REIT - Fed Says 'Not So Fast'

2023-11-13 09:00:00 ET

Summary

- Following the best week of the year, U.S. equity markets were mixed this week as interest rates rebounded from the prior week's plunge after Fed officials pushed back on market optimism.

- Posting gains in nine out of ten sessions since dipping into "correction territory" at the end of October, the S&P 500 gained 1.4% on the week, but Mid-Caps and Small-Caps posted declines.

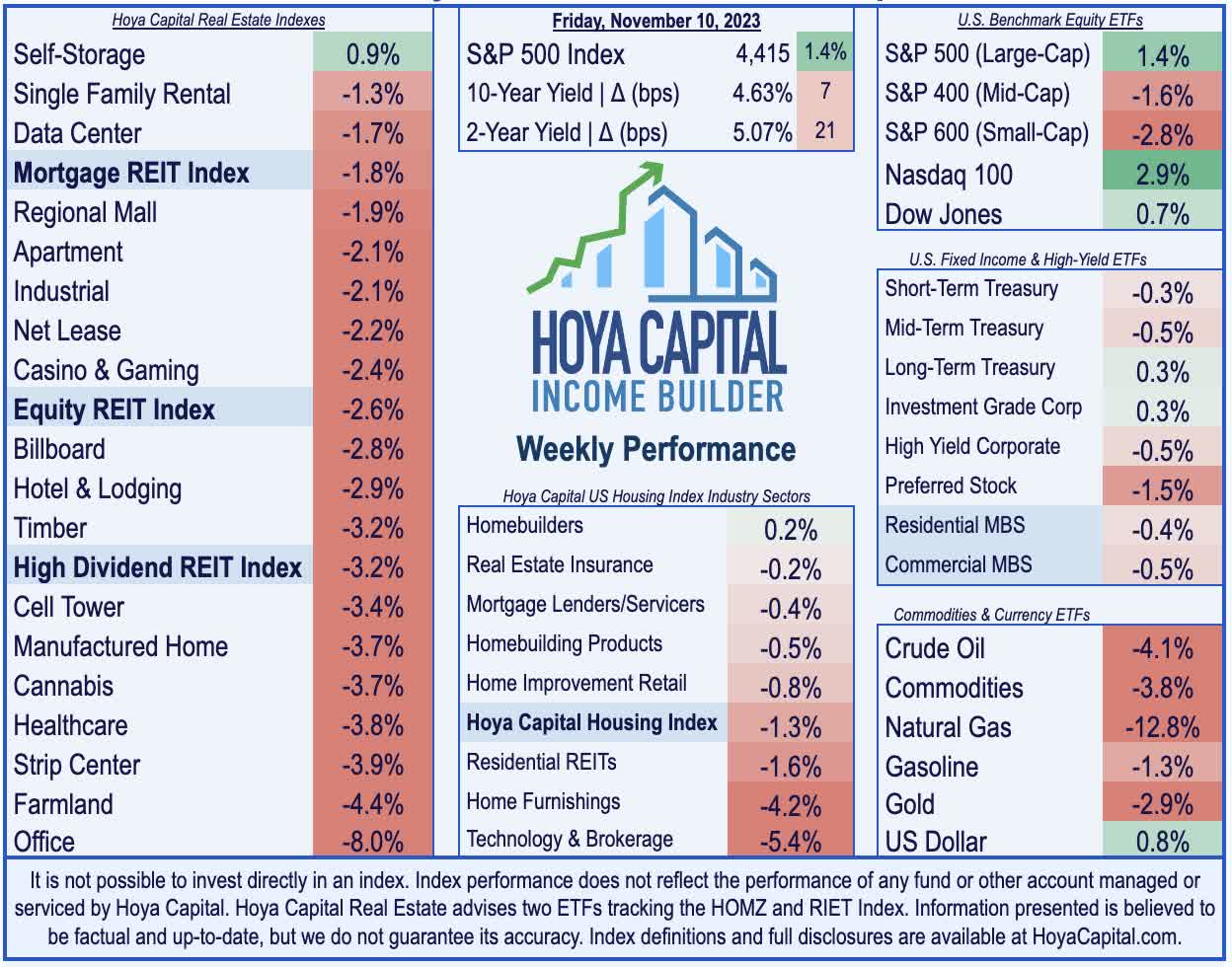

- Following their best week since 2020, REITs took a step back this week as upward pressure on benchmark interest rates offset a solid conclusion to a strong earnings season.

- Upside standouts this week included homebuilder DR Horton, storage REIT Extra Space Storage and retail REIT Tanger Outlets. Net Lease REIT Four Corners became the 72nd REIT to raise its dividend this year, while 30 REITs have reduced their dividends.

- Ahead of a critical slate of inflation data next week, data this week showed that consumer confidence fell for a fourth straight month in November, pressured by an uptick in consumer inflation expectations.

Real Estate Weekly Outlook

Following the best week of the year, U.S. equity markets were mixed this week as benchmark interest rates rebounded from the prior week's plunge after Fed officials pushed back on market optimism regarding a pending pivot towards less-hawkish monetary policy. Ahead of a critical slate of inflation data in the week ahead, Fed Chair Powell adopted a more hawkish tone in closely-watched commentary at an IMF event this week, cautioning that there remains a "long way to go” to return inflation to the Fed's 2% target, and warning about "head fakes" resulting from a potentially transitory dip in goods-related inflation.

{kind=link}

Hoya Capital

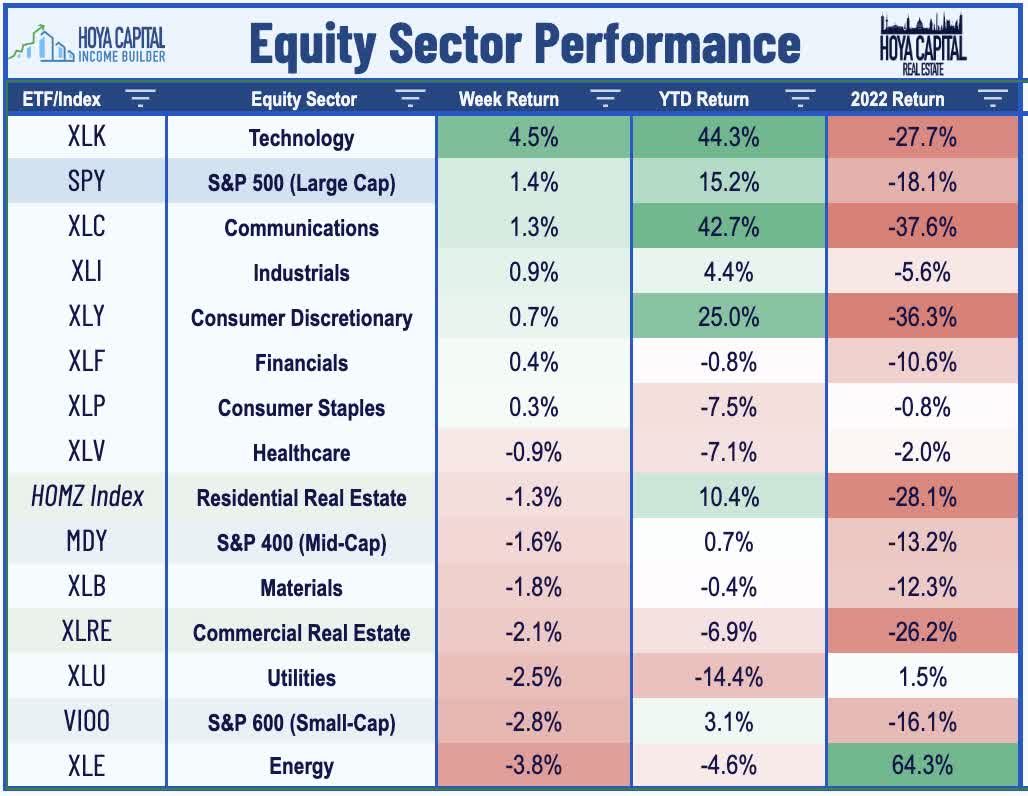

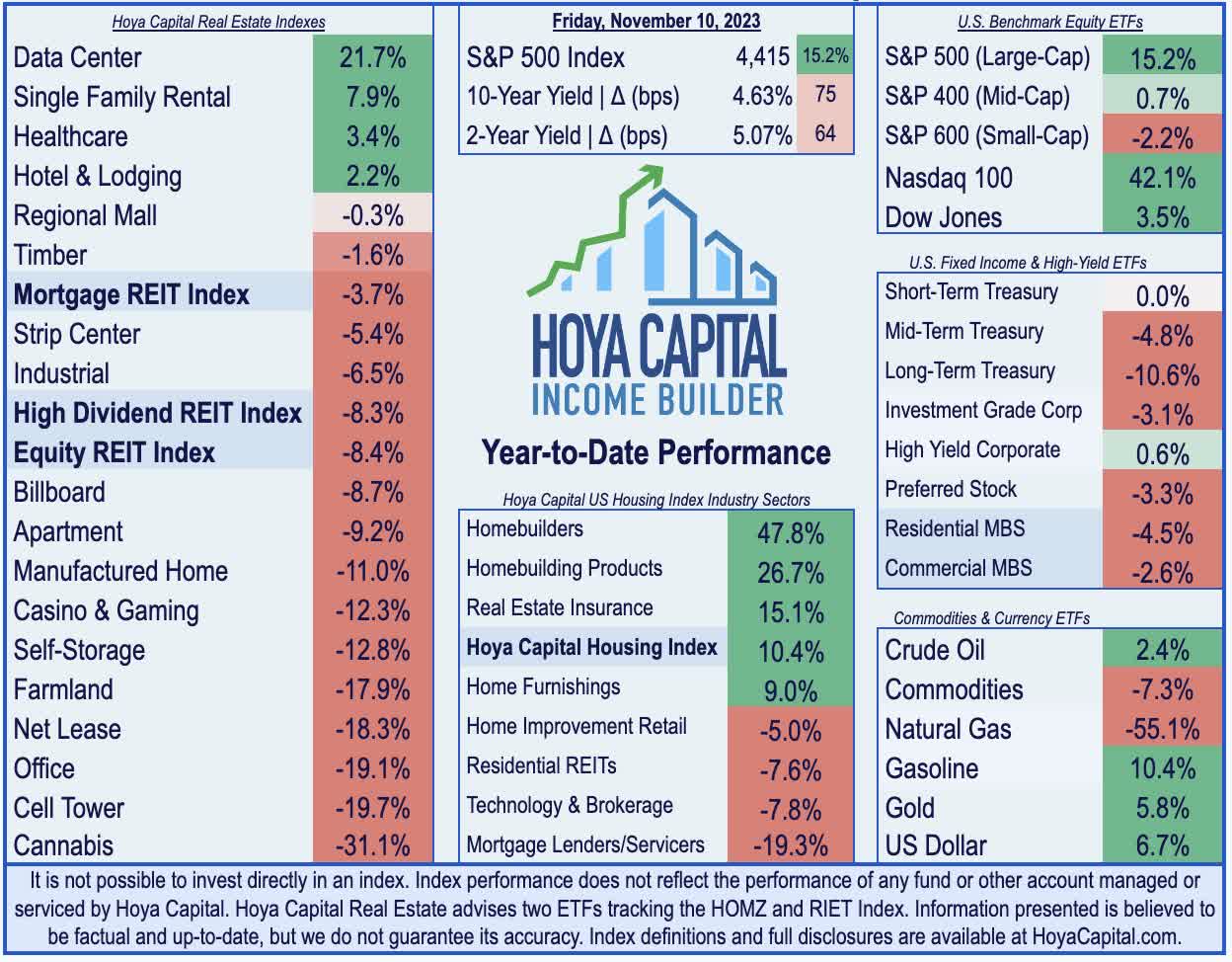

Posting gains in nine out of ten sessions since dipping into "correction territory" at the end of October, the S&P 500 gained 1.4% on the week, while the tech-heavy Nasdaq 100 posted gains of nearly 3%. Gains this week were notably top-heavy, however, as the Mid-Cap 400 declined 1.6%, while the Small-Cap 600 slid 2.8%. Following their best week since April 2020, real estate equities took a step back this week as upward pressure on benchmark interest rates offset a solid conclusion to a very strong earnings season. The Equity REIT Index declined 2.6% this week, with 17-of-18 property sectors in negative territory, while the Mortgage REIT Index slipped by 1.8%. Homebuilders finished modestly higher on surprisingly strong results from DR Horton - the nation's largest single-family homebuilder - which reported resilient demand despite the surge in mortgage rates to over 8%.

