DXC - EPAM Systems Stock Plunges On A Dour Forecast

2023-06-06 08:55:49 ET

Summary

- EPAM Systems' shares plummeted after the company revised its revenue and profit expectations for the year, indicating rapidly changing market conditions or management incompetence.

- EPAM Systems' mixed financial results and downward revision of guidance have left investors cautious and frustrated.

- Despite long-term potential, EPAM stock appears pricey on a forward basis, and the uncertainty in the present market conditions makes it a risky investment.

June 5th ended up being a very painful day for shareholders of EPAM Systems ( EPAM ). Even though the company reported earnings and guidance for the future exactly one month ago, the firm ended up releasing new guidance that revises lower expectations for revenue and profits for this year. This is never a good thing. At the end of the day, it signifies to investors one of three things. Either that market conditions are changing rapidly, that management is incompetent when it comes to having an understanding of what the near-term future will look like, or a combination of the two. When you add on top of this downward revision and the message that it sends investors, the fact that shares of the business are not exactly cheap even after taking a tumble, I believe that investors should be very cautious until more data is made available.

A look at EPAM Systems

Before we get into the meat and potatoes of the article, we should touch on exactly what EPAM Systems does. According to the management team at the company, the firm is a digital transformation services and project engineering business. This is a rather vague description of the firm that doesn't tell investors all that much. So we do need to dig a bit deeper. One of the areas that the company focuses on is engineering. Through this side of the business, management helps customers build enterprise technologies that aid in the improvement of business processes, that offer smarter analytics, and that provide a wide variety of other functions. One example that the company gives of the work that it performs is its work in helping Marathon Oil ( MRO ) build a next generation cloud native data platform for its business.

There are other activities that the company engages in. These center around improving and expanding customers’ operations and optimizing existing software by performing application testing, test management services, automation and consulting services, and more. The company's work even expands into the design arena, which makes a great deal of sense when you consider how impactful quality design is on how software ultimately looks and works. As you can imagine, the company can add value anywhere that technology exists. Its work has touched the financial services industry, the travel industry, media, life sciences and healthcare, real estate, energy, and more.

The company prides itself in establishing relationships that become long term. In 2022, for instance, 54.7% other revenue it generated came from clients that had been with the firm for at least five years. 26.4% of revenue came from clients that had been with the firm for at least 10 years. This is not to say that the company only wants to focus on servicing existing clients. In recent years, management has made it a priority to further diversify its operations. In 2020, for starters, 30.9% of its revenue came from its top ten largest customers. By 2022, this number had dropped to 23.8%.

