NLCP - Fed Says More Pain Needed

2023-09-24 09:00:00 ET

Summary

- U.S. equity markets posted their worst week since March as benchmark interest rates surged through multi-decade highs after the Federal Reserve reiterated a "higher for longer" monetary policy approach.

- Finishing lower for the sixth week in the past eight, the S&P 500 dipped 2.9%, posting its worst week since the Silicon Valley Bank collapse in early March.

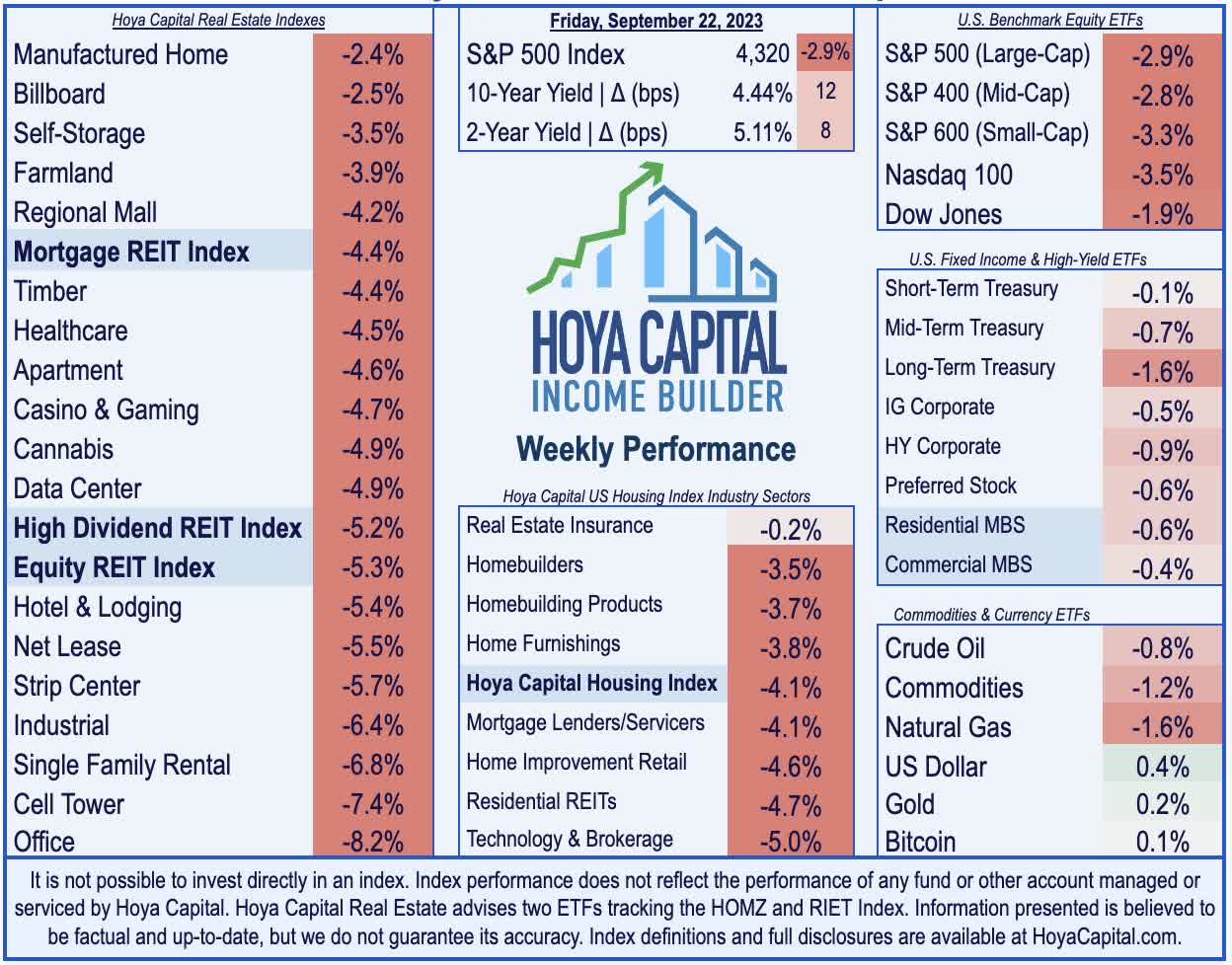

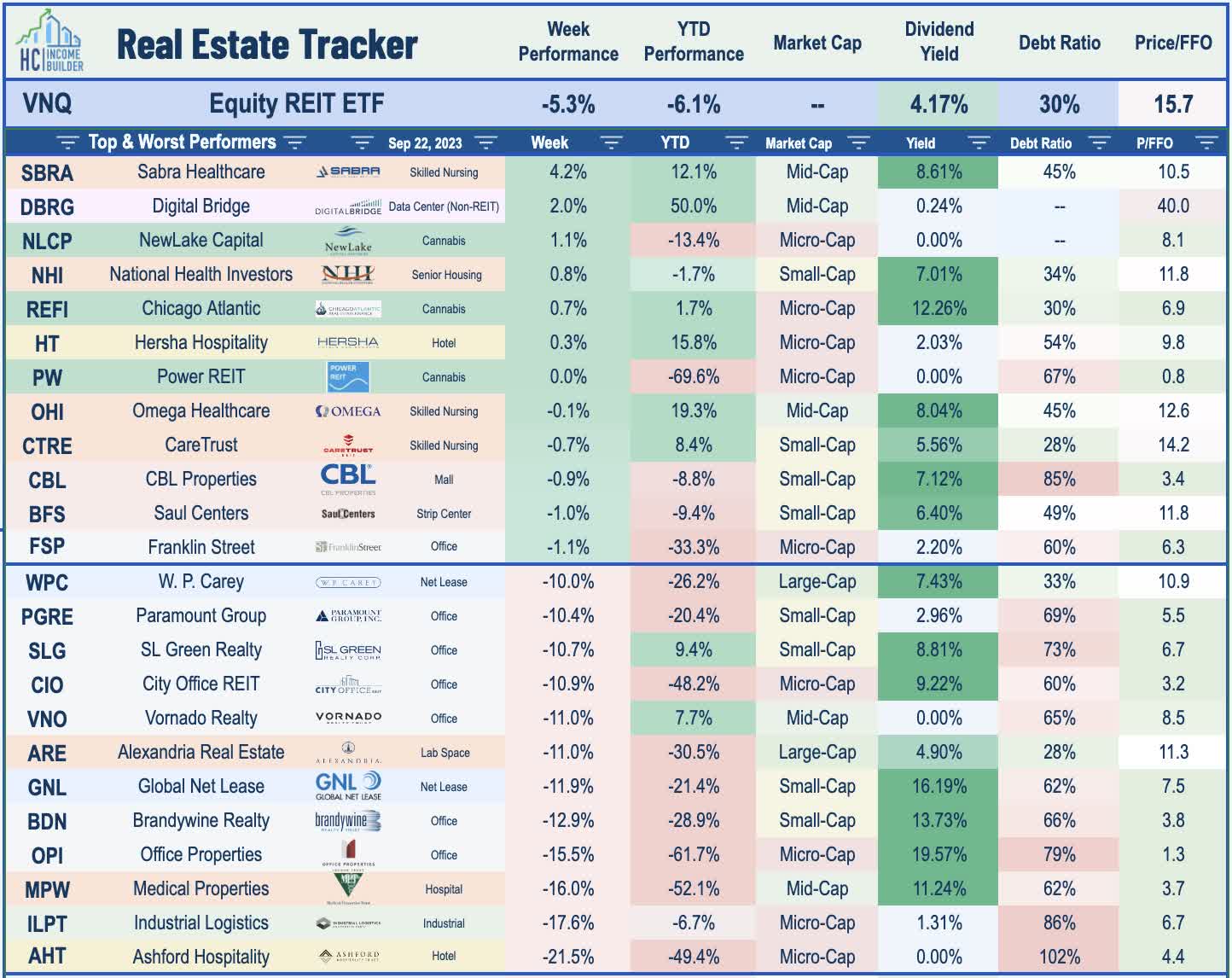

- Real estate equities were slammed especially hard on "higher for longer" concerns as interest rates soared through multi-decade highs. The Equity REIT Index dipped 5.3% on the week.

- WP Carey (WPC) lagged after it announced a strategic plan to sell its office assets - which comprise roughly 16% of its portfolio - aimed at "driving a re-rating" of WPC's stock price, which has traded at discounted valuations to similar-sized net lease and industrial REIT peers.

