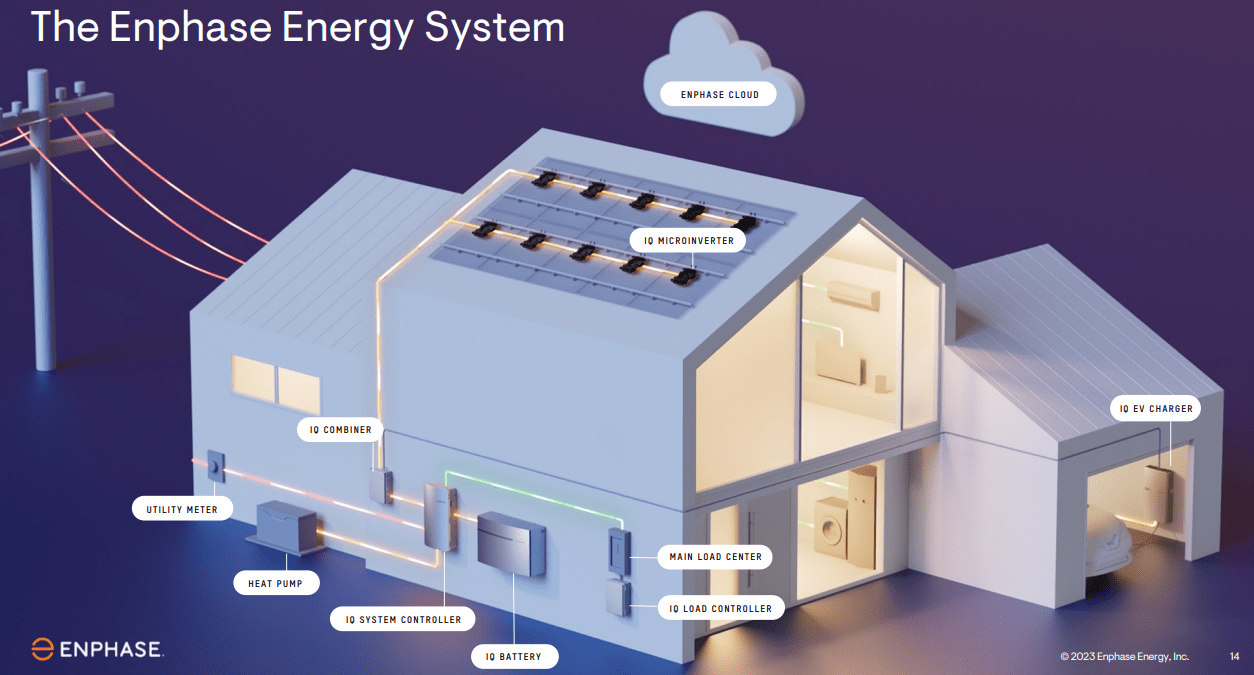

Enphase Energy , Inc. is a global energy technology company that designs, develops, manufactures, and sells microinverter-based solar-plus-storage systems. The company's semiconductor-based microinverter system converts energy at the individual solar module level, which provides a number of advantages over traditional solar panel systems, including:

- Increased energy production: Microinverters track the output of each solar module individually, which can lead to up to 25% more energy production than traditional solar panel systems.

- Improved reliability: Microinverters are less vulnerable to shading, rain or snow than traditional solar panel systems, which can lead to higher reliability and uptime. Each microinverter is isolated from the others, so if one fails, it does not affect the rest of the system.

- Enhanced monitoring and control: Enphase's microinverters come with a built-in monitoring system that allows homeowners to track their energy production and usage in real time.

Enphase's IQ8 microinverter is the world's first grid-forming microinverter, capable of providing backup power without a battery by forming a microgrid during a power outage relying solely on sunlight.

Further, Enphase is about to launch a new microinverter product. The IQ8P is targeted at a small commercial market in North America and Europe, and emerging residential markets (Brazil, Mexico, India, etc). The new product should support panels up to 650 watt DC, more than enough to provide full energy from the latest Tiger Neo solar panel of JinkoSolar ( JKS ), with power estimated at 635W.

The company has shipped over 68 million microinverters and over 3.5 million Enphase-based systems have been deployed in more than 145 countries. Enphase's customers include residential homeowners, commercial businesses, and utilities.

In addition to its microinverter systems, Enphase also offers a variety of solar-plus-storage products, including batteries, energy management software, and EV charging systems. These products allow homeowners to store excess solar energy for use at night or during power outages, to better manage their energy consumption and charge their electrical vehicles.