A look at recent pain

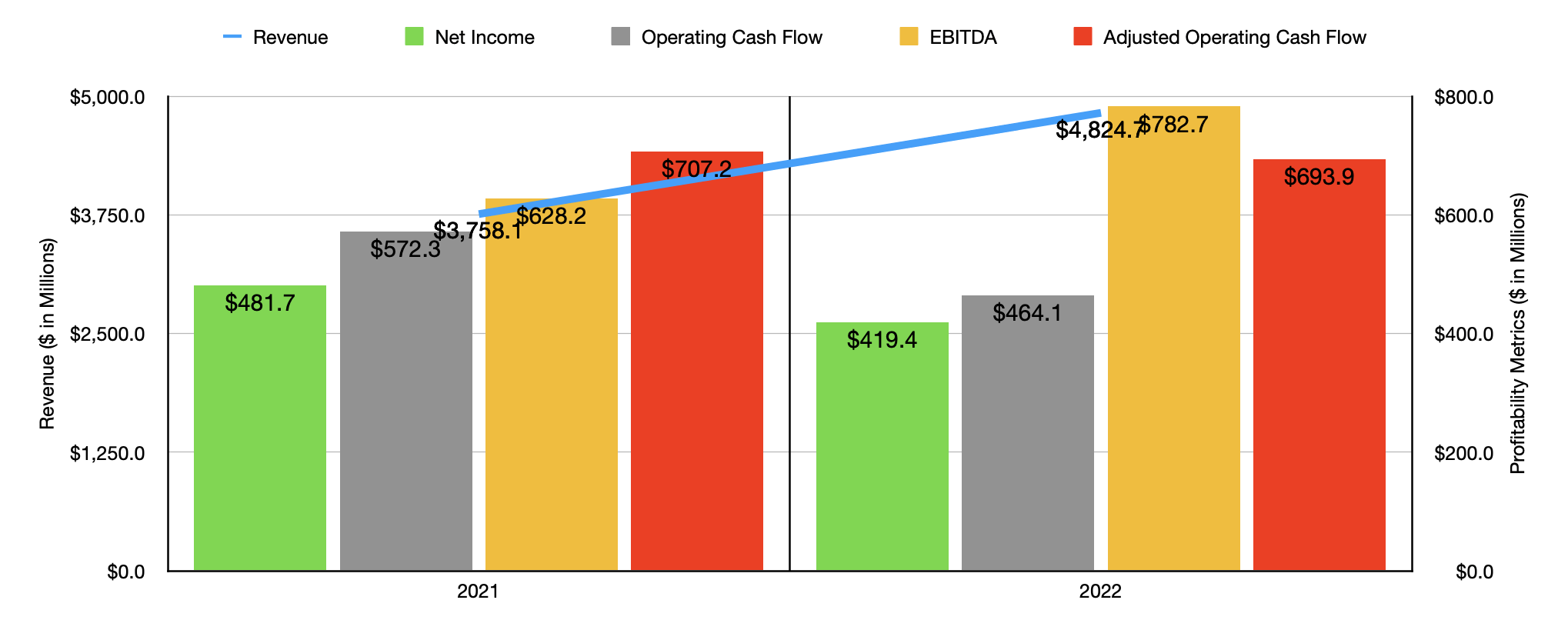

The overall financial trajectory of the company has been fairly positive, but certainly mixed. Consider how the business performed from 2021 to 2022 . In 2021, revenue came in at $3.76 billion. This number spiked to $4.83 billion in 2022. This increase, totaling 28.4%, came about even though the firm faced headwinds associated with foreign currency fluctuations totaling 4%, or $151.1 million. Acquisitions were responsible for 5.1% of the sales increase. But this was largely offset associated with the company's decision to exit Russia. The greatest revenue increase for the company came from the travel and consumer category, with revenue spiking 22.7% thanks to a return to normalcy following the COVID-19 pandemic.

{kind=link}

On the bottom line, however, the picture for the company has been pretty mixed. Net income went from $481.7 million in 2021 to $419.4 million in 2022. Operating cash flow dropped from $572.3 million to $464.1 million. Even if we adjust for changes in working capital, we would have seen the metric worsen, falling from $707.2 million to $693.9 million. The only profitability metric to show an improvement year over year was EBITDA. It ultimately grew from $628.2 million to $782.7 million.

