FIG - FIG: A Forgettable Macro Portfolio Allocator

2023-08-10 07:45:00 ET

Summary

- Simplify Macro Strategy ETF is an exchange-traded fund issued in May 2022 with limited historical data.

- The fund aims to create a lower risk, lower volatility macro portfolio allocator by incorporating tail risk structures and curve steepeners.

- FIG has underperformed its peers and exhibits a significant drawdown, suggesting poor risk/reward analytics.

- The fund has an active approach to its portfolio, with the fund manager being able to take option position on single names and the VIX complex.

Thesis

The Simplify Macro Strategy ETF ( FIG ) is a newly issued exchange traded fund. The vehicle was IPO-ed in 2022, and thus has a limited amount of historical data in terms of analytics and risk/reward metrics.

As per its literature, the exchange traded fund:

[...] is a modern take on the balanced portfolio, built to help navigate today’s toughest asset allocation challenges. FIG addresses these concerns by creating a robust portfolio comprised of equities with positive convexity, diversified and inflation-hedging managed futures, and a suite of income sources with low sensitivity to duration. The fund will also opportunistically invest in equity, credit, interest rate, and FX derivatives (listed and OTC) to capitalize on attractive idiosyncratic market dislocations.

Think about FIG as a macro allocator, a modern take on the classic 60/40 portfolio that is embedded in funds such as the iShares Core Growth Allocation ETF ( AOR ) which we covered here . FIG attempts to take a step forward here by embedding tail risk structures and curve steepeners, with the intent to create a lower risk / lower volatility macro portfolio allocator. In this article, with the limited existing historic data, we are going to have a look at whether the ETF is successful in achieving better metrics than classic portfolio allocators.

Analytics

- AUM: $0.04 billion

- Sharpe Ratio: n/a (3Y)

- Std. Deviation: n/a (3Y)

- Yield: 5.8%

- Premium/Discount to NAV: 0.02%

- Z-Stat: n/a

- Leverage Ratio: 0%

- Composition: Macro Portfolio Allocator

- Duration: n/a

- Expense Ratio: 0.72%

Holdings

The fund is one of those fund family ETFs that contains other names from the Simplify family:

- Simplify Aggr Bd Pl Cr Hd ( AGGH ) - weight 6.61%

- Simplify High Yield Pl Cr ( CDX ) - weight 17.44%

- Simplify Managed Futures ( CTA ) - weight 14%

- Simplify Mkt Ntrl Eq L/S (EQLS) - weight 4.7%

- Simplify Commodities Str ( HARD ) - weight 6.55%

- iShares Gold Trust ( IAU ) - weight 5.84%

- Sim St Treas Fut Strat Et ( TUA ) - weight 17.5%

- Simplify Intermediate Ter ( TYA ) - weight 5.68%

In addition to the defined factors which the fund holds via other ETF structures as per the above, the name contains several option positions:

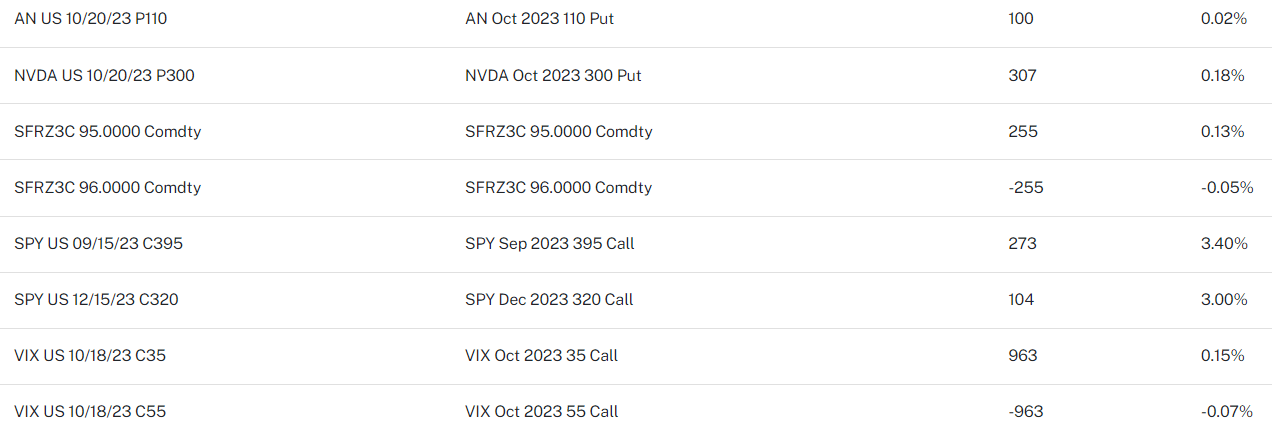

{kind=link}

Options Positions (Fund Fact Sheet)

The fund is long the SPY via SPY call options with various strikes and deltas, and takes some single name views such as the long Put option on NVDA with a 300 strike and October 2023 maturity date. In addition the fund also layers in views on VIX levels via October 2023 calls with a 35 and 55 strike respectively.

