SBNY - First Republic Bank: As Always JPMorgan Comes To The Rescue

2023-05-01 14:50:44 ET

Summary

- JPMorgan Chase & Co. once again takes the lead when things go wrong.

- The purchase of First Republic Bank may have been a bargain, but it is not without risk.

- This could be the beginning of a new financial crisis.

History repeats itself

Years go by, and yet very little has changed: when the financial system gets into trouble, the reference point for finding a solution always remains JPMorgan Chase & Co. ( JPM ).

- In 1907 due to poor banking decisions, a general sentiment of distrust toward the banking system was created. To save the country and avert a dangerous bank run, JPMorgan lent its funds to limit the damage of the financial crisis.

- In 2008 a reckless regulation of credit risk was the cause of the famous financial crisis associated with sub-prime mortgages. There, too, JPMorgan stepped in by purchasing Bear Stearns and Washington Mutual.

- In 2023, regulators, after seizing First Republic Bank ( FRC ), promptly sold most of its assets to JPMorgan with the aim of limiting the feeling of distrust toward the banking system.

So, years of history suggest how JPMorgan is the anchor of the entire financial system, and when the Fed can do nothing, we know who is going to intervene. Moreover, it is interesting to note that in this case the law was also set aside, in fact according to the Riegle-Neal Interstate Banking Act of 1994 , a bank holding company cannot control more than 10 percent of the nation's total deposits, yet with this takeover it happened. But after all, it was to be expected, for JPMorgan the government can turn a blind eye. Here are Jamie Dimon's words on the matter:

Our government invited us and others to step up, and we did. Our financial strength, capabilities and business model allowed us to develop a bid to execute the transaction in a way to minimize costs to the Deposit Insurance Fund.

Details of the acquisition and what it means for JPMorgan

For anyone interested in the full details of the acquisition, you can check out this link . Instead, for those interested in the highlights, here are the most important ones:

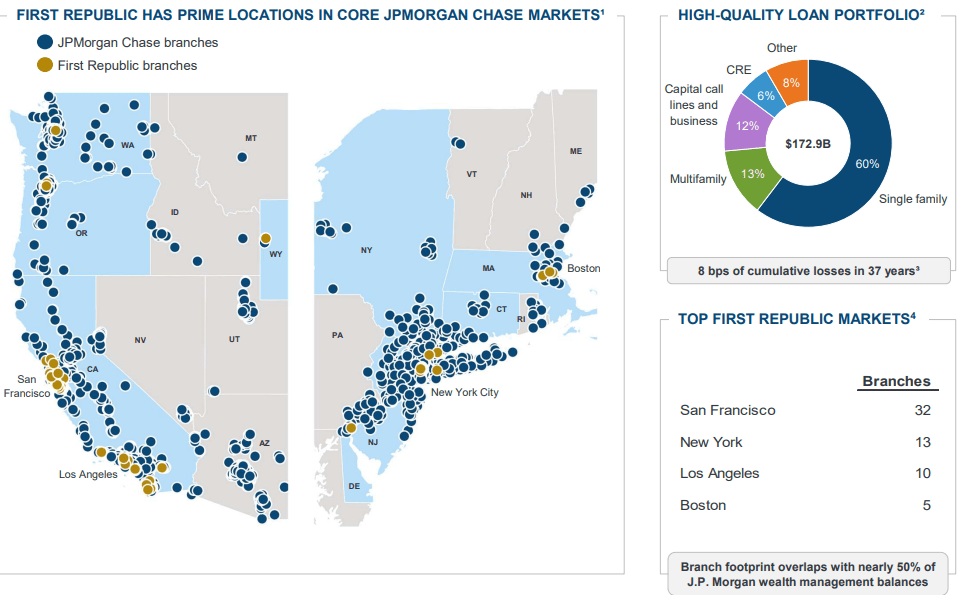

- JPMorgan will pay $10.60 billion to the FDIC for the acquisition of most of the assets and some of the liabilities of First Republic Bank. Precisely, among assets $173 billion of loans and $30 billion of securities; among liabilities about $92 billion of deposits and $28B of FHLB advances. Corporate debt and preferred stock were not assumed.

