QCLN - Enviva: Wood You Buy The Bonds Offering 19% Yield To Maturity?

2023-05-09 15:11:41 ET

Summary

- We have stayed out of Enviva as we found their capital allocation model too dangerous.

- The recent cut was expected despite management assurances to the contrary.

- The bonds now yield 19% to maturity.

- Let's look at those as well.

According to its website, Enviva Inc. (EVA) is the world's largest producer of sustainable wood pellets. It owns and operates pellet producing plants and deep water marine terminals from Missouri to Virginia.

{kind=link}

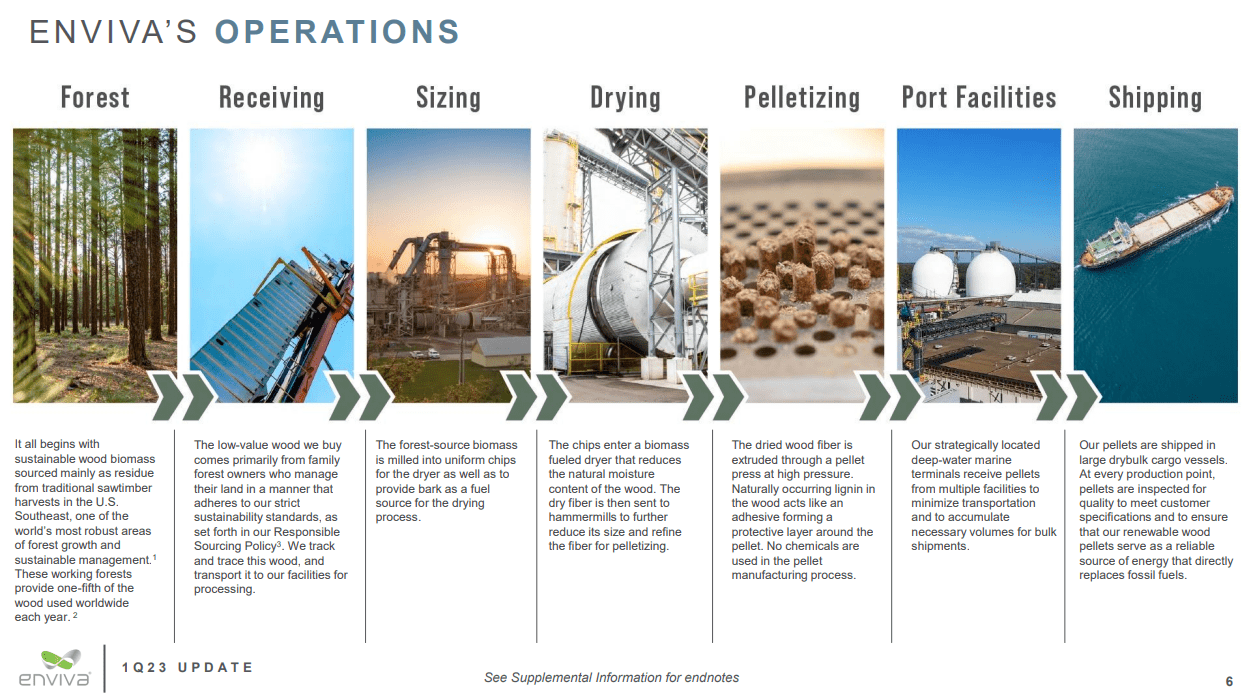

EVA calls this a renewable alternative to coal, designed to reduce emissions and reduce waste. This process though is long and complex and EVA breaks down the steps for you in its presentations.

{kind=link}

EVA was designed for the 2020-2021 timeframe. It would be hard to imagine a company better suited to capitalize on the trends that were in play back then. The company was in the clean energy space and offered a high yield at a time of low interest rates. Investors could not get enough. We will note here that the total return here was almost identical to the First Trust NASDAQ Clean Edge Green Energy Index Fund ( QCLN ), a fund we have panned a few times (see A Bubble By Any Other Name )

What Went Wrong?