{kind=link}

Hoya Capital

Hawkish commentary from Fed officials tempered the bond market optimism following a dramatic rebound in the prior week sparked by downbeat employment data. After dipping to The 10-Year Treasury Yield briefly traded as low as 4.50% this week - the lowest since late September - but rebounded following Fed Chair Powell's commentary to close the week at 4.63% - up seven basis points from last week. The moves in the policy-sensitive 2-Year Treasury Yield were more significant, jumping 21 basis points on the week 5.07%. The US Dollar Index rebounded this week to the cusp of one-year highs. Energy prices - which were the driving force behind the reacceleration in inflationary pressures from June through mid-October - remained under notable pressure this week, with WTI Crude Oil dipping another 4% this week to $77/barrel - effectively erasing the summer resurgence and now 12% below its recent September peak. The CBOE Volatility Index - a measure of equity market volatility - posted its most significant two-week decline since 2020. Six of the eleven GICS equity sectors finished higher on the week as corporate earnings season wound down, led on the upside by Technology ( XLK ) stocks, while Energy ( XLE ) stocks remained under pressure.

{kind=link}

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

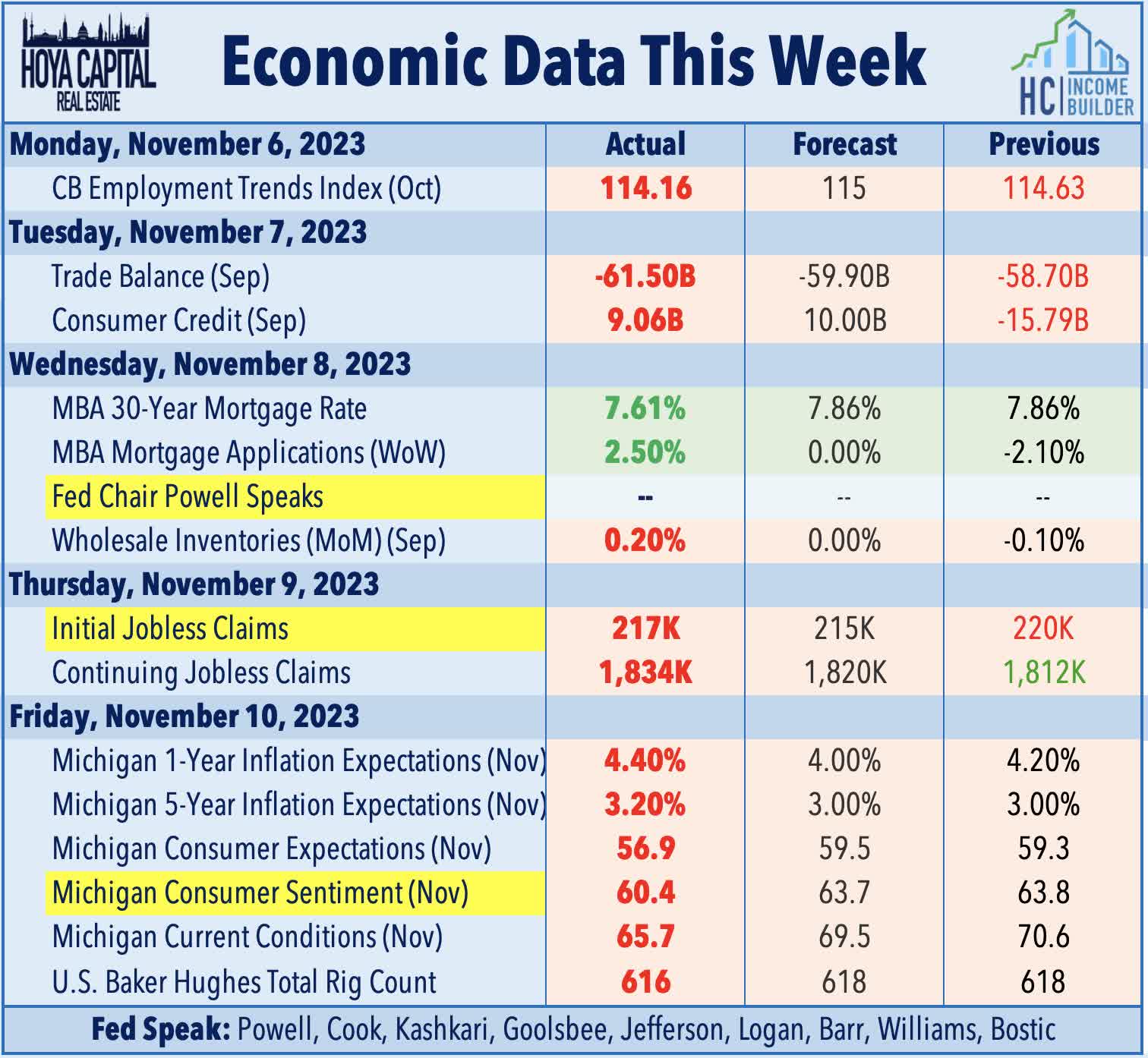

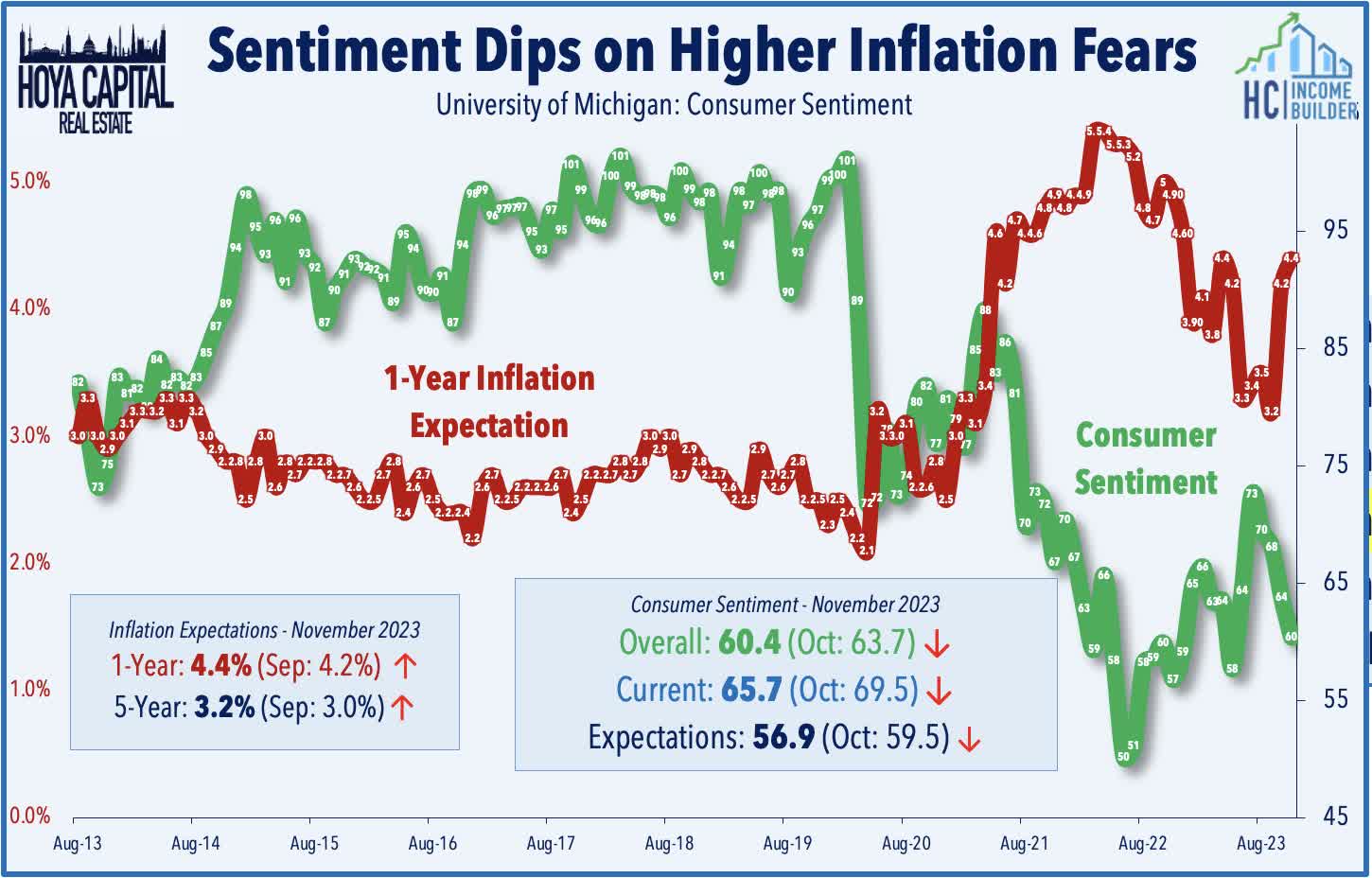

The economic calendar this past week was light, but there were several nuggets of notable data points. Fed data this week via the Senior Loan Officer Opinion Survey ("SLOOS") survey confirmed that lending standards have tightened considerably across most types of loans - with notably tight conditions in real estate loan availability - while loan demand continued to weaken in the third quarter. Elsewhere, Michigan Consumer Sentiment data this week showed that sentiment fell for a fourth straight month in November, pressured by an uptick in consumer inflation expectations. Likely reflecting a now-reversed jump in gasoline prices that peaked in October, one-year inflation expectations jumped to a seven-month high of 4.4%, while five-year expectations rose to 3.2% - the highest since March 2011. Of note, the survey showed that lower-income consumers and younger consumers exhibited the strongest declines in sentiment, but the rebound in stock markets last week was visible through a 10% jump in sentiment among stock investors.

