FFWM - First Foundation: A Steep Discount For A Risky Prospect

2023-10-16 16:26:06 ET

Summary

- First Foundation is a cheap financial services company trading at low multiples and a significant discount to book value.

- The company operates a bank catering to small and medium-sized businesses, with a focus on loans secured by multifamily properties.

- Despite a decline in net interest income and profits, the company has seen growth in deposits and has low uninsured deposit exposure.

- It does appear to be a risky prospect, but the cheap share price indicates great upside potential as well.

Since March of this year, I have been searching for some of the cheapest small financial companies on the market. The original impetus for this search was the banking crisis that enveloped the banking industry. While I have come across some very cheap firms during this search, the cheapest so far has got to be First Foundation ( FFWM ). Shares of the company are trading at very low multiples, including at a significant discount to its book value. At first glance, this may make it seem as though the bank is a fantastic buying opportunity. But the market is not that inefficient. When you dig deeper, you do see some problems with the bank. Though at the end of the day, they are not enough to stop it from being a decent ‘buy’ prospect for investors who don't mind a little extra risk.

A severe discount

Before I get into the nuts and bolts of the institution, we should first have a better understanding of the company and what it does. As I mentioned already, First Foundation operates as a financial services company, with operations spread throughout California, Nevada, Florida, Texas, and Hawaii. Primarily, the company operates a bank that caters mostly to small and medium-sized businesses. They also do provide business banking products and services to professional firms, as well as to individuals and families. All of this is done through the 31 different branches that the company has in operation.

The banking products that the company offers are what you would expect to find at a small regional or local bank. Examples include, but are not limited to, the acceptance of deposits, and the origination of a wide variety of loans. Specific loan product examples would be loans that are secured by multifamily and single-family real estate, as well as commercial properties, land, and construction projects. The company also provides loans for commercial and industrial purposes and it has a small amount of consumer loans on its books as well. In addition to the traditional banking services, First Foundation engages in wealth management activities. For instance, it has a fee based investment advisor that provides investment advisory and wealth management services for individuals and their families.