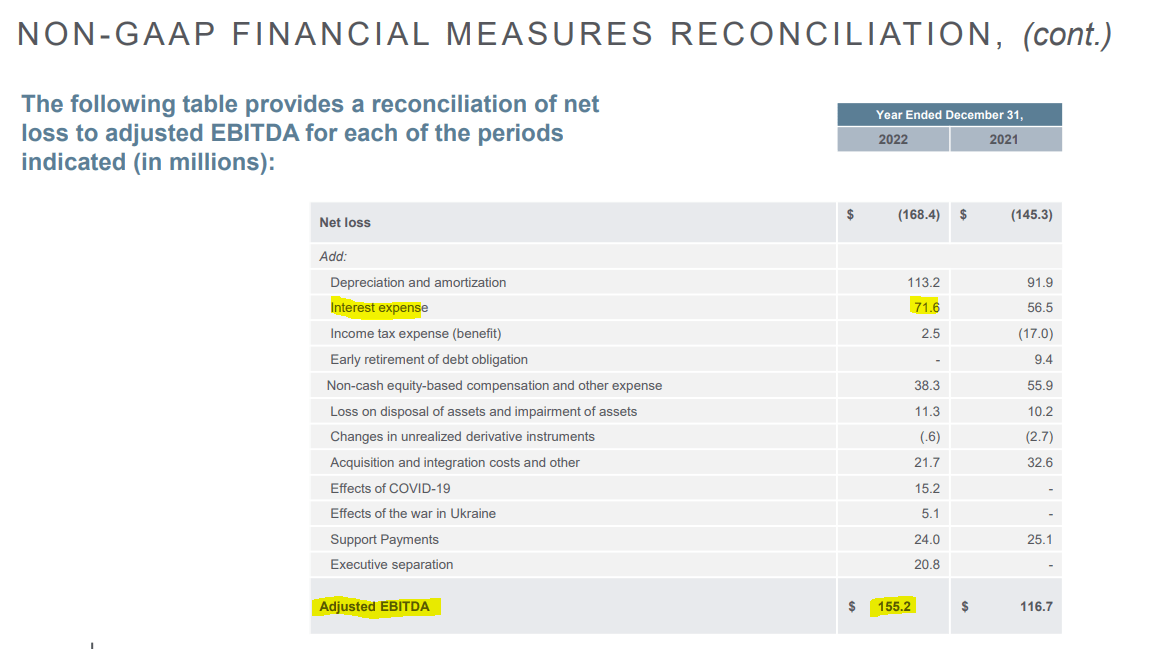

We did not follow this story very closely in 2020-2021. All we can say is that we looked at the high yield play a few times and did a hard pass. Our hard pass was based on the fact that we just could not understand how the company made an economic profit . We are not talking about the process of using wood pellets or the big European subsidies. We are referring to the adjustments made to the GAAP reported numbers. That's an area we examine all the time with MLPs, Canadian pipeline companies, oil and gas producers, and of course REITs. So walking from GAAP to something that represents real economic profit is our bread and butter. Yet, EVA's numbers just confounded us. For example, the company always reported big GAAP losses.

EVA 10-K

Then the adjusted gross margin calculation added almost the entire depreciation back.

EVA 10-K

Wood pellet plants are extremely capital intensive and have limited lives. Adding back this amount to calculate adjusted gross margin seemed really off to us. To top it off, the maintenance capex was a fraction of the total capex. Even if you bought into that adjustment, here was a company with an interest coverage of close to just 2.0X.

{kind=link}

The company paid $211 million in distributions (1.4X adjusted EBITDA) and spent $218 million (again about 1.4X adjusted EBITDA) in capex in 2022. Anyone can speculate on anything. But those numbers and (the numbers for every quarter before that) just should make your spine tingle with trepidation. You generally don't want any company with 2X interest coverage doing these kind of antics. If you couple that with consistent distribution increases and a quadrupling of share counts over two years, you know that you need to stay out. Ultimately the bubble did burst and if you got involved with EVA at almost any stage of the cycle, you are nursing big losses.