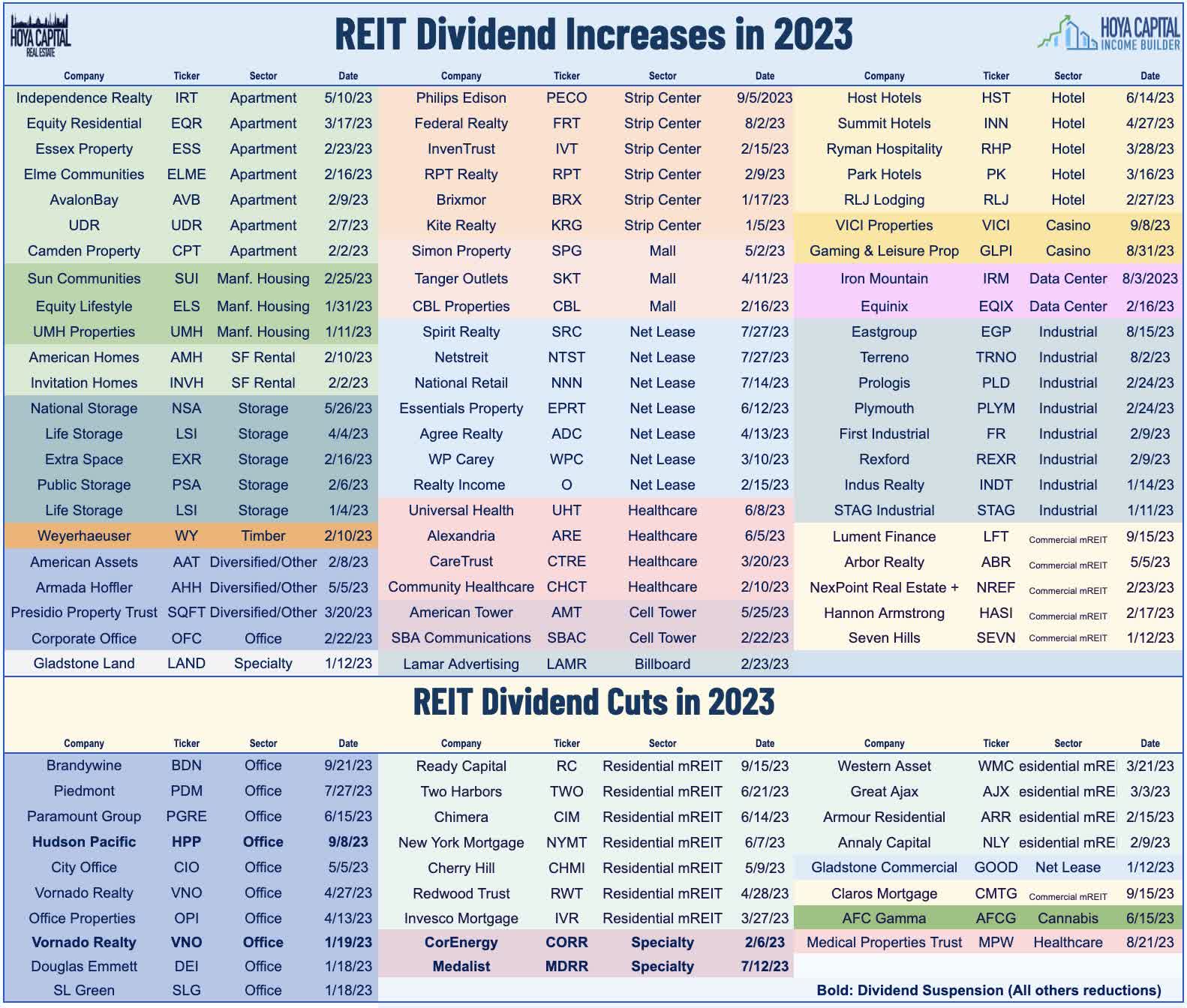

- Office REIT Brandywine (BDN) dipped more than 12% after it reduced its quarterly dividend by 21% to $0.15/share becoming the 10th office REIT this year to reduce its dividend and 27th REIT overall to lower its payout. Nearly 70 REITs have raised their dividends this year.

Real Estate Weekly Outlook

U.S. equity markets posted their worst week since March as benchmark interest rates surged through multi-decade highs after the Federal Reserve signaled that it intends to maintain policy "at a restrictive level" until it is confident that inflation is "moving down sustainably." Concerns over the fermenting " pain " of tight monetary policy - inflamed by the resurgence in oil and gasoline prices since June - have been compounded in recent weeks by a flurry of other complications, including a lingering UAW union strike, a potential government shutdown, and a flaring of trade tensions with China.

{kind=link}

Finishing lower for the sixth week in the past eight, the S&P 500 dipped 2.9%, posting its worst week since the Silicon Valley Bank collapse in early March. Losses across other equity benchmarks were steeper, with the tech-heavy Nasdaq 100 declining 3.5% while the Small-Cap 600 dipped 3%. Real estate equities were slammed especially hard on "higher for longer" concerns as interest rates soared through multi-decade highs. The Equity REIT Index dipped 5.3% on the week, with all 18 property sectors lower by at least 2% on the week, while the Mortgage REIT Index declined by 4.4%. Homebuilders dipped nearly 4% as well after mortgage rates climbed to over 7.50% across several benchmarks - the highest rate since 2002 - as the housing sector's surprising resilience in the face of surging rates will again be tested.

{kind=link}

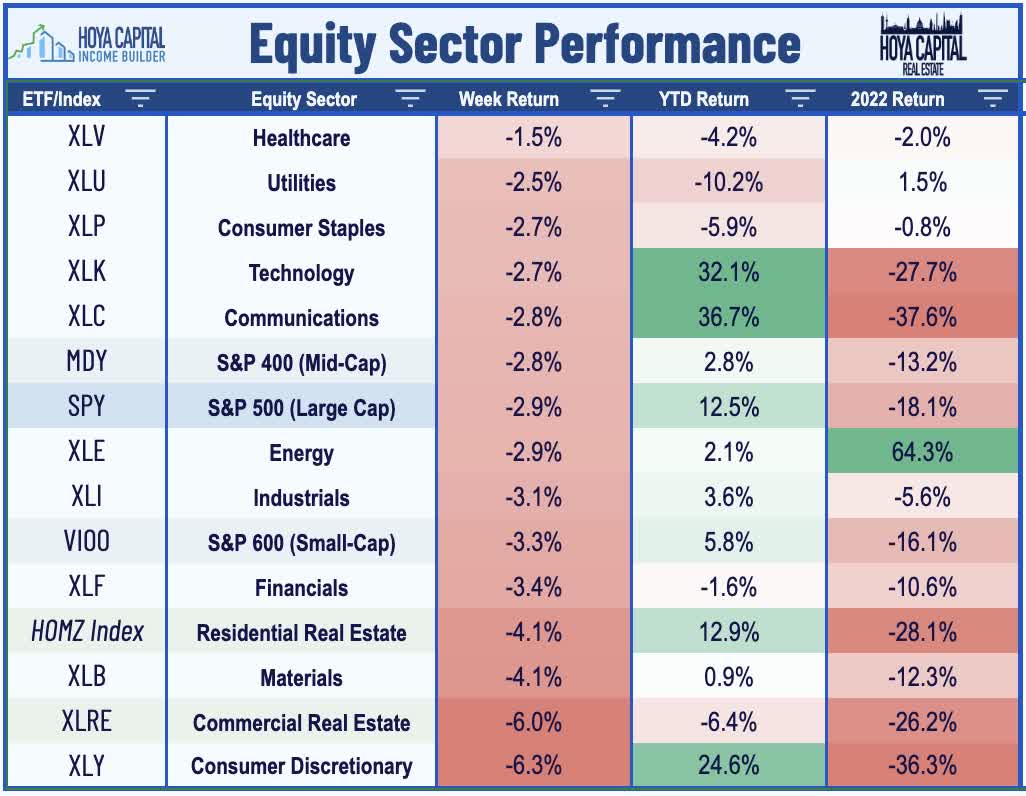

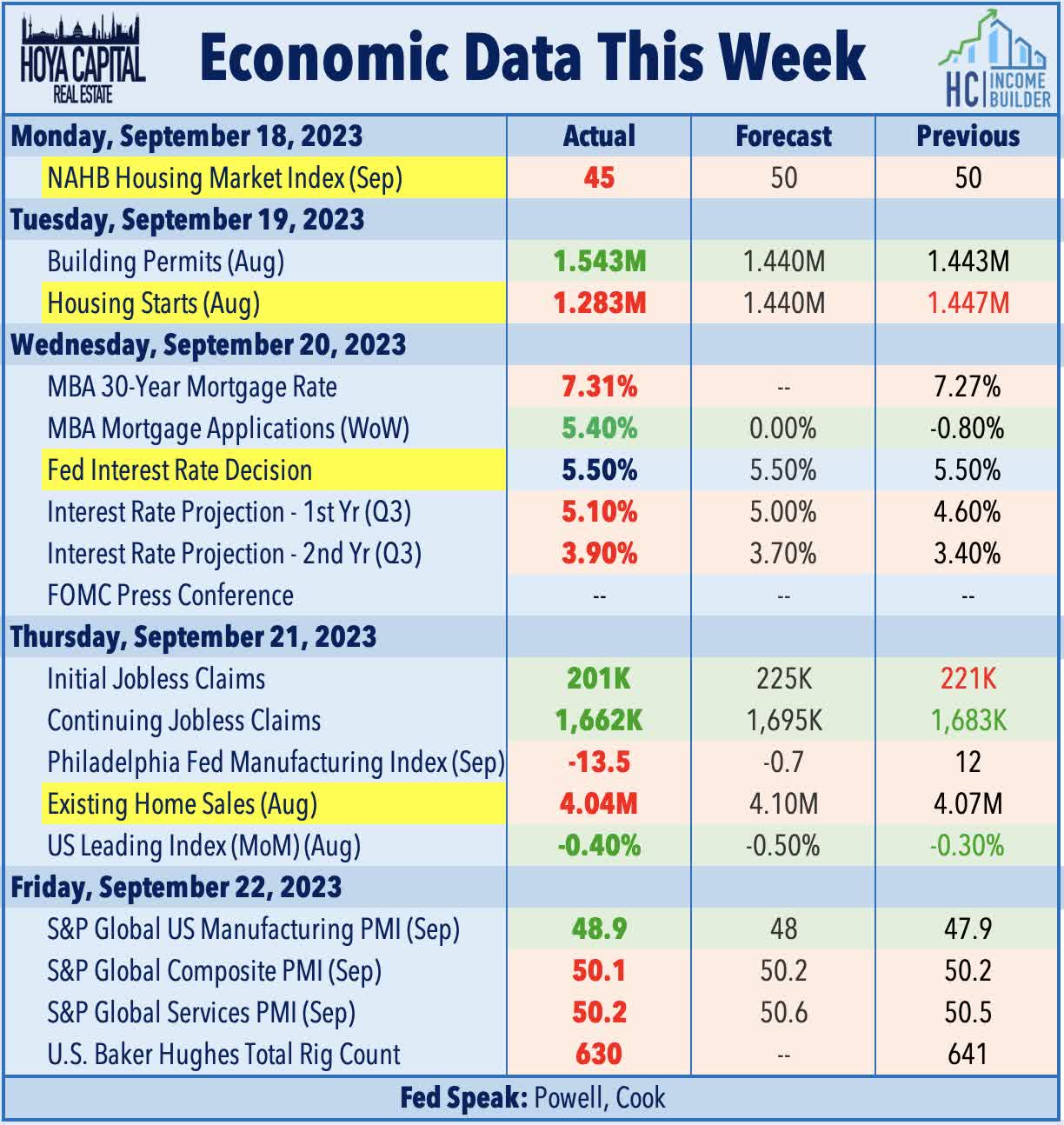

As expected, the FOMC held its target range for the Federal Funds rate at 5.25% to 5.50%, but the "higher for longer" posture was reflected in both Fed Chair Powell's press conference and in the committee's "dot plot" projections, which showed that 12 of 19 officials favored another rate hike in 2023. Fed officials also see less easing next year, with a median estimate for the Fed Funds rate of 5.1% by the end of 2024 - up from 4.6% in June. Projections showed a more upbeat economic outlook for the balance of 2023, while inflation protections were generally unchanged. Benchmark yields jumped after the decision, with the 10-Year Treasury Yield breaching 4.50% intra-day and posting its highest week-end close since 2007 - while the 2-Year Yield swelled another eight basis points this week to 5.11% - the highest weekly close since 2000. Brent Crude Oil prices retreated slightly from ten-month highs on demand destruction concerns while the U.S. Dollar strengthened for the eighth week out of the past nine. All eleven GICS equity sectors finished lower on the week, with Consumer Discretionary ( XLY ) and Real Estate ( XLRE ) posting the steepest declines.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

