SPY - FEN: This Popular MLP Fund Is A Chronic Underperformer

2023-09-08 01:04:18 ET

Summary

- The First Trust Energy Income and Growth Fund is a closed-end fund that allows investors to include master limited partnerships in a retirement account without tax consequences.

- Despite underperforming similar funds from the same fund house, FEN remains popular among analysts and readers on Seeking Alpha.

- The fund's portfolio consists of common equities of midstream companies and offers an attractive yield of 8.71%, but its disappointing performance raises concerns.

- The fund failed to cover its distribution during the first half of 2023, which could be a real problem if it continues.

- The fund is currently trading at a reasonably attractive valuation.

The First Trust Energy Income and Growth Fund ( FEN ) is a closed-end fund that specializes in investing in midstream companies, master limited partnerships, and similar entities. It is therefore one of the only ways to include master limited partnerships in a retirement account without having to deal with the risk of tax consequences. I mentioned this in my last article on this fund.

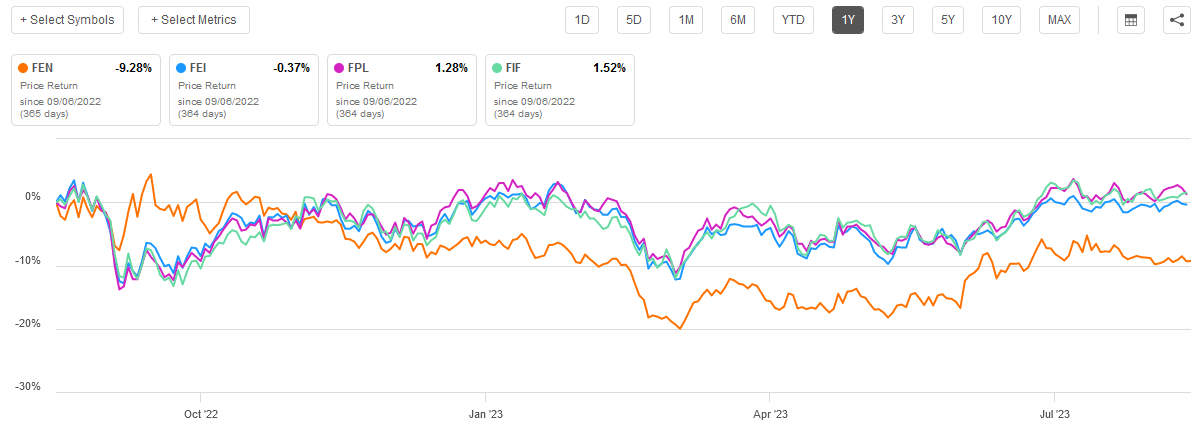

The First Trust Energy Income and Growth Fund is one of the most popular energy-focused closed-end funds among analysts and readers on Seeking Alpha despite the fact that it underperforms similar funds from the same fund house. For example, its price performance over the past year compared to First Trust's other energy infrastructure funds was very disappointing:

{kind=link}

This alone does not necessarily mean that it is a bad fund. Indeed, as we discussed in various previous articles, the portfolio itself is reasonably solid and is pretty similar to the portfolios of the other funds shown above. The fund's 8.71% yield is also very attractive and is indeed better than some of its sister funds. However, we cannot really ignore the fund's disappointing performance in our analysis. I last discussed this fund back in March, and the fund's performance was my biggest complaint about it at that time. As it has been a few months since the time the previous article was published, let us revisit it and see how the fund has changed and whether these changes were for the better or for the worse.

About The Fund

According to the fund's website , the First Trust Energy Income and Growth Fund has the objective of providing its investors with a high level of after-tax total return. As might be expected from an energy infrastructure fund, the webpage specifically states that it will deliver the majority of this total return in the form of direct payments to the shareholders:

First Trust Energy Income and Growth Fund is a non-diversified, closed-end management investment company. The fund's investment objective is to seek a high level of after-tax total return with an emphasis on current distributions paid to shareholders. The fund pursues its objective by investing in cash-generating securities of energy companies, with a focus on investing in publicly-traded MLPs, MLP-related entities and other companies in the energy sector which EIP believes offer opportunities for income and growth. Under normal market conditions, the fund will invest at least 85% of its managed assets in securities of energy companies, energy sector MLPs and MLP-related entities."

