SLQT - EverQuote Sees Lower-For-Longer Auto Insurance Industry Downturn Ahead (Downgrade)

2023-09-14 16:10:48 ET

Summary

- EverQuote, Inc. provides online consumer insurance shopping and lead generation for insurance carriers and agents.

- The company aims to simplify insurance shopping and make it more personalized while saving time and money for consumers and insurance providers.

- EverQuote's recent financial trends show a material decline in revenue and operating income, as well as a sharp fall in earnings per share.

- My outlook for EverQuote, Inc. is now Neutral [Hold].

A Quick Take On EverQuote

EverQuote, Inc. ( EVER ) provides online consumer insurance shopping and lead generation for insurance carriers and agents.

I previously wrote about EVER with a Buy outlook, before management’s surprise announcement it was exiting the health insurance business segment.

Given materially declining revenue and management’s assumption of a "lower for longer" environment ahead, my outlook on EVER is Neutral [Hold].

EverQuote Overview And Market

Established in 2008, EverQuote aims to simplify insurance shopping and make it more personalized while saving time and money for both consumers and insurance providers.

The company is led by CEO Jayme Mendal, who joined in 2017 after serving as Vice President of Sales at PowerAdvocate.

EverQuote connects insurance seekers to providers for various insurance types, including auto, home, renters, and life insurance.

Identifying suitable insurance products can be challenging for individuals due to limited online choices, pricing disparities, and an abundance of complex coverage options.

EverQuote offers a platform that streamlines insurance shopping in the United States.

As the company attracts more customers, it gathers more data to enhance personalization, conversion rates, and client satisfaction. An increased number of providers also helps to draw more consumers and contributes to data collection.

EverQuote promotes its services through numerous online channels such as search engines, email marketing, social media platforms, and display ads.

A 2023 market research report by Grand View Research estimated that the global Insurtech market was valued at $5.45 billion in 2022 and is projected to reach $161 billion by 2030 - with a very high CAGR of 52.7% during the forecast period (2023-2030).

The primary driving force behind this market growth is the need to transform the insurance industry to cater to a broader customer base including high-net-worth individuals [HNWIs], upper-middle-income groups, and lower-middle-income groups.

Leading banks and insurance firms are anticipated to improve their offerings or form strategic alliances with financial technology innovators to deliver innovative payment solutions to clients.

The growth trajectory of the U.S. Insurtech market from 2020 to 2030 is shown below:

U.S. Insurtech Market (Grand View Research)

Major competitive vendors that provide insurance industry technology include:

-

SelectQuote

-

Insurify

-

The Zebra

-

Policygenius

-

TrueMotion

-

Esurance

-

CoverHound

EverQuote’s Recent Financial Trends

-

Total revenue by quarter has dropped materially recently due to its exit from the health insurance business and a continued drop in auto industry results; Operating income by quarter has also worsened further into negative territory.

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has fallen slightly; Selling and G&A expenses as a percentage of total revenue by quarter have increased recently.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) have fallen sharply due to revenue contraction.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