The takeaway here is that this is a complex fund that gives the portfolio manager a great deal of latitude in terms of tenor and positioning. You are buying not only into defined risk factors here but also into the trading acumen of the portfolio manager. In such instances, the only appropriate risk gauge is historic performance, which we do not have yet, outside a short period of time. But let us have a look at how the allocator has done in the past year since it came to market.

Performance

As per its term-sheet, the fund benchmarks itself against the Bloomberg US EQ:FI 60:40 Index , and we are going to use the AOR ETF as a proxy for the index, since it matches its total returns closely.

On a 1-year lookback this is how the total return tallies out:

FIG is the only negative performer from the cohort, and it exhibits a very wide basis to AOR. Furthermore the simple treasuries ETF SGOV (as a risk free proxy) has done tremendously well, matching the 60/40 portfolio performance with virtually no drawdown.

We also looked at a multi asset CEF here, since the BlackRock Capital Allocation Trust ( BCAT ) tries to achieve a similar feat for a 60/40 multi-asset portfolio, but with layered leverage.

What is worrisome about FIG is not only its negative performance, but its drawdown profile - we can see the fund having a significant drawdown in 2022, and it never recovered after, while its peers have. This will translate into bad risk analytics when they finally come out.

How you should think about complex active macro allocators

FIG is a complex macro portfolio allocator that contains a plethora of risk factors - equities, rates, credit spread, curve shape, commodities, and futures. Furthermore, the fund gives the portfolio manager latitude in terms of layering in additional risk factors via options. At the end of the day, such an instrument can only be quantified through its performance because its composition is not set in stone.

FIG fails to outperform simple 60/40 instruments like AOR, and by looking at its historic performance we anticipate poor risk/reward analytics when they end up coming out.

As an example how active management can detract from this fund's performance, just look at the options in the holdings - if we do not get a significant market sell-off by the end of October, the fund will fully lose the premium paid on its 35/55 VIX call spread, as well as the premium paid on the October 300 strike NVDA put.

This is not a passive ETF, but an active one with a complex holding structure that layers in a very high amount of risk factors. Unless it demonstrates it can outperform simple builds, or exhibits better risk/reward analytics, there is no reason to take a position in this name.

Why FIG won't likely outperform AOR over the next year

FIG is an active ETF that aims to outperform simple 60/40 portfolio constructions such as AOR. The fund does this by aggregating a number of risk factors such as credit, commodities and complex rates and by taking proprietary market positions such as buying 35/55 October VIX call spreads, October NVDA puts and SOFR futures (SFRZ call spread).

Most often than not, active market timing positions fail, and serve as a detractor. As an example VIX has been suppressed all year in 2023 by the 0DTE options construct, and it would take a significant black swan event for the call spread to pay off. We expect all premiums paid for the options positions to detract from the fund performance.

Secondly the fund construct introduces too many complex risk factors which underperform long term. Having a look at its U.S. high yield component CDX, the fund focuses on U.S. high yield credit and tries to hedge the downside via SPY puts, CDX index calls, or other instruments with a cost of carry. Unfortunately, the fund does not layer in enough hedges to provide a true downside protected pay-off profile for wider credit spreads, but does pay a carry cost, meaning lower returns in a true bull market. Conversely AOR contains a much lower exposure to US high yield, and its sleeve is unhedged without a cost of carry.

Conclusion

FIG is a newly issued exchange traded fund. The vehicle came to market in 2022, and it represents a modern take on a balance portfolio. The fund layers in a multitude of risk factors and gives the fund manager latitude in terms of layering in additional risk strategies (such as shorting NVDA via put options). Given its active approach to its portfolio, time will be the judge of its acumen, but on a one-year lookback FIG has underperformed its vanilla peer AOR by more than 800 bps, and we suspect it will show poor risk/reward analytics when the numbers come out. We do not see anything appealing in FIG at this juncture, and are on Hold until more historical data is available and risk analytics come out.

For further details see:

FIG: A Forgettable Macro Portfolio Allocator