SHOP - Etsy: Great Company Expensive Stock

2023-05-03 04:16:52 ET

Summary

- Etsy is a great company. It serves a needed market and has a nice moat against competition.

- The company saw explosive growth during COVID. It is retaining most of those customers.

- I like the company but the stock price is richly valued at current levels.

Etsy, Inc. ( ETSY ) is one of those companies that I have personally interacted with and liked and wondered about owning it as a stock. The company is a great company with a strong platform and user base. They fill a great niche in the online shopping world.

The company saw extreme growth during COVID and also saw its stock price grow rapidly in response. It is interesting to see where the company shakes out following the large increases from COVID. Will they be able to continue their growth or will they drop back to pre-pandemic revenue figures?

I like the company but the question today is whether or not I like the stock.

What To Like

I like the company Etsy. I like their website and what they offer to the marketplace. I think they fill a great niche in online shopping. The company has built itself into the go to marketplace for independent creators. The products they sell on their marketplace are very unique as well. These are for the most part small, individually run shops that are creating unique products. It is not something that is commoditized. This makes their business much harder to disrupt and replace. They have reached a scale point as well that provides them some real advantages. If you are an individual who wants to sell something that you make then Etsy is your go to place. They have an audience already made for you. You don’t have to invest a bunch of money and time to build out a website and pay for marketing. All you have to do is list your product, and of course do the part that you really want, make it.

Not only do they fill a market need but in my mind they do not have many big direct competitors. The competition is not that strong for Etsy’s unique and niche market. There is of course tons of competition for online shopping in general, but Etsy has its own niche in the market. You have all of your online ecommerce platforms such as Shopify ( SHOP ) and Wix ( WIX ). Yes these ecommerce platforms make it easy to get going but there is so much more that goes into a website rather than selling on Etsy. It is just so much more of a process to build out a website and sell products through it. Not to mention you then have to get traffic to your website, marketing. That opens a whole new skill set and cost for selling products. I actually run an online business and will tell you now it is not as easy as all the Shopify pitches make it out to be. Getting found online is not a cheap or easy process. Etsy does that for you on its platform. Unless someone is doing real scale then it does not make sense for them to create their own website. It also depends if they have a brand that can sell itself. Oftentimes the products on Etsy are not really a brand but rather a customized or unique product. You then have eBay ( EBAY ) which is really not into artisan or handmade type of products. Amazon Handmade is one marketplace that is looking to compete in this space. It's never good to count out a goliath like Amazon (AMZN) but I never even knew Amazon Handmade existed until I started researching Etsy and its market a bit more. I don’t see sellers ditching Etsy to join Amazon that has high costs and less of a community feel than Etsy.

While Etsy has a great niche that it sells through, which in my mind has limited direct competition. It has to be careful to not cross over into a direct competitor with other online marketplaces. The company operates in a space that is not in direct competition with many other online commerce platforms. As they continue to grow their business they need to be careful to stay within their niche. If they allow products that are not seen as “handmade” and start to dive into drop shipped types of products then they could find themselves diluting their value. They will then start competing with the likes of Amazon, eBay, etc. I don’t think that is where the company wants to find itself either.

COVID Boom

The company saw explosive growth during COVID. This was not uncommon for many online platforms.