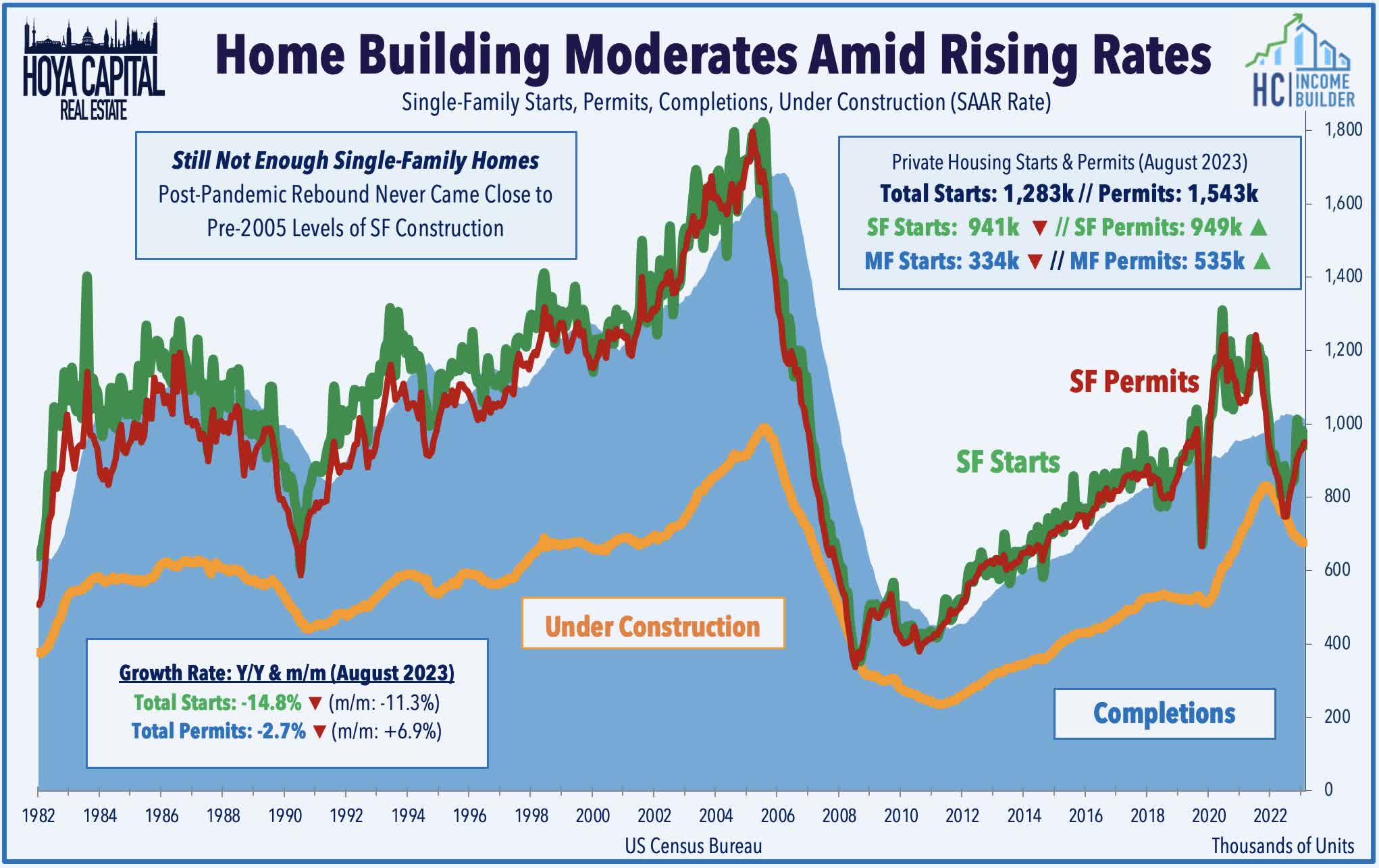

Pressured by the resurgence in mortgage rates, housing data this week showed hints of a "double dip" in housing market activity following relatively strong trends in Spring and early Summer. The Commerce Department reported this week that Housing Starts in August plunged 11.3% from July to a 1.28 million annualized rate, but the decline was driven largely by a sharp decline in multifamily construction. Single-family starts held relatively steady at an annualized rate of 941k - up about 2% from last August - despite the late-summer resurgence in mortgage rates. The 30-Year Fixed Mortgage Rate climbed to 7.19% this week on the Freddie Mac Index, which was the highest since March 2022, which has resulted in a sharp decline in mortgage applications for home purchases, which are now at levels not seen since the mid-1990s. Record-low inventory levels of existing single-family homes, however, has helped to sustain some base level of demand for new home construction in the face of these substantial interest rate headwinds.

{kind=link}

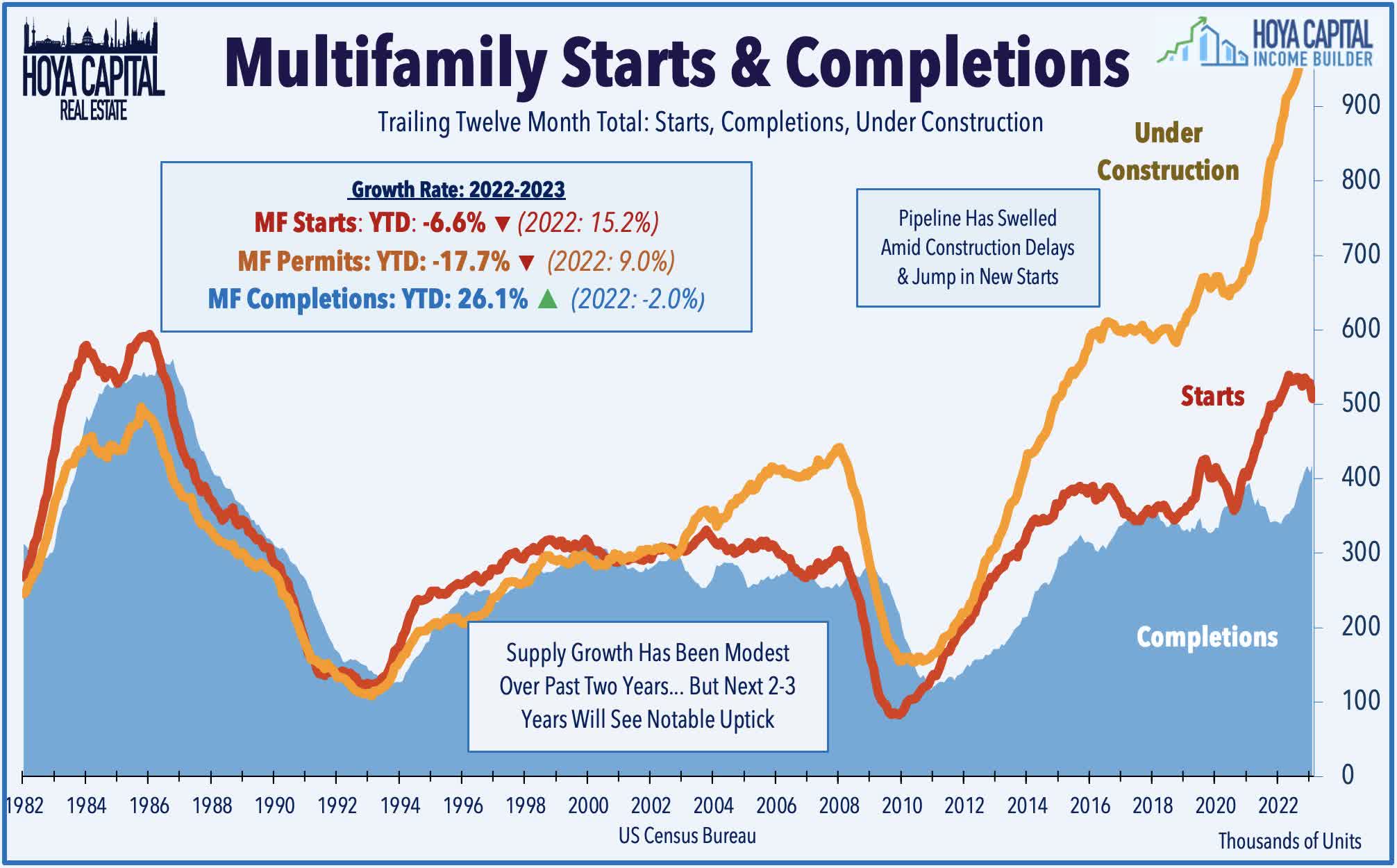

Housing Starts on multifamily projects plunged to the lowest level since the onset of the pandemic in August, continuing a trend of moderating construction activity amid a surge in financing costs and a general softening of multifamily rent growth. While multifamily housing starts are now lower by 6.6% year-to-date compared with last year's period, the pipeline of in-process development remains historically large at 995k - down slightly from the record-high of 997k in July. More than 400k new apartments have been delivered over the past twelve months - the most since 1984 - including 288k so far in 2023 through August, which was 26% above the same period last year. Notably, multifamily rent growth has remained surprisingly firm despite the supply pressures. Recent data from Zillow shows relatively solid rent growth in recent months following a sharp cooldown in late 2022 and into early 2023. Month-over-month rent growth exceeded 0.5% for a third-straight month in July, which follows a period of eight-straight months below that level.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

