WFC - FINS: This Unique CEF Is Nice As A 'Feel Good' Investment But It Is Nothing Special

2024-01-03 04:44:48 ET

Summary

- The Angel Oak Financial Strategies Income Term Trust offers a current yield of 10.98%, which compares favorably to other income-focused investments.

- The fund's historical performance has been disappointing, with a decline of 40.45% since its inception in May 2019.

- The fund primarily invests in debt securities issued by community banks, which may appeal to investors looking to support local communities. However, the fund's performance history and lack of transparency make it unattractive for new investments.

- The fund may not be able to sustain its current distribution if the market does not continue to strengthen. There is a real risk that the Fed will disappoint.

- The fund has an attractive valuation, but the risks here are too great to justify purchasing the fund today.

The Angel Oak Financial Strategies Income Term Trust ( FINS ) is a closed-end fund that income-focused investors can employ in pursuit of their goals. The fund certainly does fairly well at the provision of income, as its 10.98% current yield compares very well with many other income-focused investments in the market right now. The fund states that it has a specific emphasis on investing in debt securities issued by community banks, which is a focus that very few other funds possess. As such, this fund may have a certain “feel good” image that some investors might appreciate. After all, the giant Wall Street banks do not invoke the same warm and fuzzy feelings that the local bank in your community might. Thus, there may be some investors who purchase this fund because it makes them feel as though they are supporting their local communities. The fact that it has a similar yield to comparable funds that invest in any securities that they can find means that we do not have to sacrifice returns in order to get that satisfactory feeling.

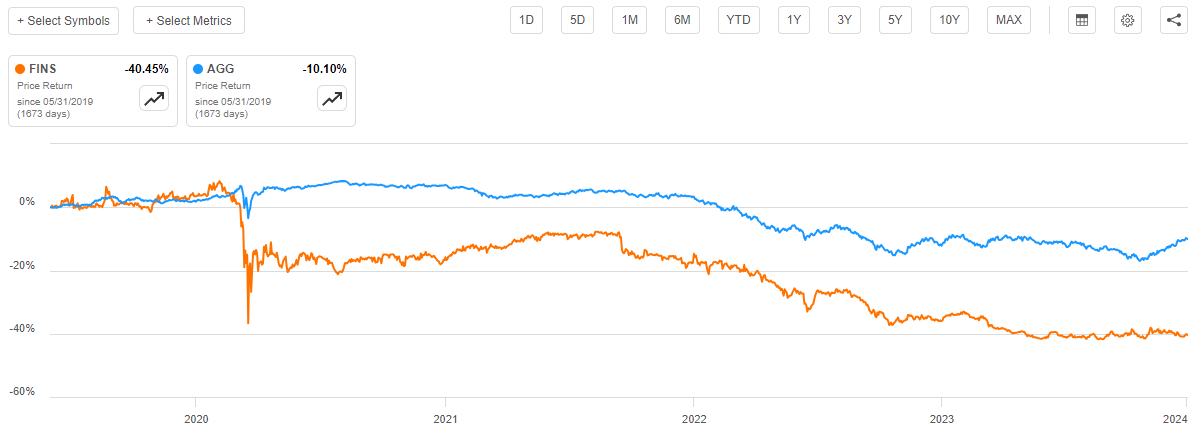

Unfortunately, the fund’s historical performance does not look particularly impressive. As we can see here, since May 31, 2019 (the date of the fund's inception), the fund’s share price has declined by 40.45% compared to a 10.10% decline of the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

The biggest thing that we see here is that the Angel Oak Financial Strategies Income Term Trust never recovered from the broad-market sell-off that occurred at the outbreak of the COVID-19 pandemic. As I have pointed out in various previous articles, investors sold off everything indiscriminately in March 2020 out of fear over the pandemic. This fund never recovered from that, which is probably because its leverage forced it to sell off its assets as they were plunging. This is akin to a margin call that effectively locked in its losses. The fund then suffered again in 2022 as the Federal Reserve started monetary tightening, which affected every fixed-income fund. Overall, this performance history is certainly not going to win this fund very many fans.

