WE - EXG: A History Of Underperformance But An Attractive 9.10% Yield

2023-10-03 16:57:32 ET

Summary

- Eaton Vance Tax-Managed Global Diversified Equity Income Fund is a popular global income-focused closed-end fund that offers diversification outside the U.S.

- The EXG closed-end fund has underperformed both the S&P 500 Index and the MSCI World Index over just about every period, including during bear markets, raising concerns.

- Despite its underperformance, the EXG fund offers a high current distribution yield of 9.10% and has a discounted net asset value, making it potentially attractive for investors.

- The fund appears to be able to sustain its distribution going forward, depending on how well it converts its unrealized gains into realized ones.

- The fund itself seems good, but the market does not appreciate it.

The Eaton Vance Tax-Managed Global Diversified Equity Income Fund ( EXG ) is one of the most popular global income-focused closed-end funds ("CEFs") on the market. The fund's global focus is something that many American investors sorely need, as the average investor in the United States has an outsized exposure to the nation, which presents risks that investors in other nations would not have. This fund advertises that it provides an easy way to invest in assets outside of the nation, which would help to reduce their domestic exposure. The fund's 9.10% current distribution yield certainly speaks well to its ability to provide an income, although we will want to investigate its portfolio to determine how good of a job it is actually doing on the global diversification front.

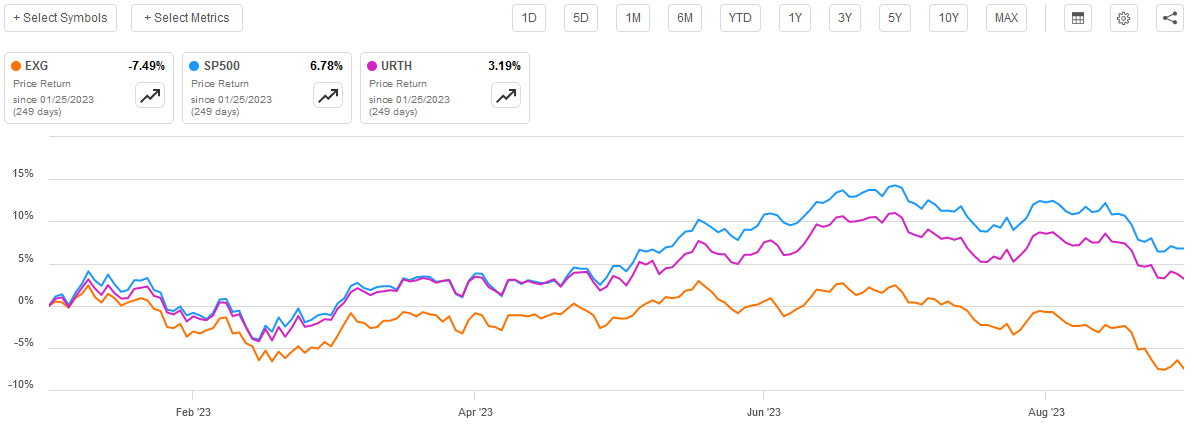

As regular readers may remember, we last discussed this fund back in January. The fund's price performance since that time has unfortunately been quite disappointing as it has significantly underperformed both the S&P 500 Index ( SP500 ) and the MSCI World Index ( URTH ):

