FSLR - Enphase Vs. First Solar: The Solar Investment Thesis May Have Bottomed

2024-01-17 09:00:00 ET

Summary

- We are seeing early signs of optimistic reversal in ENPH's investment story, with the Fed's potential pivot in Q1'24 likely to bring forth improved residential solar installations.

- At the same time, FSLR's utility scale solar panels remain in hot demand, with its growing backlog extended through 2030 at favorable ASPs.

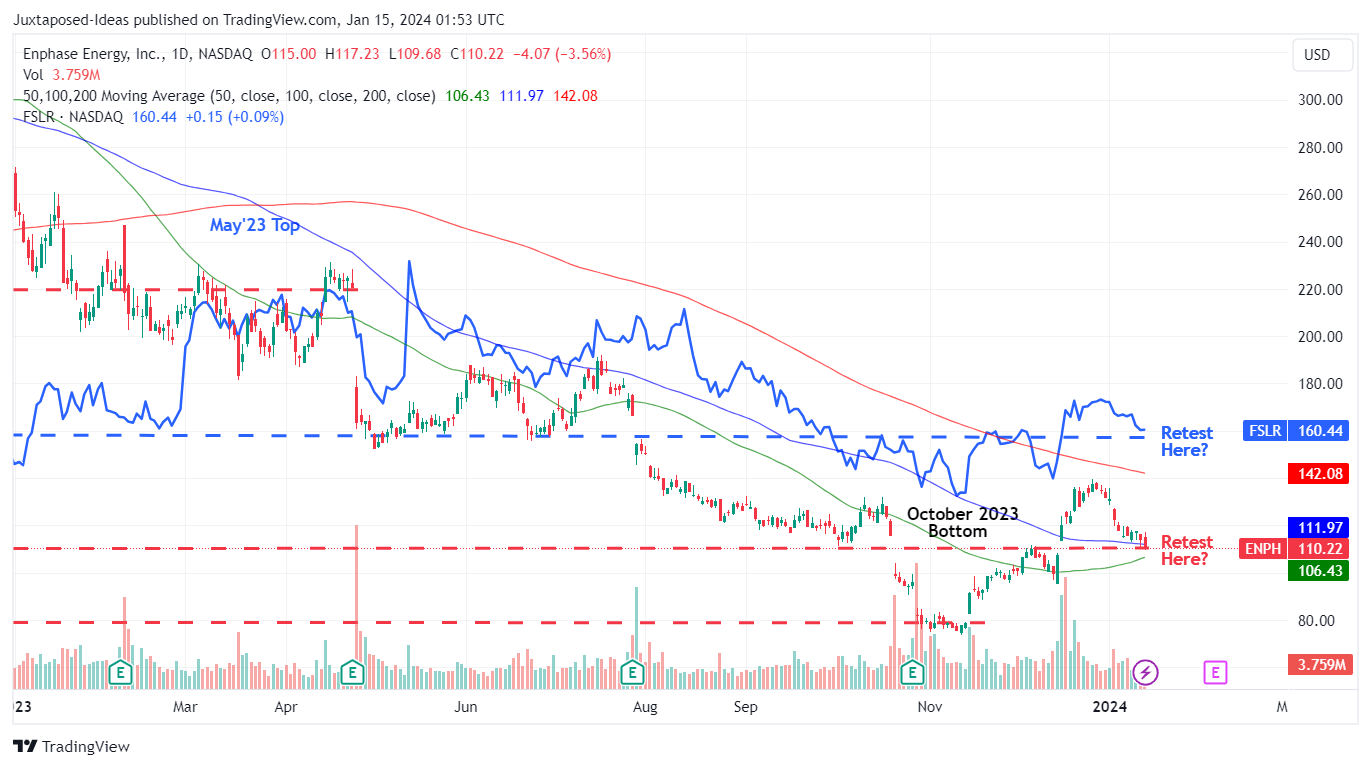

- After the bounce from the October 2023 bottom, it appears that the solar investment thesis has improved drastically, offering interested investors with a more viable entry point.