{kind=link}

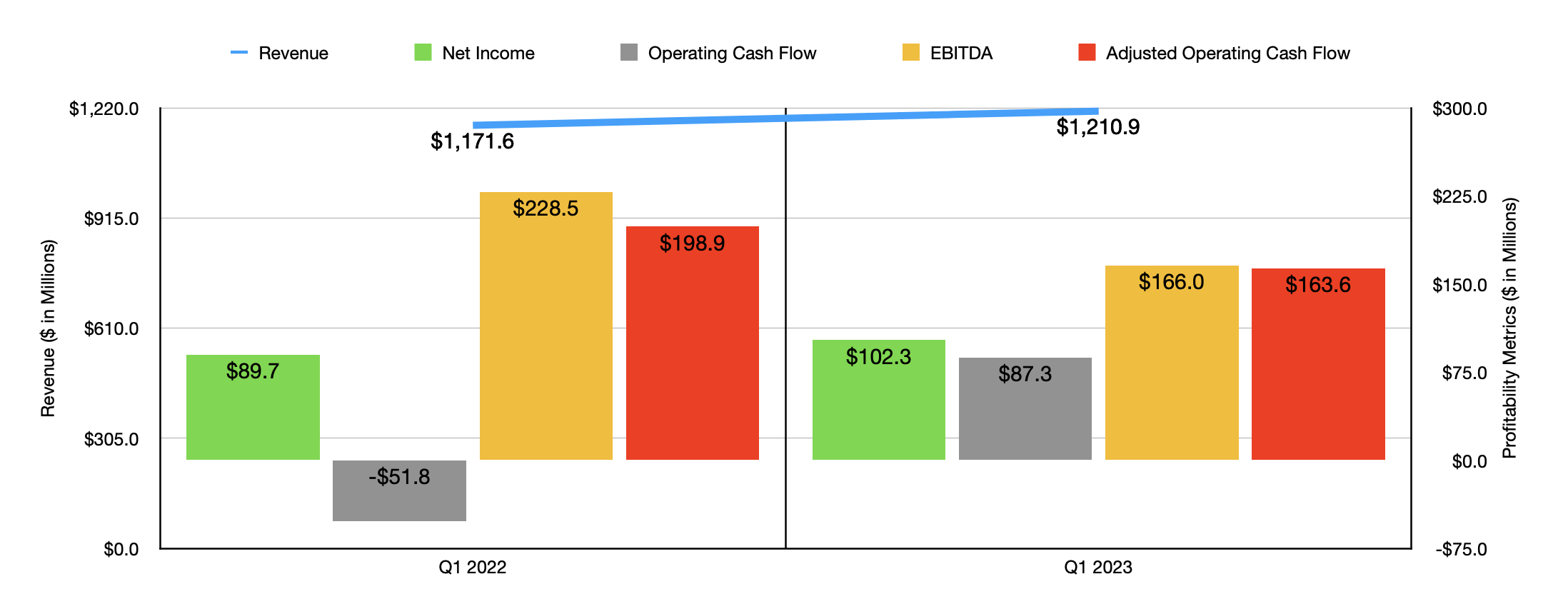

Similarly mixed results were experienced in the first quarter of 2023. Revenue of $1.21 billion came in 3.4% above the $1.17 billion the company generated one year earlier. In this case, net profits actually increased, rising from $89.7 million to $102.3 million. Operating cash flow saw a tremendous improvement from negative $51.8 million to $87.3 million. But if we adjust for changes in working capital, we would get that number falling from $198.9 million to $163.6 million, while EBITDA for the company fell from $228.5 million to $166 million.

Already, these mixed results left investors feeling rather frustrated. I say this because, the day that management reported financial results for the first quarter of the 2023 fiscal year, and the day after that, both combined, resulted in a 14.3% decline in the company's share price. However, this pain was short lived. By May 23rd, shares of the company had rebounded as much as 15.3%. The general consensus was that the long-term outlook for the company was still positive. Unfortunately, the market seems to have a different opinion now.