The company's main competitors are SolarEdge Technologies ( SEDG ), SMA Solar Technology ( SMTGF ), Tesla ( TSLA ) and Fronius International.

{kind=link}

The Bigger Picture

In the near term, Enphase is facing some challenges, including the impact of higher interest rates on loans and a new net metering program in California (NEM 3.0). Nevertheless, the company is confident that it can overcome these challenges and continue to grow its business.

Higher interest rates in the U.S. and Europe have an impact on the interest on loans. Each rate hike makes it more expensive to loan money, which creates a slowdown in long term investments, like placing solar panels and batteries. Moreover, the largest solar market state in America, California, is making changes to their net metering program. Under NEM 3.0 , the value of solar energy credits decreased by 75% for new California solar customers. Therefore, it has an impact on the payback time of the solar system, lowering the incentive to place a new solar installation.

On the other hand, solar panel prices are steadily declining, making them cheaper than ever, but also more efficient than ever before. Besides, the still elevated energy prices have two large benefits when you own a solar system. The first one is that you have less costs on your energy usage and the second one is that you can earn more money by sending excess green energy back into the grid.

Lafayette College

The upgraded tax credit ('ITC') for renewable energy projects is another tailwind in America. Between 2022 and 2032, taxpayers may claim 30% of capital costs when starting an eligible solar project.

Enphase is well-positioned to benefit from the growing demand for solar energy. The global solar market is expected to grow at a compound annual growth rate of 18% by 2030. Further, the global solar-plus-storage market is expected to grow at a CAGR of 24.2% by 2030. Enphase is well-positioned to capture a significant share of this growth due to its leading market position and its innovative technology.

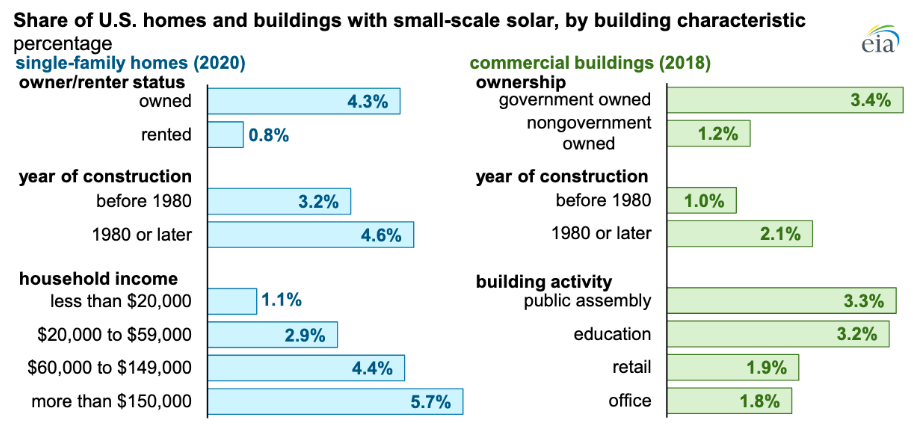

Surprisingly, by the end of 2022, only 6% of single-family owner-occupied homes had solar panels installed in the U.S., up from 4.3% in 2020. This shows that there is still immense growth left in the solar industry for America, so even while the market is currently slowing down, it should be temporary.

Energy Information Administration

{kind=link}

Furthermore, in the latest earnings call the CEO, Badri Kothandaraman, mentioned that they are opportunistic about sales growth in Europe:

And Europe for us is underpenetrated. In general, we are very strong in Netherlands and France. We are upcoming in Germany. But for us, the other -- other countries are almost a blue ocean. Like Italy, U.K., Sweden, Denmark, Greece, Austria, Switzerland, Poland. We are entering all of those regions. And so we are extremely bullish on Europe.