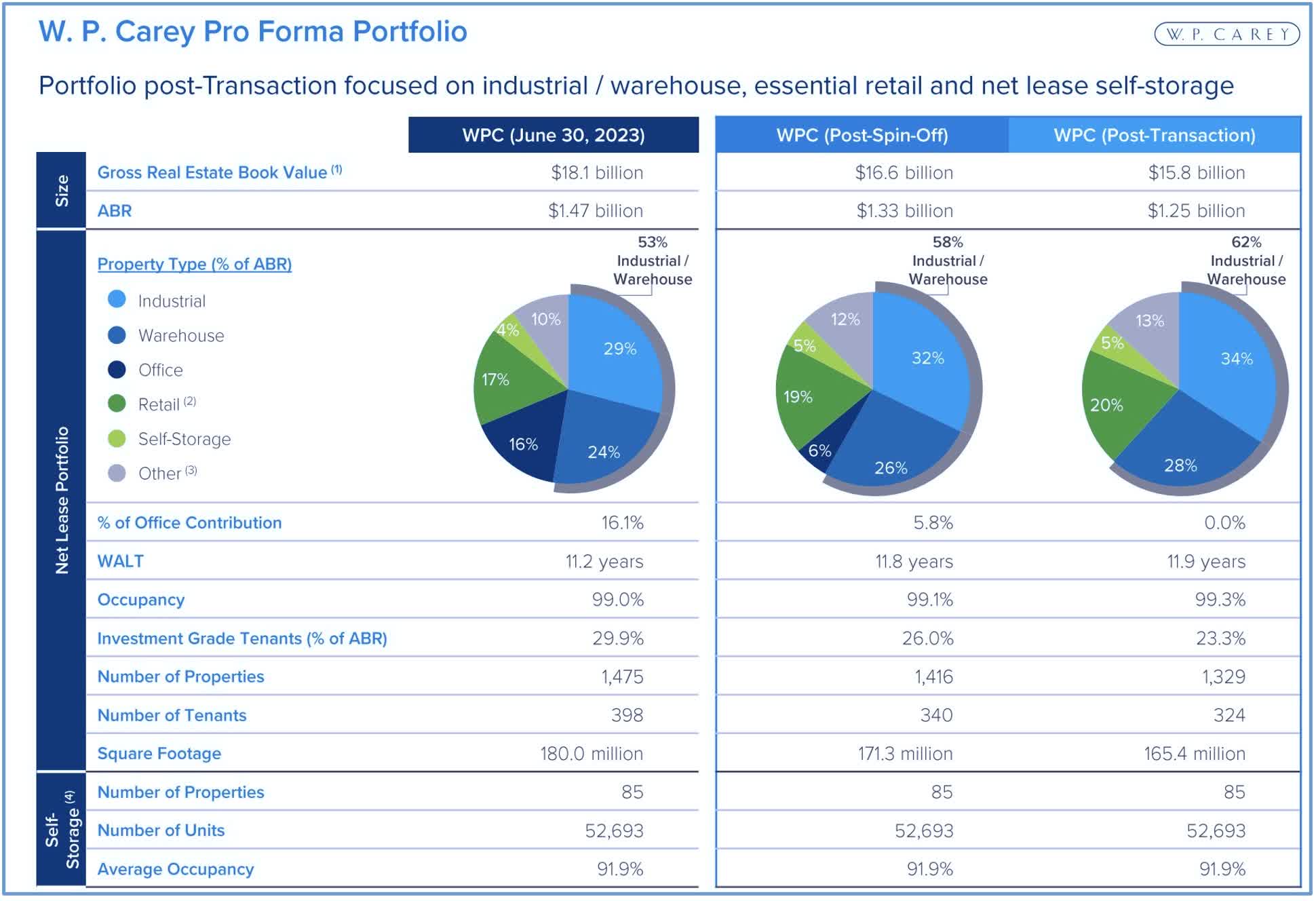

Net Lease : Darned if you do, darned if you don't. W.P. Carey ( WPC ) dipped 10% this week after it announced a strategic plan to sell its office assets - which comprise roughly 16% of its portfolio - aimed at "driving a re-rating" of WPC's stock price, which has traded at discounted valuations to similar-sized net lease and industrial REIT peers. Described by the company as a "rip off the band-aid" approach, the strategy entails a spin-off of 59 office properties into a new REIT - Net Lease Office Properties ("NLOP") that will be completed by the end of next month - and a sale of 87 remaining European office properties, which it expects to complete by early 2024. WPC notes that the office exit is "viewed as a credit positive by both S&P and Moody's" as proceeds will be used largely to repay existing variable-rate debt. WPC lowered its full-year AFFO guidance to $5.24/share at the midpoint - down from its prior outlook of $5.35 - and introduced plans to "reset" its dividend policy, "targeting an AFFO payout ratio of 70%-75%." This policy would imply an 11% dividend cut to $3.80/share based on current AFFO guidance, but WPC did not provide forward guidance for post-transaction AFFO levels. Post-transaction, roughly two-thirds of WPC's portfolio will be industrial net lease assets, with the bulk of the remainder in net lease retail and self-storage. Industrial REITs trade with a current Price-to-FFO of around 20x, while WPC trades at 11x P/FFO and similar-sized net lease REITs trade with a P/FFO of roughly 13x.

{kind=link}

Upon completion of the spin-off, WPC stockholders will own shares of Net Lease Office Properties via a pro rata special distribution, which is expected to be taxable for U.S. federal income tax purposes. Met by confusion from analysts given WPC's relatively solid operating performance in recent quarters - including sector-leading same-store NOI growth - WPC indicated that NLOP would effectively function as a liquidation company with a strategy "focused on realizing value through the strategic asset management and disposition of its assets." The 87M square foot portfolio - comprised primarily of Class B and C properties located in secondary and tertiary markets - has an average occupancy rate of 97.1% with a Weighted Average Lease Term ("WALT") of 5.7 years. NLOP will be capitalized with $169M of existing mortgage debt and a new $455 million debt financing package, with approximately $350 million of net proceeds from the new financing to be transferred to WPC. A comparable office spin-off by a large net lease REIT - Realty Income's ( O ) spin-off of Orion Office ( ONL ) - has been poorly received by investors since its 2021 IPO, significantly underperforming its office peers during this time. Orion trades with a P/FFO of under 5x.

{kind=link}

Office : Speaking of office REITs, Brandywine ( BDN ) dipped more than 12% this week after it reduced its quarterly dividend by 21% to $0.15/share (12.2% dividend yield), becoming the 10th office REIT this year to reduce its dividend and 27th REIT overall to lower its payout. BDN commented , “Our 2023 business plan remains on target with a continuation of strong leasing and operating metrics, however, current capital market conditions are such that further enhancing our already strong liquidity position makes sense." BDN hinted at a potential reduction in its second-quarter earnings call, noting "as we contemplate [the dividend], we still have work to do. And that work needs to be done against the backdrop of very challenging capital market environment... the variable right now is the pace of sales activity and the pricing in which some of those sales take place, and how some of these joint venture loan negotiations go." In our recent Office REIT report, we cautioned that because office REITs have not historically been a high-yielding sector, the attitude of treating dividends as "sacred" is not as evident in office REIT c-suites compared to historically yield-oriented sectors.