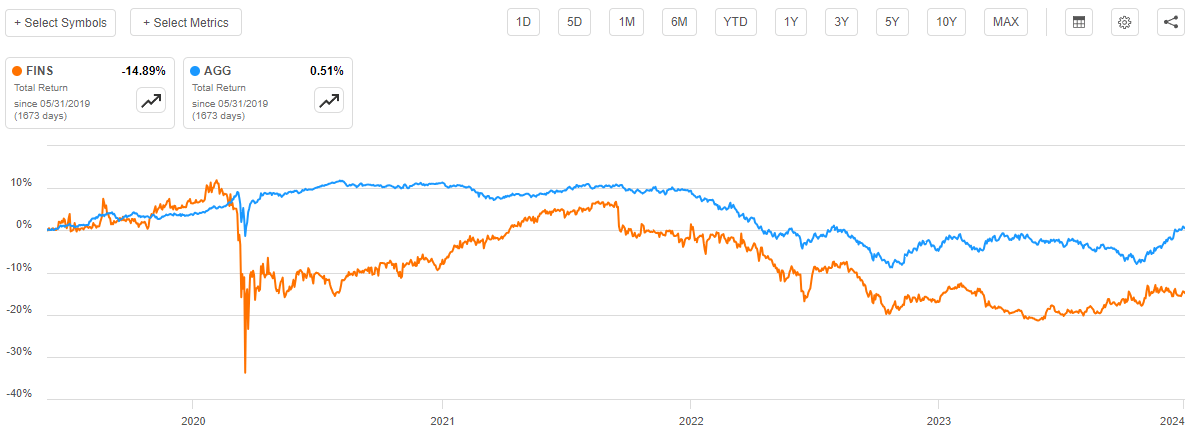

However, closed-end funds like the Angel Oak Financial Strategies Income Term Trust typically pay out all of their investment profits to the shareholders in the form of distributions. This is one of the reasons why these entities usually have much higher yields than most exchange-traded funds. These distributions can offset some of the declines that the fund experiences with respect to its share price. As such, we should always consider the fund’s distribution in any performance analysis. When we do that, we see that investors in the Angel Oak Financial Strategies Income Term Trust only lost 14.89% since its inception, which is still much worse than investors in the Bloomberg U.S. Aggregate Bond Index:

{kind=link}

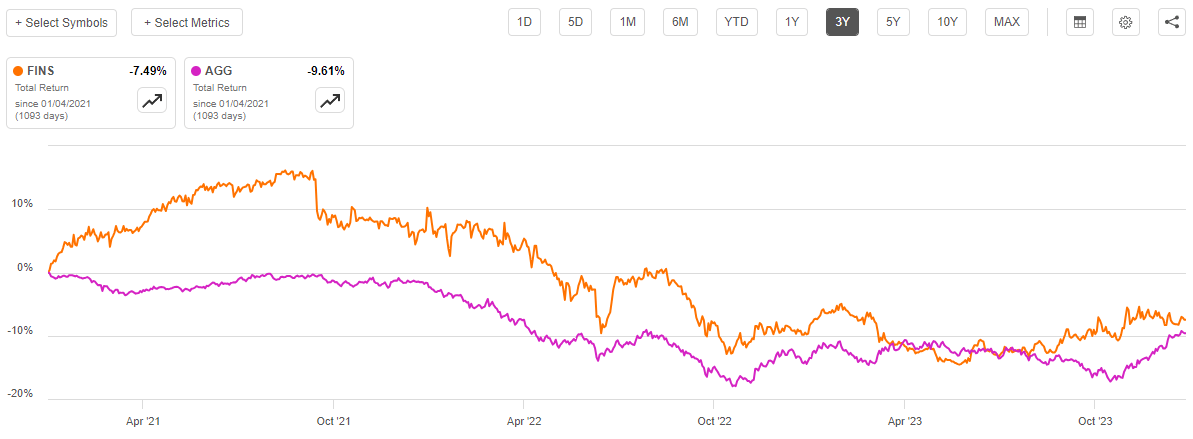

The majority of this poor performance was once again due to the panic-driven sell-off in all financial assets at the outbreak of the COVID-19 pandemic. Over the past three years, the fund has managed to beat the index in terms of total returns:

