WAL - Fifth Third Bank: Quality Regional Bank Undeservedly Affected By SVB's Collapse Fallout

2023-03-23 07:16:44 ET

Summary

- Fifth Third Bank has little similarities to failed U.S. regional banks.

- Nearly 100% of its securities are classified as AFS, with no hidden losses through HTM.

- Fed’s Bank Term Funding Program allows FITB to cover 65% of uninsured deposits.

- Exposure to tech and crypto sectors is little or non-existent.

- The main risks relate to the contraction of the net interest margin.

Fifth Third Bank ( FITB ) has been battered from the failures of Silicon Valley Bank (SIVB) and Signature Bank (SBNY), but bears little resemblance to them and shouldn't trade at the current valuations unless we are bracing for a full-blown financial system collapse. My investment thesis is that FITB's stock price should recover from the losses suffered in the aftermath of SVB's collapse and return to its pre-March 8 level because the odds are much lower than it can fail like other U.S. regional lenders. Even though it is still not unclear when the current banking crisis will end, I think that recent sell-off affecting high-quality financial institutions like FITB has been overblown and buying opportunities are present.

As of March 22, FITB has lost around 19% of its value since March 8 when SVB announced its intention to raise capital in order to fill a capital gap caused by the sale of securities classified as held-to-maturity. In comparison, the SPDR S&P Regional Banking ETF ( KRE ) has lost 20% of its value since Mar 8, while some of the worst-hit banks by the panic such as Western Alliance ( WAL ) and First Republic bank ( FRC ) have lost 50% and 86% of their value, respectively.

Company profile

FITB owns around $206bn in assets which makes it the 17th largest bank in the U.S. by asset size, according to the Federal Reserve . Its main areas of operations are the Midwest and Southeastern U.S. and has diversified sources of revenues including commercial banking, consumer and small business banking, and wealth & asset management. The Cincinnati-based bank operates 1,087 branches and has a work force of 19,319 employees.

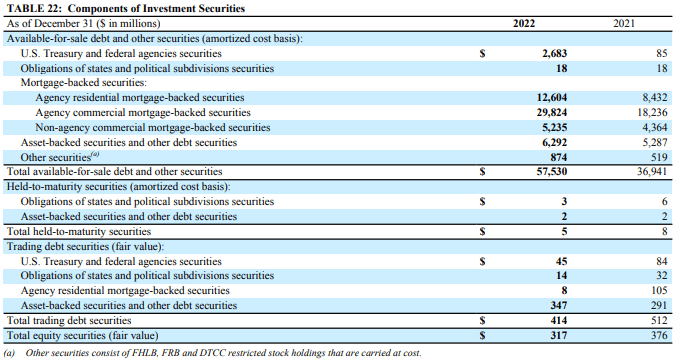

Nearly 100% of owned securities classified as available-for-sale

Importantly, FITB has nearly 100% of its $58bn securities portfolio classified as available-for-sale and is not hiding losses by classifying securities as held-to-maturity. In fact, FITB reported $5.5bn net unrealized loss on AFS securities through other comprehensive income in 2022 in its latest quarterly report. The accumulated other comprehensive loss stood at $5.1bn as of end-2022 compared to total equity worth $17.3bn.

As virtually all other US banks, FITB has endured losses on its securities portfolio due to the rising interest rate environment. However, they are not hidden and are well-documented on its balance sheet, even though there are still not reflected in its income statement. Thus, I think that balance sheet surprises are much less likely than with other banks.

Investment securities held by FITB (FITB Annual Report 2022)

{kind=link}

Federal Reserve's Bank Term Funding Program to provide backstop against deposit outflows

The Federal Reserve's Bank Term Funding Program (BTFP) is a serious backstop for banks and FITV can take full advantage of it. BTFP allows banks to borrow funds from the Fed for up to one year by using as collateral agency mortgage-backed securities and U.S. Treasuries at par value. FITB had around $45bn securities that are available to be used as collateral as of end-2022, including $2.7bn U.S. Treasuries, $12.6bn agency residential MBS, and $29.8bn agency commercial MBS. In comparison, uninsured deposits amounted to $69.4bn as of end-2022. Thus, FITB can potentially borrow funds from the Fed to cover deposit outflows worth 65% of its uninsured deposits.

