NVTA - Exact Sciences Up 25% YTD: Here Is What To Expect In 2023

Summary

- Despite its price surge, EXAS's valuation remains aligned with industry averages.

- EXAS has one of the clearest profitability paths in a market characterized by heavy losses stemming from aggressive growth initiatives.

- We might see some profit-taking in the coming weeks, but I expect EXAS will end 2023 higher than current levels.

Investment Thesis

Exact Sciences ( EXAS ) enjoys a dominant position in one of the most lucrative markets in molecular diagnostics; Colorectal Cancer screening. It is one of the deadliest yet most preventable cancers, with a total incidence rate of 150,000 annually. It takes a polyp fifteen years to turn into a cancer cell, leaving no justification for the high number of deaths caused by this condition. EXAS' business proposition for physicians and policymakers is simple; Cologuard detects CRC early, dramatically increasing the survival rates and leading to better healthcare outcomes at a lower cost.

Last year was terrible for the sector's stocks, with virtually all molecular diagnostic companies underperforming the index. With high (and in many cases sticky) R&D costs, and heavy reliance on equity funding, these companies seemed to have a low prospect given the rapid deterioration in market conditions. Restructuring plans were met with skepticism, and for a good reason. It takes time to wind down R&D programs. Medical obligations for clinical trial patients have to be met for ethical reasons, regardless of balance sheet condition, making it harder to cut expenditures at least at the same pace that market conditions have changed. In past articles, I warned investors that the "realignment plans" of Invitae ( NVTA ), Sema4 ( SMFR ), and OncoCyte ( OCX ) would progress at a slower speed than many think.

When I first looked at EXAS in the fall of 2021, I realized it was different. Unlike its peers, I believed in its ability to quickly pivot its revenue into profitability. It didn't have many of the obstacles facing the likes of NVTA. It had a solid balance sheet; a significant portion of its spending was operational, focused on marketing and sales, and its R&D spending was on mature clinical programs off their cost peak.

In October, I issued a buy rating, and after a few weeks, EXAS reported exemplary Q3 earnings, demonstrating early success in its profitability plans. Shares were up 20% in a single day. I believed that the rally had legs, and following Q3, I published another article laying out the reasons for this hypothesis. Since then, shares have been up 95%.

We might see some profit-taking in the coming days, given the rapid appreciation in EXAS' shares. The scope of my initial value hypothesis is narrower than it was in October and November, and my bull thesis is now more based on EXAS's market position and improved earnings outlook, as explained in more detail below.

Market Position

Unlike other malignancies, the colorectal cancer screening market is notoriously difficult to break into due to high barriers to entry. Government officials still allow Natera ( NTRA ) to sell controversial microdeletion prenatal tests with 11% accuracy (89% false positives). As far as I know, there is no need for FDA approval for lung, breast, prostate, or any other malignancy, and none on the market today has one to my knowledge.

This doesn't apply for CRC, where the bar is pretty high. Not only does the test need to be accurate to the highest degree, but it also needs to go through a tedious FDA formal regulatory approval process.

One might ask, why? Well, one reason that I can think of is that there exist other tests that raise the bar with relatively low risk and inconvenience. For example, a colonoscopy has a high accuracy rate, and compared to a brain tissue biopsy (brain sample collected via a needle), it is pretty decent. Since colonoscopy is a viable alternative, it is the standard for other tests.

In practice, colonoscopy has low adherence rates. Patients ignore doctors' orders for periodic screening. 40% of high-risk patients aged 60 or older have yet to have one. Physicians know that a relatively high number of these will die, despite the fact that early detection increases the survival rate to almost 100%. There is also a public interest in increasing adherence rates. CRC is common in patients aged 60 and over, the eligibility age for Medicare. Since prevention is much less costly than cure, officials are adopting a preventive approach to healthcare. EXAS's pitch to physicians and healthcare providers is simple, Cologuard, the only FDA-approved CRC screening test improves early detection, lowers mortality rates, and releases pressure on public finances. While EXAS' peers are fighting tooth and nail to get reimbursed for their services, EXAS is running a smooth ship, with low uncollectable accounts, enhancing gross margins, and less staff to chase after payments, improving operating margins. Cologuard is recommended in every major CRC guidance, and insurance companies such as UnitedHealth (UNH) and Humana (HUM) happily pay for it, knowing that it is a valuable investment for their Medicare Advantage enrollees.