{kind=link}

As we can see, over the past three years, investors in the Angel Oak Financial Strategies Income Term Trust have only lost 7.49% compared to a 9.61% loss for investors in the broader market. This should improve the fund’s standing in the minds of income-focused investors, but it is still a loss and we do not like to suffer losses. The market is expecting that things will improve in 2024 though, so let us have a closer look at this fund and see if purchasing its shares might make sense today.

About The Fund

According to the fund’s website , the Angel Oak Financial Strategies Income Term Trust has the primary objective of providing its investors with a very high level of current income. This objective seems quite logical considering that the fund’s name suggests that it tries to provide a solution to the problem that many investors have had earning income from the assets in their portfolios over the past twenty years or so. The website describes its strategy thusly:

The Angel Oak Financial Strategies Income Term Trust is a closed-end fund that seeks current income with a secondary objective of total return. The Fund utilizes a banking sector debt-centric strategy, which exhibits low historical correlations to other areas of the market.

This description specifically states that this fund invests primarily in debt securities. CEF Connect confirms this, as it states that 100.31% of the fund’s net assets are invested in bonds alongside an 11.63% allocation to preferred stock:

CEF Connect

We also see that the fund has very small allocations to common stock and convertible securities. These allocations are not nearly large enough to really matter in terms of the fund’s performance. It also has a negative allocation to cash, which is due to the fact that this fund employs leverage in an attempt to boost the effective yield of the portfolio. We will discuss the fund’s use of leverage later in this article. For now, the takeaway is that this fund is primarily investing in debt securities and preferred stock.

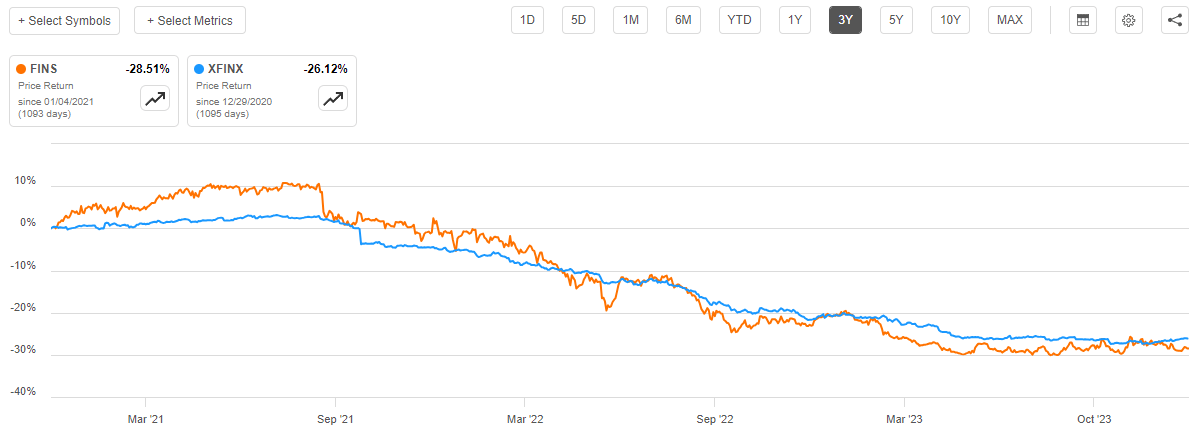

As this is a fixed-income fund, its focus on the provision of current income makes a great deal of sense. After all, bonds are by their nature income vehicles since investors purchase a bond at its face value when it is first issued and receive the face value back when the bond matures. There are no net capital gains over the bond’s lifetime and the only net investment return that investors receive is the coupon payments that the bond regularly pays out. The same is true of floating-rate securities, which are occasionally issued by banks. The only difference between these and fixed-rate bonds is that the coupon payment changes with interest rates, but the absence of net capital gains over the lifetime of the security is still true. The fund’s semi-annual report lists a number of both fixed-rate and floating-rate securities that the fund is invested in, but it does not specifically state what percentage of the fund is invested in either type of security. The fund’s share price performance correlates much more with what we would expect from fixed-income securities than floating-rate securities, as does its net asset value. As we can see here, the fund’s net asset value is down 26.12% over the past three years, which is just a bit better than the fund’s share price performance over the period:

{kind=link}

As I pointed out in a few previous articles, floating-rate securities tend to be very stable in terms of price. These securities do not decline in price as interest rates go up. Thus, the fund’s performance more aligns with that of fixed-rate securities rather than floating-rate ones. We can therefore probably assume that the majority of this fund is invested in fixed-rate securities, but as stated the financial reports nor the website provide an exact percentage.

In the introduction to this article, I stated that the Angel Oak Financial Strategies Income Term Trust invests primarily in the debt securities issued by the nation’s community banks. This is a sector that tends to be very underrepresented in the market, which is probably partly due to the fact that these banks are very small compared to much larger national or even regional banks. The Federal Reserve states that community banks have under $10 billion in assets. This compares to a bank like JPMorgan Chase ( JPM ), which has just under $4 trillion in assets. The capital markets have always emphasized much larger companies rather than small ones, so it is no surprise that a bank that may only have a few branches in one town goes unnoticed in terms of name recognition and media coverage.

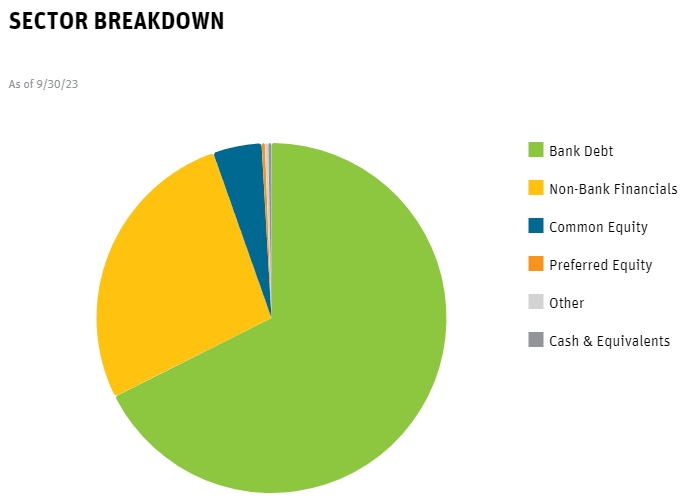

The fund’s semi-annual report does not specifically state what percentage of the fund’s assets are invested in community banks. However, the website states that 67.6% of the fund’s assets are invested in bank debt:

{kind=link}

This chart unfortunately does not do a great job of showing the fund’s sector breakdown on a static website, so here is the same information in a table format:

| Sector |

| % Of Fund |

| Bank Debt |

| 67.6% |

| Non-Bank Financials |

| 27.0% |

| Common Equity |

| 4.5% |

| Preferred Equity |

| 0.3% |

| Other |

| 0.3% |

| Cash & Equivalents |

| 0.3% |

A look at the fund’s portfolio as published in the semi-annual report shows that the overwhelming majority of the fund’s bank debt holdings consists of securities that are issued by fairly small banks. The nation’s huge banks like JPMorgan Chase, Citibank ( C ), Wells Fargo ( WFC ) are nowhere to be found on the published holdings list. Neither are the larger regional banks like PNC Financial Services Group ( PNC ), U.S. Bank ( USB ), or M&T Bank ( MTB ). Thus, we can assume that most of the bank debt weighting consists of relatively small community banks that probably only serve a specific geographic area. However, this is not certain as the fund does not provide a breakdown by company size.