{kind=link}

{kind=link}

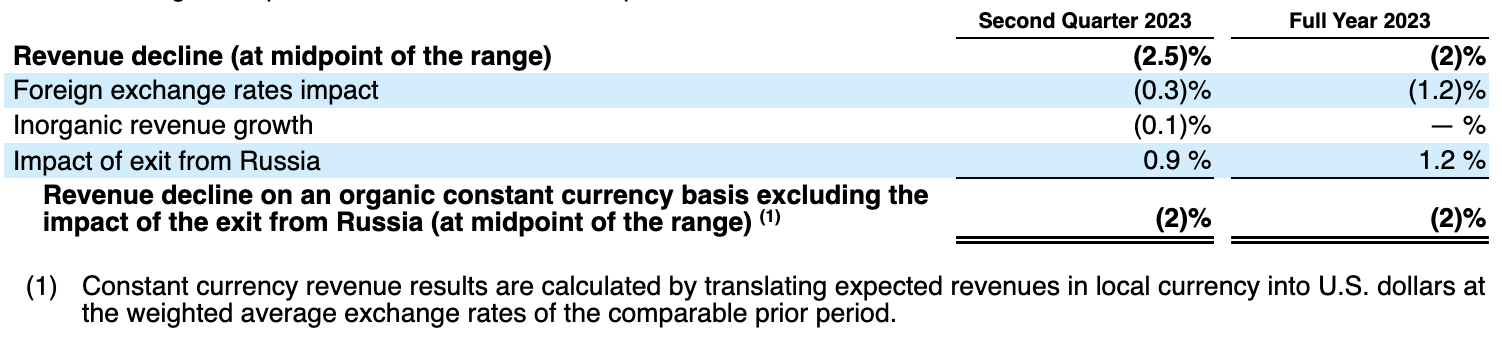

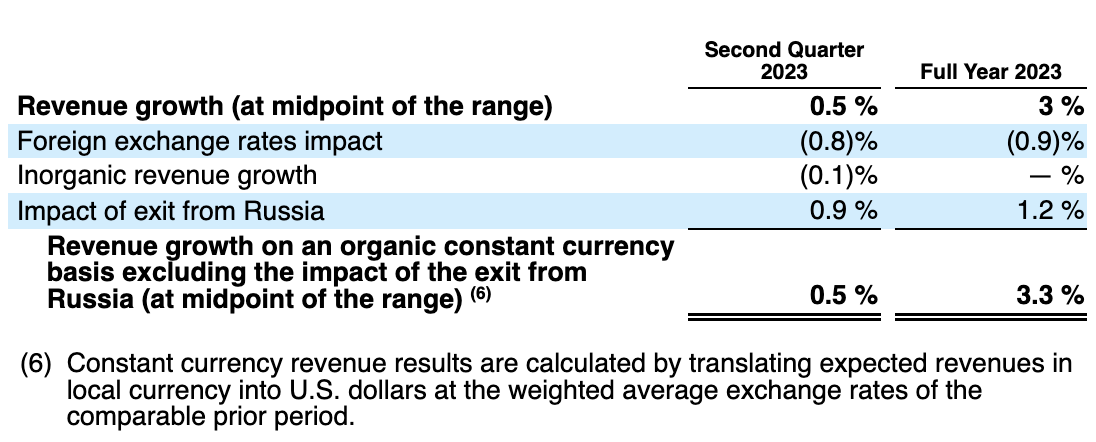

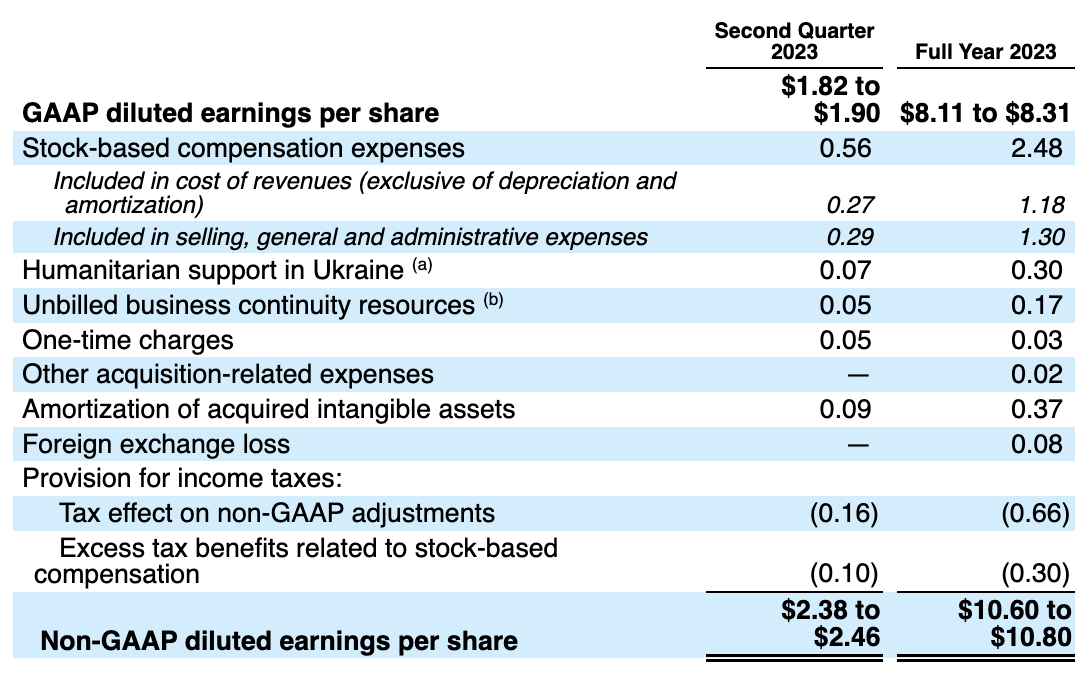

On June 5th, shares of the business plunged, closing down 21.7%. This seems to have been caused by a press release issued on the same day in which the company said that it is reducing its guidance for both the second quarter of the 2023 fiscal year and the 2023 fiscal year and its entirety. In the images above, you can see this revised guidance, while in the images below you can see the prior guidance. Overall for 2023, management is expecting revenue for the company to drop by 2%. Excluding both the exit from Russia and foreign currency fluctuations, the decline is also expected to be about 2%. This marks a significant downward revision from the 3% revenue growth and 3.3% adjusted organic growth that management expected when they announced financial results only one month ago. This all translates to between $4.65 billion and $4.80 billion of revenue for the year. That's down handily from the $4.95 billion to $5 billion previously expected.