{kind=link}

Hoya Capital

Equity REIT Week In Review

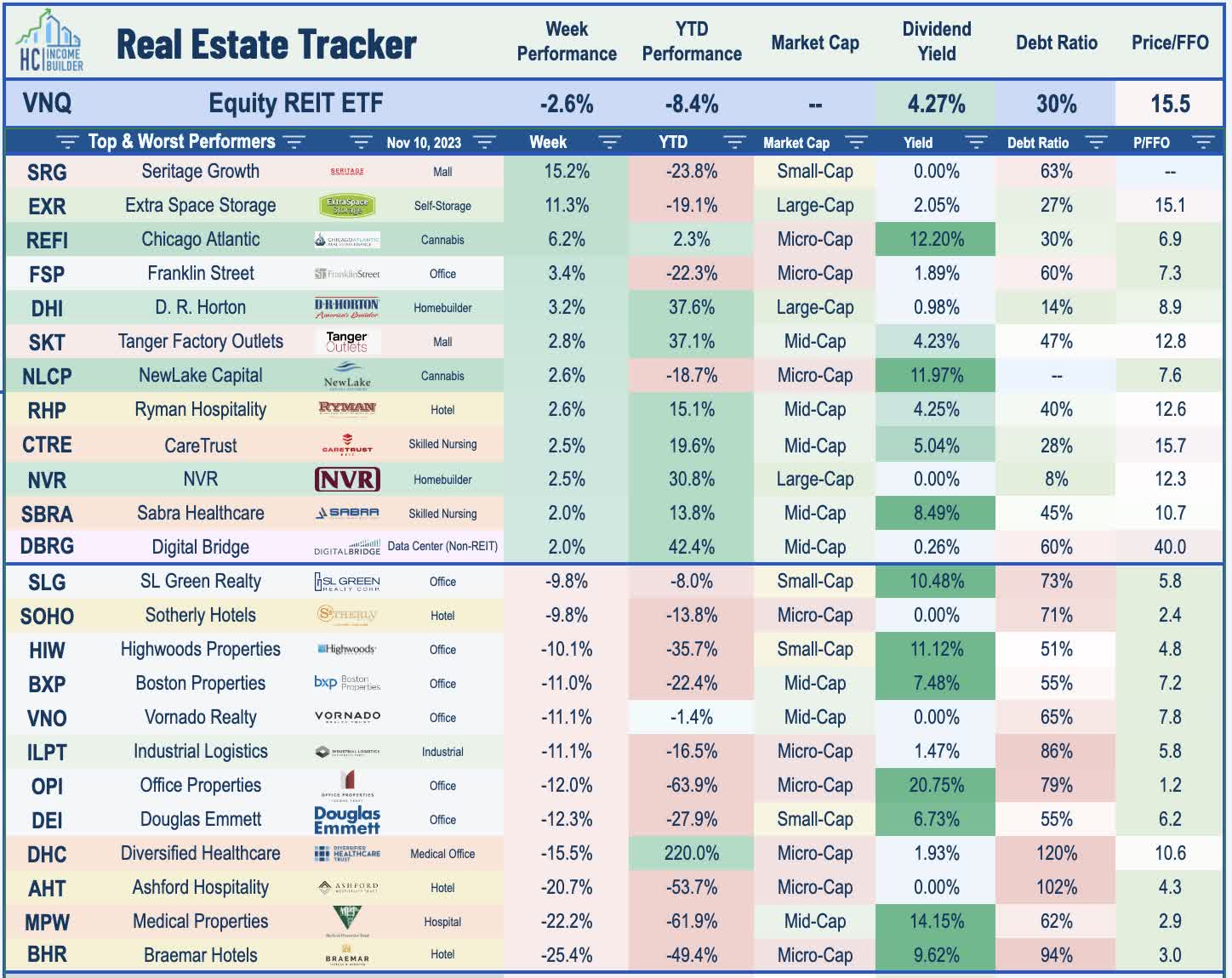

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

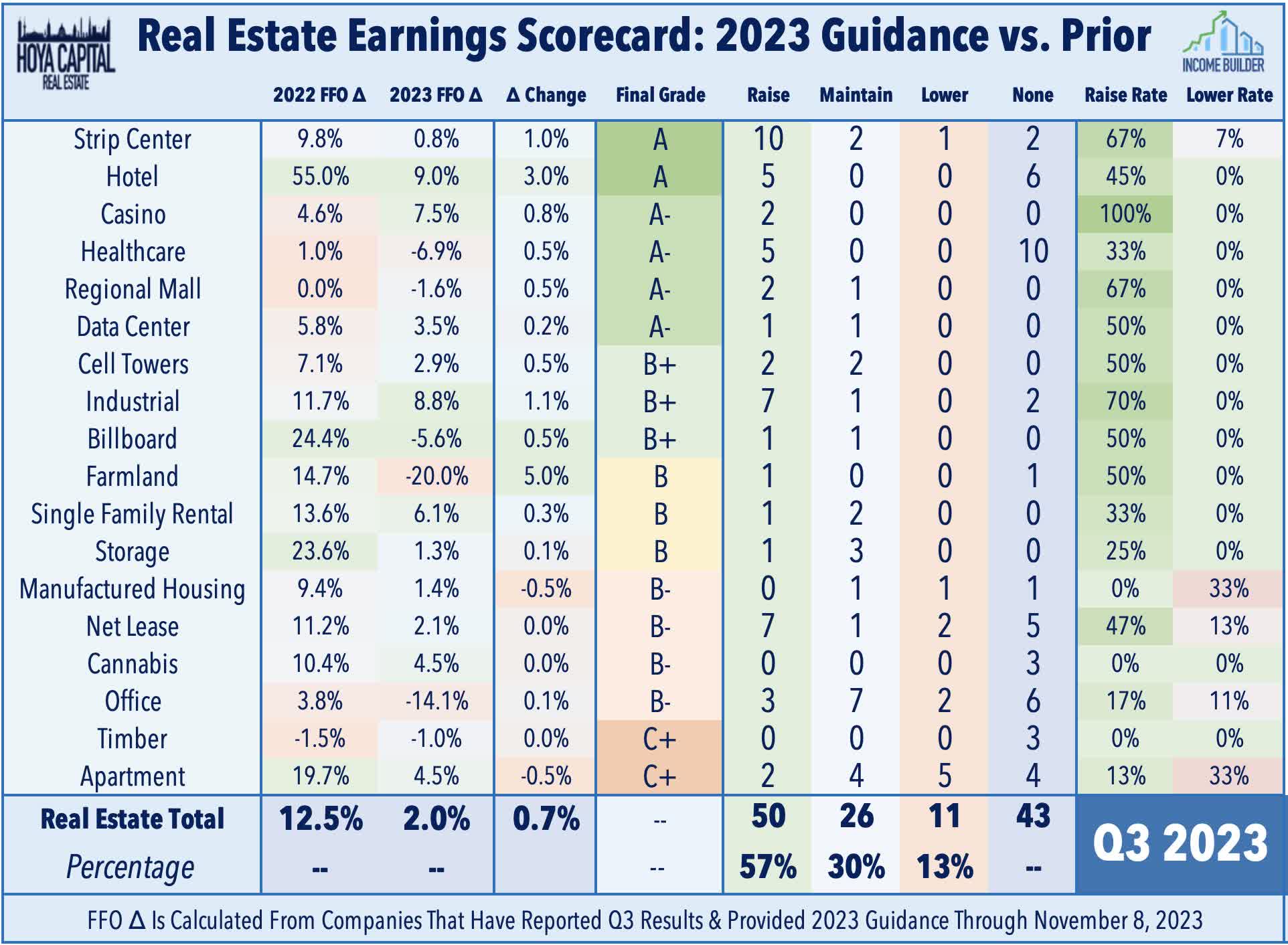

Real estate earnings season wrapped up this week with results from the final two dozen REITs. This week, we published Winners of REIT Earnings Season - Part 1 of our two-part earnings recap - with the Losers of Earnings Season to follow this weekend. We noted that beneath the "Rates Down, REITs Up" whipsaw effects, earnings results were considerably stronger than expected across most property sectors, particularly from retail, hotel, and technology REITs. Among the equity REITs that provided updated guidance, 82% increased their forecast, while only 18% lowered their full-year NOI outlook - a beat rate that significantly exceeded the S&P 500 and the best "beat rate" for REITs in over a year. As predicted, mergers and acquisitions were a major theme, with several small and mid-cap REITs being acquired by larger peers - a trend that we expect to continue into 2024. Resilient pricing power remained a common thread across most property sectors throughout earnings season - notably in data center, and retail REITs - while surprisingly solid demand in many of the most pro-cyclical sectors - notably hotel and billboard REITs - was a takeaway from the back-half of earnings season.

{kind=link}

Hoya Capital

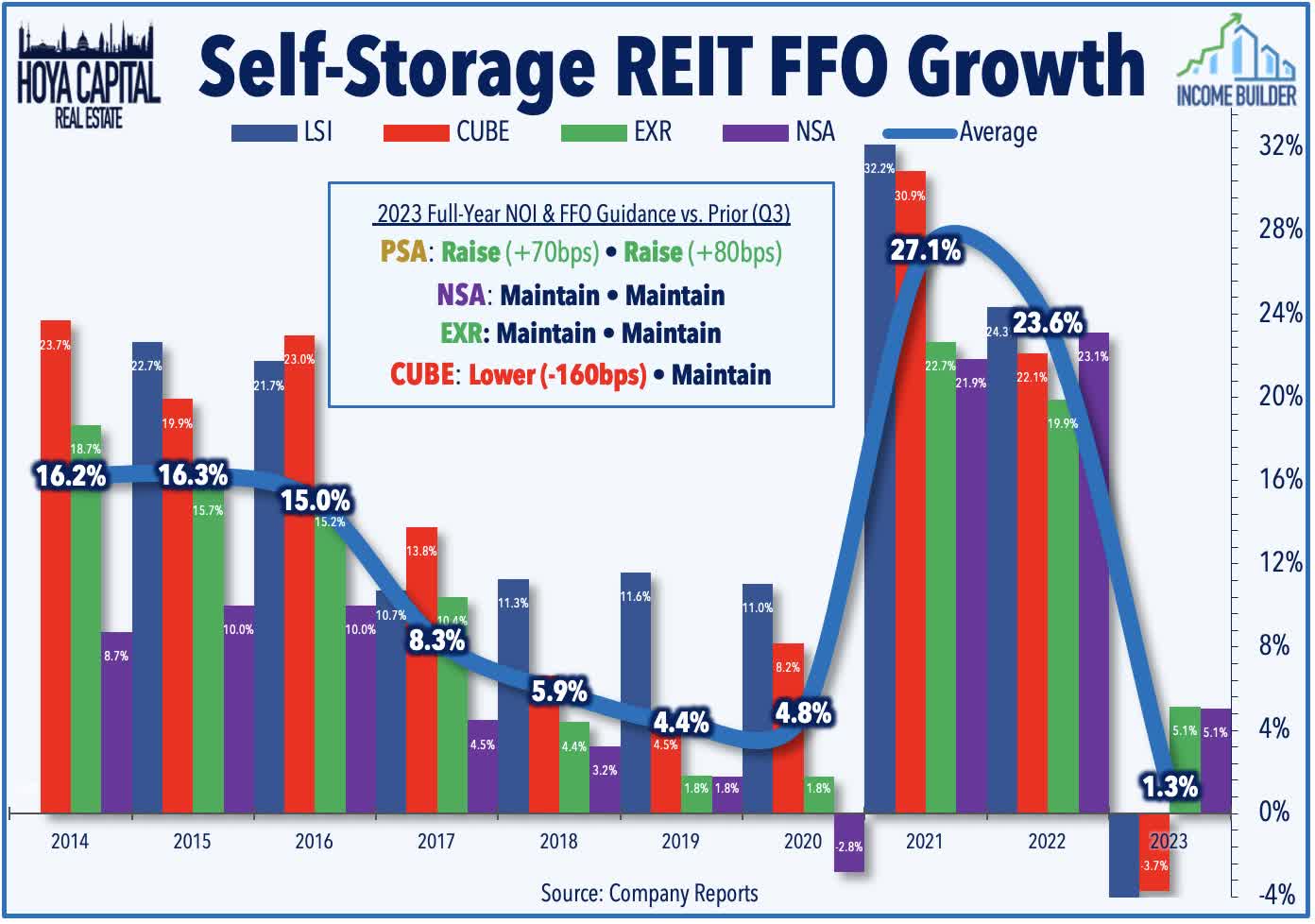

Storage : Beginning with the upside standouts this week, Extra Space ( EXR ) - which had been among the laggards this year on sluggish self-storage demand - surged more than 11% this week after reporting solid results and maintaining its full-year outlook. EXR noted rapid progress on its integration with Life Storage - which it acquired in July - and noted that it has reached its anticipated G&A expense savings run rate, and is on pace to reach its total synergies by next quarter. Demand trends for EXR - and across the storage sector - were generally stronger than feared in the third quarter despite the headwinds from sluggish housing turnover, with EXR recording an ending occupancy of 94.1% - down from 95.1% last year, but still above the average Q3 rate during the pre-pandemic period. EXR continues to expect its full-year FFO to decline 3.7% - a rather modest "normalization" following cumulative growth of over 60% in the preceding three years, and consistent with the trends observed across the sector. EXR also maintained its same-store NOI growth outlook at 2.75%, as a modest increase in its revenue target was offset by a similarly-sized uptick in its expense forecast.