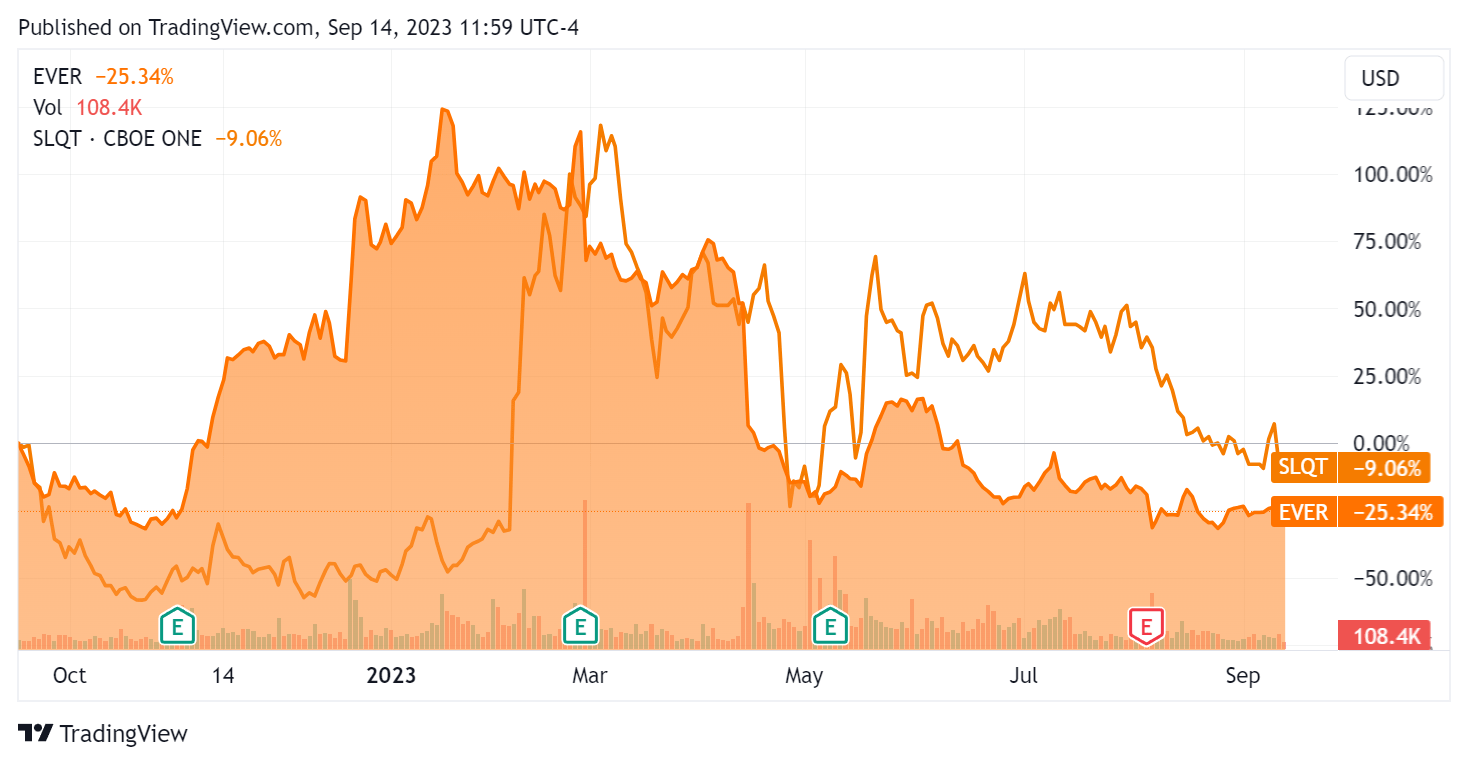

In the past 12 months, EVER’s stock price has dropped 25.34% vs. that of SelectQuote’s ( SLQT ) fall of 9.06%:

52-Week Stock Price Comparison (Seeking Alpha)

{kind=link}

For balance sheet results, the firm ended the quarter with $31.0 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash used was ($10.6 million), during which capital expenditures were $4.3 million. The company paid $27.5 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For EverQuote

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 0.5 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 0.6 |

| Revenue Growth Rate |

| -12.7% |

| Net Income Margin |

| -8.3% |

| EBITDA % |

| -6.8% |

| Market Capitalization |

| $206,870,000 |

| Enterprise Value |

| $180,450,000 |

| Operating Cash Flow |

| -$6,310,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.94 |

(Source - Seeking Alpha.)

As a reference, a relevant partial public comparable would be SelectQuote, Inc. ((SLQT)):

| Metric [TTM] |

| SelectQuote |

| EverQuote |

| Variance |

| Enterprise Value / Sales |

| 0.8 |

| 0.5 |

| -41.7% |

| Enterprise Value / EBITDA |

| 21.2 |

| NM |

| --% |

| Revenue Growth Rate |

| 31.3% |

| -12.7% |

| -140.5% |

| Net Income Margin |

| -5.8% |

| -8.3% |

| 42.5% |

| Operating Cash Flow |

| -$19,380,000 |

| -$6,310,000 |

| -67.4% |

(Source - Seeking Alpha.)

Sentiment Analysis

I prepared a Sentiment Analysis for the most recent earnings call by management:

Earnings Transcript Key Terms Frequency (Seeking Alpha)

The chart above indicates significantly negative sentiment about the industry conditions the company is facing, with the high frequency of negative terms.

Analysts questioned management about the firm’s balance sheet, a prolonged difficult macro environment and free cash flow projections.

Management responded that as Q2 proceeded, it took the decision to assume a lower for longer environment, sold its health assets and modified its loan facility to give the firm more flexibility.

Also, leadership believes the current auto industry environment is the "lowest trough of the downturn" but expects "recovery to build as we get into 2024."