{kind=link}

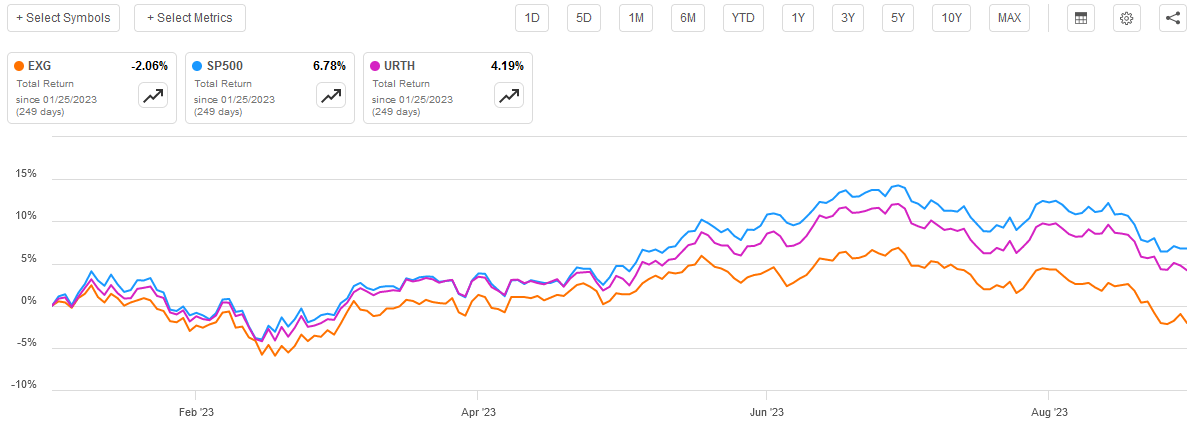

However, as is the case with most closed-end funds, this one provides most of its investment return in the form of direct payments to the investors. A simple look at the fund's share price will not therefore reflect the actual performance that the fund's investors received. After all, while the fund's price might have gone down over the period, the distributions that it paid to its investors offset this decline somewhat. Unfortunately, the fund still underperformed both of the indices even after we take this into account:

{kind=link}

This is, therefore, quite disappointing as it suggests that an investor would have been much better off eschewing the Eaton Vance Fund and just putting their money into an index fund. After all, an investor who is seeking income could always just sell off shares of the fund when they need money to pay their bills. This disappointing situation does not mean that this fund is totally without merit, however, and we should still investigate it to determine how well it can sustain its current yield and continue to deliver on the overall promise that it has made to its shareholders.

About The Fund

According to the fund's webpage , The Eaton Vance Tax-Managed Global Diversified Equity Income Fund has the primary objective of providing its investors with a high level of current income and current gains. This is a fairly reasonable objective for a closed-end fund that invests primarily in equity securities. We can see this focus on equity securities in the fact that 99.83% of the fund's assets are invested in common stock:

CEF Connect

We can also see a small allocation to cash, which is fairly typical for a closed-end fund. After all, while a closed-end fund does not technically have to maintain a cash allocation like an open-end fund does because it does not have to worry about redemptions, managers usually do maintain a small amount of cash to fund opportunistic purchases and shareholder distributions.

The thing that is a little confusing, however, is that the fund claims to be pursuing the goal of generating current income. That is very difficult to accomplish considering that yields from common equities have been at incredibly low levels for over a decade. We can see this in the fact that the S&P 500 Index ((SP500)) yields 1.52% and the MSCI World Index yields 1.67% today. These yields are both substantially lower than an ordinary bank savings account or a money market fund right now. This is why nearly all funds that are focused on the provision of income invest in fixed-income securities.

The fund's fact sheet fortunately provides some insight into the method that the fund employs to generate current income from a portfolio of common stocks:

The Fund invests in a diversified portfolio of domestic and foreign common stocks with an emphasis on dividend-paying stocks and writes call options on one or more U.S. and foreign indices with respect to a portion of the value of its common stock portfolio to generate current cash flow from the options premium received.

Thus, the fund is using a call option-writing strategy in order to generate current income. This strategy generally works pretty well to accomplish that. After all, buy-write exchange-traded funds like the Global X NASDAQ 100 Covered Call ETF ( QYLD ) are able to pretty consistently earn a premium of 1% a month from the sale of index call options. This fund does not do that well, but this is because it is writing out-of-the-money call options, which have lower premiums. In addition, this fund is not overwriting its entire portfolio. At the moment, only 48% of the fund's portfolio has call options written against it, although the majority of the options are in the money:

Fund Fact Sheet

The fact that not all of the portfolio is overwritten means that the fund's income will not be as high as one of the exchange-traded funds. However, at the same time, it means that the fund is not capping its upside to the same extent. This is the big problem with a call option-writing strategy. The investor is essentially capping their upside to the strike price of the portfolio in exchange for current income. This fund can be somewhat flexible to the extent that it does that, which means that it should be able to generate much higher capital gains during bull markets and switch to generating option income during flat or bear markets.