Outlook And Bonds

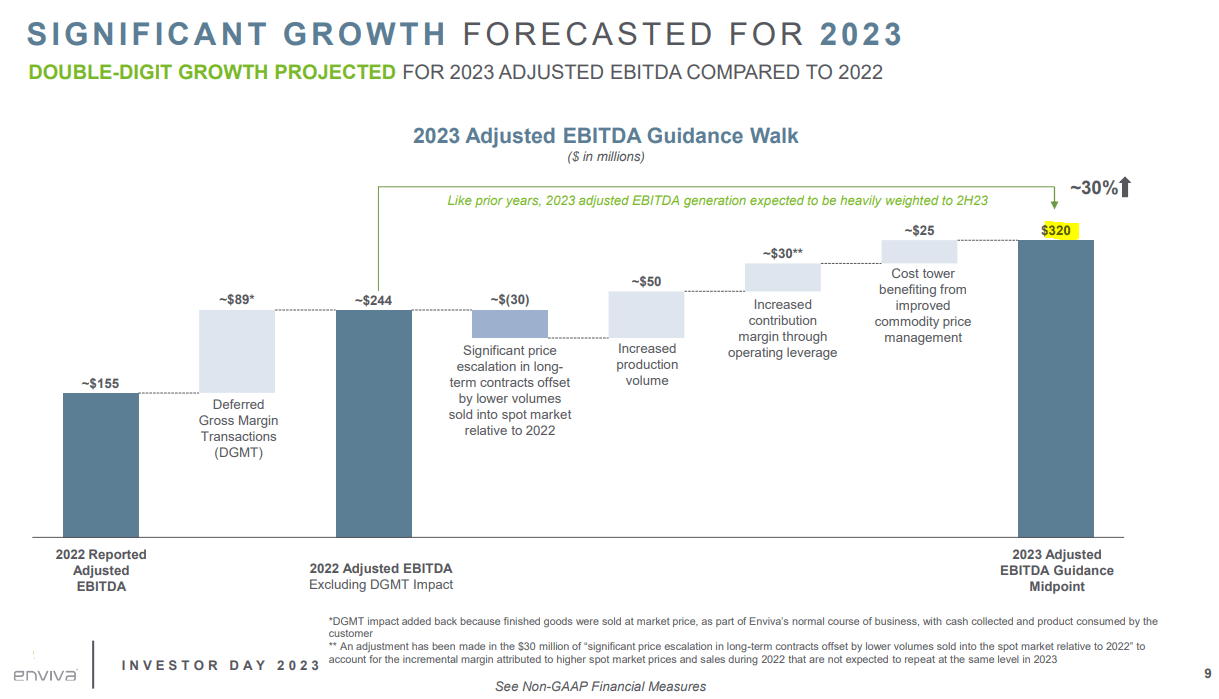

In early April, EVA guided for $320 million in adjusted EBITDA.

{kind=link}

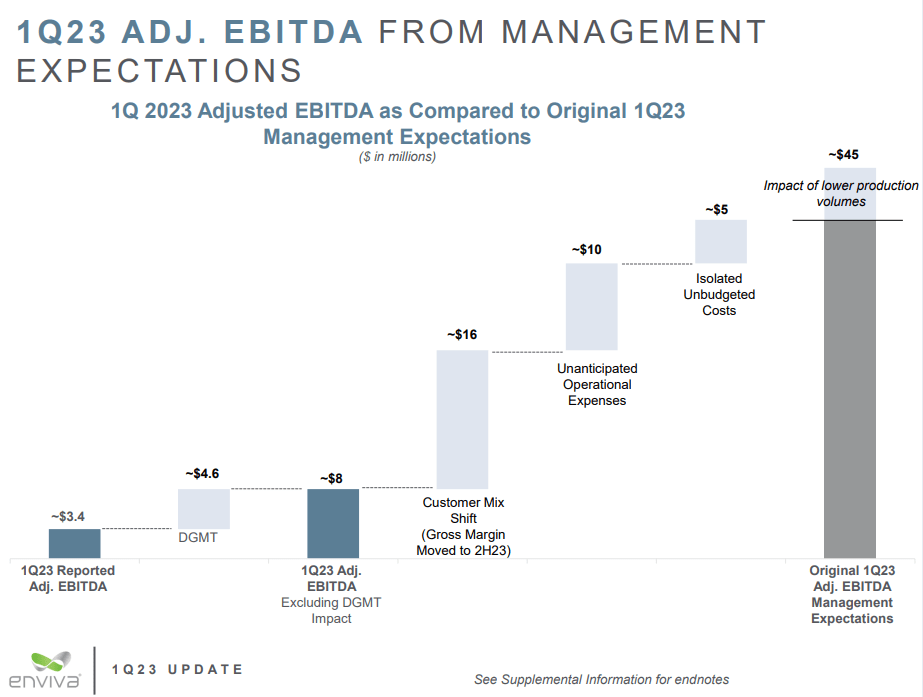

Adjusted EBITDA is a dance in most cases with a lot of subjective modifications. Nonetheless, if they could double the adjusted EBITDA there was hope. Q1-2023 was an incredible disaster though and the company managed only $3.4 million in adjusted EBITDA. EVA walked through what went wrong versus the original $45 million expected.