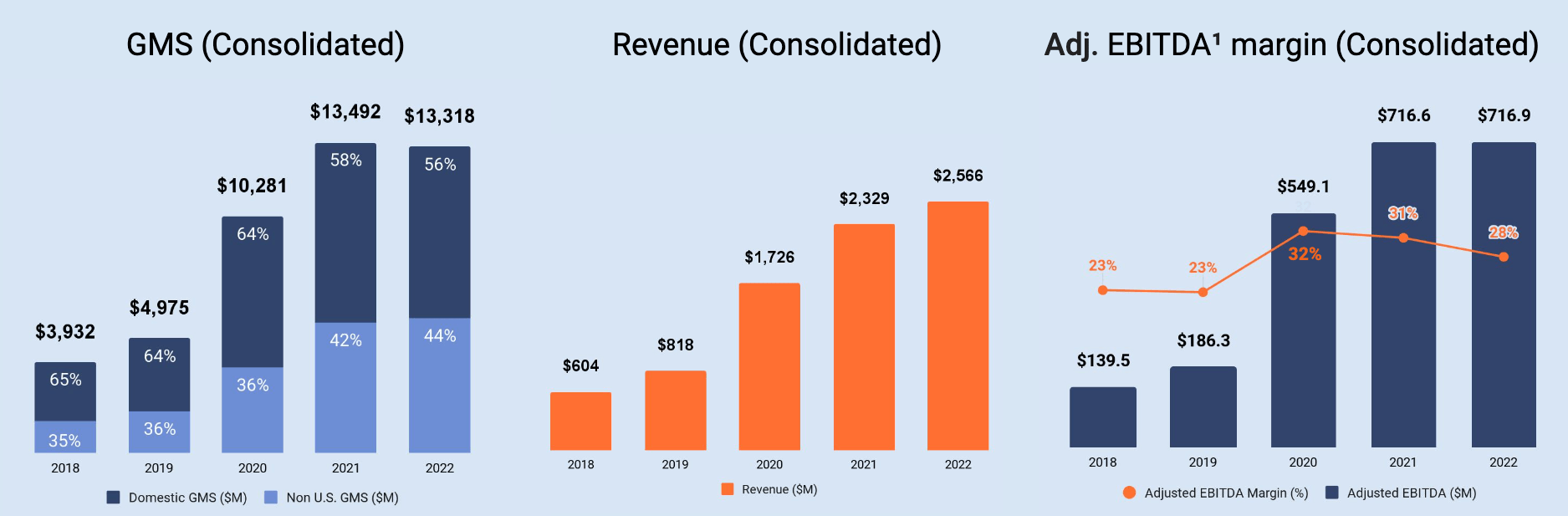

The company more than doubled gross merchandise sales ((GMS)) from 2019 to 2020, going from $4.7 billion in 2019 to $9.5 billion in 2020. It continued growth in 2021 as well, increasing GMS another 28% to reach $12.2 billion. The chart below from their presentation shows that explosive growth.

Company Presentation

The company's stock price did not get left behind during this growth either. ETSY stock opened at $46.23 in January of 2019, two years later in December 2021 the stock price closed the year at $222.01. That is a 380% increase over two years. It also had a drop off to end the year in 2021, as it peaked at a price over $294 a share in November of 2021. That means the stock saw an increase of more than 500% at its peak in 2021. The company was booming but the stock was booming even faster. The ride up came crashing down at the end of 2021 and into the start of 2022. The stock kept its fall starting in November of 2021 to hit a low of $67.01 in June of 2022.

For a variety of reasons, COVID pulled much of the online sales forward. It sped up the adoption for many to shop online. The key part is keeping those customers on once the pandemic has ended.

Going Forward

The company is now much larger than it was before the pandemic. Many customers were introduced to Etsy during the pandemic and now the company has a much larger user base and overall platform than before. It has been able to maintain many of those customers and keep much of that growth they experienced intact. That being said the company is now seeing a flat to negative growth. The chart in the section above shows that the GMS actually decreased slightly from 2021 through 2022. It fell from $12.2 billion to $11.8 billion, a negative growth of 3.3 percent for the year. You can see a similar picture in the number of Active Buyers on the platform.

Company Presentation

The company has been able to maintain most of its customers added during the pandemic. Once again they saw a slight dip in total active buyers, but it was a marginal drop. I don’t think this slight dip in growth is something to worry too much about. They saw explosive growth during the pandemic and they are for the most part keeping the large increase in users that came during the pandemic.

The other part of this that plays into the favor of the company is that getting new buyers is much harder than getting return customers. Once someone has heard about your website and used it, given it was not a bad experience, then they are much more likely to return. It is also much cheaper on an ad spend front to get those customers back to your platform than to acquire a new customer. They outlined this opportunity in their company presentation and I have included below.

Company Presentation

I do not think that the company is going to experience a drop off in sales on the platform, barring a recession. That is a risk for the company. They seem to have maintained their new customers. I would expect the company to experience small growth going forward. I do think that growth is going to be slow over the next year, especially on the GMS side of the business. They are now going to start comparing to 2022 on the year over year comparables. Business started to slow down in 2022 so don’t be surprised to see some growth over the next year. They have potential to continue to grow revenues through certain channels. We will discuss those further in the following section of the analysis. It might not be enough growth to justify the current valuation.