- Both FSLR and ENPH offer highly attractive risk-reward ratios at current level, with their upward rerating likely to occur as the macroeconomic outlook normalizes.

- Buy at any dips.

We previously covered First Solar (FSLR) and Enphase Energy (ENPH) in October 2023, discussing Mr. Market's pessimism surrounding multiple electrification stocks, attributed to the rising borrowing costs for mortgages and autos, triggering tightened discretionary spending.

At that time, it was apparent that ENPH's residential solar prospects had been impacted with the US/ EU reporting slowing retail demand and inventory correction. In a direct contrast, FSLR's utility scale solar panels had been in hot demand then, with its backlog extended through 2030 at favorable ASPs.

As a result of the intermediate term uncertainty, we had rerated the FSLR stock as a Buy then, while downgrading the ENPH stock as a Hold then.

In this article, we are seeing signs of optimistic reversal in the solar investment story, with the cooling inflation and Fed's potential pivot in Q1'24 likely to bring forth improved residential solar installation as existing/ new home sales recover.

Most importantly, assuming that the October 2023 bottom holds, we may see ENPH and FSLR offer highly attractive risk reward ratios over the next few years.

The Solar Investment Thesis May Have Bottomed - Quiet Optimism Observed

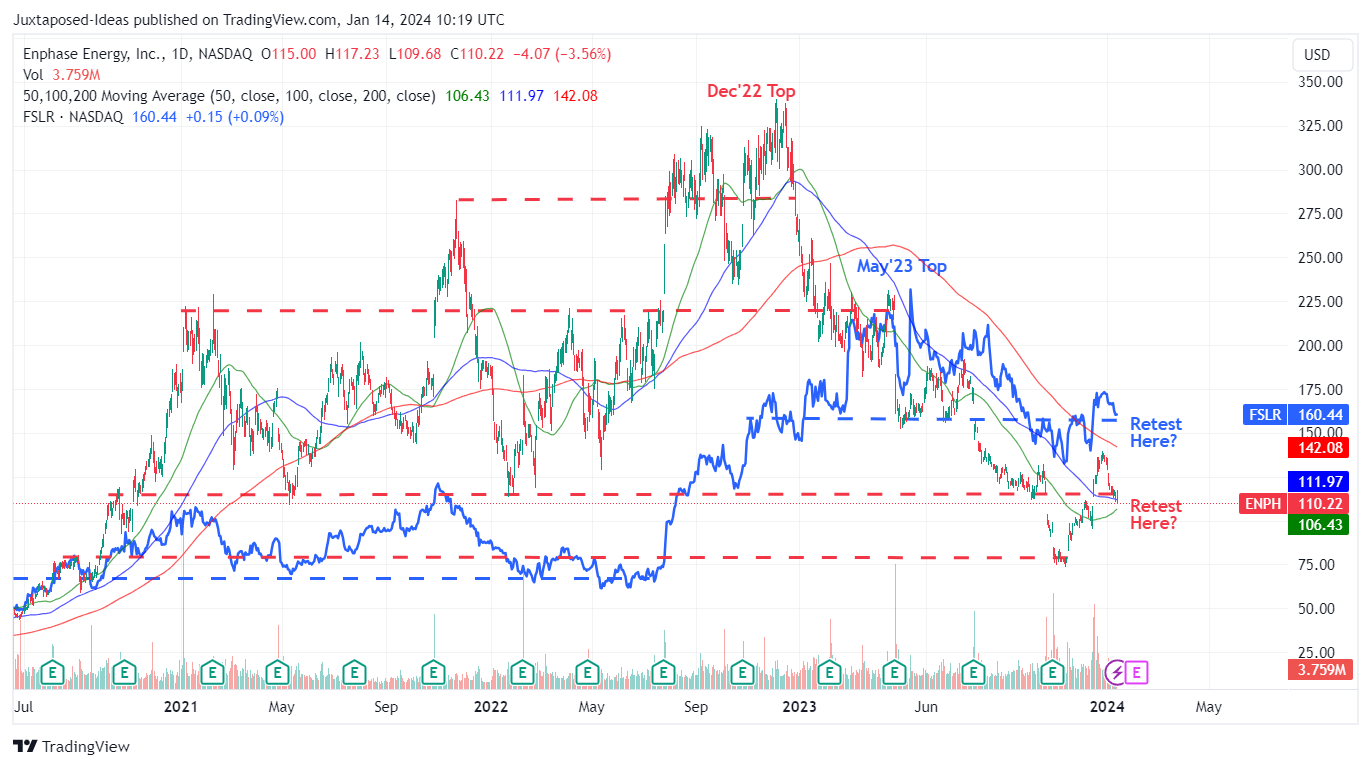

ENPH & FSLR 3Y Stock Price

{kind=link}

The electrification story has stalled after the 2021 and 2022 hyper-pandemic rally, with both ENPH and FSLR both plunging in 2023, with the latter somewhat spared from the elevated interest rate environment, attributed to its utility scale solar installation.

This is also why FSLR has reported exemplary FQ3'23 earnings call, with revenues of $801.09M ( -1.1% QoQ / +27.4% YoY ) and EPS of $2.50 (+57.2% QoQ/ +642% YoY).

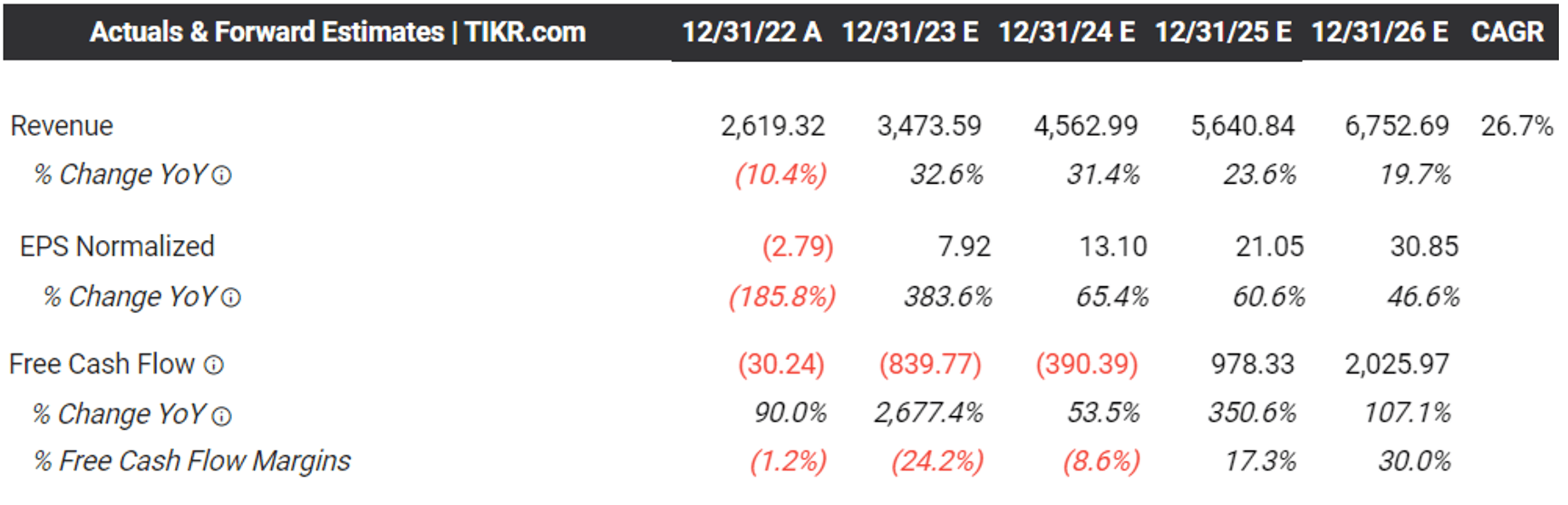

Much of this tailwind is attributed the growing booking backlog of 81.8 GW ( +5.1% QoQ / +87.1% YoY ) and booking opportunities of 65.9 GW (-15.8% QoQ/ -42.1% YoY) by the latest quarter, with the backlog extending through 2030.