{kind=link}

Author - SEC EDGAR Data

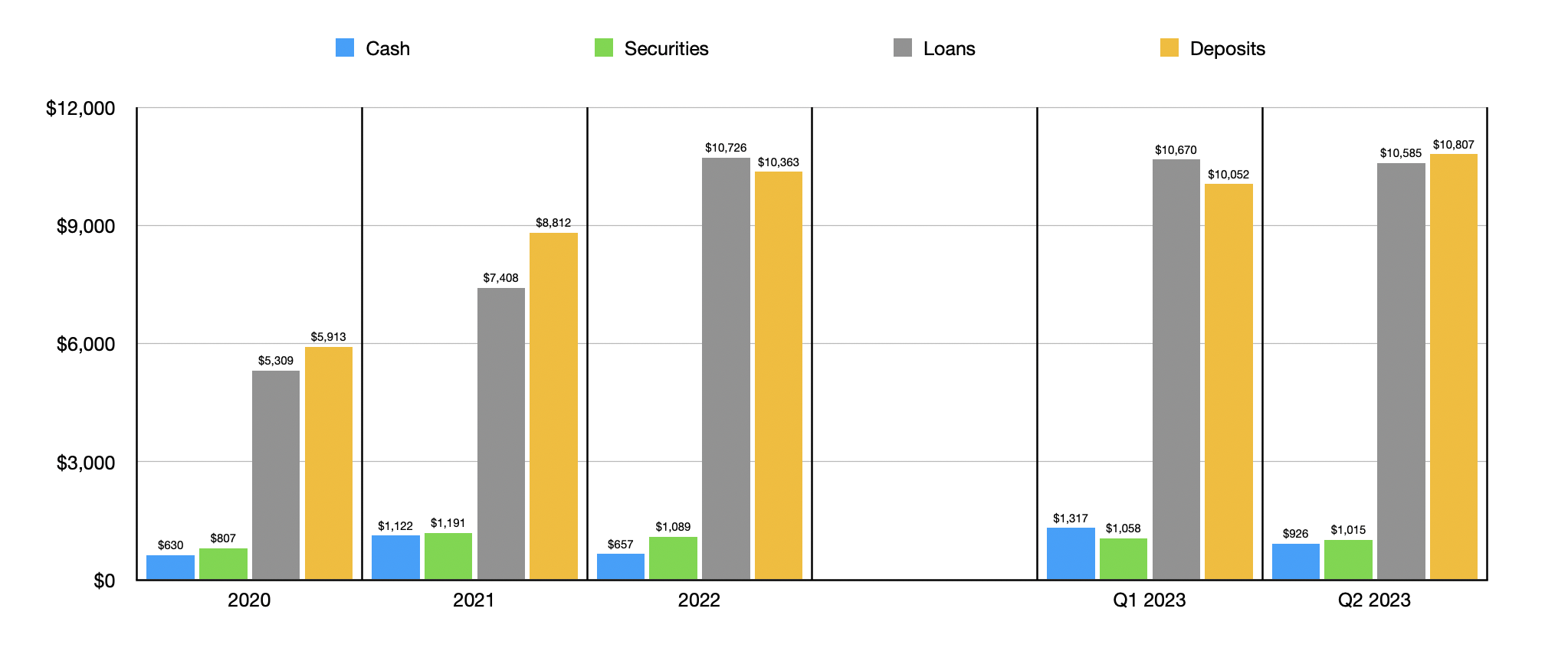

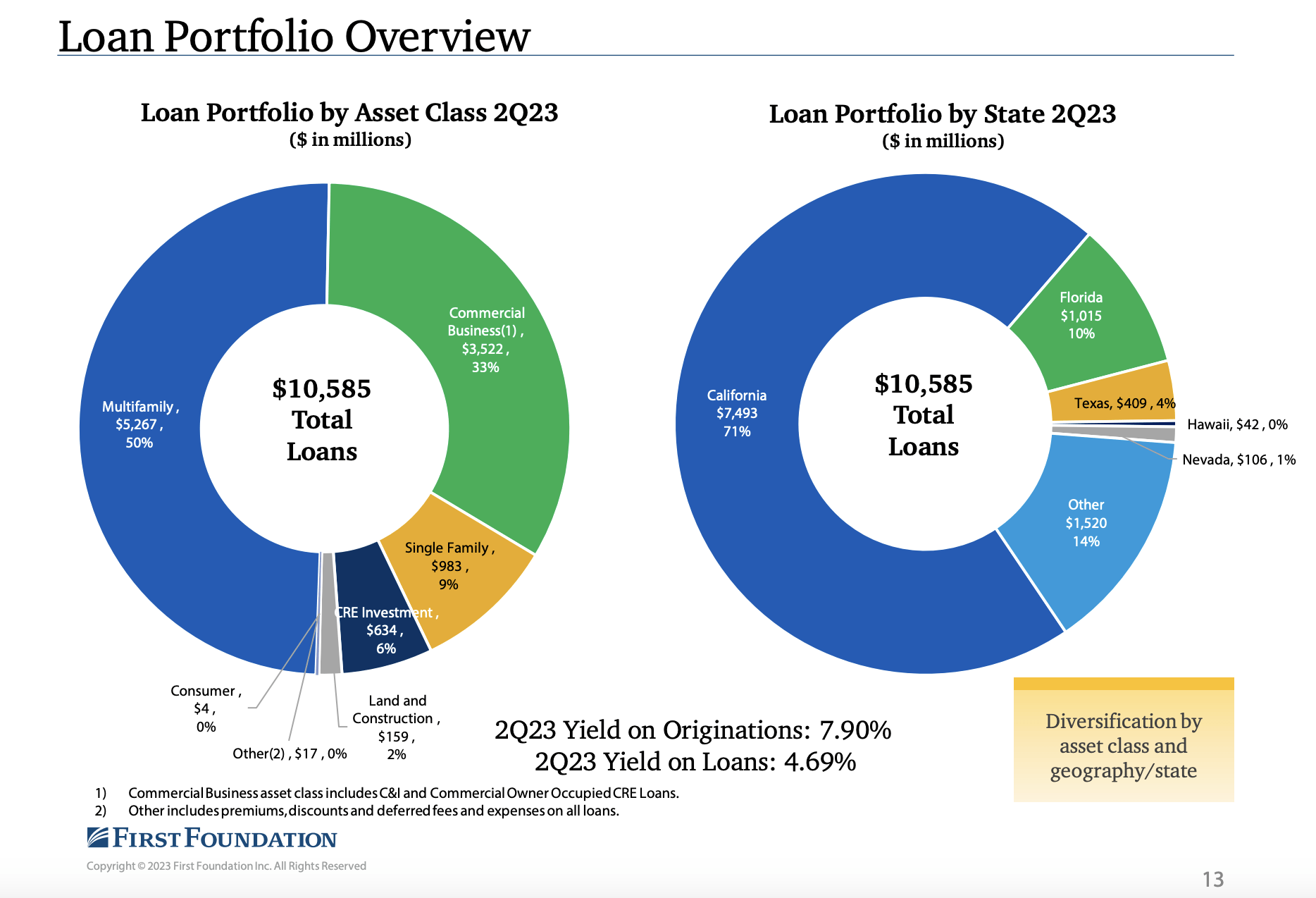

Over the past few years, management has done a stellar job growing the value of loans on its books. These grew from $5.31 billion in 2020 to $10.73 billion in 2022. We have seen them slip a bit since then, with loans dropping to $10.59 billion. Of these, 50%, or roughly $5.27 billion, are dedicated to multifamily properties. The next largest area of concentration is commercial business at 33%. This is followed up by a very distant third place for single family exposure at only 9% of the company’s total loan portfolio. Geographically, the biggest area of focus for the enterprise has historically been California. 71% of its loans, by value, come from that state. Florida is the next largest at a paltry 10%.