{kind=link}

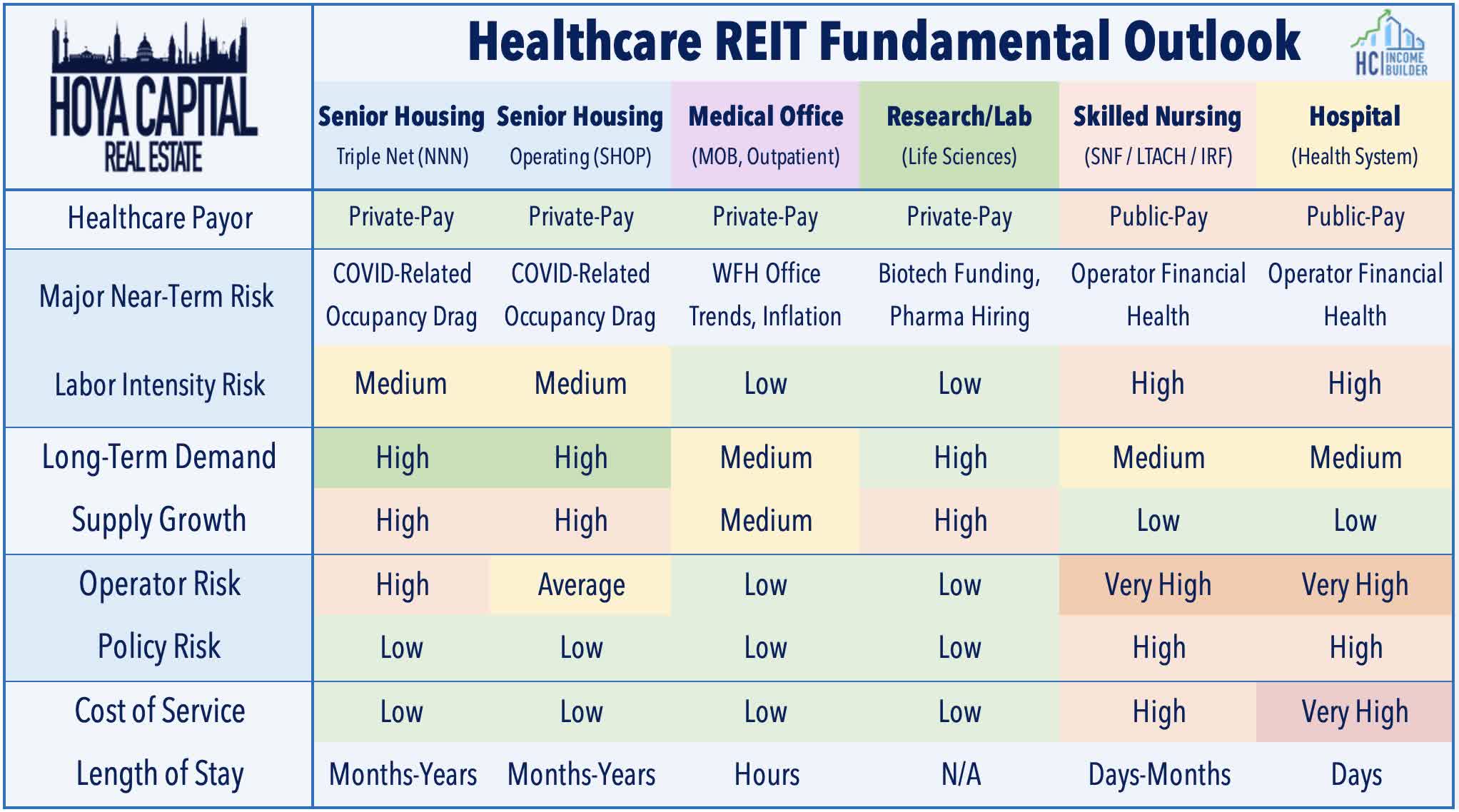

Healthcare : A handful of healthcare REITs were among the leaders this week following a ripple of analyst upgrades. Sabra Health Care ( SBRA ) rallied more than 4% after Jefferies upgraded the skilled nursing facility ("SNF") REIT citing, "significant upside embedded" in its senior housing operating portfolio and a "de-risking" of its triple-net portfolio. CareTrust ( CTRE ) was also among the best-performers after Raymond James upgraded the SNF-focused REIT, commenting that "REITs with smaller asset basses, strong balance sheets... and favorable cost of capital can be powerful recipes for robust earnings, NAV, and dividend growth." This week, we published Healthcare REITs: Recovery and Relapse , noting that Senior Housing has emerged as a leader in recent quarters as the long-awaited post-pandemic occupancy recovery is finally taking hold, but other sub-sectors have regressed of late amid a combination of macro and sector-specific headwinds. Skyrocketing labor costs from the reliance on third-party nursing agencies to plug staffing gaps have been the most pressing issue, but recent data suggest that the pressures may be easing ever so slightly.

{kind=link}

Cannabis : NewLake Capital Partners ( OTCQX:NLCP ) was among the top-performer this week after it maintained its quarterly dividend at $0.39/share (11.2% dividend yield) and announced an augmented share repurchase program. NLCP noted that its board authorized another $10M increase to its share repurchase program after it utilized $9.3M of the original $10M authorization. Cannabis REITs - led by Innovative Industrial ( IIPR ) - have rebounded this month as the cannabis industry cheered some long-awaited indications of progress toward Federal marijuana legalization. Following years of sluggish progress that some critics have characterized as "broken promises" by elected officials, the U.S. Department of Health and Human Services is officially recommending that marijuana be moved from Schedule I to Schedule III under federal law following a scientific review, a move that industry participants see as an important step towards official legalization.

{kind=link}

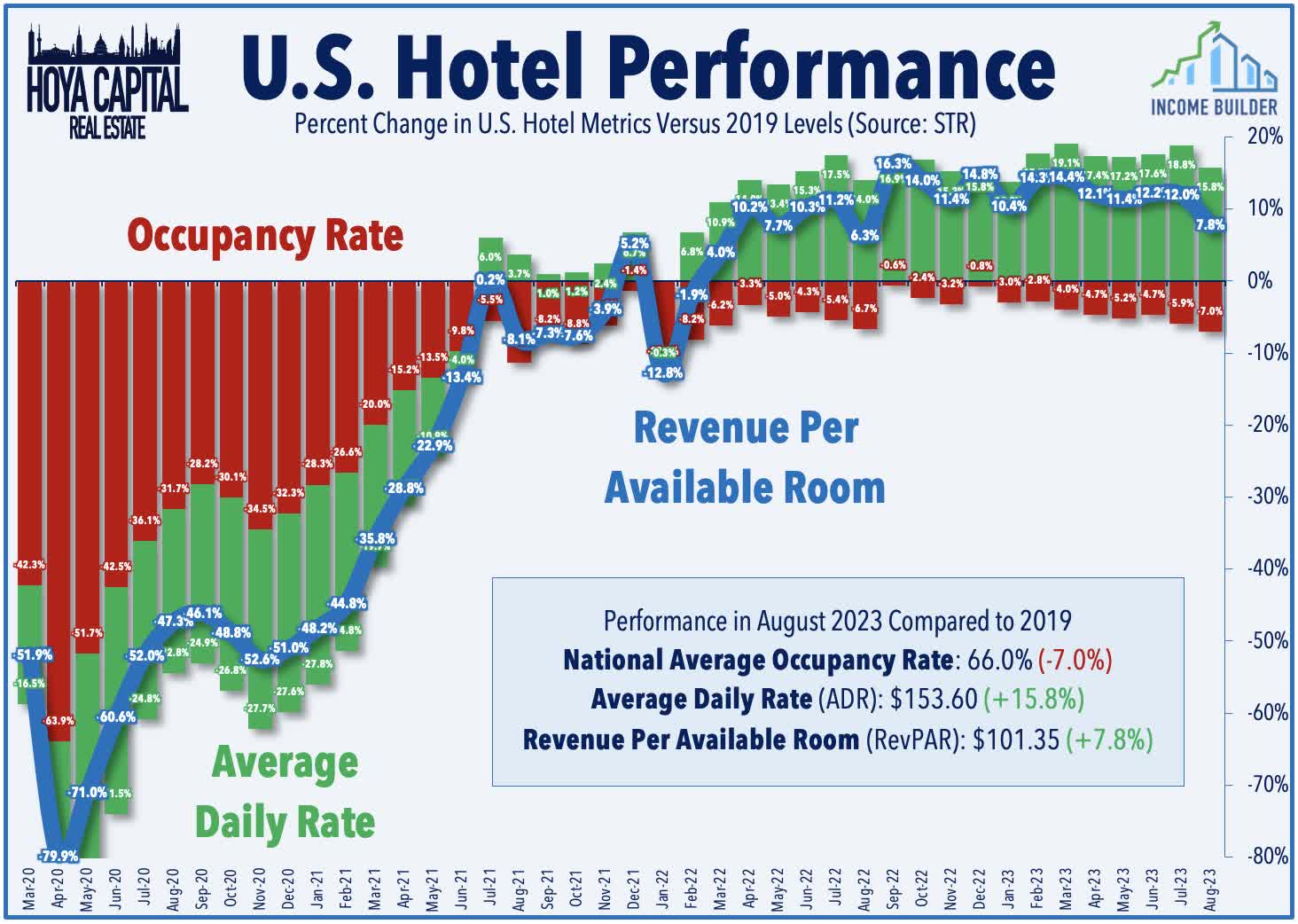

Hotels : Following two strong weeks, hotel REITs were among the harder-hit REIT sectors this week with average declines of over 5%. Pebblebrook ( PEB ) dipped 9% after it provided a business update in which it reported a modest demand impact from Tropical Storm Hilary and Hurricane Idalia estimated at $3.5M, but its Q3 operating and financial results remain in line with expectations , citing offsetting strength in its urban segment. PEB also reported that it refinanced its Margaritaville Hollywood Resort with a $140M three-year term loan at an effective fixed rate of 7.0%. Summit Hotels ( INN ), meanwhile, announced that it refinanced its $200M floating rate credit facility - maintaining pricing at SOFR+215 - and now has no material debt maturities through 2024. INN noted that 80% of its debt has a fixed interest rate after giving effect to interest rate derivative agreements. STR reported this week that Revenue Per Available Room ("RevPAR") RevPAR was roughly 8% above 2019-levels in August, as a 16% relative increase in Average Daily Rates ("ADR") has offset a 7% drag in occupancy levels. Recent TSA Checkpoint data has been quite solid in recent weeks despite the uptick in fuel prices. Driven by a very strong Labor Day, domestic throughout averaged 103% of pre-pandemic levels in August - a new post-pandemic record - and has averaged 104% of pre-pandemic levels thus far in September.