Financials

Despite the slowdown in GMS and active accounts the company did see growth on its top line. Revenue grew over 10% from 2021 to 2022. This growth mostly came from an increase in the fees that Etsy charged to users for each transaction. In April of 2022 they increased the amount sellers pay for each transaction from 5 percent to 6.5 percent. While the revenue growth number is good to see that growth is not going to be a consistent and growing figure. They cannot continue to raise the fees they charge without pushing users away. They received a lot of pushback from the selling community with the raise from 5 to 6.5. You cannot rely on this for revenue growth going forward.

The other portion of the revenue growth came from ads on the platform. This is a strong potential revenue driver for the company and a very interesting part of the business. We have seen this side of the business explode for Amazon ($37 billion in revenue and a growth rate of 50% and 20% the last two years). Etsy breaks out the revenue from this business into its “Services'' line item. Most of this revenue is related to the ads business. That business saw steady growth of 12% last year as well. I think this will continue to be a good revenue driver for the company. The company does not break out the costs related to this business so we do not know the margin, but I would think that this is a high margin business. While this business is great for Etsy, I do think there are limitations on growth here as well. Etsy is not the same platform as Amazon. If Etsy pushes this side of the business too hard they could easily frustrate many of the small shop owners. In essence those who can pay will get the traffic to their shops instead of the small shops. This matters on a platform like Etsy much more than Amazon. It is a different type of seller and buyer than what you get through Amazon. I think the company can continue to grow revenues in this business line at +10%. I think this will be one of the main profit drivers for the company going forward. I think the ad business can continue to provide growth in revenues for the company.

The company has been able to produce solid EBITDA each year as well. The EBITDA margin has fluctuated a bit but was still strong in 2022. This allows the company to continue to invest and grow its business. I would like to see this margin increase back up to 30% in the coming year. I think the company can do that if it keeps costs under control.

The chart below shows GMS, revenue, and EBITDA for the company over the past years. Overall it shows strong growth for the company.

{kind=link}

The other thing to look at are the expenses. This is one area that I was not impressed with when reviewing Etsy. I think there is a lot of room to be much more efficient on the cost side of the business. One of the benefits of a company growing revenues is that they are able to hit scale and many of their expenses become a smaller part of their revenue. Most companies have a certain amount of fixed costs. These are not really going to change much with revenues, so as revenues scale they become a smaller percentage of total revenue (this is not true for all expenses such as variable expenses). This has not been the case with Etsy. Expenses have not decreased as a percentage of revenue. Like many companies during the COVID boom, it seems that the company thought the growth would keep going longer and they were caught with more expenses than needed. They weren't like many tech companies that have gone through rounds of layoffs such as Meta, Amazon, Google, etc. but it still seems they have run expenses up a bit much. The company did make an emphasis on this though during their annual report. They slowed hiring in 2022 as the market slowed down as well.

{kind=link}

They also state how their revenue per headcount has greatly increased from 2019 to 2022. They fail to give the comparison of 2021 to 2022 though. I would imagine that the number has seen a decrease. The company does not provide headcount numbers in the 10-K to verify.