{kind=link}

Hoya Capital

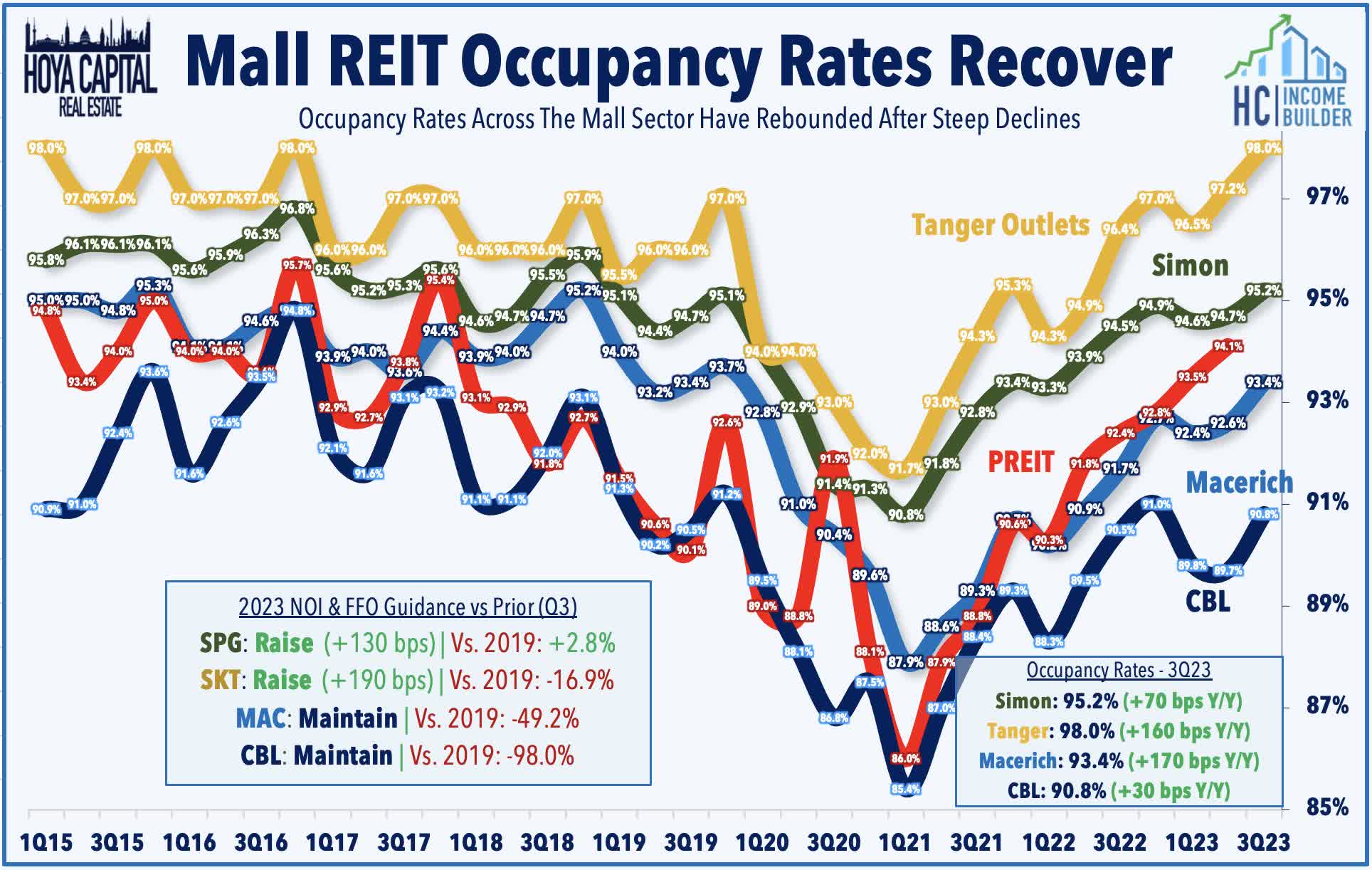

Mall : Retail REITs continued their impressive earnings season over the week. Tanger Factory Outlet ( SKT ) rallied nearly 3% after reporting strong results and lifting its full-year outlook driven by a continued recovery in occupancy rates and an acceleration in rent spreads. Tanger now expects FFO growth of 4.9% this year - up 190 basis points from its prior outlook - but still about 17% below full-year 2019 levels. Comparable occupancy climbed to 98.0% - the highest since 2016 and up 160 basis points from last year - which has driven year-to-date NOI growth of 6.5%. Leasing activity and rent growth have also been impressive in recent quarters following a stretch of nearly three years of negative rent spreads. Tanger reported blended spreads of 14.5% on a cash basis - the strongest since 2016 and marking the seventh-straight quarter of positive spreads. The company also noted that executive chair Steven Tanger will shift to non-executive chair at the end of 2023. Small-Cap CBL & Associates Properties ( CBL ) was little changed after reporting that its occupancy rate recovered to around 91% in Q3, but noted that its renewal spreads declined 6.5% driven by "several portfolio-wide lease deals with underperforming tenants." CBL maintained its full-year outlook calling for a decline in FFO of roughly 20% from last year amid pressure from higher interest expense.

{kind=link}

Hoya Capital

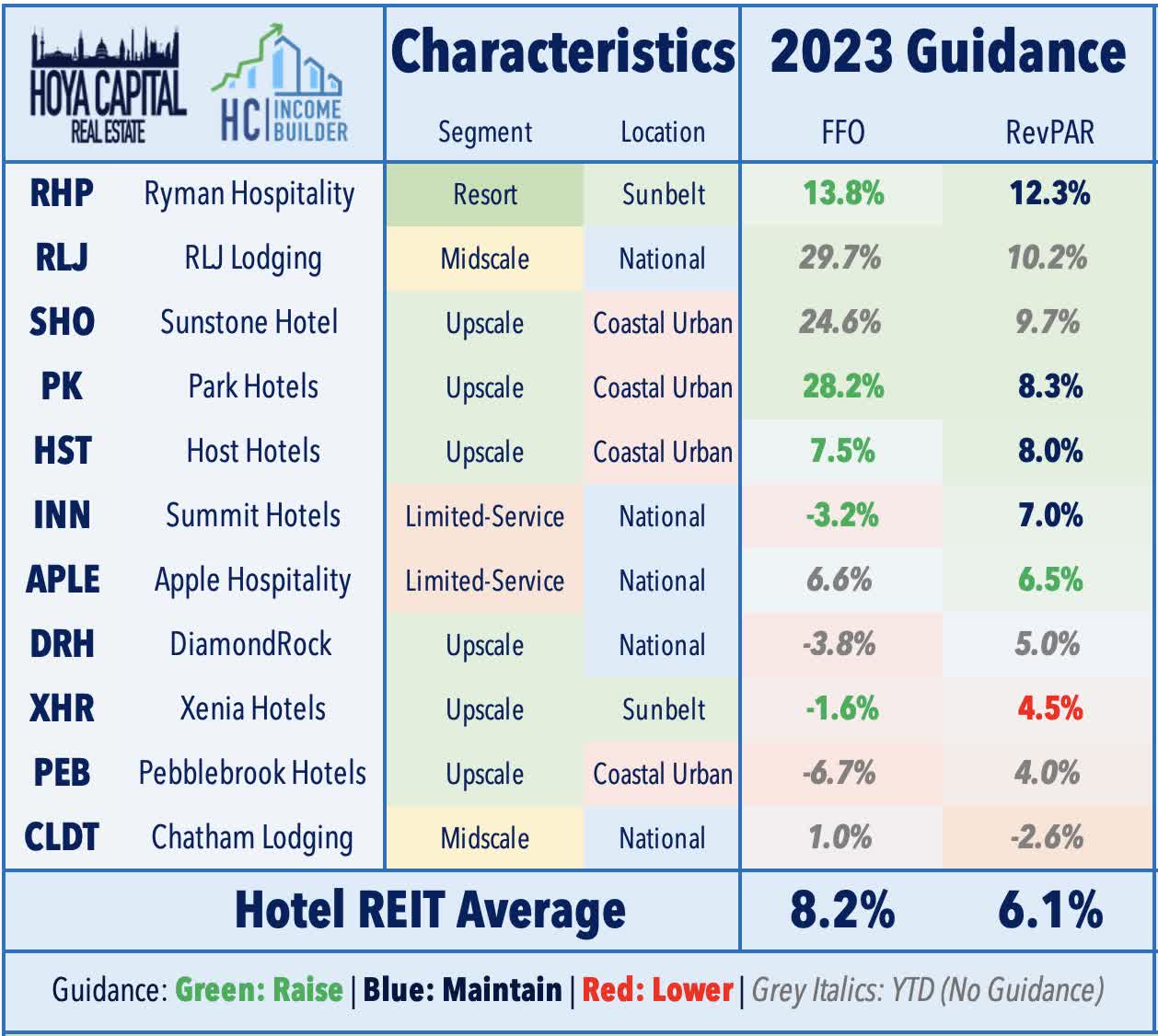

Hotel : Following double-digit gains last week, hotel REITs were mixed this week as earnings season wrapped up with five hotel REITs reporting results. Ryman Hospitality ( RHP ) gained nearly 3% after reporting strong results and lifting its full-year outlook "to reflect strong year-to-date financial results and sustained confidence in the remainder of 2023." RHP noted that its Revenue Per Available Room ("RevPAR") was up 21% compared to the pre-pandemic baseline from 2019 and now expects full-year FFO growth of 13.8% this year and lifted its outlook for total RevPAR growth to 12.0%. On the demand outlook for the holiday season, RHP commented that "early indications are very favorable. We saw a lot of international travel during the summertime, but folks may be staying closer to home for the upcoming holiday season." Apple Hospitality ( APLE ) lagged this week despite reporting strong results and raising its full-year outlook, noting that its RevPAR was 7% above 2019 levels in Q3 - its best quarterly comparable since the onset of the pandemic. All five hotel REITs that provide full-year FFO guidance lifted their full-year earnings, with commentary indicating that leisure demand has moderated only slightly in recent months, while business and group travel has continued its gradual recovery.

{kind=link}

Hoya Capital

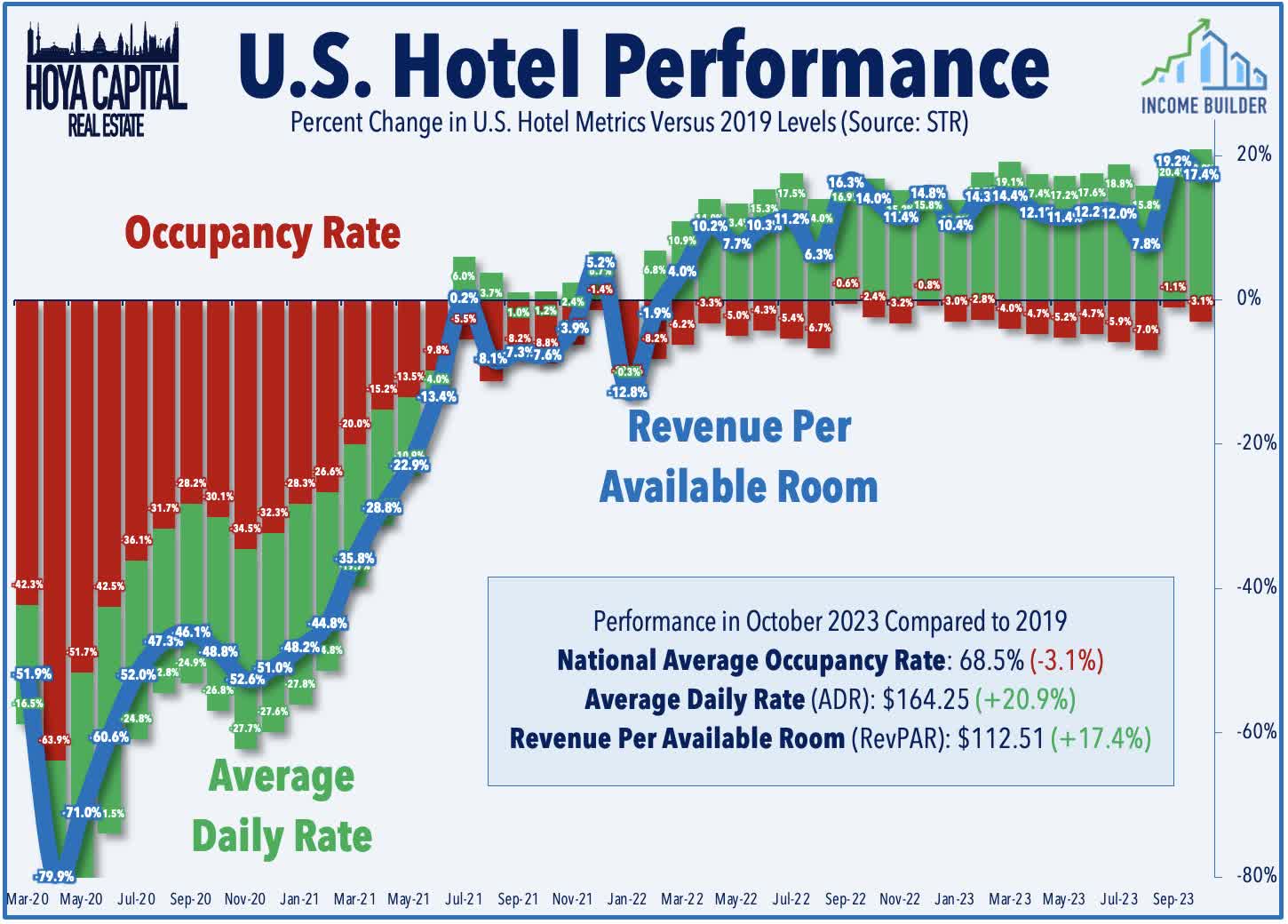

Sticking in the hotel sector, Sunstone Hotel Investors ( SHO ) - which owns a more business-travel-focused portfolio - finished little-changed after reporting in-line results, lifted by a steady recovery in its urban portfolio, which offset a "moderation" in leisure demand. Sunstone noted that its RevPAR remained about 2% below 2019 levels during the third quarter and during October, as a roughly 15% increase in room rates helped to offset a roughly 10 percentage-point dip in occupancy rates. Braemar Hotels & Resorts ( BHR ) and Ashford Hospitality ( AHT ) each dipped over 20% on the week after the highly-levered externally managed REITs reported mixed results. BHR cited a "normalization" in leisure demand, with resort RevPAR dipping 13%, partially offset by a 2% increase in urban RevPAR. AHT reported that its RevPAR was up 2.2% compared to last year - a slowdown from the 6.7% growth last quarter - and still slightly below its 2019 baseline. Recent TSA Checkpoint data shows that throughput climbed to 105% of 2019 levels in October - the highest since the pandemic - while hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was 17% above 2019 levels in October, as a roughly 21% relative increase in Average Daily Room Rates ("ADR") offset a roughly 3% relative drag in average occupancy rates.