{kind=link}

First Foundation

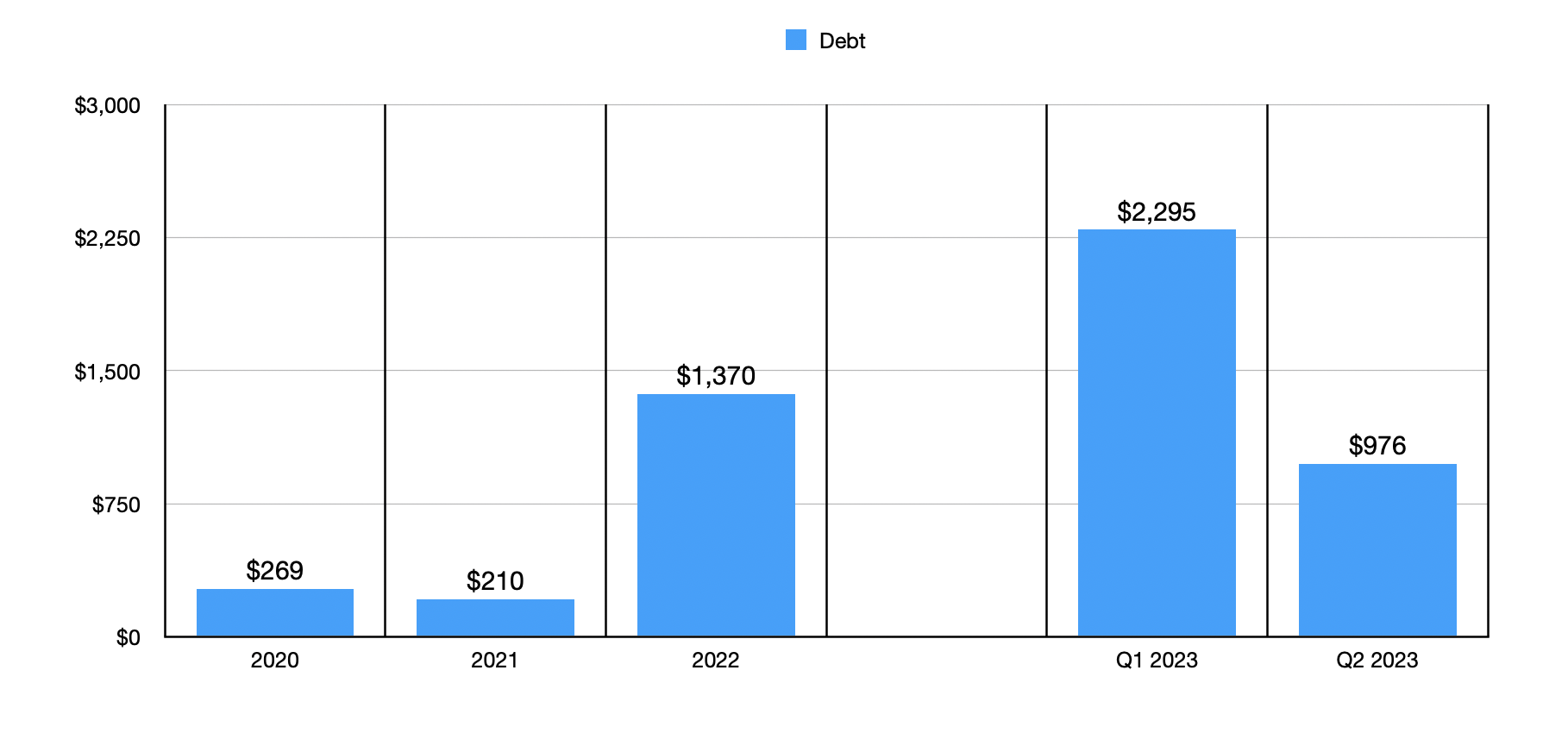

There are, of course, other areas of the balance sheet that require some attention. For instance, cash for the bank has always jumped around in a very wide range, with a low point in recent years of $629.7 million and a high point of $1.32 billion. As of the end of the second quarter of this year , cash totaled $926.1 million. The company does have $975.5 million in debt on its books, which is down considerably from the $2.29 billion reported one quarter earlier. But fortunately, it has $1.02 billion worth of securities on its books to help offset this. For context, 81% of these securities, by value, are classified as mortgage-backed securities.