Most importantly, FSLR's new net bookings come with a stable base ASP of 30 cents in the latest quarter (inline QoQ/ -5% YoY), with approximately 70% provided with upward price adjusters, naturally explaining the consensus optimistic estimates.

FSLR's Consensus Forward Estimates

{kind=link}

It is unsurprising then, that the consensus estimates are very optimistic about FSLR's long-term prospects, with its top-line growth projections raised to a CAGR of +26.7% through FY2026. This is compared to the previous estimates of +24% and its historical growth at -2% between FY2016 and FY2022.

While its FQ3'23 Free Cash Flow profitability of -$120.78M is still impacted by the intensified capex in India and Louisiana/ Alabama/ Ohio in US, we are not overly concerned, since these are expected to boost its global annual capacity to 24.7W by 2026, up from the 9.8 GW reported in 2022 .

With FSLR's investments eventually being top and bottom line accretive, further aided by the IRA credits and relatively healthy balance sheet at a net cash of $1.35B (-6.2% QoQ/ -19.1% YoY) by the latest quarter, we believe that its long-term prospects remain excellent.

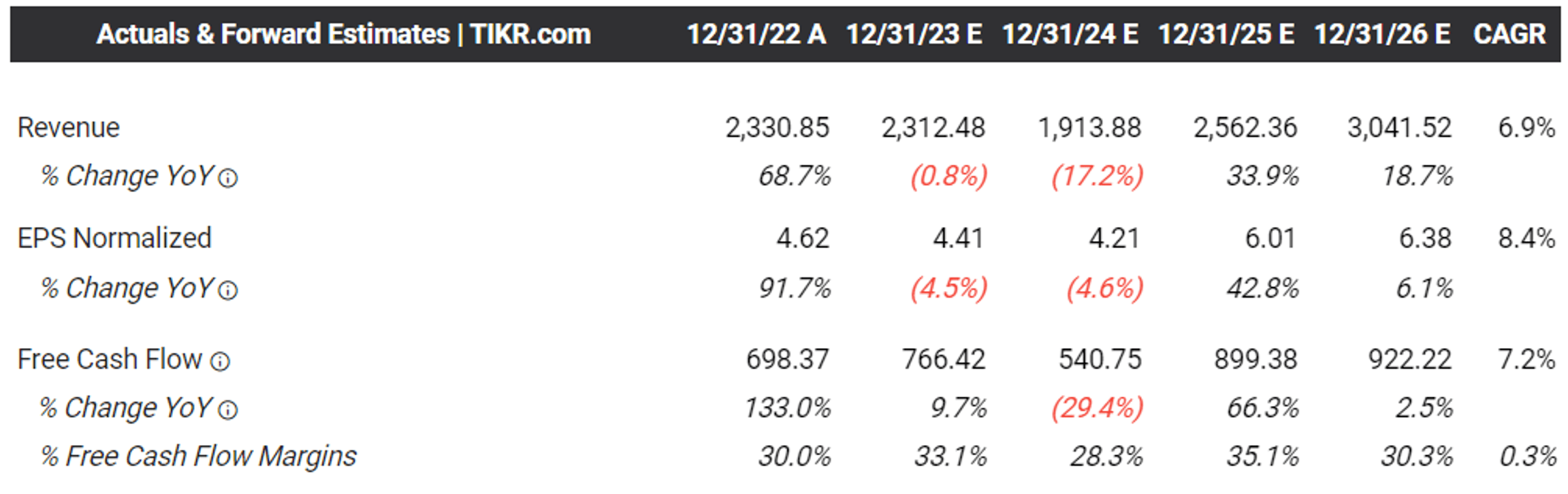

On the other hand, ENPH has been impacted by the NEM 3.0 transition in the top US solar states and the elevated interest rate environment, as the payback period lengthens and borrowing costs rise for residential installations.

