EQC - Equity Commonwealth: REIT Trading At Negative EV Ready To Deploy Cash At Attractive Returns

2023-09-05 02:14:26 ET

Summary

- Office market is bearish with little signs of recovery, creating valuation mismatches and opportunities.

- Equity Commonwealth has sold down office assets and now has negative enterprise value, with plenty of cash to allocate at attractive valuations.

- EQC is sitting on a unique opportunity and if executed correctly it can deliver optimal value to shareholders for years to come.

The market has never been so bearish on the office market. Discounts to NAVs are at all-time highs across the publicly traded REITs, and there are little signs of a true comeback to pre-pandemic levels. We certainly do not want to go all-in on the opposite idea, but at the same time, a contrarian approach helps identify valuation mismatches and opportunities.

We believe that Equity Commonwealth ( EQC ) is one of these. In the midst of luck and skills, management correctly sold down the bulk of their office assets starting in 2017. Now the company sits on plenty of cash, resulting in negative enterprise value.

The setup: the market, the company, and the history

The Commercial Real Estate ((CRE)) market is not in its best shape as a series of (partially) correlated events are taking place: high rates, depressed occupancy rates (for offices), and concerns about demand/recession. This is depressing valuations - i.e. driving cap rates higher - and creating a hard time for many public REITs that are facing rising financing costs difficult to pass on to tenants.

We propose as an example this analysis by Capital Economics which forecast a very harsh scenario for the office market, with recoveries very slow to take off.

The office real estate crash will be so sharp and deep that Capital Economics thinks office values are unlikely to recover by 2040

The article goes on to forecast a very depressed recovery of occupancy rates, the main data point that all CRE investors are looking at now. The projected low and steady recovery won’t truly start before 2025, leaving a lot of room for losses as development and Capex costs are still here to be paid.

Office occupancy data (Various)

This data from different resources suggests that places like NY and San Francisco are the biggest losers from this chronic issue, with occupancy rates less than half the pre-pandemic levels. But why are we discussing office RE? Well, EQC had a huge portfolio of office properties located all across the US, with meaningful exposure to ((now)) risky markets like NYC. However, today the company has a totally different shape. In what we believe was a very skilled move (maybe with some luck involved in timing), management has been selling down the bulk of their office properties starting in 2017.

From an interview in 2019 , we quote the CEO:

We basically sold what we thought were the least desirable assets, and we’ve left the best assets,” he said. The current “higher-quality” portfolio is focused in Austin, Boston, Denver, Philadelphia, Washington, D.C., and Bellevue, Washington.

The focus has been on leaving out the assets that were not of the best quality, cashing in, and looking for more attractive returns in the future.

creating value through entrepreneurial leasing [and] creative asset management

Our take is that EQC, led by one of the most famed RE investors Sam Zell, understood very well that they were sitting on top of a sub-optimal portfolio while valuations were at all-time highs. This mix led to a restructuring of the entire company that went on for years, and EQC ended up selling its assets at very favorable cap rates compared to today's.

EQC Balance sheet development (Seeking Alpha)

This is what their balance sheet looked like over the last few years. The company has used some of the proceedings from the well-timed sales to pay off some $1 billion in debt over just 2 years. Now sitting on the liabilities side there is only common equity and some $120 million of preferreds. They are also been focused on returning cash to shareholders, for example with close to $500 million returned in 2022 with a dividend.