Uninsured deposits stand at less than 50% of total deposits

FITB fares slightly better than the average regional bank in terms of its uninsured deposits ratio, Fifth Third Bank CEO Timothy Spence said in an interview on CNBC from March 13. The ratio of insured deposits to total deposits is in the low-50%, which is slightly better than the peer average, according to data shared by Spence. Looking at the data from the 2022 annual report , uninsured deposits stood at 42% of total deposits at end-2022. In addition, some 53% of deposits came from consumer and small business banking segment which is less prone to deposit outflows. Uninsured deposits at panic-hit banks such as FRC and WAL were much higher at 79% and 76% of total deposits, respectively, as of end-2022.

Loan portfolio with little exposure to tech sector

FITB has little exposure to the tech sector as its commercial loan portfolio is mainly focused on the real estate and manufacturing sectors. In addition, it didn't mention the word "crypto" even once within its 229-page 2022 Annual Report. This is because FITB is a traditional bank that serves commercial and individual clients in areas such as the Midwest and the Southeast.

It gained some presence in the fintech sector by purchasing Dividend Finance in 2022, which FITB evaluates as the third-largest residential solar financing provider nationally. Even though the unit currently contributes negatively to asset quality due to the housing market downturn, it is still expected to generate $4.5bn loan production in 2023.

When looking at asset quality, FITB reported $2.4bn allowance for credit losses as of end-2022 and had a ACL ratio of 1.98% (up by 7bps from end-Q3). The bank expects $100mn ACL build per quarter during 2023 if the macroeconomic outlook remains unchanged from Q4 2022.

FITB Commercial loan and lease portfolio (FITB Annual Report 2022)

Main risks related to potential narrowing of net interest margin

As I do not believe that FITB will become a failed bank in the foreseeable future, the main risks from a fundamental point of view stem from potential contraction in the net interest margin. However, the consensus remains that the Federal Reserve will raise its policy rate by 25bps in its next meeting on Mar 22, according to Bloomberg . The Federal Reserve is likely to fight the current banking crisis using non-monetary tools as reversing policy too early may lead to unhinged inflation. On the other hand, there are still no signs that the economy will experience a hard landing that could force the Fed to cut rates sharply.

At any rate, I expect that regional banks will raise their credit standards somewhat as a result of the banking crisis which will reduce lending activity, but net interest margin will remain the dominant factor that will drive profitability. In the case of FITB, net interest margin increased to 3.35% at end-2022 from 2.55% at end-2021 which led to an increase in net interest income to $1.6bn in Q4 2022 from $1.2bn in Q4 2021. At the same time, total interest-bearing assets rose by just 1% to $186.3bn in 2022.

Valuation multiples in the middle of the pack

FITB remains in the middle of the pack among regional lenders when looking at the P/E ratio. FITB trades at 7.82 times earnings, which is less than other regional lenders such as Northern Trust ( NTRS ) which trades at 13.73 times earnings and State Street Corp ( STT ) which has a 10.22 P/E multiple. On the other hand, Huntington Bancshares (HBAN), KeyBank ( KEY ) and Comerica Bank ( CMA ) have lower P/E ratios of 7.34, 6.07 and 5.28, respectively. However, I think that valuation multiples are less meaningful in the current crisis as the most important thing is to identify banks that are resilient to the factors that have brought down SVB and SBNY.

Conclusion

FITB remains well-positioned to survive the current banking crisis and recover from it regardless of what happens to other banks. Even if the bank suffers some deposit outflows to large banks in the short-term, I think it is still going to benefit in the long-term from the fact that it is one of the more solid regional banks. Furthermore, FITB is already ahead of the curve with the treatment of nearly 100% of its purchased securities as available-for-sale, which limits its exposure to potential future regulations that force banks to reclassify held-to-maturity as available-for-sale. FITB maintains a conservative business model and has no exposure to high-risk sectors such as crypto or tech start-ups. Moreover, I am optimistic net interest margins will remain high throughout 2023 as Fed is unlikely to rapidly reverse its policy stance.

For further details see:

Fifth Third Bank: Quality Regional Bank Undeservedly Affected By SVB's Collapse Fallout