This has resulted in its impacted FQ3'23 revenues of $551.08M ( -22.5% QoQ / -13.2% YoY ) and EPS of $0.80 (-26.6% QoQ/ +0.7% YoY), with the management also offering an underwhelming FQ4'23 midpoint revenue guidance of $325M (-41% QoQ/ -55.1% YoY).

The few silver lining to ENPH's execution is its improving gross margins of 47.5% (+2 points QoQ/ +5.3 YoY), implying the management's determination to maintain its premium ASPs and profitability, despite the elevated inventory levels of $174.11M (+4.8% QoQ/ +18.8% YoY).

This is compared to FY2019 levels of 35.4% (+5.5 points YoY) and $32.06M (+97% YoY), respectively.

In addition, ENPH's asset light strategy must not be discounted, since the company only expects approximately $17M in restructuring and asset impairment charges despite ceasing its contract manufacturing operations at two locations.

ENPH's Consensus Forward Estimates

{kind=link}

Then again, readers must note that the combination of the consistently lowered management guidance and decelerating residential installations have contributed to ENPH's underwhelming consensus forward estimates, with it expected to generate a top/ bottom line growth at a CAGR of +6.9% and +8.4%.

This is compared to the previous estimates of +20%/ +24.7% and its historical growth of +39%/ +28.2% between FY2016 and FY2022, respectively.