{kind=link}

Hoya Capital

Office : Sunbelt-focused office REIT City Office ( CIO ) was among the better performers after wrapping up earnings season with a solid report, recording third quarter AFFO of $0.15/share - easily covering its $0.10/share dividend. CIO noted that it signed 119K SF of leases during the quarter - roughly in line with its pre-pandemic averages - and achieved positive re-leasing spreads of 3.1% on these leases. Underscoring the continued outperformance of Sunbelt-focused REITs over their Coastal peers, Sunbelt-focused office REITs reported leasing volumes that were roughly 10% below pre-pandemic averages in Q3, while Coastal-focused office REITs reported volumes that were 30% below these levels. CIO maintained its full-year guidance, which calls for an 11.5% decline in FFO - slightly better than the broader office sector average. CIO commented, "future supply of new development has and will continue to dramatically taper given the sector's uncertainty and a lack of equity and debt capital. Outside of projects already under construction, we expect limited delivery of competitive buildings in the near to medium term." Orion Office ( ONL ) - the office spin-off that results from the Realty Income ( O ) and VEREIT merger - declined about 7% on the week despite raising its full-year FFO guidance - one of four office REITs to raise its outlook. Leasing activity was non-existent in Q3, however, as the company's occupancy rate dipped to 80.5% by the end of Q3 compared to 86.5% at the end of Q2.

{kind=link}

Hoya Capital

Net Lease : Realty Income - the largest net lease REIT - was among the better performers this week after reporting solid results and lifting its full-year outlook. The single-most active consolidator across the REIT sector - and perhaps the entire real estate industry - Realty Income also boosted its full-year acquisition target to $9 billion following its announced acquisition of Spirit Realty ( SRC ) last week. Realty Income now expects full-year FFO growth of 1.4% - up 10 basis points from last quarter - and also upwardly revised its guidance for same-store rent growth of over 1.5% increased from its prior outlook of over 1.25%. During the quarter, Realty Income acquired $2.0 billion in properties at a cash cap rate of 6.9% - a slightly lower pace of activity compared to the $3.1B in properties acquired during Q2, which were also acquired at a 6.9% cap rate. Gladstone Commercial ( GOOD ) dipped 5% on the week after reporting mixed results, noting that its year-to-date FFO is flat compared to the prior year. GOOD highlighted progress towards its shift away from office properties and towards industrial assets, which now represent 59% of its annual rent following three additional office sales in Q3, which were completed at a disposition cap rate of 8.2%. Global Net Lease ( GNL ) declined about 8% on the week after reporting that its year-to-date FFO is about 10% below last year but noted that its acquisition of Necessity Retail REIT and management internalization - which was completed in September - is "on track" to achieve its projected cost savings by the third quarter of 2024.

{kind=link}

Hoya Capital

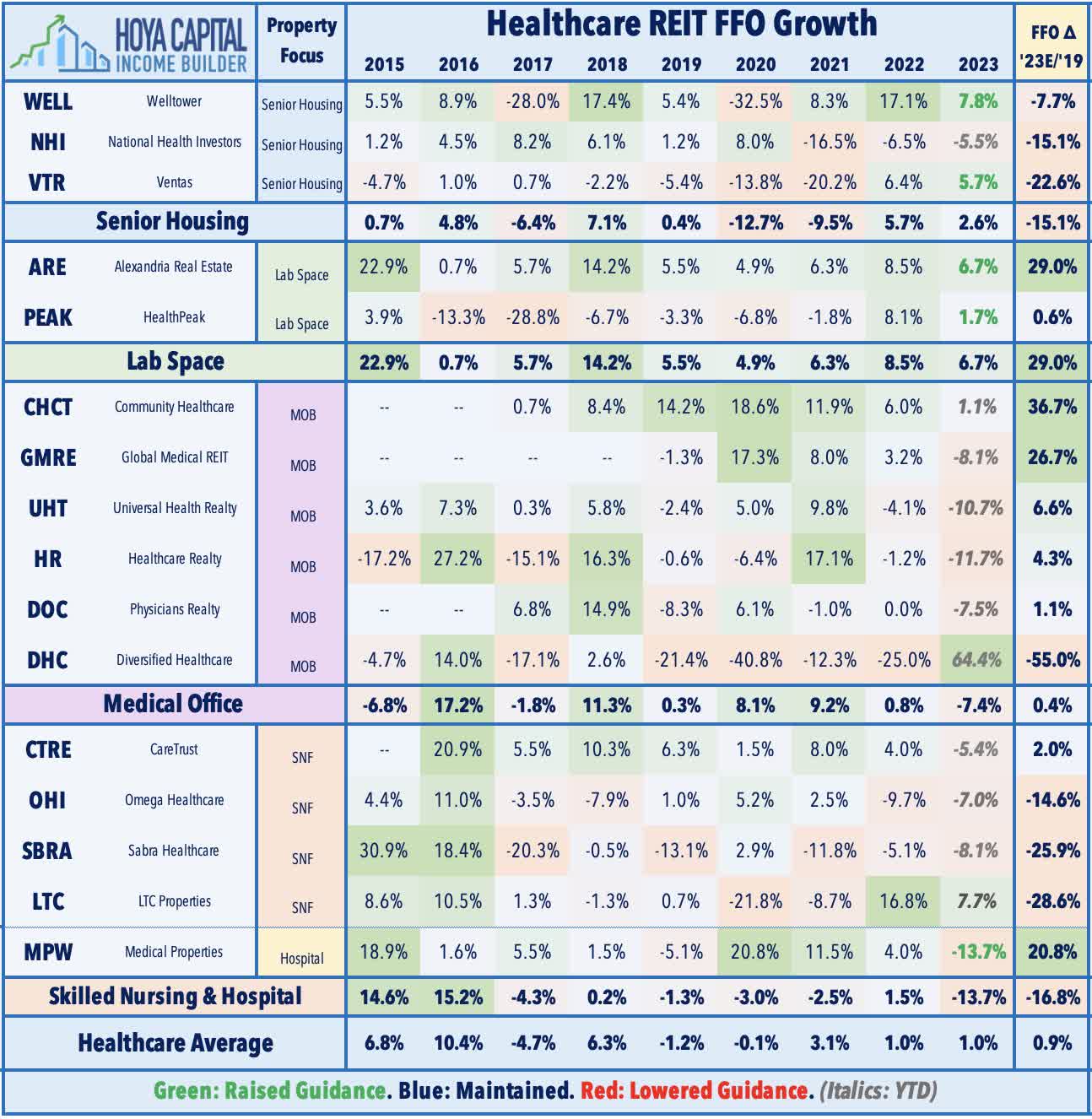

Healthcare : Senior housing strength remains the theme of a relatively impressive slate of reports from healthcare REITs. Sabra Health Care ( SBRA ) - which focuses on skilled nursing and senior housing - gained 2% after reporting solid results and highlighting continued strength in its senior housing portfolio, driven by 6.5% growth in Revenue Per Occupied Room ("RevPOR"). SBRA commented, "while we expect labor issues to persist, we do see continued improvement... occupancy and rent coverage in our skilled and senior housing triple-net portfolios remain on an upward trajectory." Skilled nursing REIT CareTrust ( CTRE ) gained 2% after noting that it collected 97.5% of rents in Q3 - up 80 basis points from the prior quarter - as operator financial stress has eased a bit in recent months. CTRE also provided an upbeat outlook for 2024, noting, "the investment landscape is very favorable for us as we head into 2024... we have a macro environment that has sidelined some of our historic high leverage competitors, and we do not expect the banks to come roaring back with cheap debt anytime soon." Global Medical REIT ( GMRE ) - which focuses on medical office buildings ("MOB") was also an outperformer after in-line results. Elsewhere, Medical Properties Trust ( MPW ) - which rallied after reporting better-than-expected results last week - dipped 20% this week after Stifel downgraded the hospital owner, citing lingering concern over tenant operator health, and the delay of its Connecticut asset sale to Yale New Haven Health.