{kind=link}

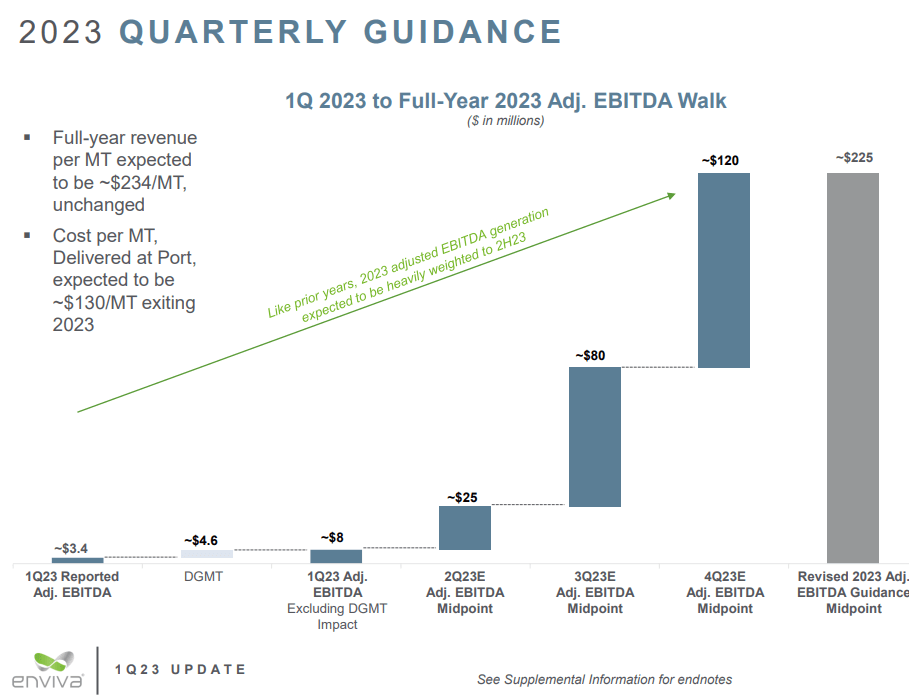

There was now a further cut to 2023 projections, settling in at $225 million.

{kind=link}

Management added some color on this in the conference call.

Approximately $30 million of the decrease between the previous guidance midpoint of $320 million and the revised midpoint of $225 million is related to the weakness in the first quarter of 2023. The remaining $65 million is related to shift in timing expectations as to when productivity and cost improvements are fully realized. To break down the revised guidance further, we are providing quarterly expectations for the next 3 quarters to improve transparency around our realistic expectations for the remainder of the year.

Source: Q1-2023 Conference Call Transcript

Our interpretation here is that even this seems incredibly optimistic. You can see above that the back half is supposed to do the extreme heavy lifting. Q4-2023 will apparently produce more adjusted EBITDA than the first three quarters combined. Even if you accept that possibility this is what you end up with.

