WMB - Enterprise Products Partners: Get Paid To Future-Proof Your Portfolio

2023-10-24 09:10:00 ET

Summary

- Enterprise Products Partners is a top-quality player in the energy midstream industry with irreplaceable assets that will be essential for a very long time.

- EPD has a low leverage ratio and an A- credit rating, which saves it millions in annual interest costs compared to lower rated peers.

- EPD has outperformed the market and continues to achieve records in pipeline volumes, and it has excess cash flow for potential bolt-on acquisitions.

There are plenty of high-yielding bargains on the market today, but it pays to choosy, as high interest rates remain a headwind for many overleveraged players that relied on a ZIRP (zero interest rate policy) to fuel their growth.

That’s why conservative income investors may want to stick with quality players that have irreplaceable assets and carry strong balance sheets. Such I find the case to be with Enterprise Products Partners ( EPD ), which I last covered here back in November of last year with a ‘Buy’ rating, noting its very strong demand in end markets and high distribution coverage ratio.

In this article, I revisit the stock and discuss why it remains a ‘Buy’ at present prices, so let’s get started! (EPD issues a Schedule K-1)

Why EPD?

Enterprise Products Partners is well known for being a juggernaut in the energy midstream base, with assets that transport, process, and export natural gas across the U.S. This enables EPD to capture profits along the full hydrocarbon value chain. It also carries irreplaceable assets along the Houston Ship Channel for LNG export as well as storage facilities at its Mont Belvieu site, which serves as a trading hub for NGLs.

In a ‘higher for longer’ interest rate environment, you would want to own moat-worthy companies with steady and recurring income streams and strong balance sheets, as in the case for EPD. This is reflected by EPD’s industry-leading leverage ratio with net debt to EBITDA of 3.0x, sitting far below the 4.5x generally considered to be safe by ratings agencies

This has earned EPD an A- credit rating from S&P. Considering EPD’s current $27.4 billion long-term debt balance, EPD’s strong credit rating could save it anywhere from $274 to $411 million in annual interest costs over the course of refinancing its entire debt compared to lower rated peers. This is based on a conservatively estimated 1 to 1.5% interest rate spread between A- rated bonds versus BBB- rated bonds. For reference, according to the Corporate Finance Institute, the current spread between AA+ rated U.S. Treasuries and BBB- rated bonds is 3%.

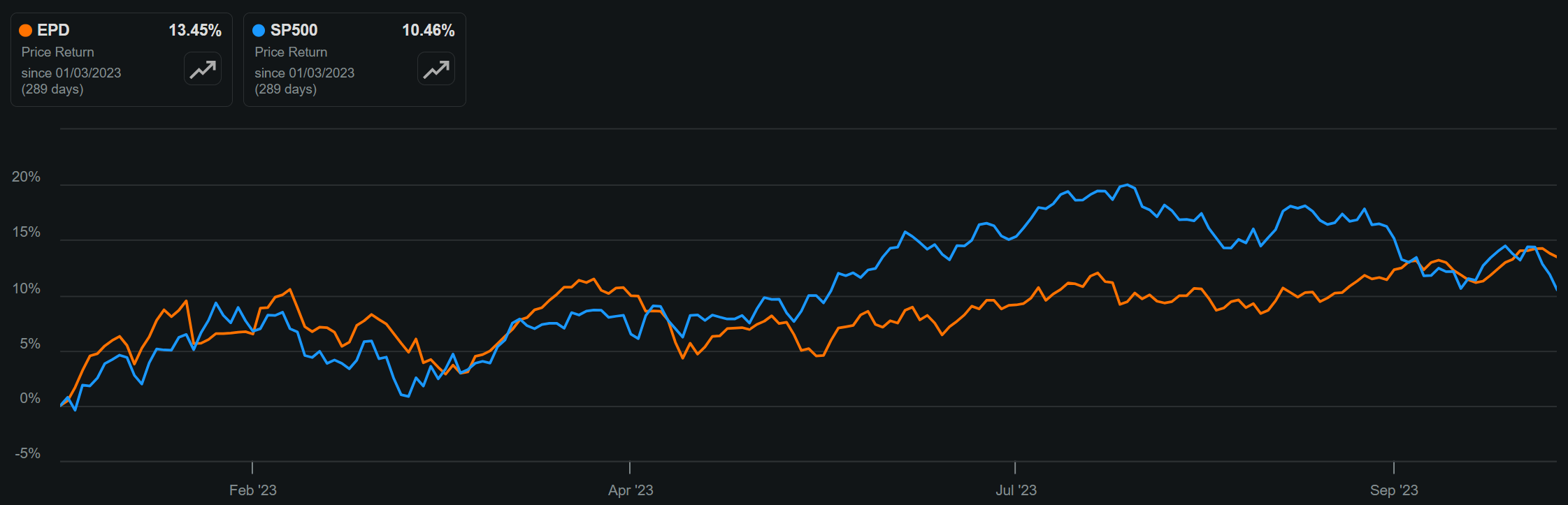

It appears that the market values this stability, as reflected by the 9.5% rise in EPD’s unit price since my last piece in November (16% total return thanks to distributions), surpassing the 6.2% rise the S&P 500 ( SPY ). As shown below, EPD has even outperformed the market since the start of the year, despite the tech-rally in the tech-heavy index during this timeframe.