{kind=link}

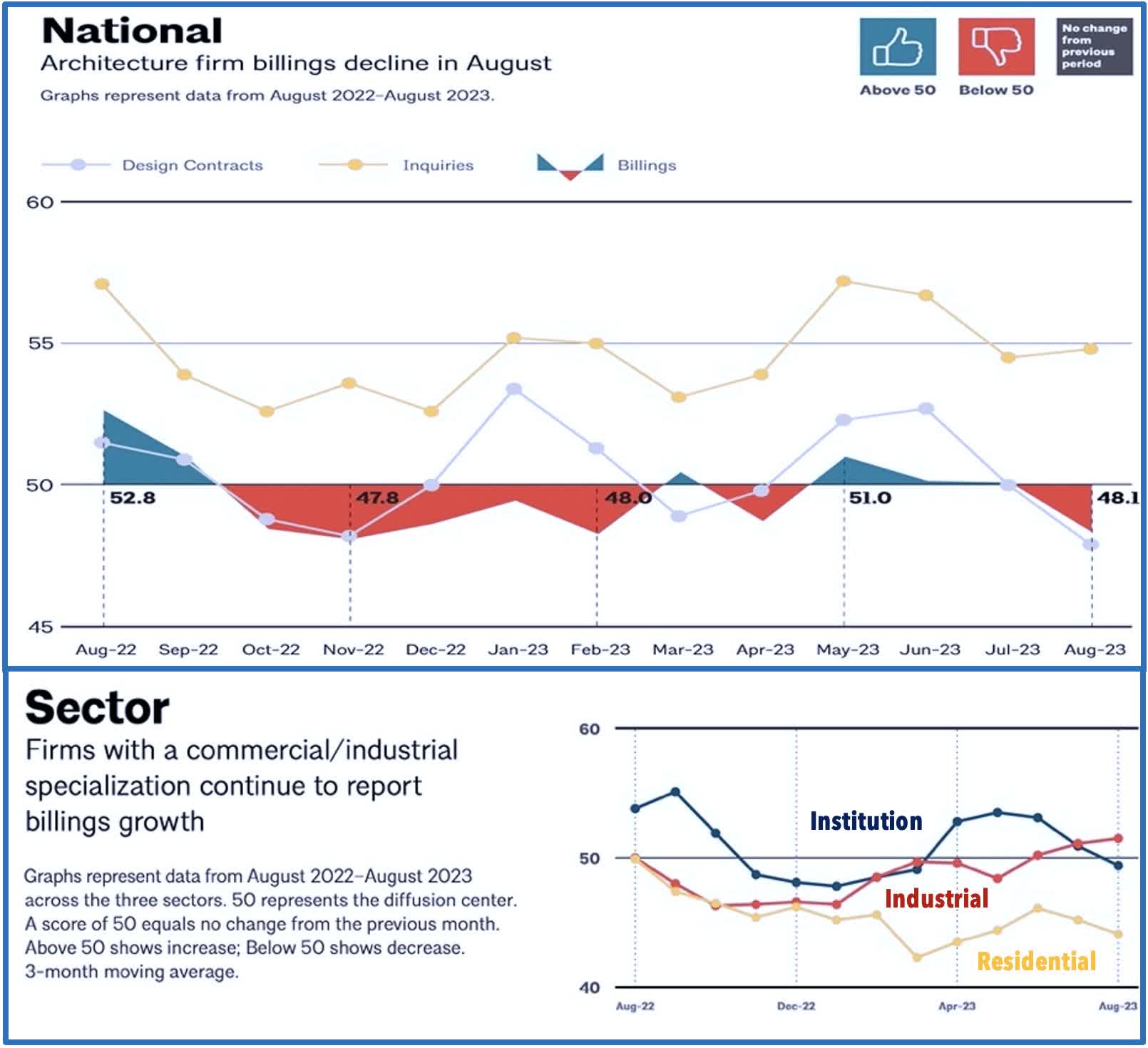

Apartments : A closely-watched leading indicator of commercial real estate development and supply growth, data this week via the AIA/Deltek Architecture Billings Index ("ABI") showed "sluggish" demand for architecture services in August, particularly for multifamily projects, which have now been negative for thirteen consecutive months in the ABI benchmark. The overall ABI index declined to 48.1, which was the lowest since November 2022. (Any score below 50.0 indicates decreasing business conditions.) This period of relative weakness follows several quarters of robust growth in 2021 and 2022. Firms with a commercial/industrial specialization, however, reported billings growth for the third month in a row in August, offsetting weakness in the residential and "institutional" category. Of note, architecture billings declined for the eleventh consecutive month at firms located in the West, while billings remained essentially flat in the South and Northeast.

{kind=link}

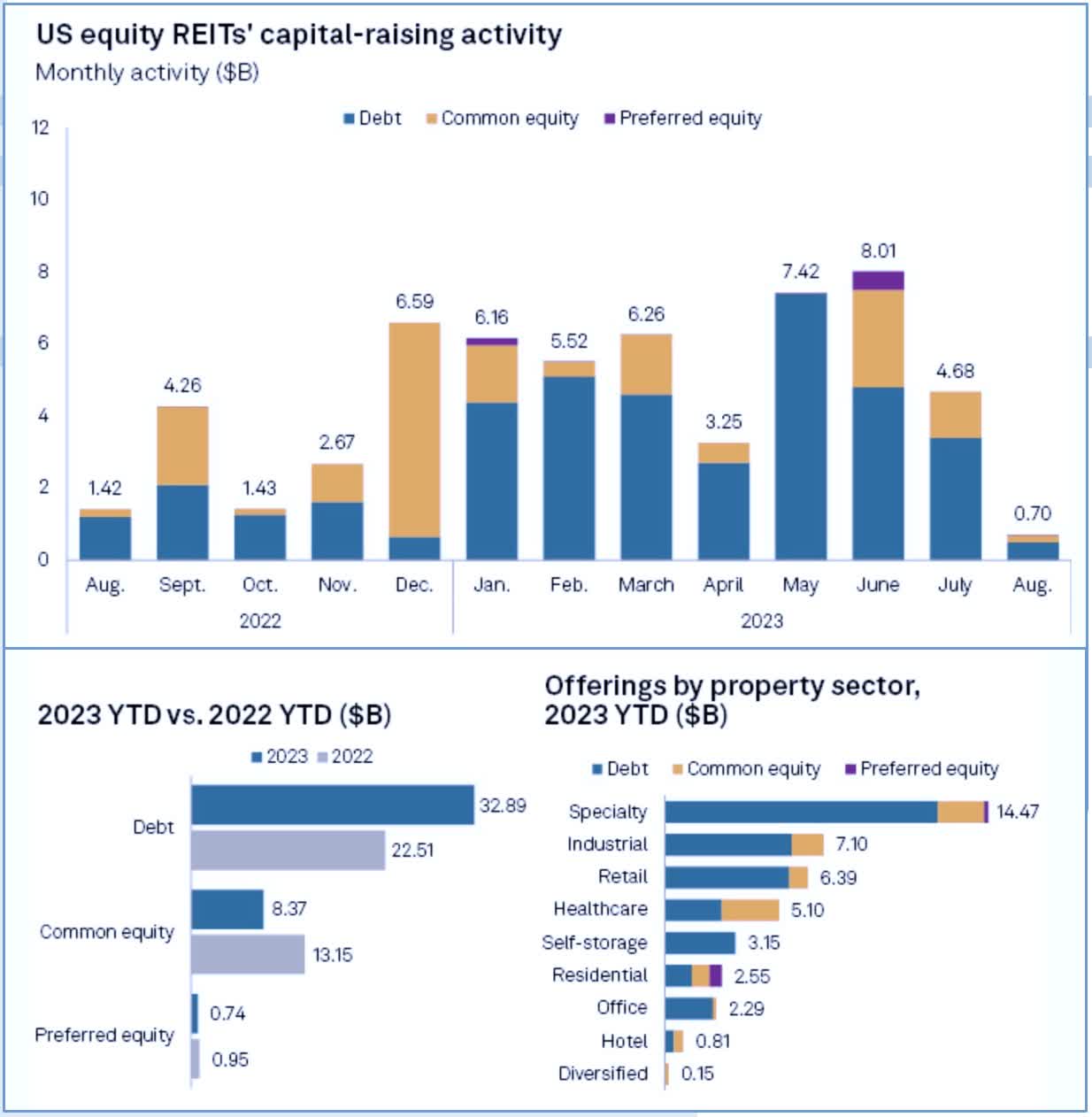

S&P reported this week that REIT capital raising activity slowed significantly in August after a relatively strong three months of activity from May through July. REITs collectively raised $702.3 million in new capital during August - an 85% decline from the $4.68 billion collected in July and 50% below August 2022. Of the total, $500M came through debt offerings. Common equity offerings accounted for $194.7M, while the remaining $7.6M was obtained through preferred equity offerings. The offerings in August brought the year-to-date total to $42 billion, 14.7% higher than the capital raised during the same period in 2022. REITs were again quiet on the capital-raising front this week. Office Properties Income ( OPI ) announced that it refinanced two mortgage loans totaling $69.2M, bringing its year-to-date refinancing total to $177M. It was also a quiet week on the credit ratings-front with no major upgrades or downgrades. Fitch Ratings affirmed Global Net Lease's ( GNL ) credit ratings, including its “BB+” issuer default rating with a stable outlook.

{kind=link}

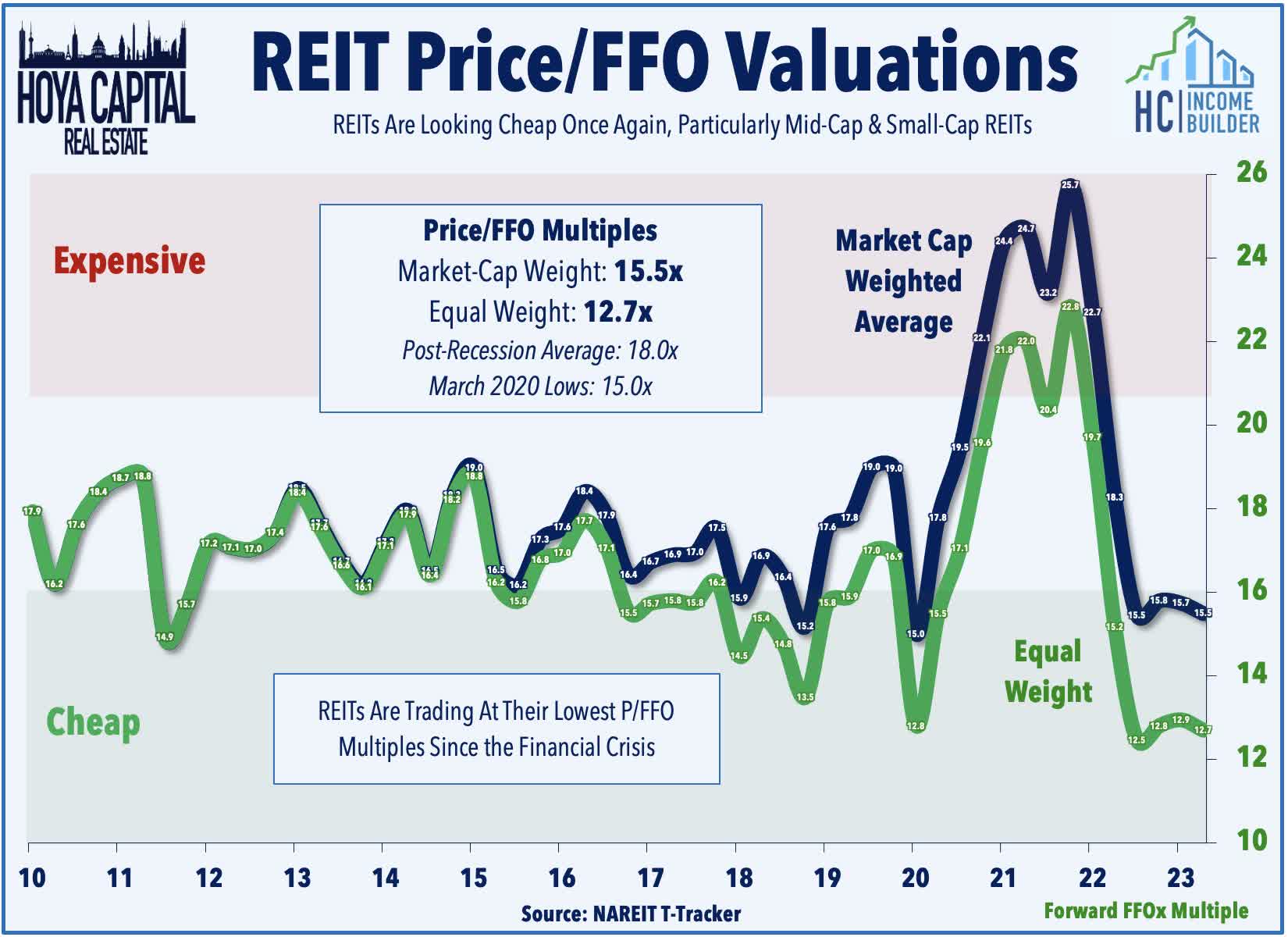

Earlier this month, we published REITs Are Historically Cheap . Commercial and residential real estate markets remain an easy transmission mechanism - or "punching bag" - of the Federal Reserve's historically swift monetary tightening cycle. The business models of many private equity funds and non-traded REITs were simply not designed for a period of sustained 5%+ benchmark rates or double-digit declines in property values. Private market players and non-traded real estate platforms were willing to take on more leverage and finance operations with short-term and variable-rate debt - a strategy that worked well in a near-zero rate environment but quickly crumbles when financing costs double or triple in a matter of months. "Hope" is the only strategy for some highly-levered property owners amid a dearth of buying interest and dwindling refinancing options. Pockets of distress remain almost entirely debt-driven, however, as property-level fundamentals remain solid across most property sectors. Conditions are aligning in an ideal manner for low-levered entities with access to "nimble" equity capital - conditions that maximize the true competitive advantage of the public REIT model, which these entities have been unable to exploit in the "lower forever" rate environment.