Competition

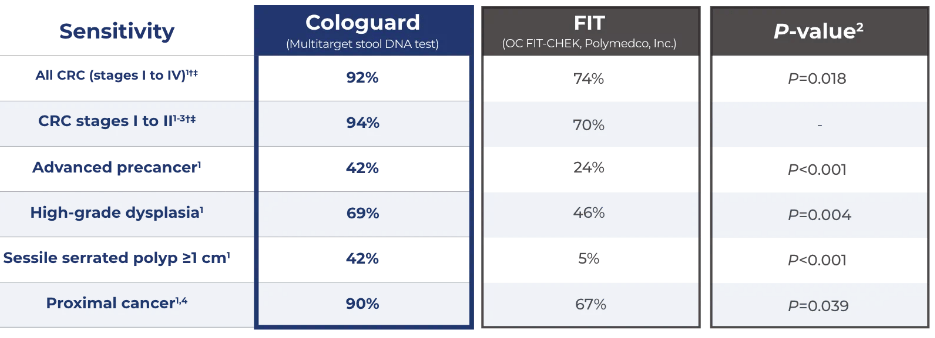

Cologuard competes with legacy s-DNA tests such as FIT and FBOT, with the latter constituting the lion's share in the CRC screening market, competing on price rather than quality. FIT costs $30 compared to Cologuard's $550, making it the preferable test for some Managed Care Organizations. Nonetheless, Cologuard's superior accuracy underpins the marketing pitch of its sales force across the US.

{kind=link}

There are some companies currently developing s-DNA CRC tests. DiaTech Pharmacogenetics, a private, Italian-based molecular diagnostic company, sells EasyPGX CRC screening kits in Europe. I am unaware of any FDA pre-authorization application for EasyPGX, leaving the US market for EXAS.

Prescient Metabiomics is also developing a CRC screening test, differentiating its product by focusing on adenomas. It announced a prospective study in 2021, but since then, there has yet to be any update on recruitment, unlike Geneoscopy, which finished recruiting patients for its 10000-strong clinical trial last year. Regardless of the recruitment progress, these companies will take at least five years before they're able to provide meaningful results and a few more years for the FDA application process. Until then, EXAS has its sDNA market of its own.

In the liquid biopsy space, there have been attempts to create a blood alternative to stool DNA. Epigenomics gained FDA approval for Epi proColon in 2014 but found little commercial success, failing to win the minds and hearts of Key Opinion Leaders, who recommended against its use.

Guardant Health recently announced disappointing results for Guardant Shield, with a sensitivity of about 83%, significantly lower than Cologuard. Its competitive advantage stems from it being a blood test, which could enhance adherence for patients who find it inconvenient to hand stool. In terms of testing quality, EXAS has a decisive advantage.

Valuation

Despite the recent rise in the company's shares, its price-to-sales ratio remains in line with peers (third from the top, as shown in the graph below.) It is a bit more expensive than the likes of NeoGenomics ( NEO ), which experienced an arguably botched leadership transition in recent quarters, potentially determining shareholder confidence. Its premium over ONX and NVTA is also justified, stemming from its superior balance sheet, compared to these two companies, who barely have enough cash for the coming 12 - 18 months, as discussed in previous articles.

Yesterday, the company announced that it is ahead of profitability plans which previously estimated a positive adjusted EBITDA margin in Q3 2023. The new guidance points to a positive adjusted EBITDA margin starting in Q4 2022. I am not surprised that this was the case, given the company's relatively low spending on R&D as a percentage of revenue compared to peers. This is due to its solid market position in CRC, which already has FDA approval. Most of its spending goes on Sales and Marketing, giving the company more flexibility in managing costs.

Assuming a 14% adjusted EBITDA and a declining growth schedule starting at 17% in Q4 2022, the company could generate $5 billion in operating cash flows in the next ten years. Our main concern stems from the high capital costs, which currently hover around $150 - $200 million annually. Advancements in Next Generation Sequencing devices drive significant capital expenses, and many molecular diagnostic testing companies find themselves driven to invest in the latest devices to maintain their edge.

Nonetheless, we believe that EXAS has entered a new era of value creation, and we don't expect a decline in shares in the coming few years. Its defensive revenue stream, with high exposure to reliable payors such as Medicare and Medicare-Advantage sponsors, shields it from recession dynamics.

On the balance sheet side, I don't find the convertible debt too alarming. These convertible notes carry insignificant interest rates and will likely be converted into stocks once they reach maturity. In total, if converted, these shares will add approximately 20 million shares, representing an 11% increase from the current number of shares outstanding. Below is a maturity schedule showing the impact of converting EXAS' convertible notes.

| Amount |

| Maturity |

| Conversion/Shares |

| % Shares Outstanding |

| $315.00 |

| 2025 |

| 4.2 |

| 2.4% |

| $747.00 |

| 2027 |

| 6.7 |

| 3.8% |

| $1,200.00 |

| 2028 |

| 9.4 |

| 5.3% |

*Figures in millions except percentages and maturity dates.

Summary

I think EXAS's relatively low R&D spending will allow it to leverage its revenue into profitability more quickly than its peers. The changes to its guidance on operating income margins point to the company being on track toward achieving long-term value creation objectives. We anticipate a healthy and consistent stream of free cash flow in 2025 and forwards, providing a sustainable income stream for EXAS to continue investing in new R&D initiatives to drive future growth in an expanding market. Our primary concern stems from the high CAPEX necessary to maintain its edge beyond Cologuard CRC screening, where it enjoys a dominant market share protected by high barriers to entry. We might see some profit-taking in the coming weeks, but I remain bullish on EXAS in 2023.

For further details see:

Exact Sciences Up 25% YTD: Here Is What To Expect In 2023