{kind=link}

Hoya Capital

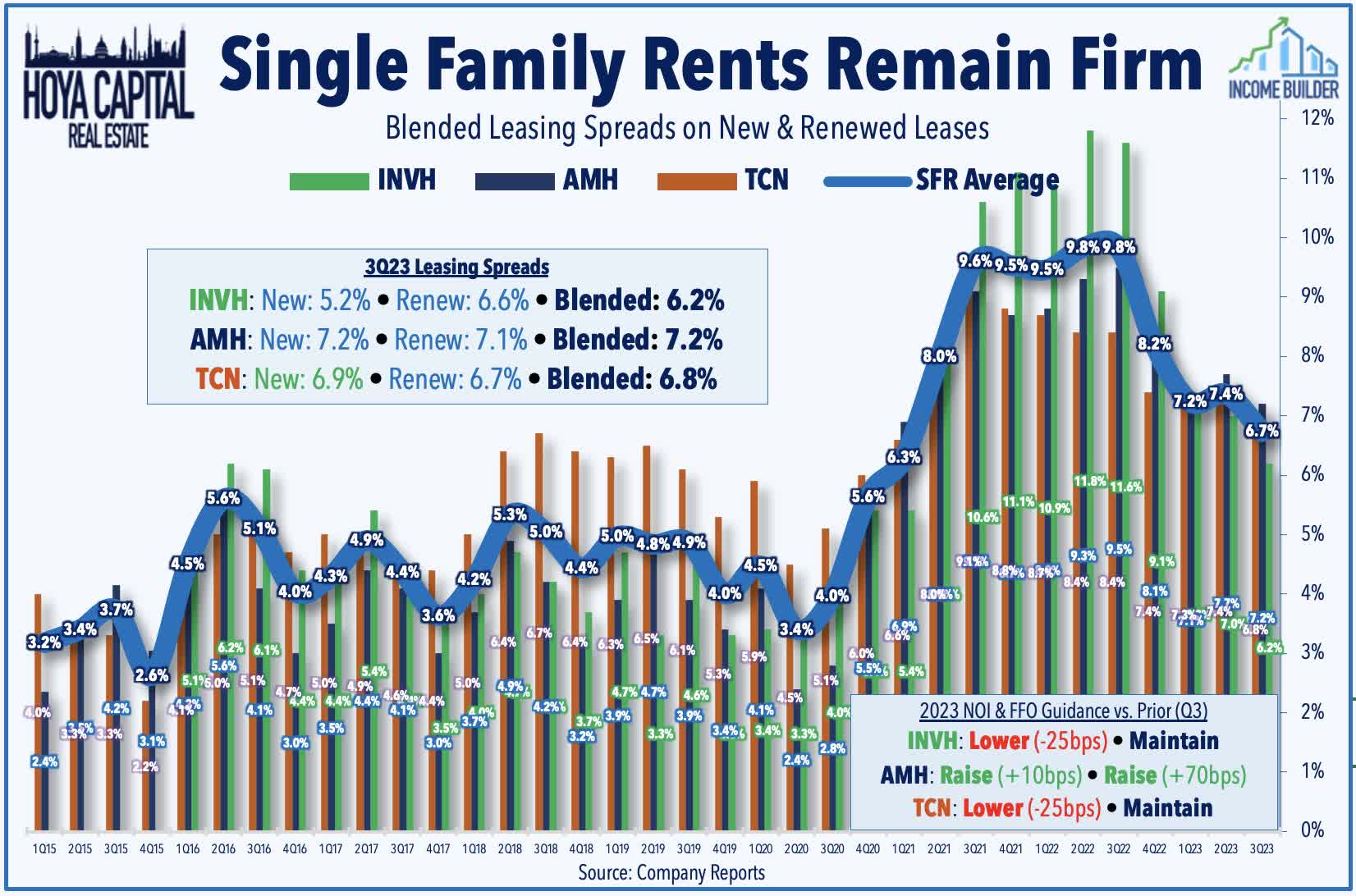

Single-Family Rental : Tricon Residential ( TCN ) - the smallest and most highly-levered of the three SFR REITs - declined about 3% this week after it wrapped up residential REIT earnings season with a decent report showing continued buoyancy in SFR rents. TCN maintained its full-year FFO outlook, which calls for its FFO to revert back to 2021 levels following last year's 30% increase, a decline due entirely to higher interest expense. TCN slightly trimmed its same-store revenue growth target to 6.25% from 6.50% to reflect "softer rent growth on new move-ins" but favorably revised its expense outlook to reflect a "successful reduction of controllable expenses, including property management, repairs, maintenance and turnover." TCN also trimmed its full-year outlook for home acquisitions to 1,850 from 2,000 to "allow for lower leverage parameters" in its JV investment programs. TCN noted that it achieved blended rent growth of 6.8% in Q3 and October - a slight moderation from the 7.4% spreads achieved last quarter - comprised of new lease rent growth of 6.9% and renewal rent growth of 6.7%.