{kind=link}

Mortgage REIT Week In Review

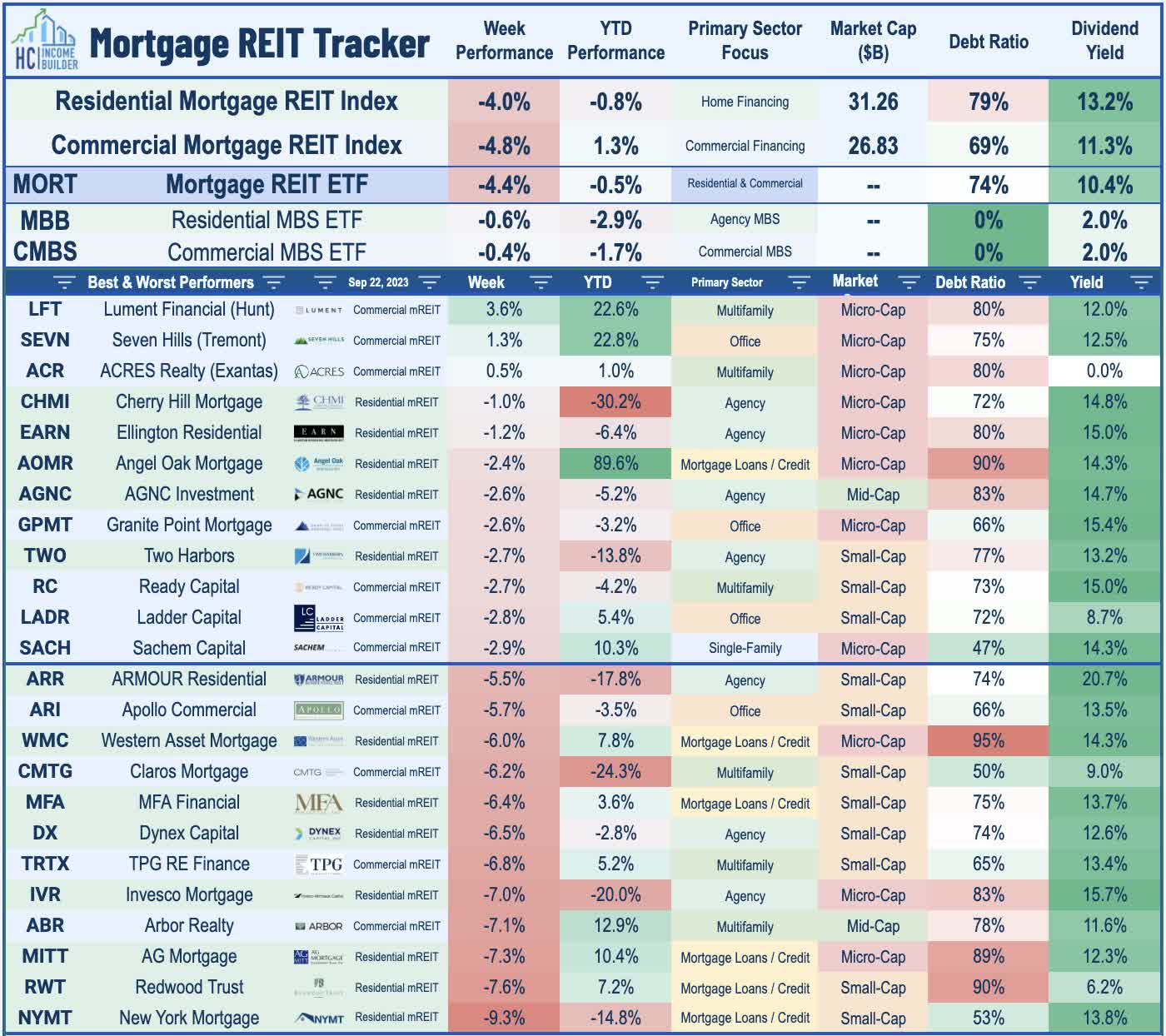

Mortgage REITs were also under pressure this week amid the surge in interest rates, with the iShares Mortgage REIT ETF ( REM ) dipping more than 4%. Small-cap Lument Finance ( LFT ) - which raised its dividend in the prior week - was one of just three mREITs in positive territory on the week. Claros Mortgage ( CMTG ) dipped 6% this week after it announced last Friday afternoon that it would reduce its quarterly dividend by 32% by $0.25/share (8.7% dividend yield). Ready Capital ( RC ) was among the better-performers, however, despite also announcing a dividend cut last Friday, reducing its quarterly dividend by 10% to $0.36/share (13.5% dividend yield). Each of the other mREITs that declared dividends over the past week held their payouts steady at current levels. PennyMac Mortgage ( PMT ) was among the better-performers this week after it announced that it will list a new exchange-listed "baby bond" - a five-year senior note that will be listed on the NYSE under the symbol “PMTU.” The company intends to use the net proceeds, in part, to refinance its 5.50% exchangeable notes due 2024.

{kind=link}

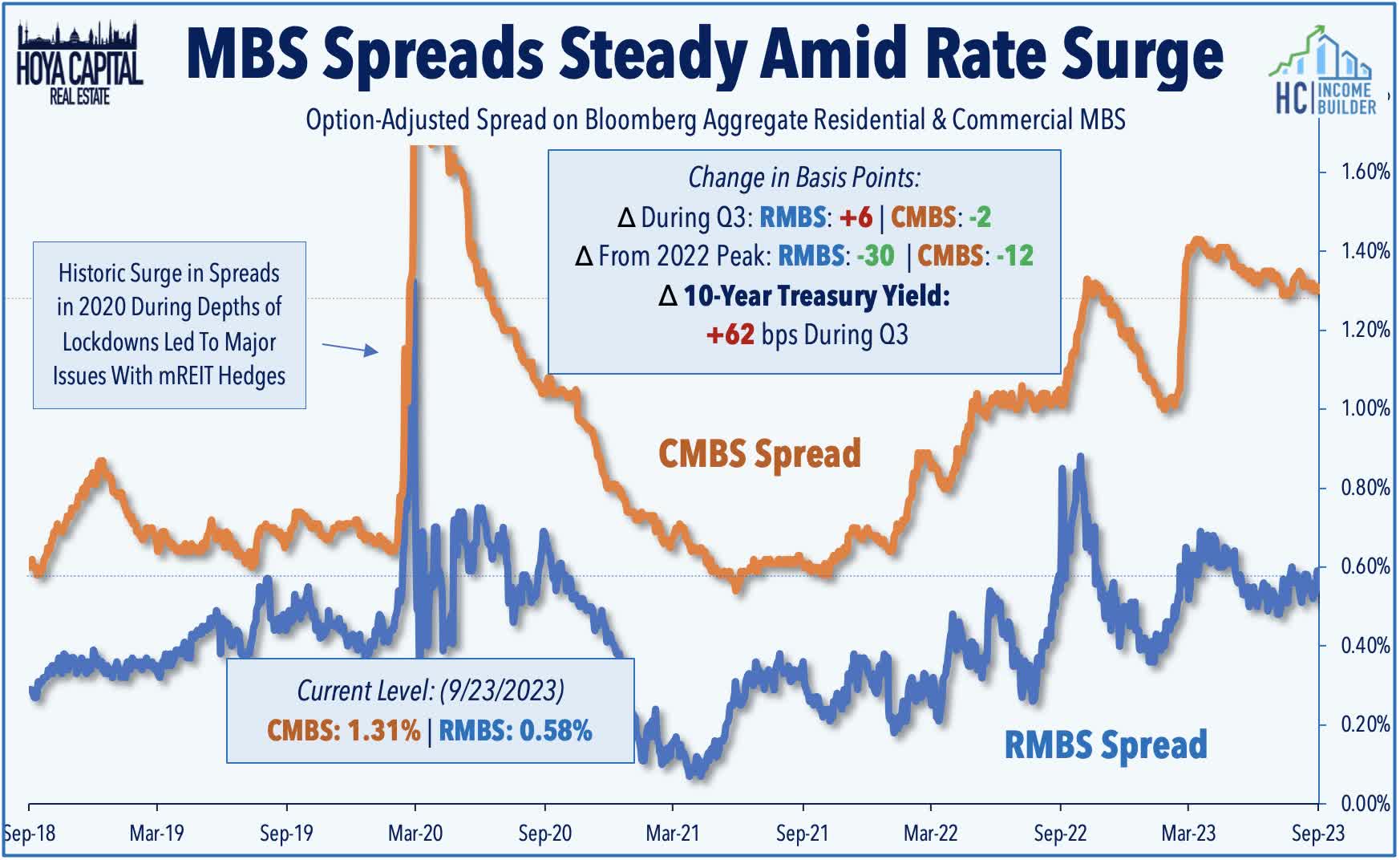

Recovering from a sharp sell-off in the wake of the Silicon Valley Bank collapse, Mortgage REITs have solidly outperformed their Equity REIT peers this year as turmoil across interest rate markets has calmed. Distress in the commercial and residential real estate markets has been more isolated than the magazine covers would suggest. Outside of urban office properties, default rates remain near pre-pandemic lows. Dividend cuts have come as a 'ripple' rather than a 'wave' with 12 of 40 mREITs reducing their dividends this year, but industry-wide payouts are only down about 8% YTD versus 60% in 2020. The squeeze on highly-levered private market portfolios is still in the early innings, however, but an orderly unwind remains the base case. Spreads on mortgage-backed bonds ("MBS spreads") - an important input into Book Value models - have been roughly flat in Q3 for both RMBS and CMBS, but benchmark interest rates - the other critical input affecting Book Values - have increased significantly during this period.