As a result, management expects the firm to reach cash flow breakeven in the first half of 2024 based on the assumptions of a modest recovery in auto insurance and reduced cash flow breakeven point after cost cuts.

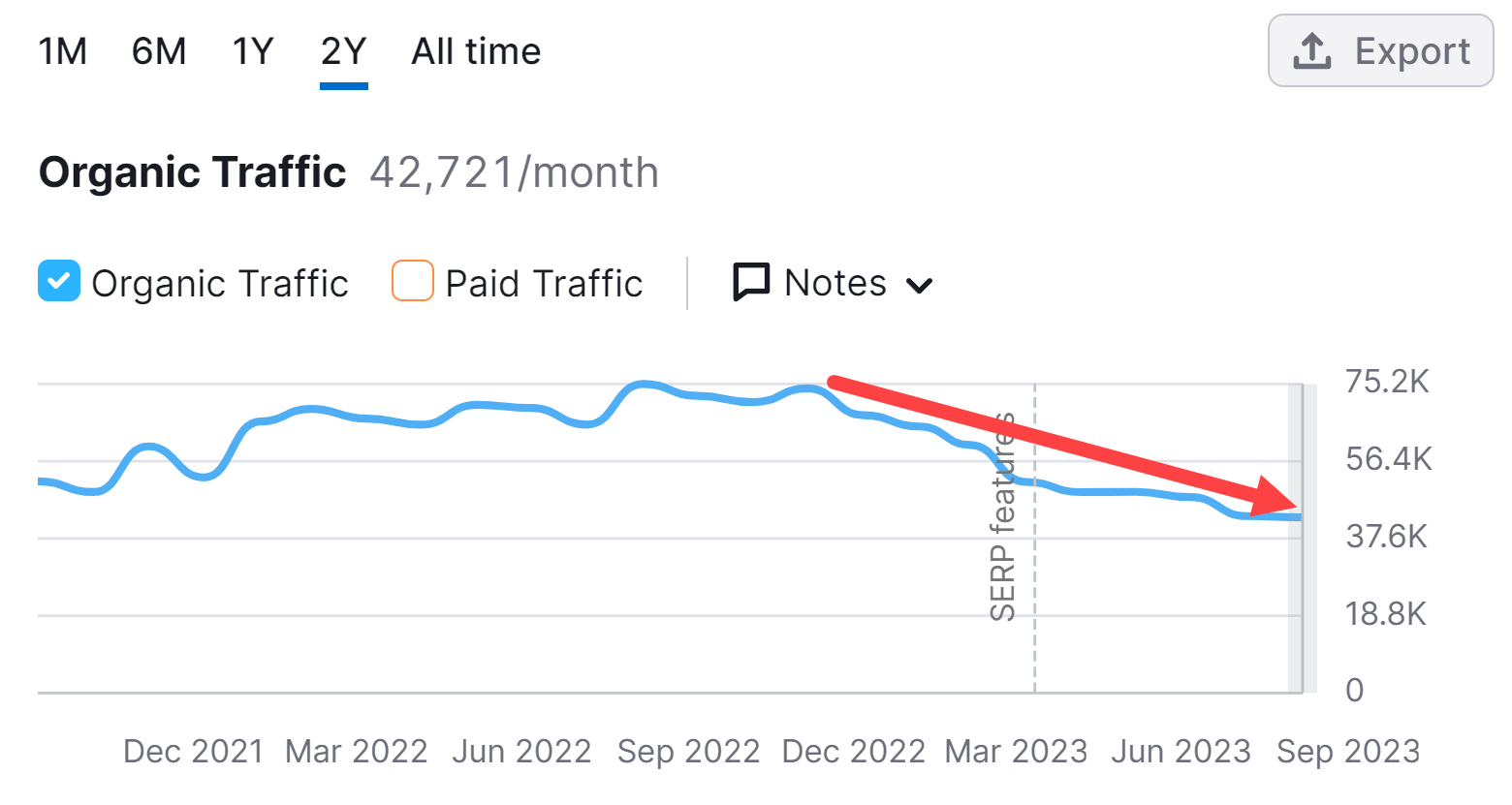

SEMRush’s traffic monitoring service indicates a significant drop in traffic to EverQuote’s website over the past several months:

Website Traffic History (SEMRush)

{kind=link}

Commentary On EverQuote

In its last earnings call (Source - Seeking Alpha ), covering Q2 2023’s results, management highlighted a drop in revenue due to reduced insurance carrier marketing budgets and a contraction in agent demand due to cutbacks from carrier marketing subsidies for agents.