The fund's description does not explicitly state what securities issued by energy companies it will be investing in. In many cases, when a security is described as being "cash-generating," the description refers specifically to fixed-income securities such as preferred stock and bonds. However, in this case, the fund is mostly investing in common equities. As we can see here, the fund's portfolio is currently 97.32% invested in common equities with only a relatively small allocation to cash:

CEF Connect

As this fund invests mostly in common equities of master limited partnerships, midstream corporations, and other energy infrastructure firms, the fund can state that it is investing in "cash-generating securities." After all, as I have pointed out numerous times in the past, many energy infrastructure companies have very high yields even on their common equity. As of the time of writing, the Alerian MLP Index ( AMLP ) yields 7.96% compared to the 1.45% yield of the S&P 500 Index ( SPY ). Basically, the S&P 500 Index has a negative real yield right now, but master limited partnerships certainly do not. As such, common stock issued by the companies that this fund invests in can be a pretty good way to generate cash.

The majority of the fund's largest positions should be familiar to most regular readers, as I have discussed many of them in the past. Here they are:

First Trust

The largest positions in the fund are the same as the last time that we discussed it, although a few of the weightings have changed. This could be caused by one security outperforming another in the market and is not necessarily a sign that the fund is actively changing its positions by trading stocks. However, the fund does have a 54.00% annual turnover, so it is definitely doing some trading. That is not an excessive level for a closed-end fund though. Here is how that compares to First Trust's other funds, which we have been using for our performance comparison:

| Fund |

| Annual Turnover |

| First Trust Energy Income and Growth Fund |

| 54.00% |

| First Trust MLP and Energy Income Fund ( FEI ) |

| 51.00% |

| First Trust Energy Infrastructure Fund ( FIF ) |

| 60.00% |

| First Trust New Opportunities MLP and Energy Fund ( FPL ) |

| 57.00% |

As we can see, the fund's annual turnover is comparable to that of its sister funds. As such, we can conclude that the performance differences between the funds cannot be explained by excessive trading expenses.

For the most part, the First Trust Energy Income and Growth Fund has a very reasonable portfolio that consists of many of the best companies in the industry. I might consider replacing Cheniere Energy Partners ( CQP ) with its parent company Cheniere Energy ( LNG ) were I to construct this portfolio, but the partnership does have a much more attractive yield than its parent. The fund's management appears to be targeting a high level of dividend and distribution income here, so the partnership does make some sense.

One thing that we see here is that the largest positions in the fund's portfolio operate in a variety of subsectors in the midstream industry. For example, The Williams Companies ( WMB ) and DT Midstream ( DTM ) are almost exclusively focused on natural gas transportation and storage. Meanwhile, Magellan Midstream Partners ( MMP ) and Plains All American Pipeline ( PAA ) are active in the liquids space with neither company having much in the way of natural gas infrastructure. The remaining companies, with the exception of Cheniere Energy Partners, are generally diversified between liquids and natural gas to one degree or another. This diversification continues over the entire portfolio, as can be easily seen here:

First Trust

This is nice to see because of the different fundamentals possessed by some of these subsectors. I have pointed this out in numerous previous articles. Basically, natural gas-focused midstream companies have much greater growth prospects than either refined product-focused or crude oil-focused midstream companies. This is because the demand for natural gas is likely to grow much more than the demand for hydrocarbon liquids over the coming years. That is a direct result of electrification and the growing use of unreliable renewable energy generation, which is a trend that will benefit the electric utilities that comprise 16.36% of this fund's portfolio. The market seems to recognize this, and liquids-focused midstream companies tend to have higher yields so the presence of these companies will provide this fund with greater income than it would generate were it to exclusively focus on the high-growth areas. Thus, the fact that the portfolio is split between these different segments should prove beneficial for the fund's investors.

Performance Comparisons

As mentioned in the introduction, the First Trust Energy Income and Growth Fund has delivered much worse price performance than its sister funds over the past year. However, there is far more to consider than price performance. For example, each of these funds has a different yield:

| Fund Ticker Symbol |

| Current Distribution Yield |

| FEN |

| 8.71% |

| FEI |

| 7.43% |

| FIF |

| 7.79% |

| FPL |

| 7.12% |

This is very important because a high yield can sometimes offset weak share price performance. This is especially true if an investor is reinvesting the distributions, as it can offset some price declines and allow the investor to obtain extra shares for cheap. For example, someone that buys a fund yielding 7% will still be ahead if the fund declines 5%. I have shown this in numerous previous articles.