{kind=link}

EPD vs. SPY Price Return (Seeking Alpha)

Meanwhile, the durable and in-demand nature of EPD’s asset base continues to be evident, as reflected by six operational records achieved during the second quarter, including natural gas pipeline volumes, NGL fractionation volumes and 11.9 million barrels of oil equivalent of total pipeline volumes. While adjusted EBITDA did decline by around $200 million from the prior year period to $2.2 billion during Q2, that was due to weaker processing margins that is largely out of EPD’s control.

Nonetheless, EPD retains plenty of excess cash flow, with a DCF-to-distribution coverage ratio of 1.6x. Over the past 12 reported months, EPD has retained $3.3 billion in cash after paying the distribution. For reference, EPD purchased Navitas Midstream early last year for $3.25 billion . This means that EPD has the capacity to make additional bolt-on acquisition if it so chooses without being reliant on external financing.

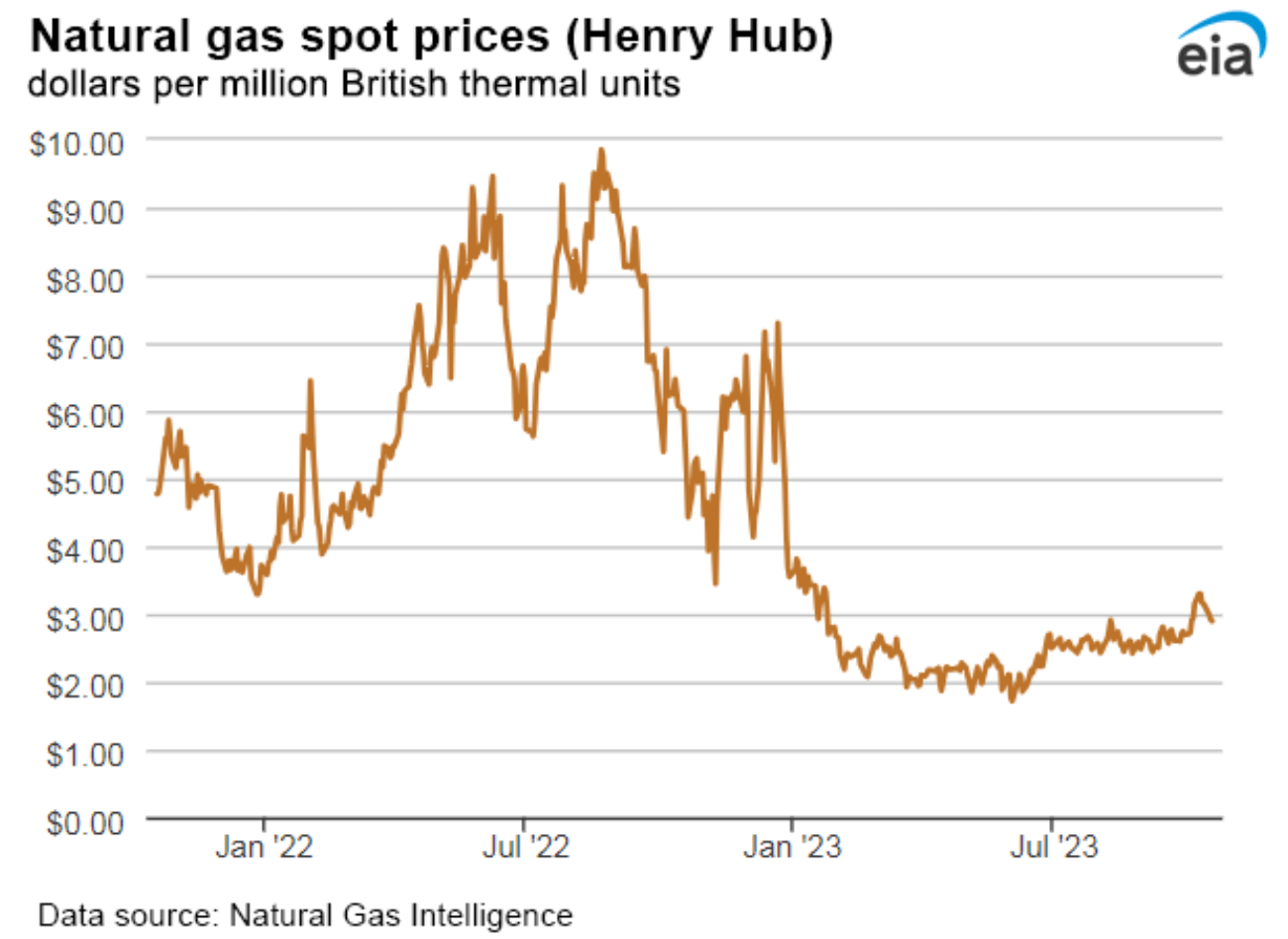

Looking ahead to Q3 results and beyond, I would expect for EPD’s adjusted EBITDA and margins to slightly improve, considering the uptick in natural gas price since the end of June to close to $3.00 per mBtu, as shown below.

{kind=link}

U.S. EIA

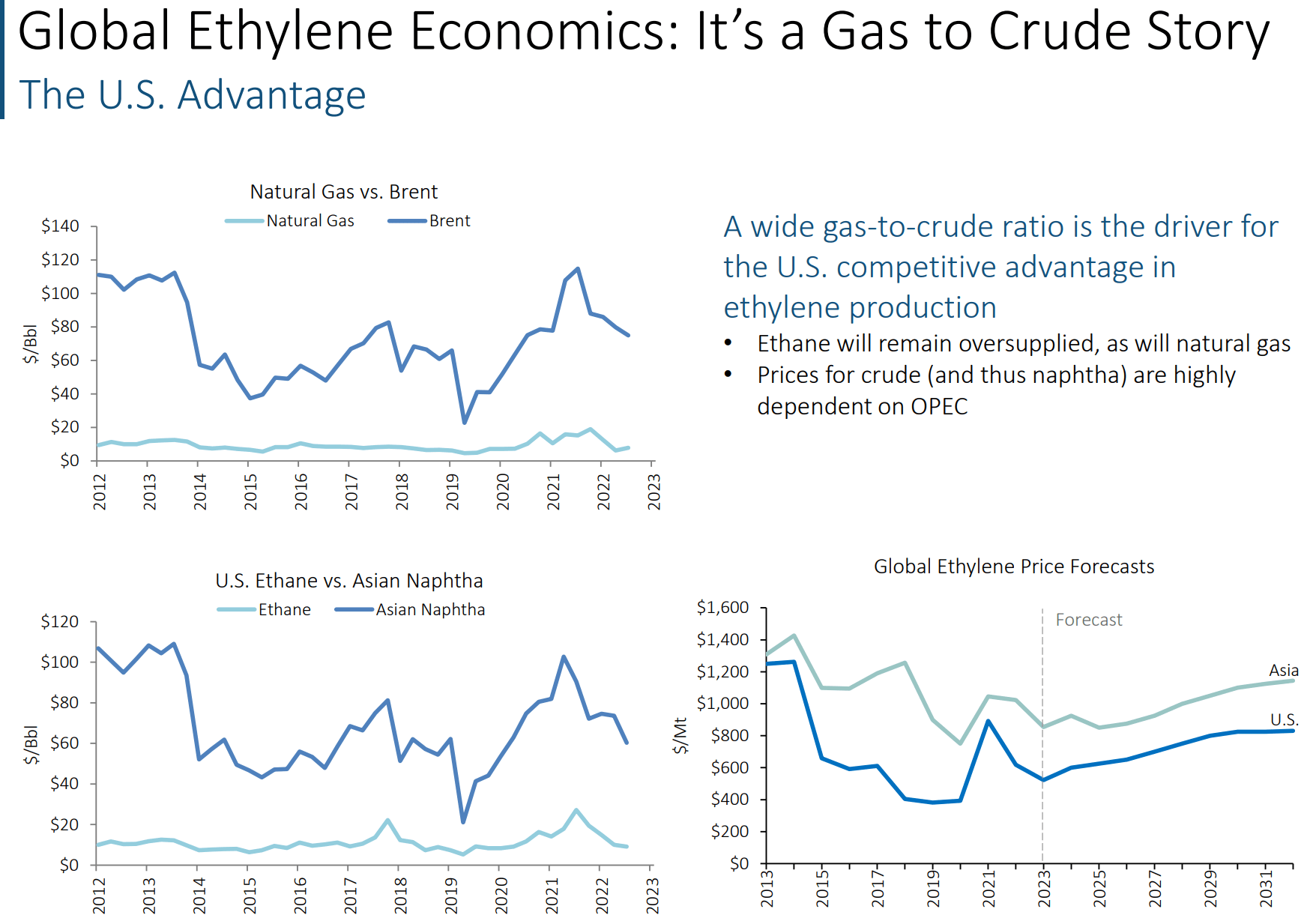

Looking out longer term, EPD should benefit from increased LNG exports considering the lower cost of extracting and processing gas compared to crude oil According to the U.S. EIA’s Annual Energy Outlook 2023, U.S. natural gas production and LNG exports are projected to increase by 15% and 152% , respectively, between the end of last year and 2050.