{kind=link}

Hoya Capital

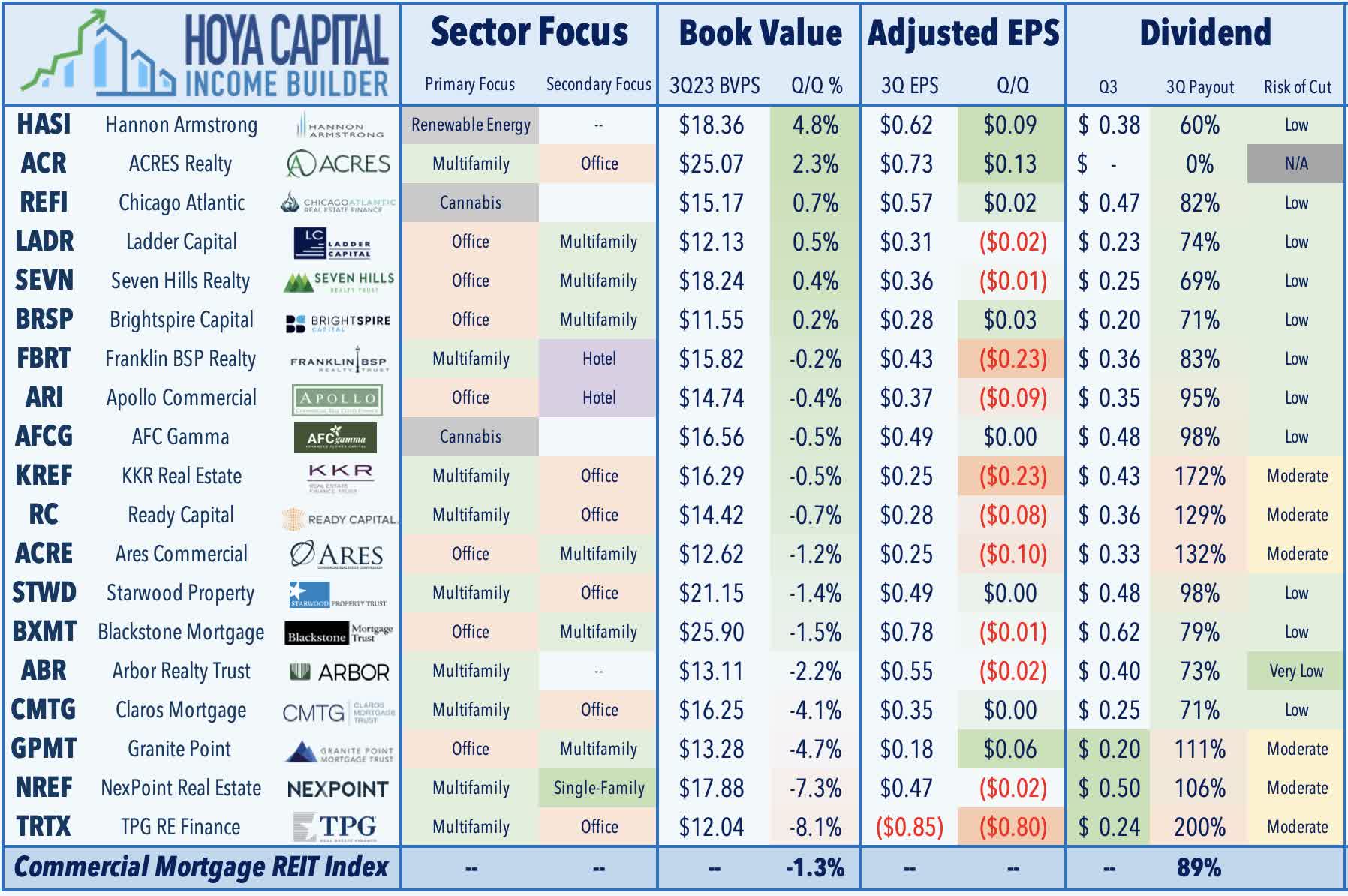

Mortgage REIT Week In Review

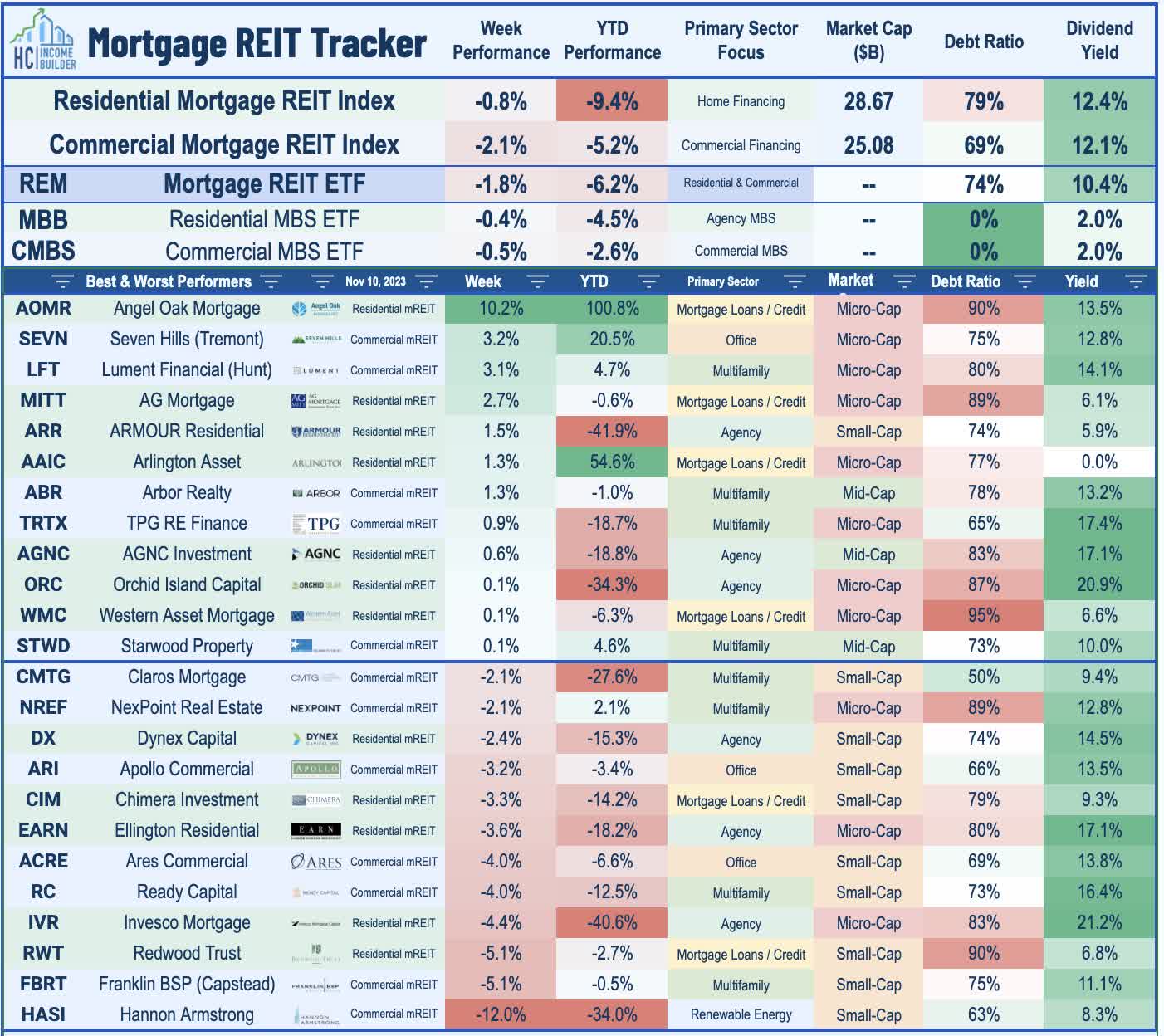

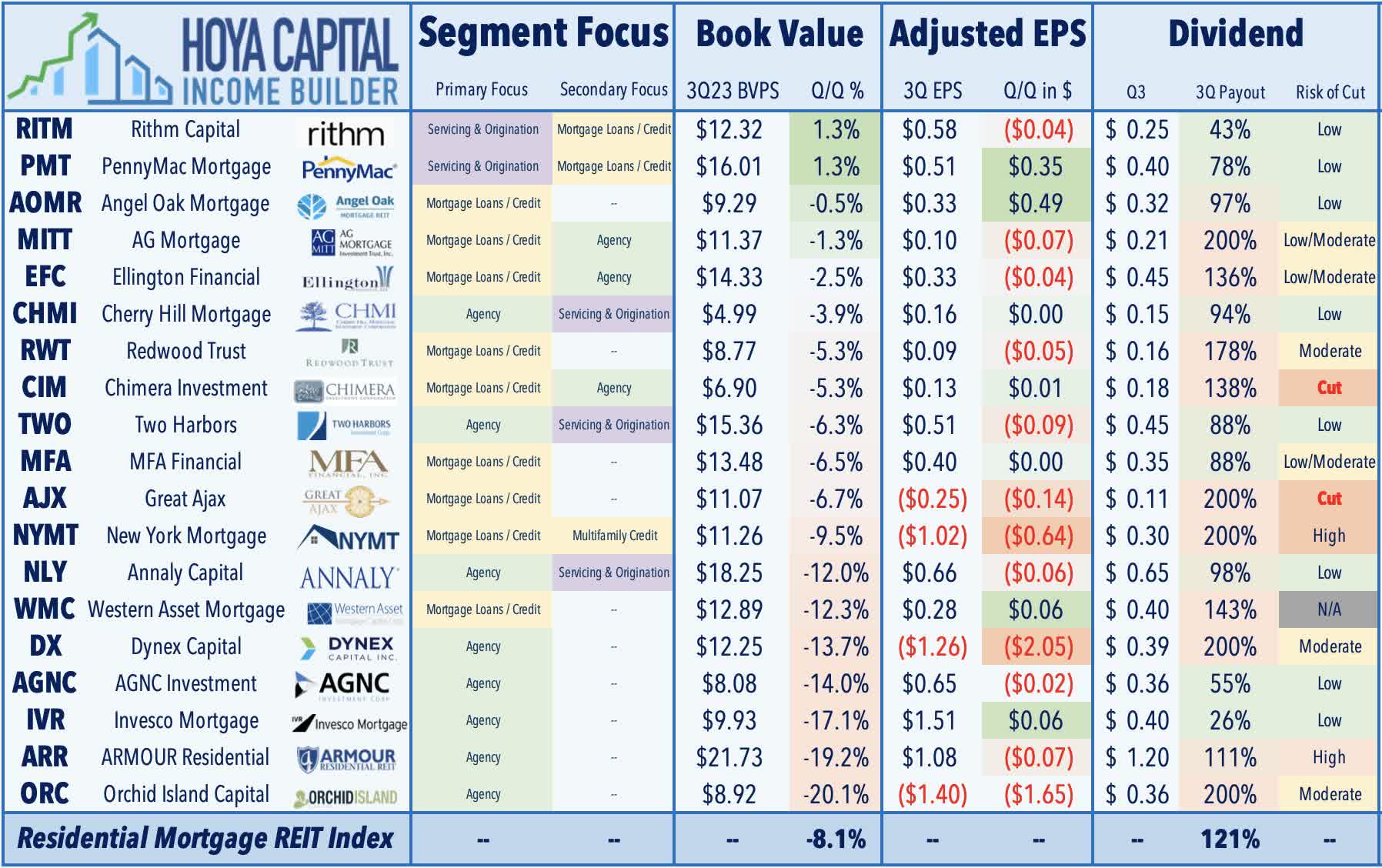

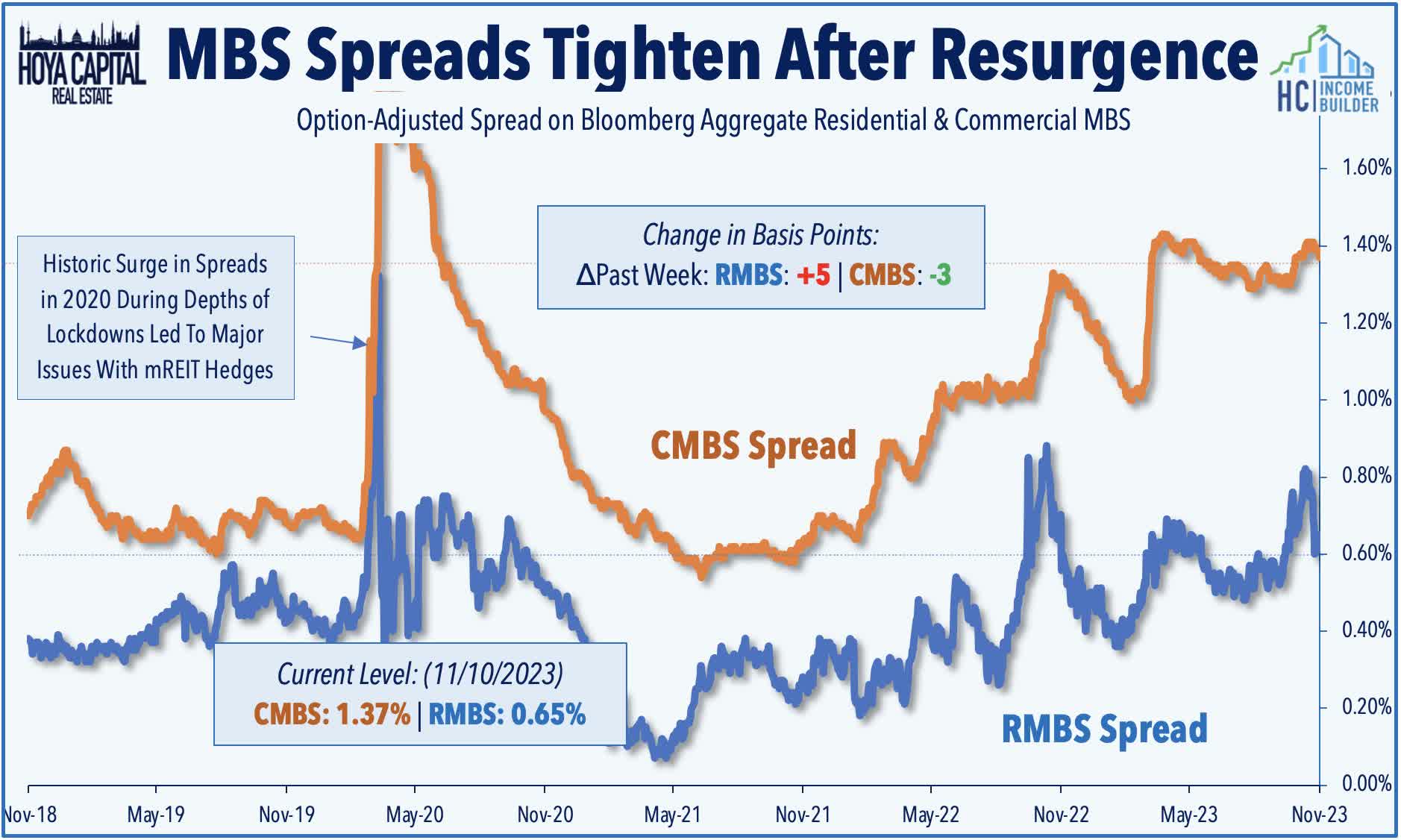

Following frenetic gains of over 13% last week, mortgage REITs finished modestly lower this week as earnings season wrapped up, with the iShares Mortgage Real Estate Capped ETF ( REM ) slipping 1.8% for the week. We saw earnings results from roughly a quarter of the sector this week, with a handful of reports still remaining next week. Angel Oak ( AOMR ) - one of the newer mREITs that went public in 2021 and focuses on non-agency-backed residential credit - rallied more than 10% this week and extending its year-to-date gains to over 100% after reporting strong results, noting that its Book Value Per Share ("BVPS") was lower by just 0.5% in Q3 - the third-best among residential mREITs this earnings season. AG Mortgage ( MITT ) - which also focuses on non-agency-backed residential credit - gained nearly 3% on the week after reporting that its BVPS was lower by just 1.3% in Q3 - the fourth-best among residential mREITs. MITT commented, "residential credit spreads were resilient relative to Agency RMBS," but noted that low mortgage origination volume has become a headwind for its mortgage services-focused business segment. MBA's Mortgage Market Index - a measure of origination volumes - is lower by more than 60% from its peak in 2021.

{kind=link}

Hoya Capital

Elsewhere on the residential side, Invesco Mortgage ( IVR ) - a pure-play agency mREIT - declined 4% after reporting that its BVPS dipped 17% in Q3 to $9.93 - the third-steepest book value decline in the mREIT sector this earnings season - and was estimated to be $9.26 at the midpoint as of last Friday. IVR's distributable EPS, however, increased slightly to $1.51 due to hedge gains, covering its quarterly dividend of $0.40/share. IVR commented that it faced a "challenging environment for Agency RMBS as financial markets adjusted to shifting expectations for fiscal and monetary policy." MFA Financial ( MFA ) was little changed after reporting that its BVPS declined 6.5% in Q3 while its EPS was unchanged from last quarter. Residential mREITs reported an average decline in BVPS of 8.1% in Q3, but there were sharp differences in performance between mREITs focused on traditional agency-backed mortgages and credit-focused mREITs. Agency mREITs reported an average decline in BVPS of 13% in Q3, while credit-focused mREITs reported just a 4% average decline in BVPS.

{kind=link}

Hoya Capital

On the commercial mREIT side, Starwood Property ( STWD ) finished flat this week after reporting better-than-expected EPS of $0.49 - even with last quarter - and noting that its Book Value Per Share ("BVPS") was little changed from last quarter. STWD provided an upbeat outlook, commenting "with the U.S. regional and money center banks having dramatically reduced their real estate lending activities, the lending markets today present tremendous return opportunities. In contrast to many of our public peers, we have actually been deploying capital and STWD is positioned to become one of the leading private credit alternative firms for real estate and infrastructure lending in the world." STWD noted that it placed one new loan on non-accrual, a $61 million loan on a multifamily property in Portland, Oregon. As of quarter end, our nonaccrual loans and REO represented less than 4% of our total assets.

{kind=link}

Hoya Capital

Elsewhere, Granite Point ( GPMT ) declined 2% on the week after it reported that its BVPS declined 4.7% due to an increase in its loan loss reserves, while its distributable EPS declined to $0.18 - shy of its $0.20/share dividend. Its overall CECL reserve increased to 4.9% of total commitments from about 4.1% in the prior quarter. GPMT downgraded a $37M office loan in Los Angeles to a 5-risk rating. The 4 loans that are risk-rated 5 total about $250 million in principal balance and have established an $85 million specific seasonal reserve against them, implying an impairment of about 34% on average. Ready Capital ( RC ) dipped 4% on the week after reporting that its BVPS declined 1% in Q3, while its EPS slipped to $0.28 - shy of its $0.36/share dividend. RC cited "short-term earnings pressure from the ongoing integration of our merger with Broadmark." RC noted that 60-day plus delinquencies remained low at 2.9%, with most delinquencies concentrated in a modest 5% allocation to office.

{kind=link}

Hoya Capital

REIT Capital Raising & REIT Preferreds

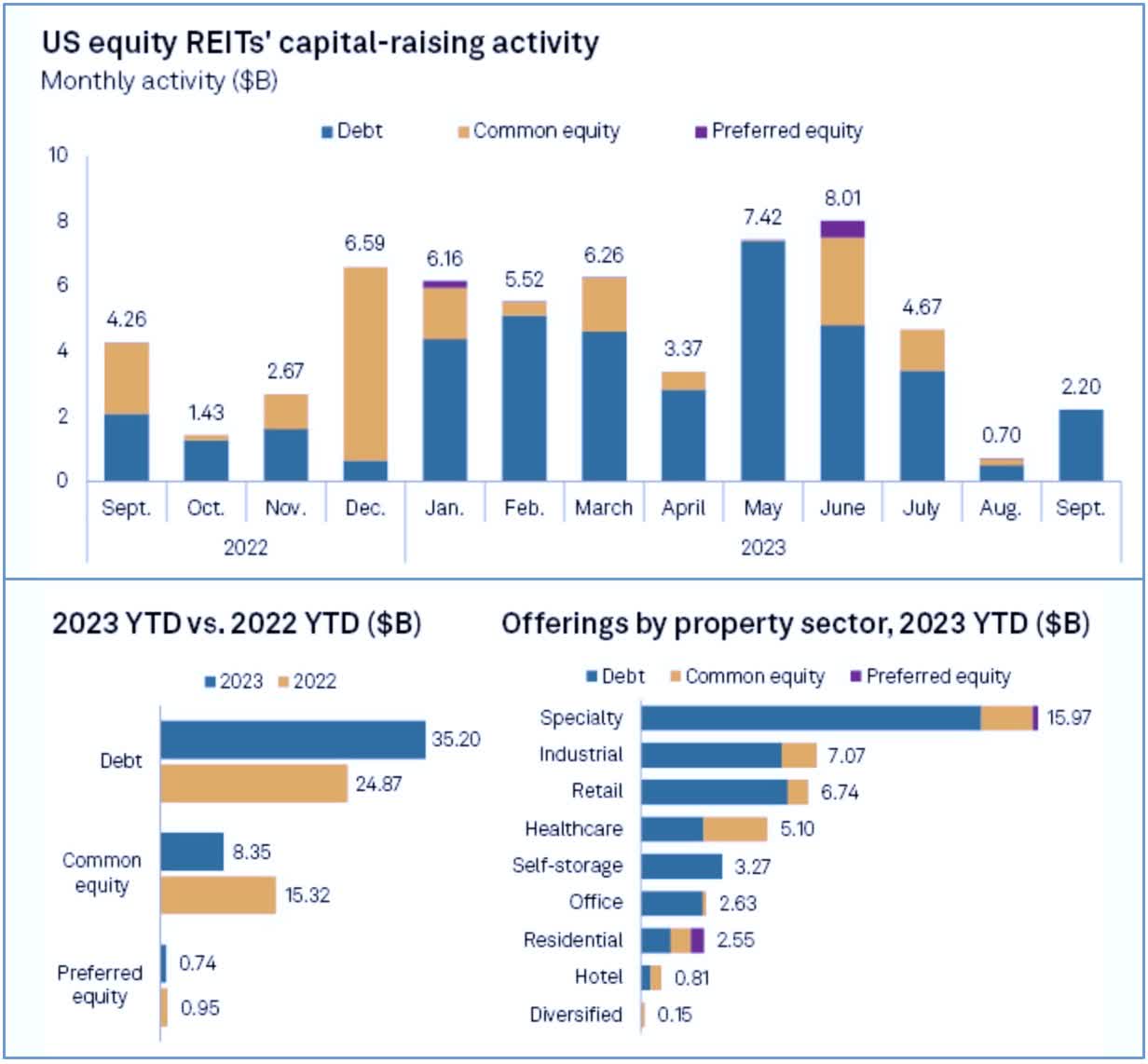

Several REITs were active on the capital-raising front this week, quickly taking advantage of the recent retreat in interest rates. Mall REIT Simon Property ( SPG ) raised over $1.5B this week: $500 million in ten-year notes due 2034 at 6.25%, $500 million in thirty-year notes due 2054 at 6.65%, and €750M of exchangeable bonds at a fixed coupon rate of 3.50%. Apartment REIT Camden Property ( CPT ) raised $500m in three-year senior unsecured notes at 5.85%. Hotel REIT Service Properties ( SVC ) raised $1B in eight-year senior unsecured notes at 8.625%. Billboard REIT OUTFRONT ( OUT ) raised $450M of eight-year senior secured notes at 7.375%. Healthcare REIT Welltower ( WELL ) raised $1.5B through a common stock offering of 17.5M shares at $85.71/share. EastGroup ( EGP ) announced that it has raised $43.6M so far this quarter through its at-the-market common stock issuance program at a weighted average price of $169.21/share. S&P reported last week that REITs had raised $44.3B in new capital through September, which was 8% above last year's pace, but well below the record-high capital-raising activity in 2021 and 2022. The majority of the capital raised this year has come through debt offerings, which have accounted for 80% of the total capital raised this year - well above the historical average of around 50%.