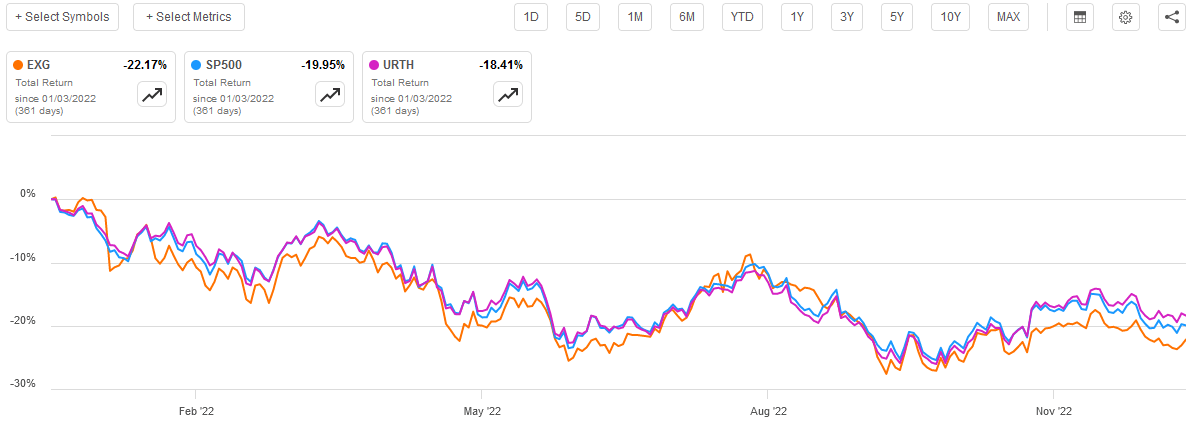

As may be implied by the previous paragraph, the fund's strategy should outperform during flat or bear markets. This is because the premium that is received from the sale of the option boosts the return in the absence of capital gains. It could also serve to offset some of the losses during a bear market. However, this fund underperformed both the S&P 500 Index and the MSCI World Index over the full-year 2022 period, even when the distribution is taken into account:

{kind=link}

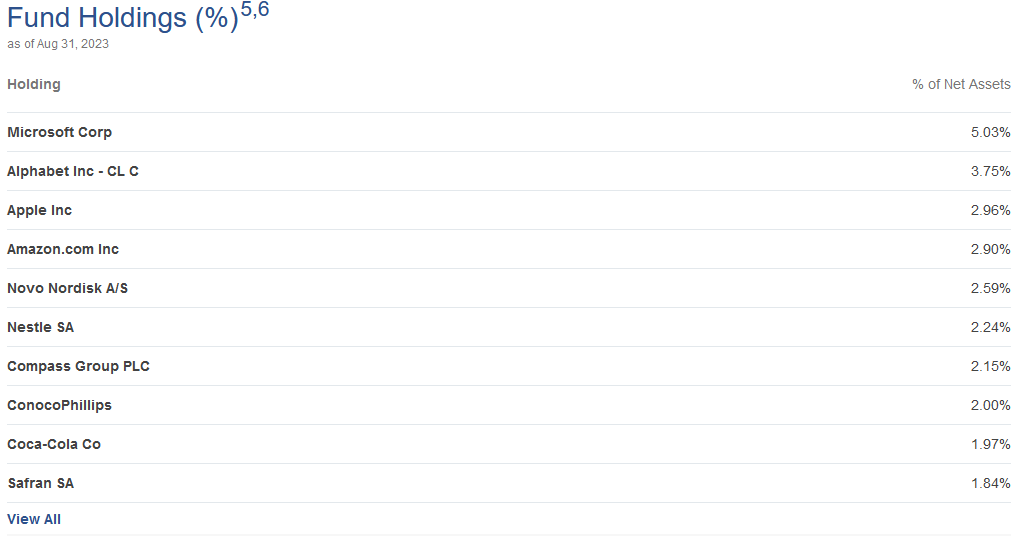

Thus, the fund's strategy failed to perform in a bear market like it is supposed to, although admittedly the fund did manage to keep up reasonably well. In the case of many Eaton Vance funds, this is because the portfolio was heavily weighted towards stocks that underperformed the market in 2022. However, this one does not share that flaw, which we can see by looking at the fund's largest holdings:

{kind=link}

As I pointed out in a blog post , all of the mega-cap technology companies along with Netflix ( NFLX ) and Tesla ( TSLA ), which had been the darlings of the bubble years, substantially underperformed the S&P 500 Index in 2022. This is because the rising interest rates have been leading investors to put their money into short-duration assets. This caught most of Eaton Vance's option-income funds off guard as they had been very heavily weighted to all of these companies. However, this fund does not appear to be as bad as some of Eaton Vance's other funds. However, we do still see that Microsoft ( MSFT ), Google ( GOOG ) (GOOGL), Apple ( AAPL ), and Amazon.com ( AMZN ) account for 14.64% of the fund's portfolio. While this is certainly a lot, it is less than their weightings in the S&P 500 Index so their presence should not be the factor that dragged the index down. If anything, the fact that the fund is less weighted to the index than the S&P 500 should have resulted in outperformance.