{kind=link}

{kind=link}

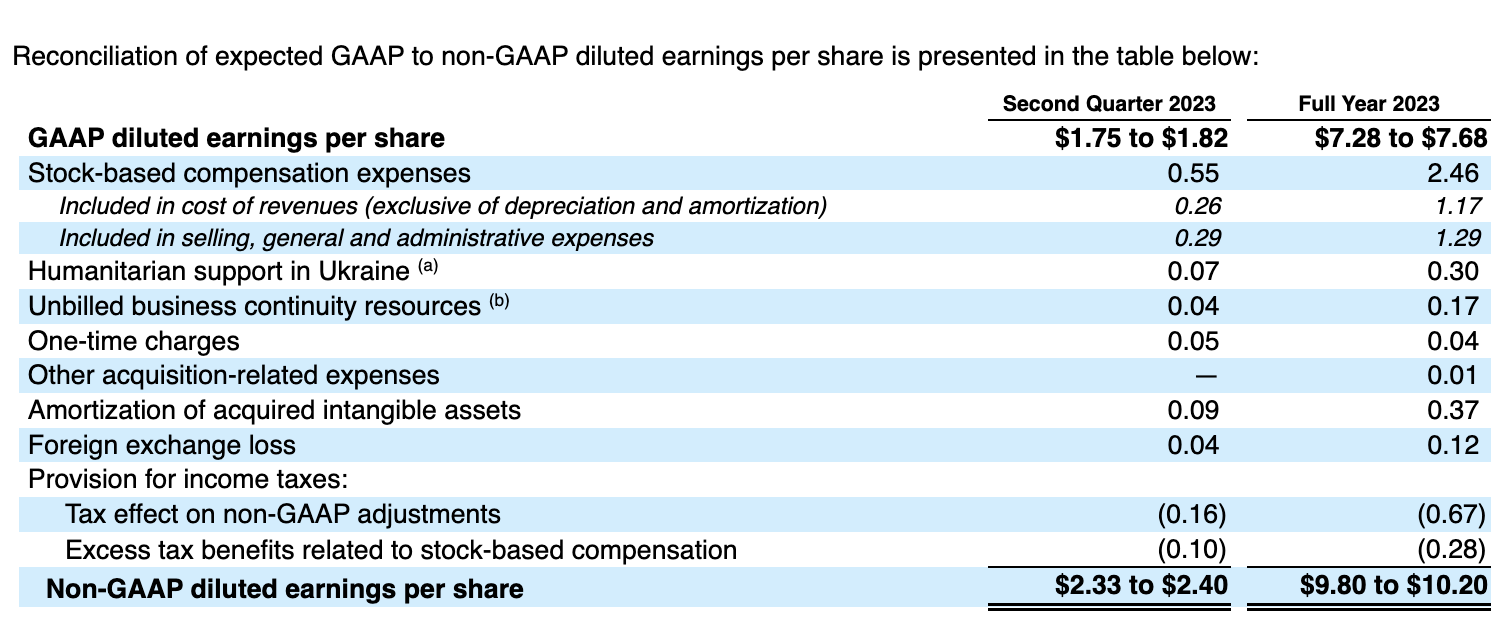

On the bottom line, we have also seen a revision lower. Earnings per share are currently forecasted to be between $7.28 and $7.68. At the midpoint, this should be about $7.48. By comparison, prior guidance called for earnings of between $8.11 and $8.31. Using midpoint figures, this is an 8.9% decline in guidance for the year. In its press release on the matter, management said that the revision was driven by the fact that its clients have become even more cautious with spending, particularly in the ‘build’ segment in the global IT services market. Overall pipeline conversions are occurring at slower rates than the company previously assumed and the overall size of the pipeline for work seems to be decreasing as well. There were some bright spots, such as a rising pace of new logo acquisition and the fact that customer retention and satisfaction rates remain high. So in the long run, according to management, the picture should still be positive. But uncertainty in the present is causing the near-term outlook to suffer.

I don't mind buying shares of companies when those shares plummet. In fact, I love doing it. But it only makes sense when shares of the businesses in question are fundamentally attractive. And that is not the case here. If we take management's guidance for earnings this year, profits should be $443.5 million. No guidance was given when it came to adjusted operating cash flow or EBITDA. But if we annualize those results so far, we would get readings of $570.7 million and $568.6 million, respectively.