Moreover, gas prices are not driven by OPEC and are highly competitive compared to crude prices. This gives EPD competitive advantages in the world market due to having lower input costs in the production of ethylene, a highly sought after chemical feedstock that’s used for agriculture.

{kind=link}

Investor Presentation

Risks to EPD include an accelerated transition to renewable energy that goes beyond what the U.S. EIA is forecasting. Other risks include fluctuations in natural gas prices and price competition from new potential sources, which can compress EPD’s margins and profitability. Nonetheless, EPD’s strong balance sheet should enable it weather these types of headwinds, and supposed ‘safe’ renewable energy plays like NextEra Energy Partners ( NEP ) have taken a dive due to far weaker balance sheets.

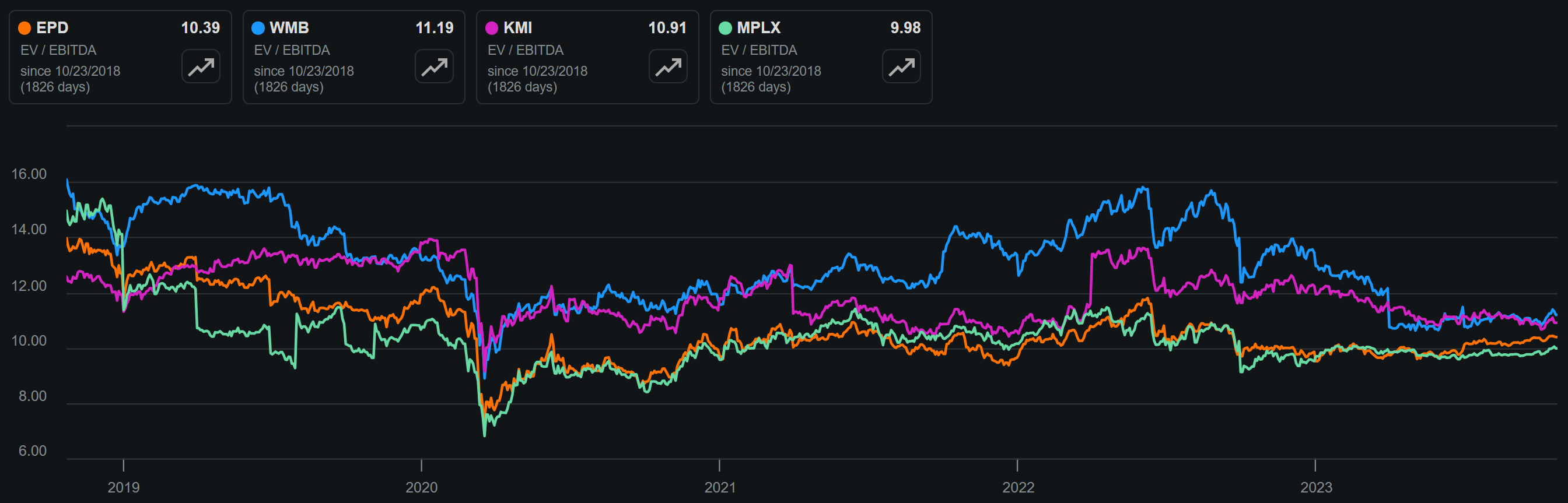

Turning to valuation, I continue to see EPD as being a solid choice at the current price of $27.52 as of writing with an EV/EBITDA of 10.4, which fits toward the low end of its 5-year range of 8-14x. As shown below, EPD also trades at a discount to peers Williams Companies ( WMB ) and Kinder Morgan ( KMI ) while sitting at a slight premium to MPLX ( MPLX ), despite having a stronger credit rating.

{kind=link}

EPD vs. Peers' EV/EBITDA (Seeking Alpha)

With a 7.3% distribution yield and ~5% annual distribution increases, which I believe EPD can sustain, investors can potentially achieve around a 12% annual long-term total return, which surpasses the 9-10% long-term annual return of the S&P 500. Considering all the above, I reiterate my ‘Buy’ rating on the stock.

Investor Takeaway

EPD continues to show why it is among the best choices to weather a 'higher for longer' interest rate environment with its strong balance sheet, stable and recurring income streams, and potential for growth as LNG exports increase. It also trades at a discount compared to its historical valuations and has demonstrated its ability to meaningfully raise its distribution due in part to its already built-out asset base and plenty of retained capital. These factors support the thesis that EPD serves as potentially great 'all weather' holding for what the future may bring.

For further details see:

Enterprise Products Partners: Get Paid To Future-Proof Your Portfolio