{kind=link}

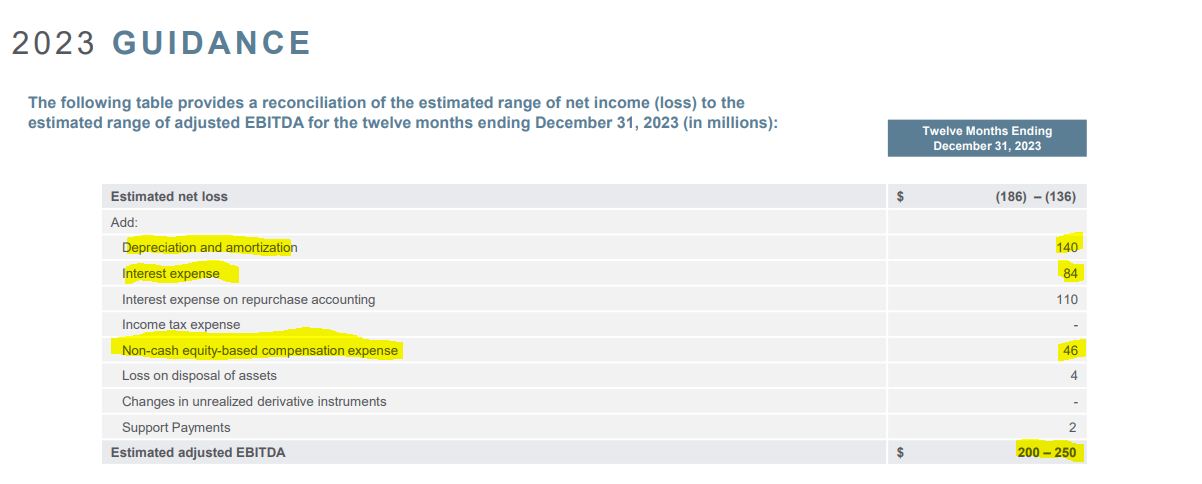

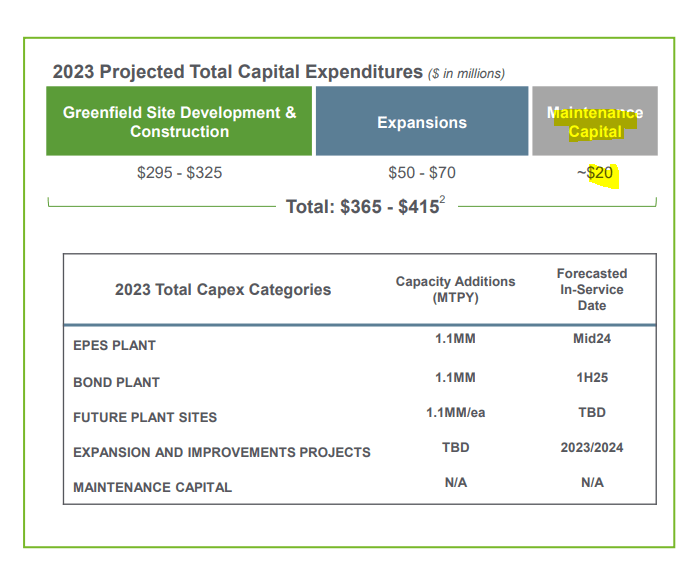

The interest coverage does improve from the 2022 baseline, but as before, we remain skeptical that the $140 million depreciation and amortization is not a true cost here. According to EVA the maintenance capex is $20 million. It will be spending close to $400 million in total this year.