We saw this same thing occur over the past month, which has also been a bear market for most assets. As we can see here, once again the fund underperformed both indices on a total return basis:

{kind=link}

The same thing occurs when we look at the total return of this fund compared to the indices on both a six-month and a year-to-date basis. Thus, clearly, the fund is failing to deliver the performance that we would normally expect given its strategy.

As might be expected considering that the fund only has 86 positions in its portfolio, it does not perfectly match the weightings of the MSCI World Index:

Fund Fact Sheet

In particular, we see that energy, materials, and real estate are all significantly underweight relative to the index. In the case of real estate, that is probably a good thing as this sector has been performing very poorly in the face of rising interest rates and the pressure from employees at many companies to continue the telecommuting lifestyle that they became accustomed to during the pandemic. In fact, WeWork ( WE ) filed a regulatory document with the Securities and Exchange Commission yesterday that states that the company withheld $95 million of payments on some of its outstanding notes due in 2027. This is a sure sign that the troubles affecting the office space market are unlikely to be resolved in the near future.

However, the underweight to energy may not be a very good move, as crude oil prices have been one of the only bright spots in the market over the past few months. The price of West Texas Intermediate crude oil is up 17.4% over the past six months and 3.8% over the past month, and energy stocks are also generally among the better-performing sectors in the market right now. While I doubt that a 125-basis point underweight to this sector is enough to cause the entire fund to underperform the MSCI World Index to the degree that it has, it is definitely an issue that the fund could correct.

Distribution Analysis

As mentioned earlier in this article, the Eaton Vance Tax-Managed Global Diversified Equity Income Fund has the primary objective of providing its investors with a high level of current income and current gains. In order to accomplish that task, it invests its assets into a portfolio that primarily consists of dividend-paying stocks. The fund then writes index call options to generate income through the premiums received. This can certainly provide the fund with a high level of income but because these are naked calls, it will sometimes be forced to buy them back before expiration and thus offset some of its income. The fund basically collects all of the dividends that it receives from the common stocks, any capital gains that it realizes from the stock portfolio, and all of the net option premiums and pays them out to its shareholders, net of the fund's own expenses. This can be expected to result in the fund having a very high yield.