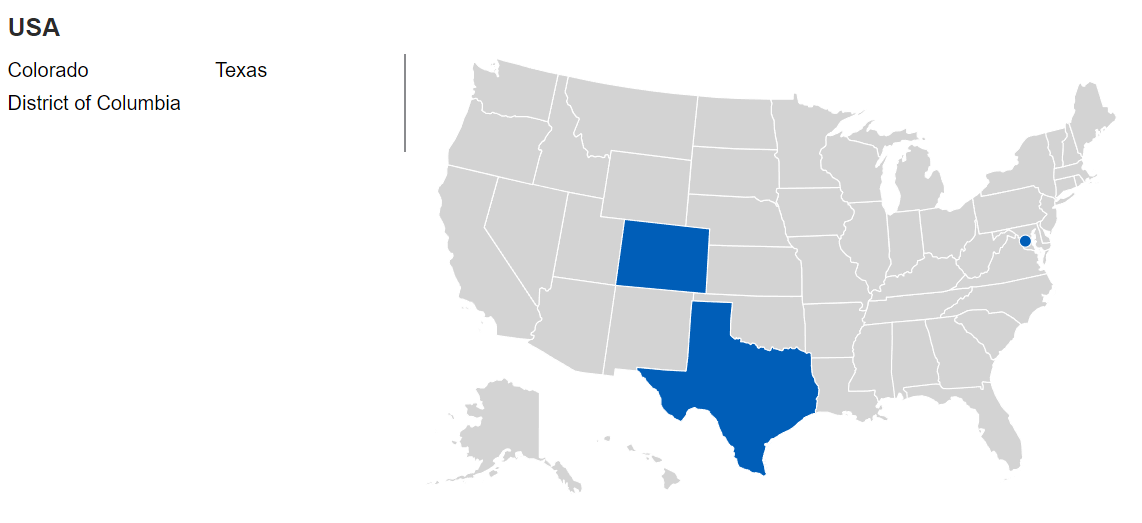

Today their geographical exposure and portfolio of properties look like this:

{kind=link}

Two properties in Texas, one is a state-of-the-art facility with diversified activities inside, including a fitness center leased separately from the office. And then they also retained one of their key assets, an office building in the center of DC.

An incredible capital structure to build up for future capital returns

The central part of our thesis is that EQC is in a unique position. With the market and its competitors burning with inflationary pressures, higher cost of debt, and contracting valuations, this is one of the most painful moments for RE after the GFC. Amid all this, this company is incredibly positioned with plenty of cash to execute deals while valuations are at some of the lowest levels in years. If management wants to keep the company alive and running, they will likely start to deploy some of this cash, and will likely be at attractive returns.

EQC Balance sheet (Latest 10-Q)

This is what the balance sheet looks like. They have $2.1 billion in cash and zero debt. $360 million in PP&E which are 8 buildings currently rented and generating $60 million in annual revenue. We think that there is significant room for upside considering that cap rates are not 2 to 3 times the levels seen when they were selling assets.

The equity side of the balance sheet has around $120 million of preferred shares. These securities cost a 6.5% yield to the company, yearly, which is very low if compared to funds rates being above 5%. This is another sign that the capital structure is set optimally to keep the liabilities side at pre-pandemic costs, while the assets side can grow at the current generous market valuations just by executing a deal.

Idiosyncratic and systemic risks need to be considered carefully

We started this article by highlighting the chronic nature of the issues that are affecting the CRE market, and in particular for offices in the US. We believe that an investment in EQC is affected by both idiosyncratic and systemic risks that may turn this investment much worse than forecasted.

On the systemic side, we have, of course, all the demand-related and rates-related problems. On top of depressed occupancy rates and leases coming to expirations without renewals, the bottom line is the valuations of transactions. This is driven by demand for CRE and inversely correlated with rates. If EQC was to enter a deal and the market conditions worsened or rates remained this high for a prolonged period of time, the outcome would be a depressed investment.

On the idiosyncratic side, we have execution. The path to bring back an entire portfolio of properties that is efficient and high-yielding is not easy, and management is somewhat unproven after the loss of EQC founder Sam Zell. We think that the wrong deal and the wrong debt/equity mix in the capital structure are mistakes not tolerated in the current market environment, as they could be lethal. However, we are confident given the strong cautiousness demonstrated by management over the years as they have been selling down the assets.

Overview of the fair value: Buy now to collect future yield

The main idea that we have for Equity Commonwealth is for management to look out for distressed opportunities that can be picked up for a cheap price. There is a hilarious case study for this. In 2021 EQC bid for Monmouth Real Estate Corporation, and lost to Industrial Logistics Properties Trust ( ILPT ), a REIT focused on industrial properties. After financing the deal with virtually all debt, the company has now burned $4 billion of equity as financing costs went up considerably. This is a hard lesson for timing in the RE market, and EQC can pick up these now-distressed assets for a much cheaper valuation than the one they would have paid in 2021.