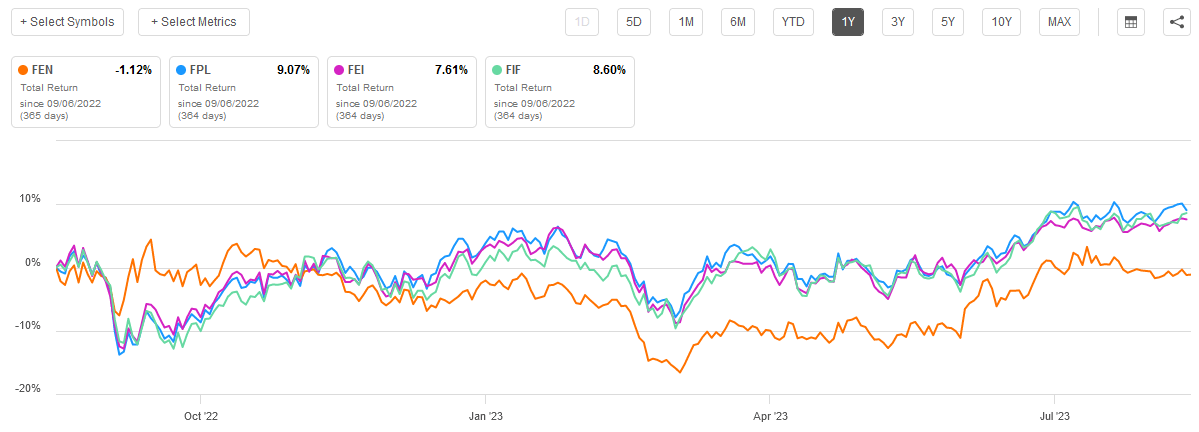

As such, the most important thing to use when evaluating the performance of a fund is the total return. Here are the total returns of all four of the First Trust energy infrastructure funds over the past year:

{kind=link}

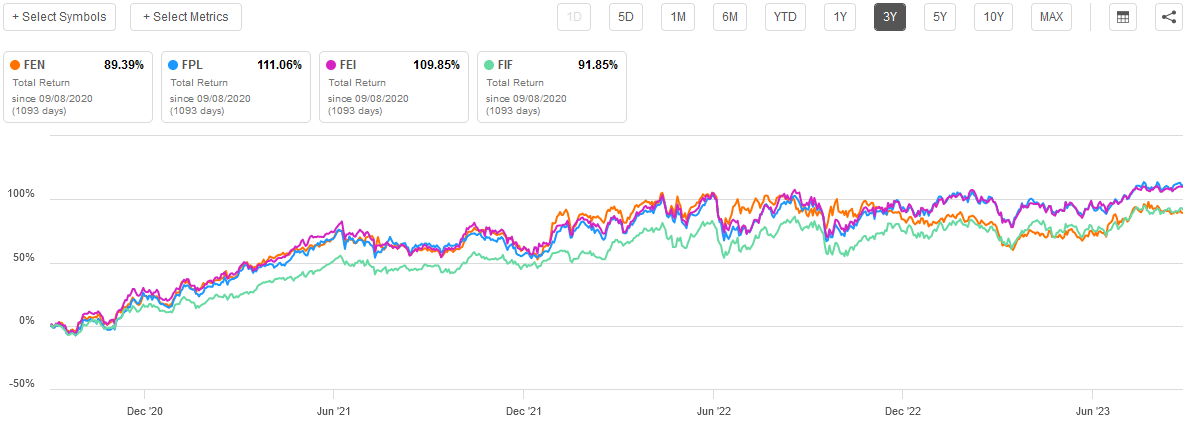

As clearly shown, the First Trust Energy Income and Growth Fund was the only one of the four that delivered a negative total return over the past year. Fortunately, the fund's total return does swing positive when looking at any longer period of time. However, we still see that this fund underperformed its peers over longer time periods. For example, here is the same comparison chart extended out to the past three years:

{kind=link}

That is a very respectable three-year total return for all four of these funds, but it is important to remember that this was coming off of the depths of the worst market for energy companies in a generation. As such, investors should not expect to see returns this attractive from any of these funds during a typical three-year period. The First Trust Energy Income and Growth Fund still underperformed its peers during this period though, which was disappointing.