{kind=link}

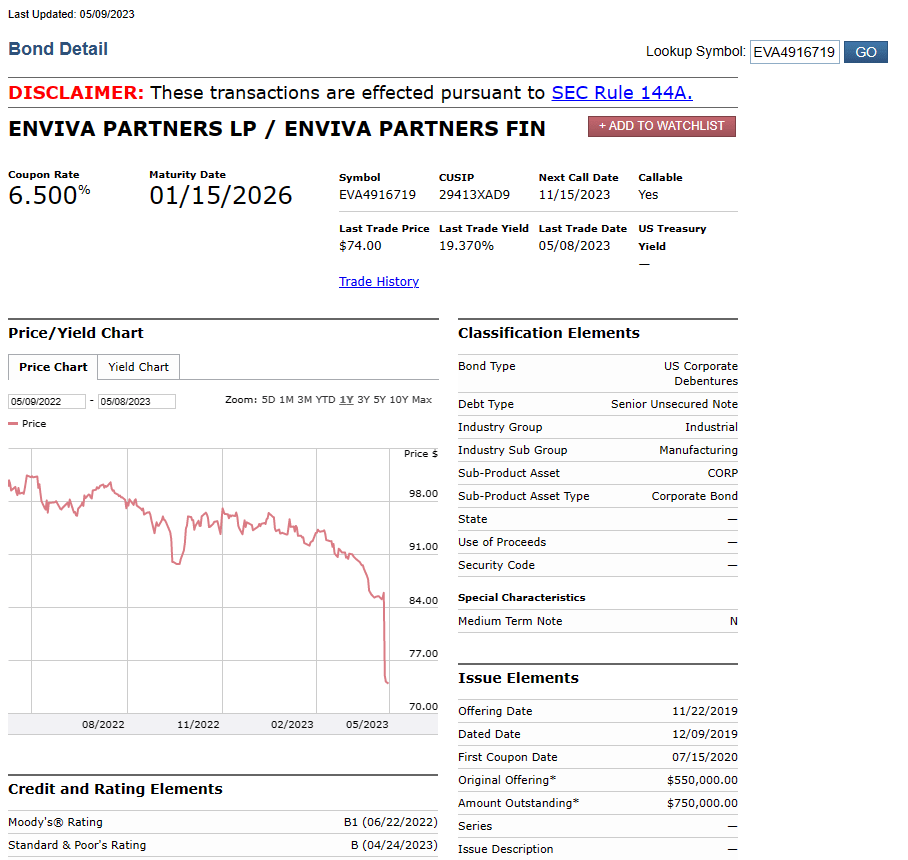

The company's long term debt is just shy of $1.4 billion and this will go up during the year. So using their numbers, you are looking at a debt to adjusted EBITDA of close to 7.0X. That will be a challenge for capital funding in the years ahead. The near term bonds are yielding 19.37% to maturity. They are SEC 144A but were tradeable on Interactive Brokers.

{kind=link}

What is quite interesting about those bonds is that they shrugged off the S&P Global downgrade on April 23.

S&P Global Ratings downgrades Foreign Currency LT credit rating of Enviva to "B+"; outlook stable. S&P Global Ratings downgraded from "BB-" to "B+" the Foreign Currency LT credit rating of Enviva on April 24, 2023. The outlook is stable.

Source: Cbonds

But the bonds tanked hard on release of the Q1-2023 results. That is quite the move and notable considering one very important fact. EVA eliminated the distribution with the Q1-2023 results. This should be very bond-friendly as $250 million of cash flow will now be retained over the next 12 months. And yet, the bonds sold off hard on that news. They seemed to have interpreted the poor Q1-2023 as a strong negative and insufficient to overcome the distribution elimination.

Verdict

We don't think the 19% yield to maturity compensates us for the risks. Hence we are not even buying the bonds. We said the same thing internally in our Marketplace Service, even before the Q1-2023 results . So this is not Monday morning quarterbacking.

{kind=link}

The company did a massive equity raise just before the distribution was eliminated.

On February 28, 2023, the Company and certain accredited investors (the "Investors"), entered into subscription agreements (the "Subscription Agreements") to sell shares of Series A Preferred Stock of the Company, par value $0.001 per share ("Preferred Shares") in a private placement (the "Private Placement"). The Private Placement priced at the official closing price of the New York Stock Exchange on March 1, 2023, which was $37.71 . On March 20, 2023, we closed the Private Placement and issued 6,605,671 Preferred Shares and received gross proceeds of $249.1 million.

Source: EVA 10-Q

These preferred shares will convert into common shares.

Each Preferred Share is convertible into one share of common stock of the Company, par value $0.001 per share, subject to adjustment for any stock dividends, splits, combinations, and similar events, and will automatically convert into common stock upon shareholder approval of the conversion by a majority of the votes cast, which is expected to be obtained on or before June 15, 2023.

Source: EVA 10-Q

So there are two ways to look at this. The first is that the cash raised does give the company some breathing room to complete its projects. The second is that you have one extremely angry set of accredited investors (down 75% in two months and distribution gone) and the equity market is closed off. To top that, here is what was said after the fourth quarter results.

Based on our capital allocation policy, we expect to maintain our 2023 dividend payout at the 2022 level, whereby we expect to pay $0.905 per quarter for an annual dividend of $3.62 per share. We definitely see the ability to increase the dividend over time and returning incremental value to shareholders is certainly top of mind for our management team.....

And let me just add. For 2023, when you look at our cash flow from operations, what we expect is that our normal course of business fulfilling our contracted backlog in 2023 will generate operating cash flow that will not only cover our dividend that we've guided to, but in fact, exceed that dividend. So that I think it's important to note what you should expect from us and what we have conviction around for.

Source: Q4-2022 Conference Call Transcript

Chalk this up to yet another one where management changed their tune within one quarter. We will monitor this and see if the company is able to turn around its operations and start showing improving real economic returns.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Enviva: Wood You Buy The Bonds Offering 19% Yield To Maturity?