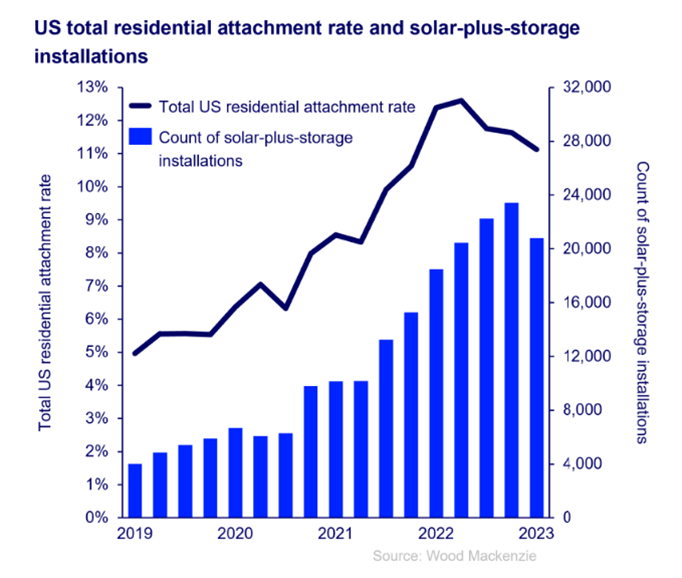

Together with the rise of electrical vehicles, the battery or energy storage attach rate has been increasing rather quickly. Despite the recent drawback, the overall trend is bullish for Enphase's solar-plus-storage systems, which are supported with one the best software platforms out there.

{kind=link}

Valuation

Historically, Enphase has not traded cheaper since the COVID-19 crash. Considering Enphase's earnings per share is expected to grow 9% in 2023, 32% in 2024 and 30% in 2025, the forward price-to-earnings is relatively inexpensive at 24x. Zooming out to 2024 and 2025 the forward price-to-earnings are respectively, 18x and 14x. Since the PEG ratio is well-below 1, I believe we can assume Enphase is an undervalued growth stock.

Additionally, when we compare Enphase with some of the publicly listed competitors, it is visible that Enphase is by far the cheapest based on enterprise value to free cash flow. Two reasons are the company's strong profitability and CAPEX lite business model.

Enphase has not traded at a higher free cash flow yield in last 5 years. The free cash flow yield is now standing at almost 5%, which is pretty impressive for a growing business. Some might say that comparing SolarEdge based on free cash flow is unfair, yet the PEG ratio of Enphase is also lower than that of SolarEdge.

So while Enphase has been the cheapest stock compared to peers, they also have the highest gross margin. This showcases how efficiently run the company is and the amount of pricing power the Enphase brand has in my view.

On top of that, Enphase's profit margins are again outperforming competitors by far. The large benefit of all this is that the business does not demand a lot of resources, and everything that is leftover can be reinvested in R&D, M&A or now share buybacks to counter dilution from stock-based-compensation. In case we see a recession, Enphase will be the last man standing and able to take over market share while remaining the leader in innovation due to better capital returns. In the last earnings call, the CEO mentioned that the higher margin IQ8 microinverter will soon be introduced in Europe, which can further improve profit margin:

Let's now cover Europe. Our European business remains strong. Q3 is typically down due to summer vacation, but our year-on-year growth trend is very robust. We plan to introduce IQ8 microinverters and batteries into more countries in Europe such as Sweden, Denmark, Greece, U.K. and Italy later this year.

Enphase has built up a strong balance sheet with a current ratio around 3.4x. As a result, the management is able to start doing share buybacks to stop the dilution of the shareholders. In the second quarter, Enphase bought back 1.25 million shares at an average price of $159.43 for a total of $200 million.

A new $1 billion buyback program got announced as well, the CEO had this to say about it in the Q2 earnings call:

I'm happy to announce that our Board of Directors has authorized a new share repurchase program. Given our confidence in Enphase's future growth, free cash flow generation and the value we see in our stock, our Board has authorized an additional $1 billion for share repurchases.

Takeaway

Overall, Enphase is a leading player in the solar energy industry. The company has a strong track record of innovation and growth, and it is well-positioned to benefit from the growing demand for solar energy.

The secular solar tailwind seems far from over and the temporary headwinds in North America overshadow the international growth ahead. The relentless focus on cost efficiencies has created a highly profitable business, that can easily reinvest profits in the business, and secure their dominant position for the foreseeable future. Knowing that Enphase has an average return on invested capital of 14.6% over the last 5 years, investors can rest assured money is invested well. Another positive for shareholders is the end of dilution, equity raises should not be needed anymore and share buybacks are expected to easily cover stock-based compensation going forward.

The third quarter is expected to be the weakest for 2023, as inventory levels are getting a correction. Nonetheless, the business is completely fine and should be back on track by 2024 with new product launches coming globally. Enphase has an edge on competitors with their highly innovative microinverters and software ecosystem that is especially user-friendly.

Shares might drop lower in the coming months with the arrival of the third quarter, but I rate Enphase a 'Strong Buy' at $120 a share. At this price level, investors have a high chance to outperform the market in my opinion. If we see further downward pressure, I'll be a massive buyer of this excellent company.

For further details see:

Enphase: No Time To Waste, Consider The Stock Now