{kind=link}

Hoya Capital

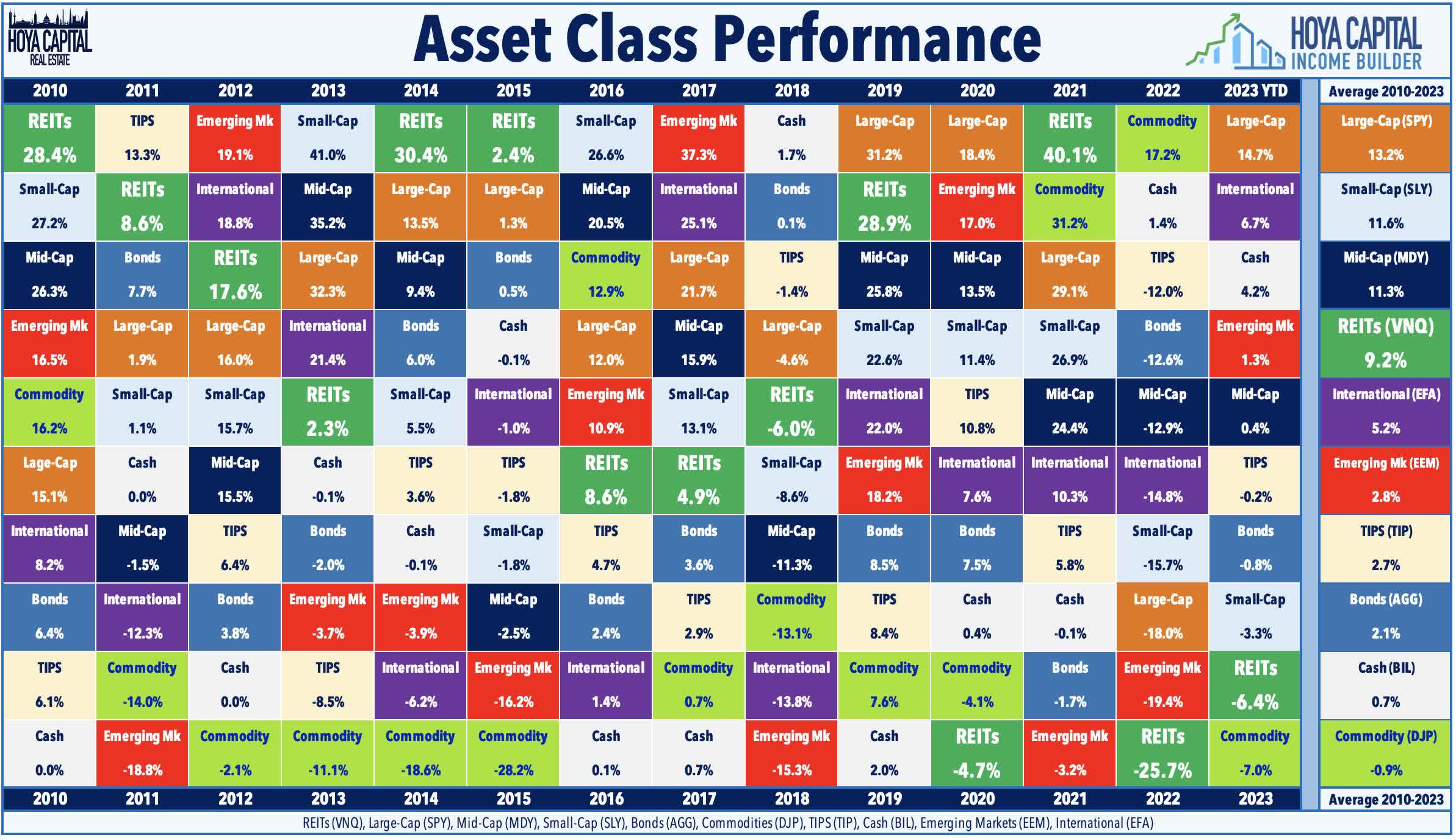

2023 Performance Recap & 2022 Review

With just seven weeks left in 2023, the Equity REIT Index is now lower by 8.4% on a price return basis for the year (-4.4% on a total return basis), while the Mortgage REIT Index is lower by 3.7% (+5.5% on a total return basis). This compares with the 15.2% gain on the S&P 500 and the 0.7% gain for the S&P Mid-Cap 400 . Within the real estate sector, four property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, and Healthcare REITs, while Cell Tower and Office REITs have lagged on the downside. At 4.63%, the 10-Year Treasury Yield has surged by 75 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but down from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is lower again this year, producing total returns of -0.8% thus far. WTI Crude Oil - perhaps the most important inflation input - is higher by 2.4% this year.

{kind=link}

Hoya Capital

There have been few places to hide across financial markets since the start of 2022 in a historically brutal two-year period for investors, which has wiped out nearly a fifth of global financial wealth. The typically steady US bond market delivered its worst year in history in 2022 with a loss of 13.01% on the Bloomberg US Aggregate Bond Index , which is over 4x larger than the previous worst year back in 1994 (-2.9%). Among the ten major asset classes, Commodities was the only segment to see positive inflation-adjusted returns in 2022. After leading the charge in the prior year, REITs finished in the basement of the performance tables among the ten major asset classes on a total return basis with declines of roughly 25% and are again in the basement of the performance tables this year. Notably, the performance dispersion between U.S. Large-Cap and Small-Cap Equities has been unusually large this year at nearly 15 percentage points, which would be the most since 2016.

{kind=link}

Hoya Capital

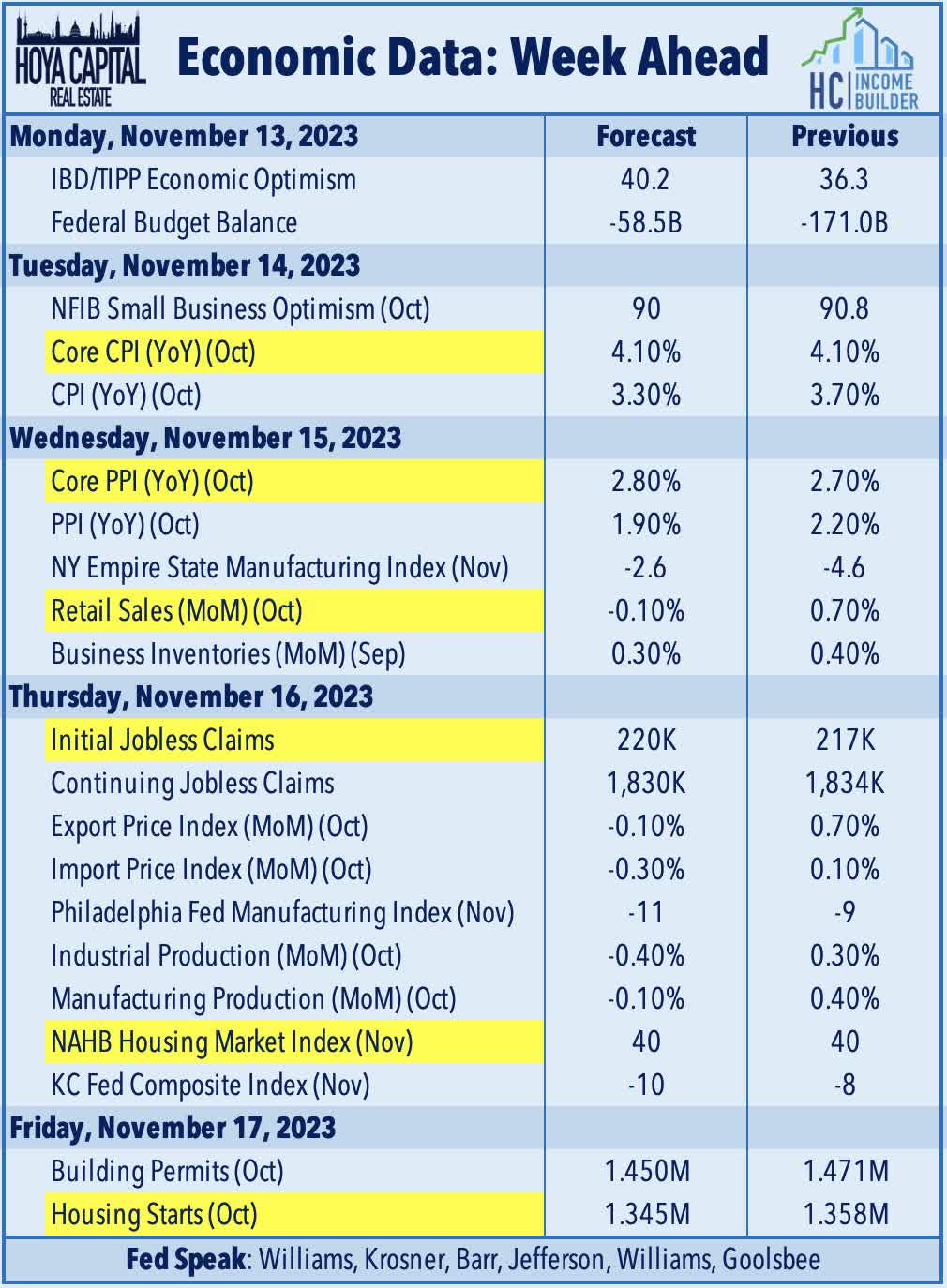

Economic Calendar In The Week Ahead

Inflation data is in the spotlight in a jam-packed week of economic data in the week ahead. The main event comes on Tuesday with the Consumer Price Index for October, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The Headline CPI is expected to moderate to a 3.3% year-over-year rate - down from 3.7% last month - while the Core CPI is expected to remain at 4.1% as some of the "hottest" prints seen in mid-2022 begin to roll off, while the heavily-weighted shelter component finally begins to moderate. Gasoline prices - which drove a reacceleration in inflation from June through September - were lower by an average of 6% during October compared with the prior month and are currently 12% below the September peak. On Wednesday, we'll see the Producer Price Index, which has recently shown an even more significant cooling of price pressures. The Headline PPI is expected to decline back below the Fed's 2% target to 1.9% in October, while the Core PPI is expected to tick up slightly to 2.8% from 2.7%. We'll also be watching Retail Sales data on Wednesday, which has shown surprising strength since early Summer after posting sequential declines in 4-of-5 months early in the year. We'll see housing data later in the week, with the NAHB Homebuilder Sentiment data on Thursday, which is expected to decline for a fourth straight month. On Friday, we'll see September Housing Starts and Building Permits data, which is similarly expected to moderate amid a challenging financing environment for both single-family and multi-family development.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Fed Says 'Not So Fast'