{kind=link}

2023 Performance Recap & 2022 Review

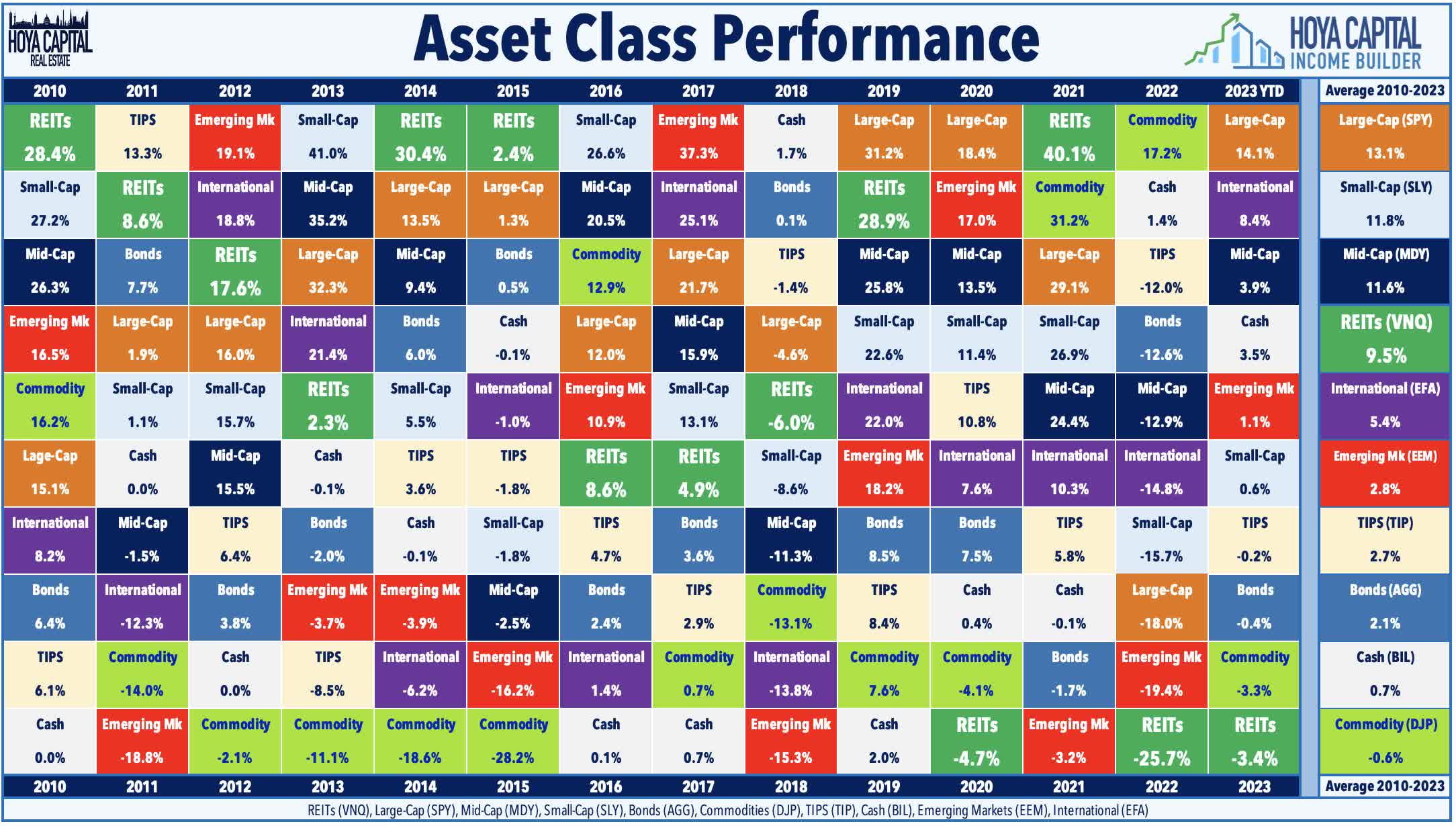

Approaching the end of the third quarter, the Equity REIT Index is lower by 6.1% on a price return basis for the year (-0.2% on a total return basis), while the Mortgage REIT Index is higher by 2.0% (+7.5% on a total return basis). This compares with the 12.5% gain on the S&P 500 and the 2.8% advance for the S&P Mid-Cap 400 . Within the real estate sector, 5-of-18 property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, Industrial, and Healthcare REITs, while Cannabis and Cell Tower REITs have lagged on the downside. At 4.44%, the 10-Year Treasury Yield has increased by 44 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - and now hovering at 15-year highs . The US bond market has stabilized following its worst year in history as the Bloomberg US Bond Index has produced total returns of -0.2% this year. WTI Crude Oil - perhaps the most important inflation input - is higher by 15% this year but remains roughly 15% below 2022 peaks.

{kind=link}

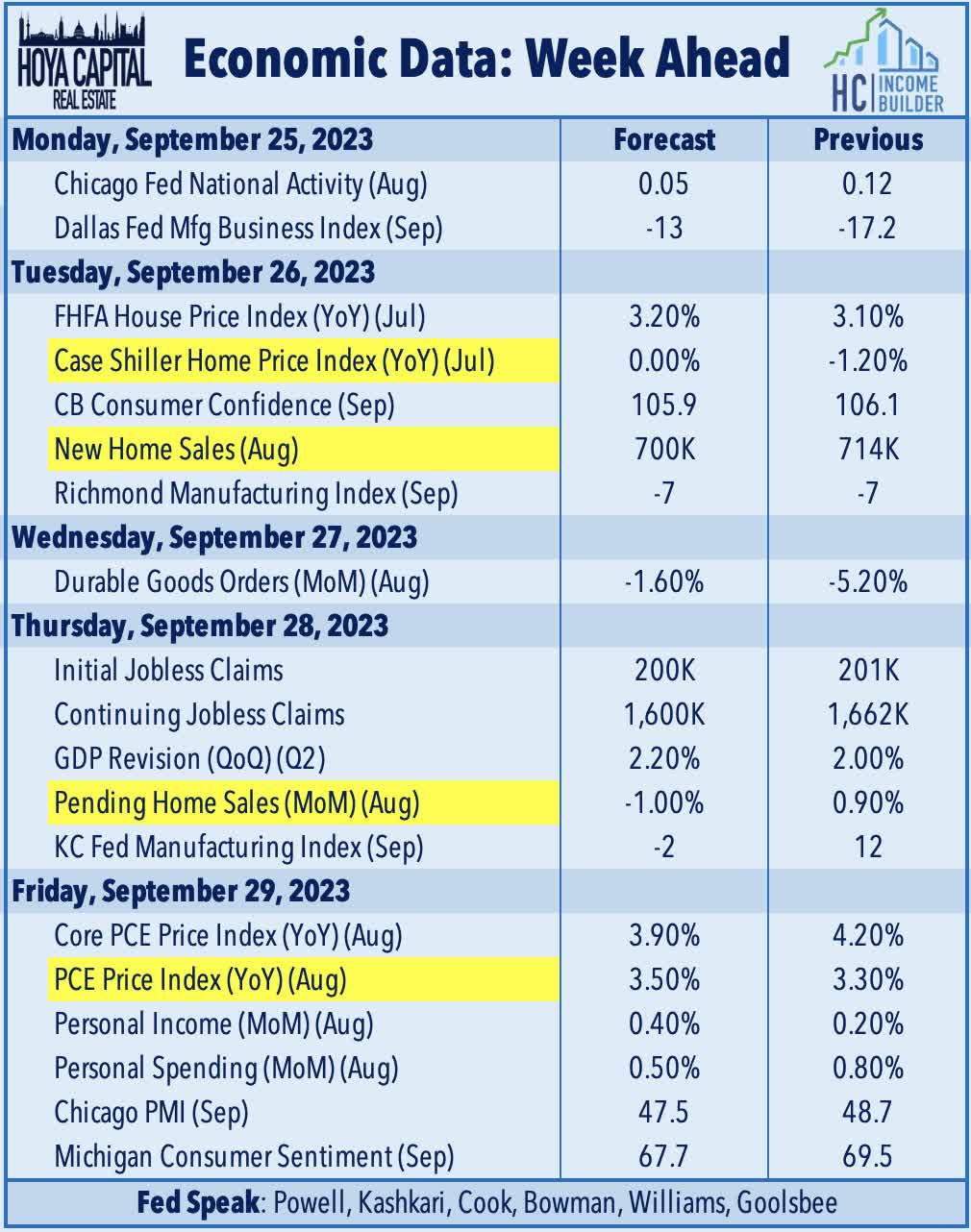

Economic Calendar In The Week Ahead

The state of the U.S. housing market remains in focus in the week ahead. We'll see New Home Sales data on Tuesday, which is expected to show an annualized sales rate of 700k in August - up from the 2022 lows of around 550k but well below the peak velocity of over a million units in late 2020. The largest single-family homebuilders have, so far, been able to cope with multi-decade-high mortgage rates by leveraging their platform's scale to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market. We'll also see home price data on Tuesday via the Case Shiller Home Price Index and Pending Home Sales data on Thursday. Historically low inventory levels have kept a floor on home values this year despite the surge in mortgage rates, and, while national home prices have been flat since last May, several markets have seen double-digit price declines in that time. The most closely-watched report of the week comes on Friday with the PCE Price Index - the Fed's preferred gauge of inflation - which is expected to show a year-over-year increase of 3.5% - up from last month but down sharply from the 7.0% rate seen a year ago.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Fed Says More Pain Needed