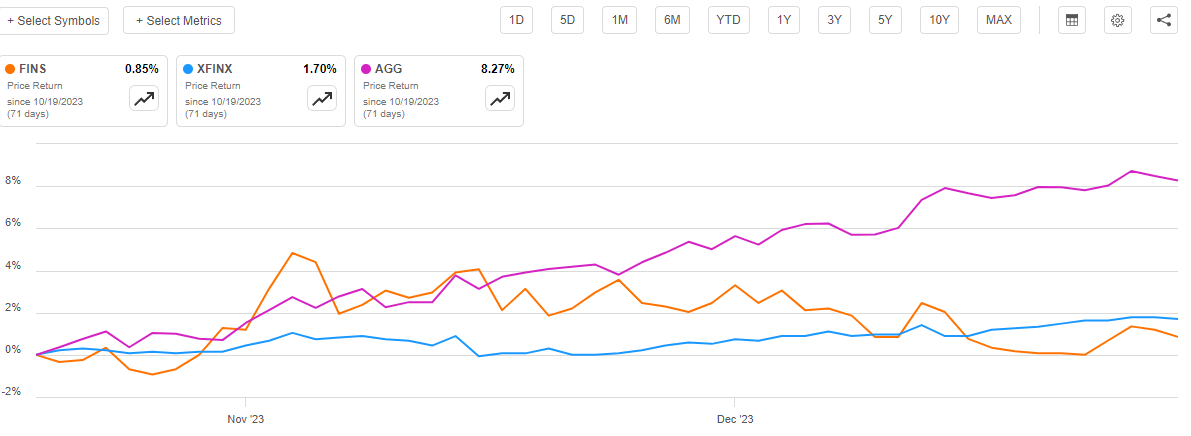

As everyone reading this is no doubt well aware, fixed-rate debt securities have generally delivered a very strong performance over the past few weeks. Ever since the middle of October, the market has been widely expecting that the Federal Reserve will slash interest rates dramatically in 2024 and investors have been bidding up the price of bonds in anticipation of this event. The Bloomberg U.S. Aggregate Bond is up 8.27% since October 19, 2023 (the date that the ten-year U.S. Treasury hit its peak yield in the current cycle). This is a much stronger performance than either the share price or the net asset value of the Angel Oak Financial Strategies Income Term Trust has managed to deliver over the same period, though:

{kind=link}

This is certainly disappointing, as right now this fund seems to be dramatically underperforming the bond market. This might be due to the floating-rate securities that it holds in its portfolio since those would not appreciate to nearly the same degree as bonds. It would be nice to know what the fund’s weighting to those securities is right now, as that would help us determine the degree to which these securities are holding the fund’s performance down compared to other factors. My big concern here is that the fund is being held back because investors are still concerned about the financial condition of many of the nation’s smaller banks in the wake of the collapse of Silicon Valley Bank ten months ago.

If the fund’s underperformance is being caused by the floating-rate securities that it holds, then that could be a good thing. As I pointed out in a recent article , the market seems to be overly optimistic about the Federal Reserve’s potential pivot. The market is expecting that there will be six rate cuts in 2024, which is highly unlikely to happen unless the economy enters into a severe recession within the next month or so. That is not especially likely to happen, so we might see a correction in the bond market. The floating-rate securities that this fund is holding should prove resistant to losses in that scenario, but the fund would need to be holding enough of these securities for them to represent a meaningful percentage of the portfolio. That may or may not be the case, as the weightings are not disclosed.

In short, this fund may or may not be a decent holding right now depending on the characteristics of the debt securities that it is holding, and it does not disclose the characteristics that we want to know for the purposes of our analysis.

Leverage

As is the case with most closed-end funds, the Angel Oak Financial Strategies Income Term Trust employs leverage as a method of boosting the effective yield from the assets in its portfolio. This was mentioned earlier in this article when we saw that the fund has a negative net cash position. I explained how the fund’s leverage works as a strategy in a number of previous articles on other closed-end funds. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase various debt securities issued by community banks and other entities. As long as the yield of the purchased securities is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the fund’s portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, so this will usually be the case. However, it is important to note that the use of leverage as a method of boosting the effective portfolio yield is not as effective today with interest rates at 6% as it was a few years ago when interest rates were basically 0%.