{kind=link}

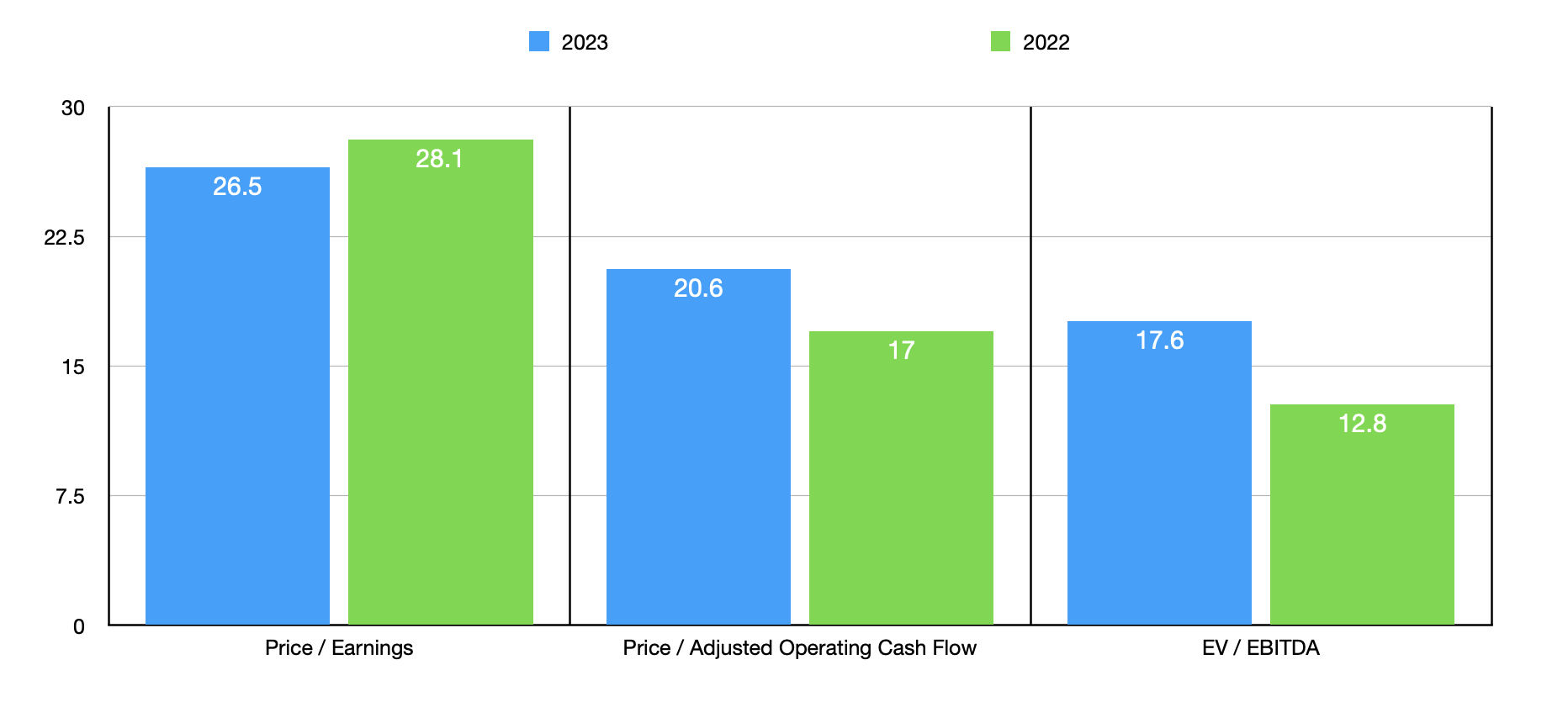

Taking these figures, I was able to easily value the firm. You can see the results on a forward basis and the results using data from 2022 In the chart above. While the price to earnings multiple for the company is dropping, the other two valuation metrics look worse. In the table below, meanwhile, I compared the company with five similar firms. When it comes to both the price to earnings approach and the EV to EBITDA approach, four of the five companies listed ended up being cheaper than EPAM Systems. And when it comes to the price to operating cash flow approach, our target ended up being the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| EPAM Systems |

| 26.5 |

| 20.6 |

| 17.6 |

| Amdocs ( DOX ) |

| 21.4 |

| 14.7 |

| 12.6 |

| Globant S.A. ( GLOB ) |

| 50.5 |

| N/A |

| 37.8 |

| CGI Inc. ( GIB ) |

| 21.7 |

| 16.7 |

| 13.2 |

| DXC Technology ( DXC ) |

| 8.5 |

| 4.1 |

| 9.8 |

| Wipro |

| 18.7 |

| 19.1 |

| 11.1 |

Takeaway

In the long run, I suspect that management is correct. EPAM Systems very likely will do you just find down the road. For those who are bullish on the company, I can understand the desire to buy. I won't attempt to dissuade you from this. But to me, the stock looks a bit pricey on a forward basis. When you add on top of this the message that this sends to investors that either management is incompetent or that market conditions are changing rapidly, I believe that the picture is just too volatile to make sense for me. If the condition of the company is changing so quickly that we have already had to see a downward revision, how bad could the picture be in another month? Due to these factors, I've decided to rate the company a ‘hold’ at this time.

For further details see:

EPAM Systems Stock Plunges On A Dour Forecast