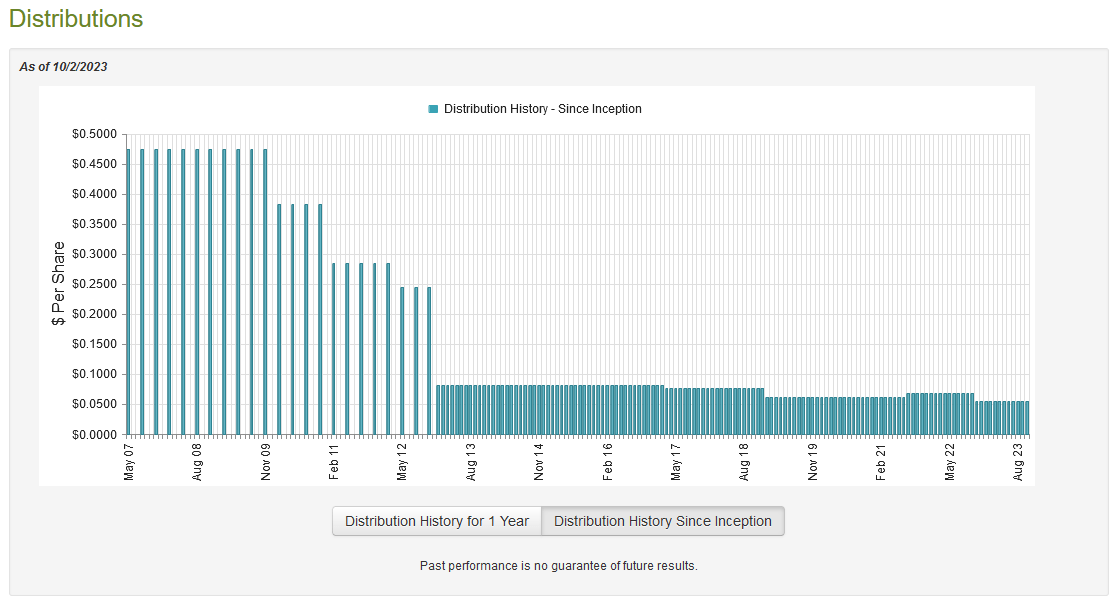

This is certainly the case as the fund pays a monthly distribution of $0.0553 per share ($0.6636 per share annually), which gives it a 9.10% yield at the current price. This is substantially more than either the major domestic or global indices, as was mentioned in the introduction. The fund has, unfortunately, not been especially consistent with respect to its distribution as it has varied quite a bit over the years:

{kind=link}

As we can see, the fund has historically cut its distribution every few years, with the exception of an increase in response to the general euphoria of 2021. This is a worse track record than most of Eaton Vance's other option-income funds, which were frequently quite stable with respect to their distributions until the 2022 bear market. Overall, this fund's distribution history is likely to be a bit of a turn-off for any investor who is seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. When we consider that this is the major goal for most people who are seeking income opportunities in the securities markets, that is a major blow against this fund.

However, as I have pointed out numerous times in the past, the fund's history is not necessarily the most important thing for anyone looking to invest in the fund today. This is because today's buyer would receive the current distribution at the current yield and will not be negatively impacted by the fund's past actions. Thus, the most important thing for a buyer today is how well the fund can sustain its current distribution.

Fortunately, we do have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. This is a much newer document than the one that we had available to us the last time that we discussed this fund, which is nice. This is because this report should give us a good idea of how well the fund managed to take advantage of the market strength that existed during the first half of this year. After all, there was a temporary bubble forming due to optimism over the potential of artificial intelligence that pushed up tech stock valuations and could have allowed the fund to realize some capital gains.

During the six-month period, the Eaton Vance Tax-Managed Global Diversified Equity Income Fund received $25,773,249 in dividends and $8,486,473 from other sources. The fund does not specify what exactly these other sources are, but it reported a total investment income of $34,259,722 over the six-month period. The fund paid its expenses out of this amount, which left it with $20,726,755 available for shareholders. This was, unfortunately, nowhere close to enough to cover the $101,625,748 that the fund actually paid out in distributions to its shareholders over the period. At first glance, this is quite likely to be concerning as the fund's net investment income was clearly insufficient to cover the distributions.

However, there are other methods through which the fund can obtain the money that it needs to cover its distributions. For example, the fund could be able to realize capital gains from appreciation of the stocks in its portfolio. It also receives premium payments from the sale of options. These two things clearly do result in money coming into the fund's possession, but they are not considered investment income for tax purposes. The fund had somewhat mixed results during the period as it reported net realized losses of $26,716,411 but this was more than offset by net unrealized gains totaling $342,356,941. Overall, the fund's net assets increased by $234,741,537 after accounting for all inflows and outflows during the period. In short, this distribution probably is sustainable depending on the degree to which the fund managed to convert the unrealized gains into realized ones. The biggest risk here is that it lost some of its gains in the market correction over the past two months.

Valuation

As of October 2, 2023 (the most recent date for which data is currently available), the Eaton Vance Tax-Managed Global Diversified Equity Income Fund has a net asset value of $8.16 per share but the shares only trade for $7.18 each. This gives the fund's shares a 12.01% discount on net asset value at the current price. This is quite a bit better than the 9.49% discount that the shares have had on average over the past month. Thus, the current price seems like a very good entry point for anyone who is interested in this fund.

Conclusion

In conclusion, the Eaton Vance Tax-Managed Global Diversified Equity Income Fund is one of the most popular global funds for people who are seeking income. Unfortunately, its performance leaves something to be desired as it has been consistently underperforming both the S&P 500 Index and the MSCI World Index during both bear and bull markets. This is certainly not what we would expect from an option-income fund, and it certainly reduces the fund's appeal. Fortunately, the fund's 9.10% yield appears to be sustainable and its current valuation is quite attractive so it might still be worth some consideration.

For further details see:

EXG: A History Of Underperformance But An Attractive 9.10% Yield