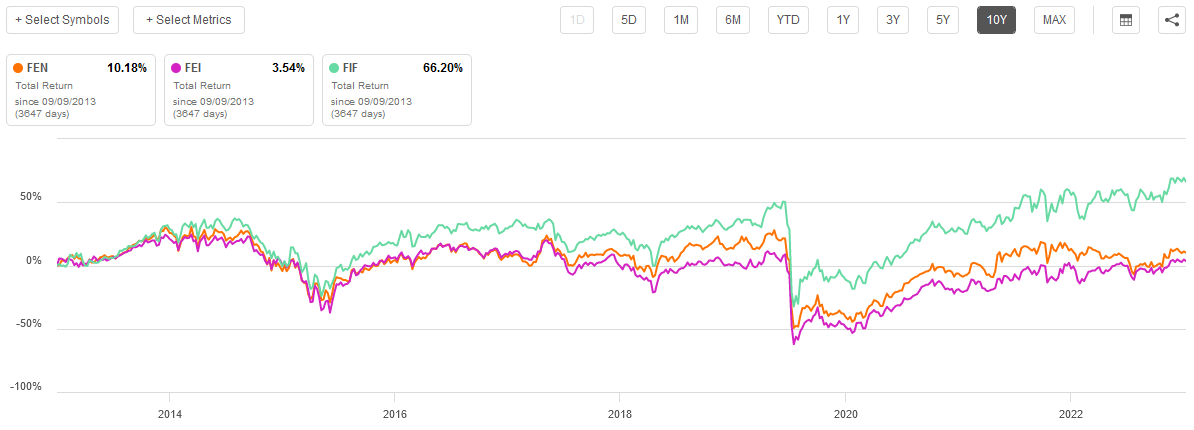

In fact, we have to go out to the trailing ten-year period before this fund begins to competitively perform.

{kind=link}

Here we can see that the First Trust Energy Income and Growth Fund managed to beat the First Trust MLP and Energy Income Fund, although it still lost to the First Trust Energy Infrastructure Fund by quite a lot. The fourth fund is not included in this comparison because it does not have a performance history that stretches back that far.

The takeaway here is that the First Trust Energy Income and Growth Fund is not really the best-performing closed-end fund available for those investors who are still building wealth. It does have the highest yield of any of these funds though, so that aspect might still be attractive to someone that simply wants to maximize their income.

Leverage

As I have pointed out numerous times before, it is common for closed-end funds like the First Trust Energy Income and Growth Fund to employ leverage as a strategy for boosting the effective return of its portfolio. I discussed how this works in my last article on the fund:

Basically, the fund borrows money and then uses those borrowed funds to purchase master limited partnership units. As long as the yield of the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, so this will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As a result, we should ensure that the fund is not employing too much leverage because that would expose us to too much risk."

For the most part, energy infrastructure closed-end funds do not employ excessive amounts of leverage. This fund is no exception to that as its leveraged assets only comprise 20.26% of the portfolio as of the time of writing. Thus, the overall balance between risk and reward here seems to be quite acceptable.