In response, leadership made a large force reduction late in the quarter and exited its health and Medicare insurance segment due to its capital-intensive characteristics and ‘constant changing regulatory environment’.

Management now has a "lower for longer" auto insurance industry outlook and raised additional capital to fund periods of volatility the team anticipates ahead.

Total revenue for Q2 2023 dropped 33.3% year-over-year and gross profit margin fell 2.3%.

Selling and G&A expenses as a percentage of revenue rose by 1.6% YoY, and operating losses increased by 40.8%.

The company's financial position is moderate, with about three year’s worth of cash based on trailing twelve-month free cash use. EVER has no debt.

Looking ahead, consensus estimates for 2023 full-year revenue anticipate a drop in total revenue of about 30.6% YoY.

If achieved, this would represent a far larger decline versus 2022’s drop of 3.46% over 2021.

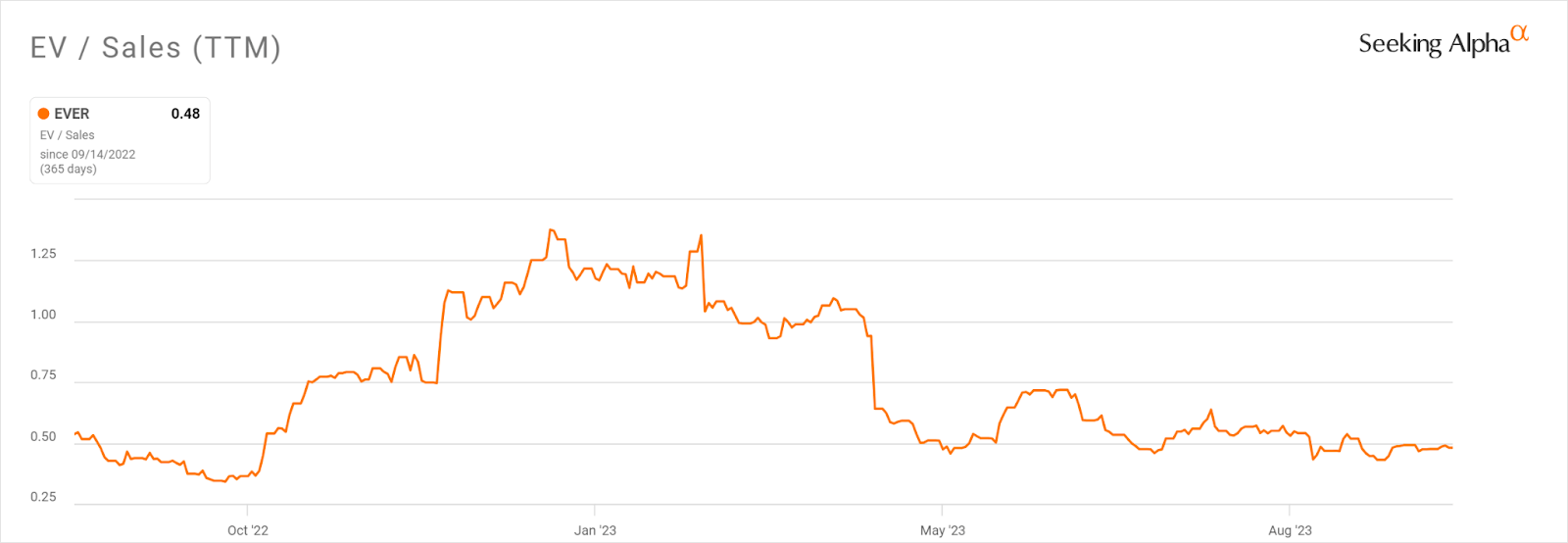

In the past twelve months, the firm's EV/Sales valuation multiple has ended the period roughly the same as it started, as the chart from Seeking Alpha shows below:

EV/Sales Multiple History (Seeking Alpha)

{kind=link}

A potential upside catalyst to the stock could include improved operating results from the firm’s restructuring efforts.

However, given declining revenue and management’s assumption of a "lower for longer" environment ahead, my outlook on EverQuote, Inc. is Neutral [Hold].

For further details see:

EverQuote Sees Lower-For-Longer Auto Insurance Industry Downturn Ahead (Downgrade)