To find a proper fair price for the company, we will use a non-conventional approach. As we do not have real assets to evaluate now, we will make assumptions on hypothetical deals that may come up in the next months. Then we compare the multiples to EQC peers and extract a possible range of valuations.

EQC - Valuation (Author's estimates)

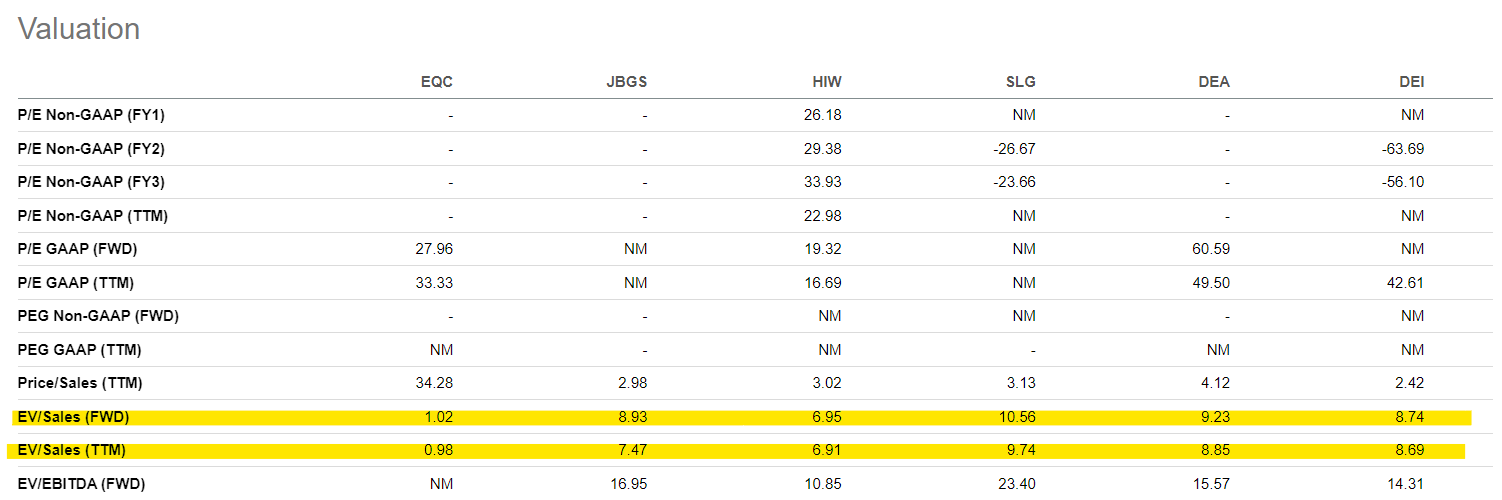

This is the valuation table. The main assumption is of course the EV/Sales multiple and the cap rate. We think that a 6% cap rate with FED funds rates above 5% is far more than reasonable, leaving a wide margin of safety. Then we went on estimating revenues by applying a standard 40% NOI margin. Then we used the multiples from the table below, the peers of EQC as provided by Seeking Alpha:

Peers Valuation (Seeking Alpha)

{kind=link}

We also know that the company may access leverage to pay itself dividends later when financing becomes cheaper. Last but not least, cap rates are usually inversely correlated with financing rates, this leaves room for multiple expansions in the upcoming years. All this gives us some conviction to assume that a $25 per share would be around fair value, with some room for expansion if the company is able to execute well.

Conclusion

Equity Commonwealth is one of the few REITs with office exposure that is de-risked. Their balance sheet is full of cash that we expect to be allocated at attractive returns in the next months. We expect the company to deliver strong returns for shareholders as we find a fair value per share no lower than $25.

For further details see:

Equity Commonwealth: REIT Trading At Negative EV Ready To Deploy Cash At Attractive Returns