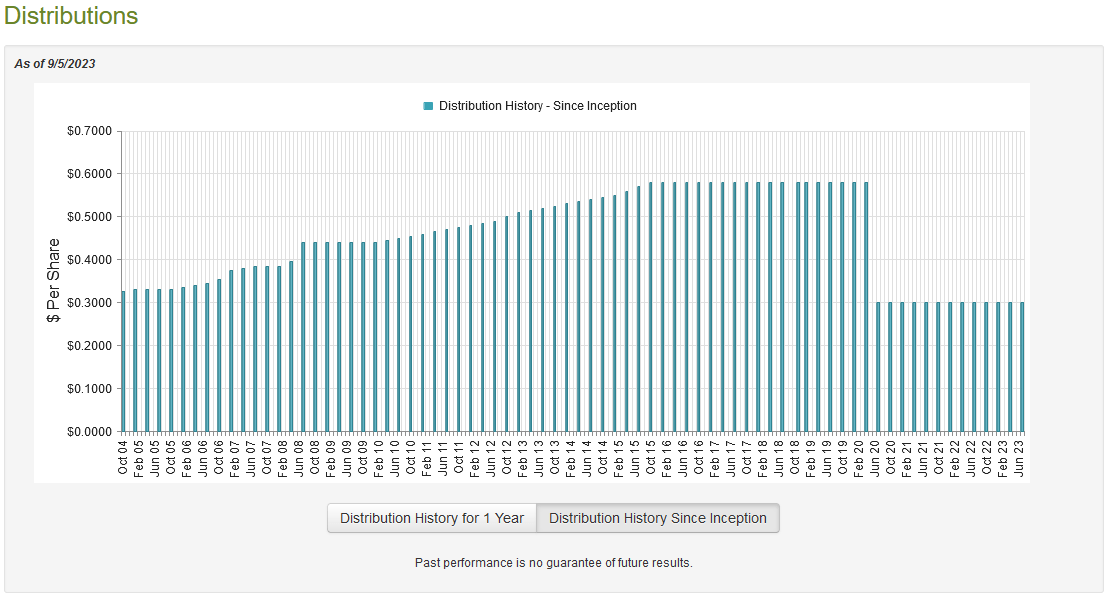

Distribution Analysis

One of the biggest reasons why investors purchase master limited partnerships or midstream companies is that they frequently have higher yields than just about anything else in the market. We can see this quite clearly by considering the yield of the Alerian MLP Index, which was already mentioned. The First Trust Energy Income and Growth Fund purchases the common equity of these entities and then applies a layer of leverage to boost the effective yield of the portfolio above that of the underlying assets. It then pays out the majority of its net investment profits to the shareholders. As such, we can expect that this fund will have a fairly high yield itself. That is indeed the case as the fund pays a quarterly distribution of $0.30 per share ($1.20 per share annually), which gives it an 8.71% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over the years:

{kind=link}

As we can see, the fund slashed its distribution back in 2020 and has yet to restore it. This is rather disappointing. As I mentioned in numerous previous articles, most energy infrastructure funds cut their distributions back in 2020 when the coronavirus devastated the energy sector by severely curtailing the demand for crude oil. However, most energy infrastructure funds have since begun to raise their distributions as the industry has recovered in a fairly big way. We saw that earlier in this article in this fund's three-year total return. The fact that this one continues to pay out the same distribution that it did when the sector was facing much more challenging market conditions is disappointing.

Let us have a look at the fund's finances to see how well the fund is covering its distribution, as well as how well it can likely sustain it.

Fortunately, we have a very recent document available to us that we can consult for the purpose of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a much more recent report than the one that we had available to us the last time that we discussed this fund, so it should give us a better idea of how well it is handling the current market conditions. In particular, both crude oil and natural gas prices were substantially lower in the first half of this year than they were during the same period of last year. Crude oil prices have finally started to recover , hitting their year-to-date high yesterday. Natural gas prices continue to languish though. This can have an impact on the performance of midstream companies in the market, even though their cash flows do not really vary with energy prices. The fund would have had a more difficult time achieving capital gains during the reporting period than it would have during most of last year though, so this report will give us an idea of how successful it was given the more challenging environment.

During the six-month period, the First Trust Energy Income and Growth Fund received $3,998,160 in dividends and $132,344 in interest from the assets in its portfolio. This gives the fund a total investment income of $4,130,504 during the six-month period. The fund paid its expenses out of this amount, which left it with a net investment loss of $2,914,817 during the period. In short, the fund's total investment income was not enough to cover its expenses. Obviously, then, it did not have sufficient net investment income to cover the distribution. This is likely to be concerning at first glance.

However, the fund does have other methods through which it can obtain the money that it requires to cover the distribution. The most important of these are the distributions that it receives from the various master limited partnerships in its portfolio. These distributions are not considered investment income for tax purposes so they will not be included in the figures just described. In addition, the fund might have been able to earn some capital gains that can be paid out to the shareholders. Unfortunately, it was generally unsuccessful at this task during the period. The fund did manage to achieve net realized gains of $10,415,421 but this was more than offset by $20,778,327 net unrealized losses. The fund paid out $11,678,233 in distributions during the period, which it was clearly unable to afford to do. After all, the net realized gains were not enough to cover the distribution, let alone the net investment loss. Normally with a fund like this, that needs to be the case. Overall, the fund's net assets declined by $24,955,956 after accounting for all inflows and outflows during the period. This is very concerning and could indicate that the distribution is not going to be sustainable unless the fund can turn around its performance. It only had net assets of $285,423,379 as of the end date of the period so it cannot tolerate bleeding for very long.

Valuation

As of September 5, 2023 (the most recent date for which data is available as of the time of writing), the First Trust Energy Income and Growth Fund has a net asset value of $15.61 per share but the shares trade for $13.71 each. This gives the fund's shares a 12.17% discount on net asset value at the current price. That is a very reasonable discount that is quite a bit better than the 8.88% discount that the shares have had on average over the past month. As such, the price certainly appears to be acceptable right now.

Conclusion

In conclusion, the First Trust Energy Income and Growth Fund is a fairly popular and commonly recommended fund for anyone looking to gain exposure to master limited partnerships and similar vehicles inside of a retirement account. Unfortunately, it dramatically underperforms similar funds from the same sponsor and fails to cover its distribution during the most recent six-month period. As such, it may not be the best fund to purchase unless you are looking for the highest possible yield and are willing to sacrifice performance to get it. The fund's portfolio and price are certainly not bad, though.

For further details see:

FEN: This Popular MLP Fund Is A Chronic Underperformer