{kind=link}

Author - SEC EDGAR Data

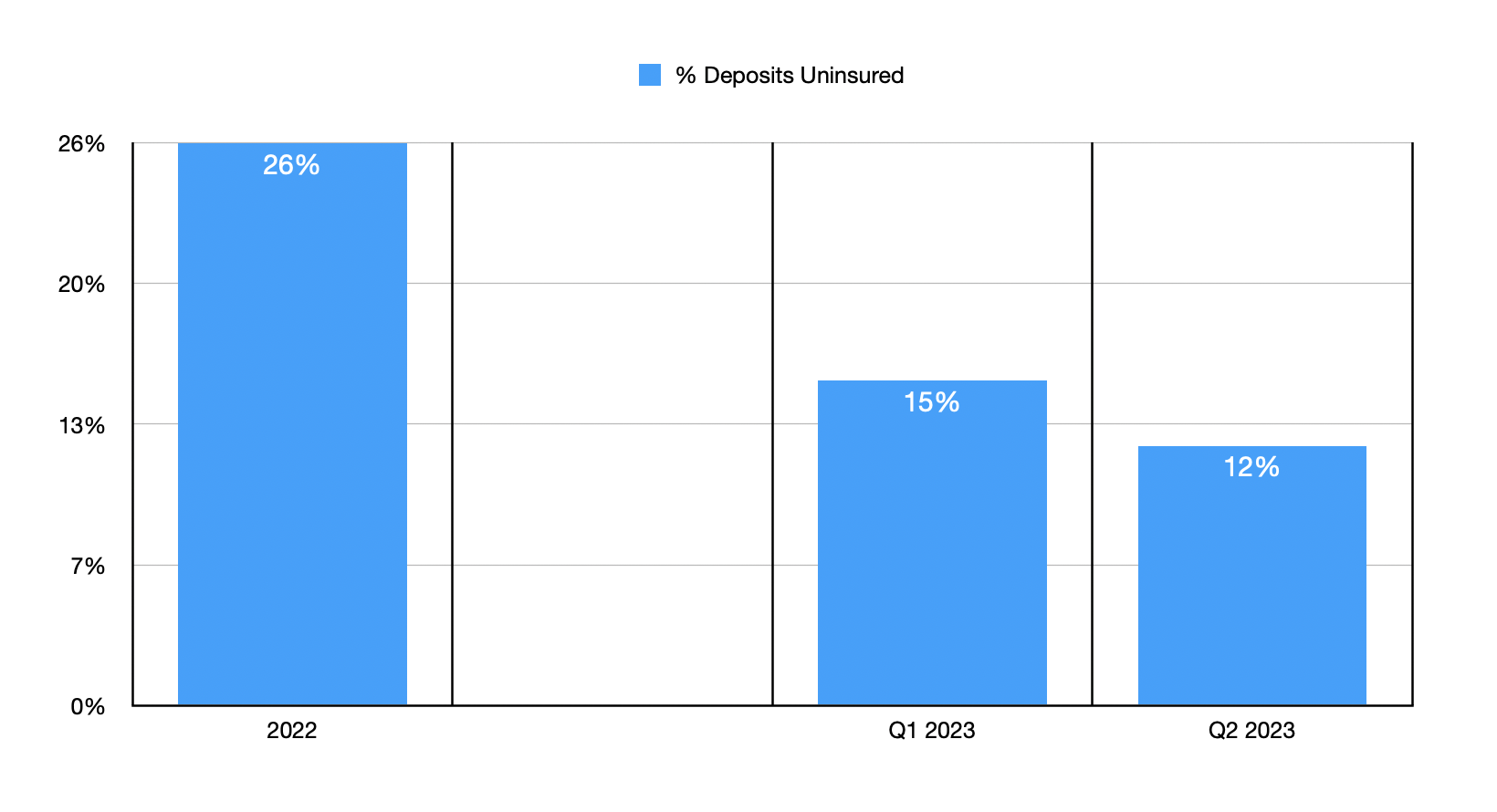

The growth in loans on the company's books would not have been possible if it weren't for significant growth in the deposits that the bank has. These nearly doubled from $5.91 billion back in 2020 to $10.36 billion by the end of 2022. There was a decline to $10.01 billion in the first quarter of this year, with that drop likely driven by the banking crisis. After all, banks that were most heavily exposed to California were the ones initially impacted the most. So that wouldn't be a surprise here. But that decline was short lived. I say this because, by the end of the second quarter, deposits had grown to an all-time high of $10.81 billion. Even as deposits grew, the exposure that the bank has to uninsured deposits dropped. By the end of last year, uninsured deposit exposure was 26%. That number has been cut by more than half to only 12% as of the second quarter.