The use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I do not usually like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Angel Oak Financial Strategies Income Term Trust has leveraged assets comprising 28.70% of the fund’s portfolio. This is well below the one-third level that I would ordinarily prefer a fund to possess. It is also a bit lower than the leverage ratios that are possessed by many other fixed-income funds.

Overall, it appears that this fund’s leverage represents a reasonable balance between risk and reward right now. As such, we probably do not need to worry too much about its use of leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Angel Oak Financial Strategies Income Term Trust is to provide its investors with a very high level of current income. In pursuance of this objective, the fund invests in debt securities that are primarily issued by community banks all across the United States, although there are some other income-producing securities in the fund’s portfolio. These securities primarily deliver their investment returns in the form of direct payments to their owners, and the yields can be quite respectable. The fund’s current holdings have an average coupon of 5.83%, and the portfolio currently has an SEC yield of 7.72%. That is fairly reasonable in today’s environment considering that the fund is not investing in junk debt or similar assets. This fund employs leverage, which allows it to collect payments from more securities than it could control solely using its equity capital. That boosts the effective yield that the fund ends up earning. The fund collects all of the payments that it receives from the securities in its portfolio and then distributes the money to its investors, net of its own expenses. We might expect that this would give the fund’s shares a very attractive yield today.

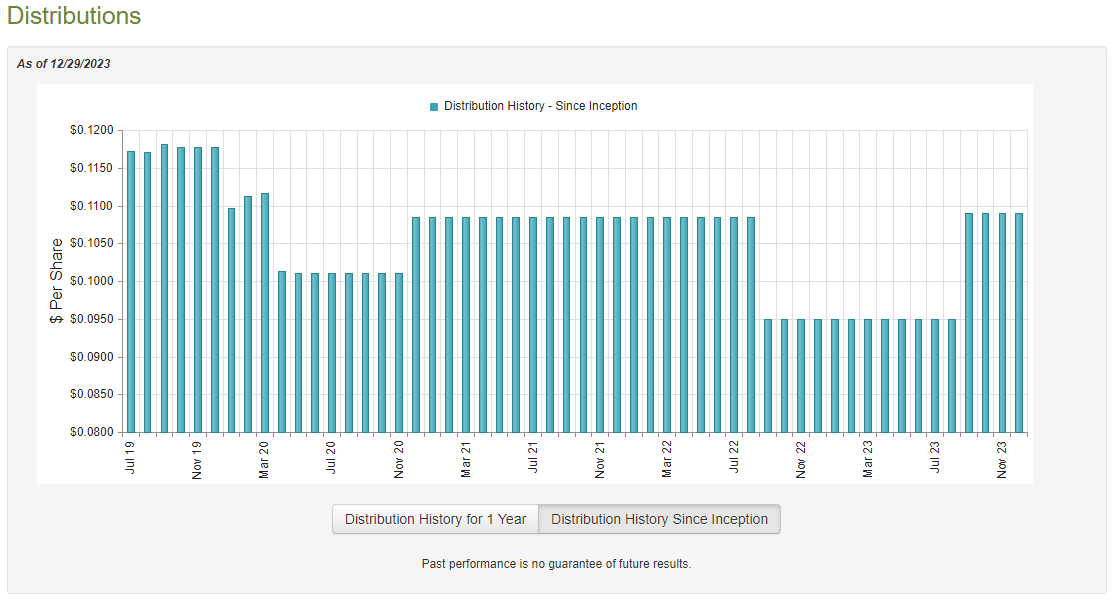

This assumption proves to be correct, as the Angel Oak Financial Strategies Income Term Trust pays a monthly distribution of $0.1090 per share ($1.308 per share annually). That gives it a 10.98% yield at the current share price. Unfortunately, this fund has not been especially consistent with respect to its distribution over the years. As we can see here, the fund has both raised and cut its distribution multiple times over its history:

{kind=link}

This history of varying the distribution seems likely to be a turn-off for those investors who are seeking to earn a safe and secure income from the assets in their portfolios. This is a group that would include many retirees, as most retirees are relying on their portfolios to fund their lifestyles and pay their bills. The fund did increase its distribution in September though, which is very nice to see. After all, in today’s inflationary environment, the cost of everything that we buy is rapidly increasing. We need more income just to maintain our purchasing power, and the fund’s recent increase should help a bit here.