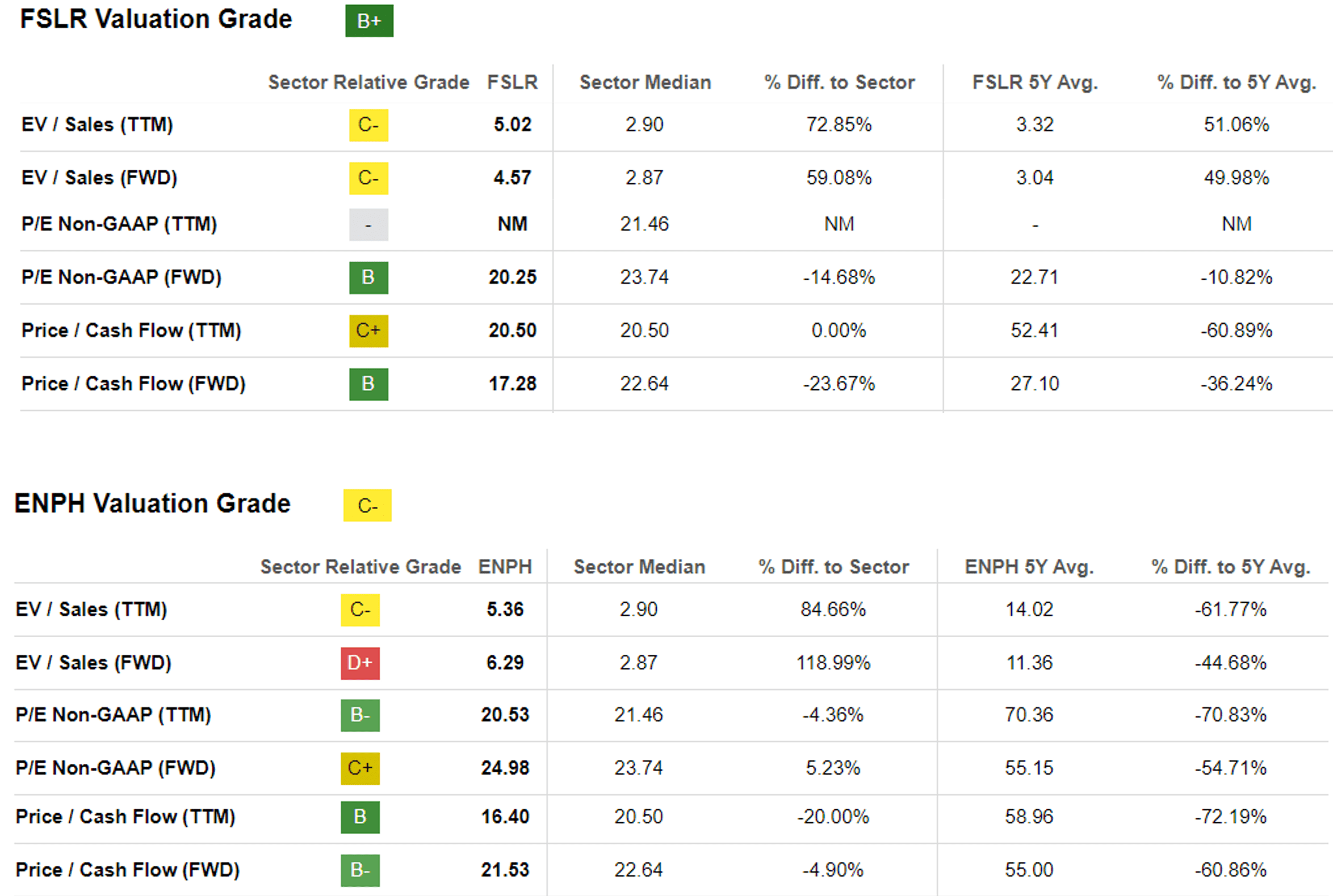

ENPH & FSLR Valuations

{kind=link}

And it is based on these reasons, we believe that FSLR's FWD P/E of 20.25x and FWD Price/ Cash Flow of 17.28x are not expensive after all, especially due to the inherently robust demand for solar installations at utility scale.

This is due to the promising consensus top-line estimates over the next few years, with its Free Cash Flow profitability likely to improve from FY2025 onwards once its capacity expansions and investments moderate.

At the same time, we believe that ENPH's FWD P/E of 24.98x is not overly ambitious, when compared to the sector median of 23.74x, its 1Y mean of 31.43x, and its pre-pandemic mean of 27.80x, after successfully bouncing off the October 2023 bottom of 17.80x.

Much of our optimism is attributed to the temporal impact of the elevated interest rate environment, since the Fed is likely to pivot by Q1'24 with the consensus only expecting an impacted FY2024 performance.

Most importantly, we believe that residential solar installation is likely to lift from FY2025 onwards, as the impact from NEM 3.0 normalizes, with the US existing home sales already showing moderate MoM recovery in November 2023 and new homebuilding sales remaining robust.

With the US still determined to achieve the 2030 and 2050 decarbonization goals , the eventual rebound for solar investment thesis is only a matter of time.

So, Is ENPH & FSLR Stock A Buy , Sell, or Hold?

ENPH & FSLR 1Y Stock Price

{kind=link}

With both stocks already drastically down from their previous highs and successfully bouncing from the October 2023 bottom, it appears that the solar investment thesis has improved drastically, offering interested investors with a more viable entry point.

Then again, while we may be rerating both stock as Buys, interested investors may want to observe their stock near-term movements since both stocks have also returned part of their recent gains.

Assuming that both ENPH and FSLR are able to bounce off their recent support levels of $110s and $155s, we believe that those levels offer rather attractive upside potentials of +36.4% and +165.6% to their long-term price target of $150.10 and $426.20, respectively.

This is based on ENPH's FY2025 consensus adj EPS estimates of $6.01/ FWD P/E valuations of 24.98x and FSLR's FY2025 adj EPS estimates of $21.05/ FWD P/E of 20.25x.

Anyone concerned about the temporal slowdown in EV adoption, must also be aware that the lithium spot prices have continued to decline, with the EV market growth expected to grow to $906.7B by 2028 and Goldman Sachs already projecting price parity to ICE vehicles by mid 2026.

This means that energy storage costs are likely to moderate as well, further triggering tailwinds in the residential and utility solar transition over the next few years, as borrowing costs normalize.

Therefore, while we may have missed ENPH's recent October 2023 bottom, we are not overly concerned, since we are glad that bullish support has finally materialized with its long-term prospects still bright.

For further details see:

Enphase Vs. First Solar: The Solar Investment Thesis May Have Bottomed