{kind=link}

Author - SEC EDGAR Data

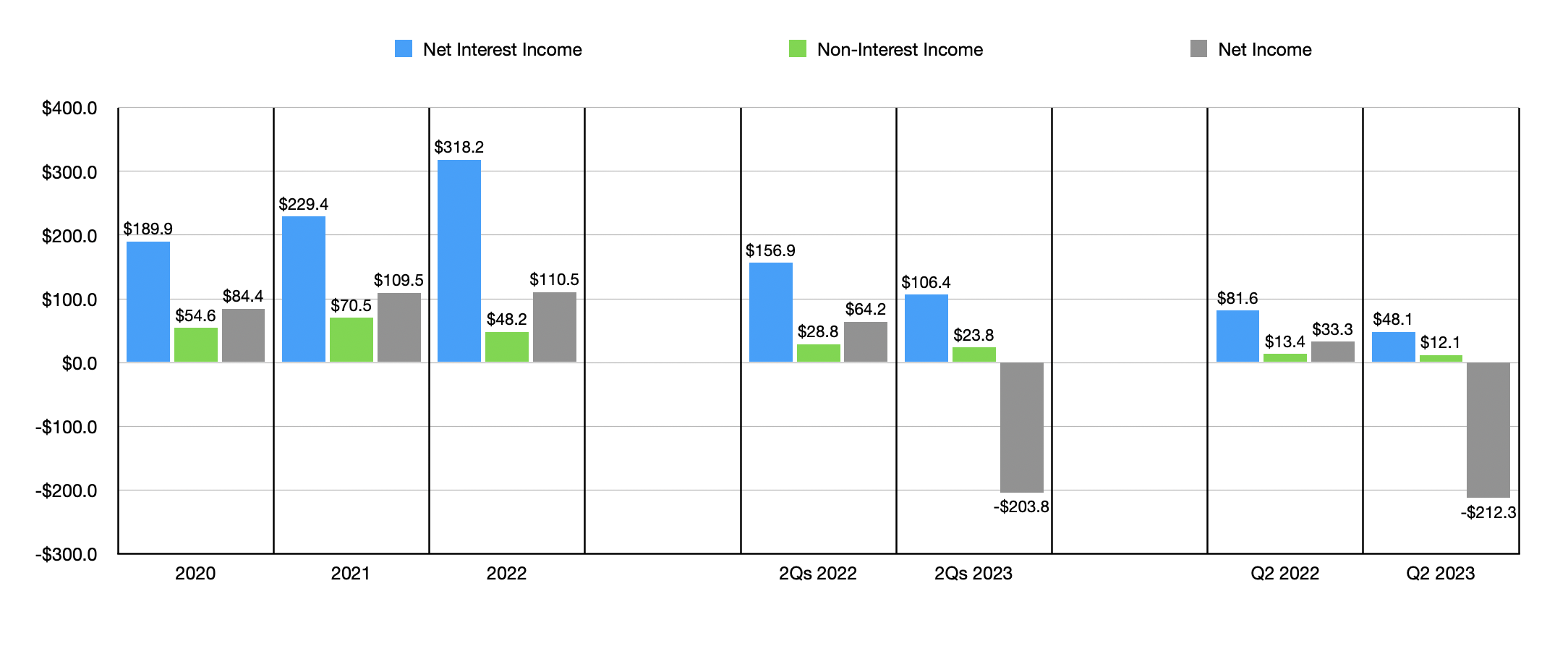

With growing deposits and loans also came a growing income statement. Net interest income grew from $189.9 million in 2020 to $318.2 million in 2022. We did see non-interest income bouncing around a bit, but the general trend there has been lower. But that didn't stop net income from expanding from $84.4 million to $110.5 million. While all of this looks fine, this year has been a bit more problematic. You see, for the first half of the year, net interest income was only $106.4 million. That's down from the $156.9 million reported the same time last year. Non-interest income dropped from $28.8 million to $23.8 million. And even more significant was the decline in net profits from $64.2 million to negative $203.8 million.

{kind=link}

Author - SEC EDGAR Data

It might be easiest to first address the low hanging fruit. And this is the $215.3 million goodwill impairment that the company incurred in the second quarter. This kind of activity is done when certain assets that the company paid more than the fair market value of the assets for end up being lower than the ultimate price that the company paid. The good news is that this is a non-cash charge. But just doing the math in your head really quick, you would see that even removing this would have resulted in a rather meaningful decline in profits. And this leads us to the biggest problem that the institution faced that was not a non-cash item.

The issue at hand is the net interest margin. Even as the weighted average interest earning assets at the bank grew nicely, the net interest margin contracted from 3.10% to 1.67%. A surge in average borrowings from $314.3 million to $1.63 billion, combined with a higher interest rate on those borrowings of 4.89% compared to the 2.02% seen one year earlier, was largely responsible for this. But the company also saw the cost of keeping deposits (money market, savings accounts, and CDs) grow materially from the first half of last year to the first half of this year. Most notable was the increase in rates that the company had to pay for the CDs at its shop. The interest rate went from 0.37% to 4.26%. Similar increases were seen when it came to the other two aforementioned items. This more than offset the rise in gross interest income that the company got from its assets.

At the end of the day, what this shows is that the bank had to take a rather large hit in order to keep depositors at the institution. It is telling that most of the pain occurred in the second quarter of the year. In short, in response to painful market conditions, the institution ended up having to ratchet up how much it compensated depositors in order to keep the funds flowing in. This strategy worked, but it wasn't exactly a pleasant outcome for those wanting profits to continue rising. A lot of the concern about the company and its potential likely revolves around how long the company will have to keep these rates up in order to keep funds in the door. What I will say is that I believe there has been a considerable improvement in sentiment regarding banks, even as interest rates have crept up further. And I also believe that next year will see rates gradually decline.

{kind=link}

Author - SEC EDGAR Data

If my assessment turns out to be correct, then shares of the company will be some of the cheapest out there. If we assume an eventual return to the kind of performance seen in 2022, the company would be trading today at a forward price to earnings multiple of 3.1. The price to book ratio is only 0.37, while the price to tangible book ratio is 0.38. The industry average for the price to earnings multiple right now is somewhere around 10.4. So this does imply rather significant upside if things go well.

Takeaway

Based on the data provided, First Foundation is definitely an interesting prospect that fans of the banking sector should keep in mind. I am slightly worried about the significant contraction in net interest margin. But I like that debt has fallen recently and their deposits have returned to growth. Uninsured deposit exposure is quite low compared to many of the other banks that I have seen. And given how cheap the stock is, both relative to earnings and its book value, I would say that a solid ‘buy’ rating makes sense, so long as the investors picking up the stock are comfortable with risk that is higher than what you would normally expect.

For further details see:

First Foundation: A Steep Discount For A Risky Prospect