As I have pointed out numerous times in the past though, anyone who is considering purchasing this fund today will not be positively or negatively affected by actions that the fund took in the past. The important thing for today’s investors is determining how well the fund can sustain its current distribution going forward. Let us investigate this.

Fortunately, we do have a fairly recent document available to use for our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on July 31, 2023. This document was linked to earlier in this article. Unfortunately, this report will not include any information about the fund’s performance over the past four months. This is a shame because that period includes both pessimistic and euphoric periods that could have caused the fund to incur losses or have the opportunity to realize some gains. This report will give us no information about the fund’s performance over that period. However, this report will include the regional banking crisis last Spring, which was probably the worst thing that happened to community banks in many years. It will be nice to see how the fund withstood the collapse of a few large banks in March and the aftermath of that crisis.

During the six-month period, the Angel Oak Financial Strategies Income Term Trust received $13,791,177 in interest along with $1,926,515 in dividends from the assets in its portfolio. This gives the fund a total investment income of $15,717,692 over the six-month period. The fund paid its expenses out of this amount, which left it with $8,960,493 available for shareholders. Unfortunately, that was nowhere near enough to cover the $14,285,704 that the fund paid out in distributions during the period. At first glance, this is likely to be quite concerning, as we would normally prefer a fixed-income fund to fully fund its distributions out of net investment income. This fund is obviously failing to accomplish that task.

However, there are other methods through which a fund can obtain the money that it needs to cover its distributions. For example, it might be able to capitalize on the price appreciation that fixed-rate bonds exhibit when interest rates decline and realize some capital gains. The first half of 2023 was characterized by falling long-term interest rates, so there might have been an opportunity for this fund during that period. Unfortunately, this fund generally failed to earn money from alternative sources during the period. It reported net realized losses of $1,939,541 and had an additional $15,997,479 net unrealized losses over the period. Overall, the fund’s net assets declined by $23,262,231 after accounting for all inflows and outflows during the period. This is very concerning as it strongly suggests that the fund cannot afford the distributions that it paid out.

The fund has not managed to correct this problem despite the improved market that has existed since mid-October. As we can see here, the fund’s net asset value per share is down 0.44% since August 1, 2023:

{kind=link}

This is not horrible, and if the market strength continues over the next few months, then the fund might be able to sustain its distribution at today’s level. However, there is no guarantee that this will be the case and there are a lot of reasons to believe that the Federal Reserve will not reduce interest rates to nearly the degree that the market has priced in. As such, the fund might struggle to cover its distribution. This is something that we should keep an eye on going forward.

Valuation

As of December 29, 2023 (the most recent date for which data is available as of the time of writing), the Angel Oak Financial Strategies Income Term Trust has a net asset value of $13.72 per share but the shares currently trade for $11.90 each. This gives the shares a 13.27% discount on net asset value at the current level. This is a much better price than the 10.77% discount that the shares have had over the past month. As such, the current price does represent a reasonable entry price.

Conclusion

In conclusion, the Angel Oak Financial Strategies Income Term Trust is a very under-followed fund that appears to offer investors the opportunity to invest in small local banks and still earn a very attractive yield. That is a proposition that might prove to be attractive to some readers. However, the fund’s performance history is not especially attractive, and it is not as transparent with its holdings as I would like to see. In particular, the interest-rate risk here is very hard to judge. The fund also may not be able to sustain its distribution if the market turns against it. As such, it does not really make sense to buy the fund today despite the relatively attractive discount. I cannot really see a reason to sell it if you already have it though, so the hold rating is probably appropriate.

For further details see:

FINS: This Unique CEF Is Nice As A 'Feel Good' Investment, But It Is Nothing Special