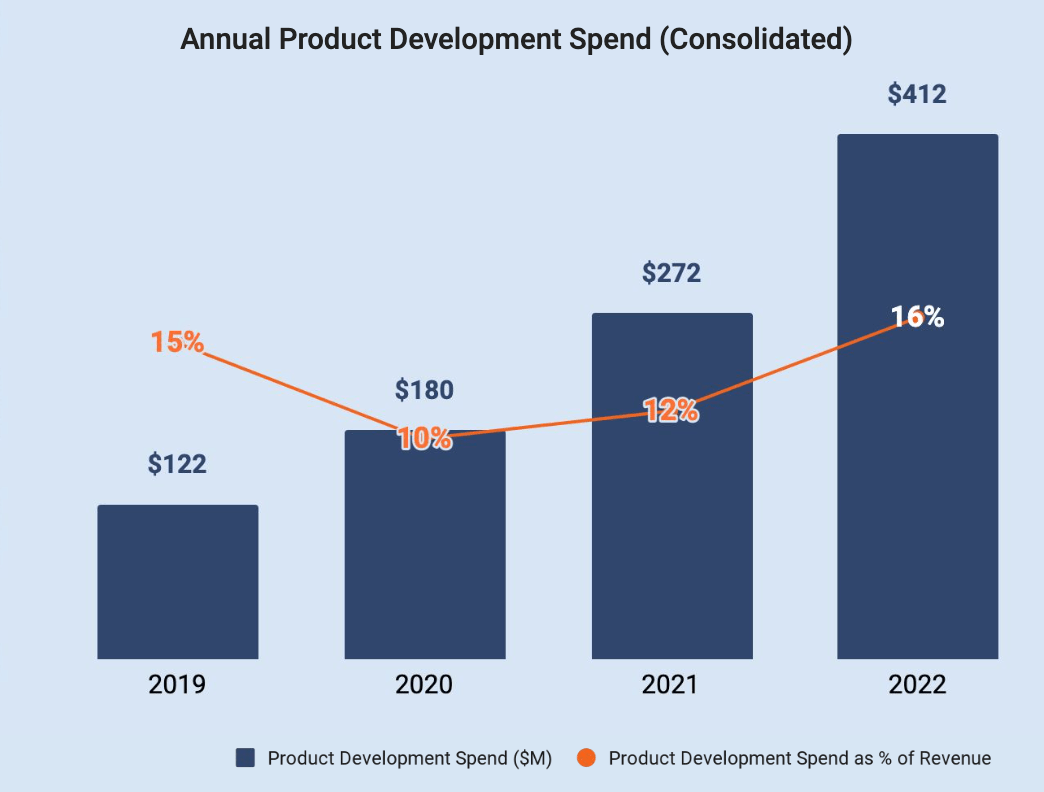

One of the big expense increases is in Product Development. Normally I would say that R&D is a great place to put money. It seems though that Etsy might have gotten carried away on this front. They saw massive increases in revenues and their expenses on this side of the business grew even faster. They spent nearly 4x as much on product development in 2022 as they did in 2019. Their revenues have grown rapidly but the product development costs make up a higher percentage of revenue than they did in 2019 off a much smaller revenue base. They state that most of this increased cost is in headcount.

{kind=link}

Their G&A expense also grew at a faster pace than revenue last year. It is hard to generate a higher profit when your expenses are growing at a faster pace than your revenues. This is an expense that I think Etsy could easily have more control over.

In short the company is growing expenses as fast if not faster than revenues. It seems to have overhired during the pandemic boom, like most tech companies. I understand the increase in product development, but I do think it got out of hand. I don’t know if they are getting 4x the products internally as compared to 2019. I would like to see Etsy get its costs more under control. They are no longer in a booming growth stage and need to be more disciplined on costs.

Risks

The biggest risk to Esty that I see is the economy as a whole. Etsy is discretionary spending. If people need to tighten their belts and cut back on spending then Etsy could feel that pain. Recession risk is very real for Etsy. The company came off a booming period during COVID there is the risk that the company is not able to maintain the added customers. We have already seen a slowdown in business, although small at the moment. They need to be able to hold onto those customers. I also think there is a risk they try to grow the business in the wrong way and alienate their sellers and buyers. They need to be sure to stay in their lane.

Conclusion

Overall I really like Etsy as a company. They have a strong business with a certain amount of moat from competition. They have become a much bigger company following COVID. I think they have some opportunities to continue to grow revenues, particularly with their ad business. The company saw a small dip in its GMS while increasing prices to push out some revenue growth. I think the company can continue to grow from here going forward, although I do think that growth is going to be much slower. This is where my hold up with the stock comes into play. It is currently trading at a P/E ratio of 35.8 for expected earnings in 2023 and 28.9 for expected earnings in 2024. This is a fairly rich multiple for a company that I see growing revenues at a rate in the single digits this year. Maybe they keep costs down and are able to drive higher earnings. That seems to have been baked in somewhat to the estimated EPS provided. I really like the company but I think the valuation is a little rich for me at the moment. I would be interested in purchasing the stock were it to experience a pullback in price. I like the company, I just don’t necessarily like the stock at the current price. Watch this one for any pullbacks in pricing.

For further details see:

Etsy: Great Company, Expensive Stock