- The $30 billion deposited by large U.S. banks in aid of First Republic a few weeks ago will be repaid, including $5 billion from JPMorgan itself. In addition, First Republic's branches and offices will be regularly active and some of them will be converted into new JPMorgan wealth centers.

So, in light of these considerations, was it worth it for JPMorgan? In my opinion yes, but there is a premise to be made.

It is clear that behind this acquisition, also based on Jamie Dimon's words, there was the strong will of the government for it to go through. So rather than a choice to buy First Republic my sense is that it was almost an imperative. I see a lot of similarities with what happened a few weeks ago in Switzerland, when the Swiss authorities designed a takeover plan to make it possible for UBS to acquire Credit Suisse. That said, this does not necessarily mean that JPMorgan made a bad deal, in fact I think it is the opposite, and there are three main reasons why I think so.

Why I consider it a good deal

The first reason is that there are some guarantees and financial aid for JPMorgan within the agreement.

The FDIC will provide loss-sharing arrangements to most of the loans acquired. Specifically, for single-family residential loans there will be 80 percent loss coverage for seven years; for commercial loans there will be 80 percent loss coverage for five years. These guarantees are very important, as they limit the risks related to these assets and consequently will not worsen the minimum capital requirements under Basel III regulations. The CET1 ratio remains within the target of 13.50% for Q1 2024. In addition, the FDIC will provide a new $50 billion five-year fixed-rate financing to reduce the duration gap and improve the balance of the capital structure.

JPMorgan Press Releases

The second reason is that getting First Republic's clients and its branches is an important value-add for JPMorgan.

First, because First Republic's clients tended to be wealthy individuals who benefited from the excellent service this bank provided. Their financial position is stable, so making new loans to these individuals involves relatively little risk. In addition, they could benefit from other services provided by JPMorgan.

Second, new branches would be available in wealthy markets, increasing JPMorgan's national footprint in these markets.

{kind=link}

The third reason concerns the income benefits.

While JPMorgan expects to spend $2 billion in restructuring costs over the next 18 months, it will realize a one-off gain of $2.6 billion from this deal. In addition, the deal has IRR above 20 percent and net income is expected to increase by $500 million.

Overall, for these three reasons, I evaluate the whole operation as positive. In any case, it is too early to say whether JPMorgan has made a bargain or not. Certainly, the market reacted well to the news, but let's also consider that the deal happened in a very narrow time frame despite its magnitude. Over time the acquisition of First Republic may turn out not to be as profitable as hoped, and this is a risk to consider. It could be that JPMorgan has been working on the acquisition for weeks, but government pressure may have accelerated the process and led to a rushed conclusion. After all, there is not always time to think carefully when the banking system is asking for immediate help.

My take on what will happen after FRC's failure

To know a priori whether JPMorgan has once again lifted the financial system is difficult if not impossible to say, but here is my humble opinion on the matter. I will try to be as brief and concise as possible.

Based on history, the moment banks start to fail it tends to be a sign of strong weakness in the banking system, which then results in a financial crisis. Banks are at the heart of any economy, because if they stop lending money it stops both businesses and households. Few can buy homes without a mortgage, just as few businesses can grow without the possibility of taking on debt.

Over the past few years, the Fed's aggressive monetary policy has led interest rates to rise abruptly, and both banks and households have quickly found themselves faced with an entirely different macroeconomic environment. As interest rates are high, banks have less and less incentive to lend, as do both businesses and households since they will be forced to pay higher interests. To make matters worse, there are the large unrealized losses of held-to-maturity securities that weaken the financial strength of the banks that own them. The latter was the reason behind the failure of SVB, which subsequently triggered within the economy a sentiment of distrust toward regional banks with a prevalence of uninsured deposits. Then it was Signature Bank's turn and now it is First Republic's turn, despite originally being a great bank.

{kind=link}

Together, FRC, SVB and SBNY are the second, third and fourth largest bank failure in U.S. history, respectively. But there is more.

In the current situation, the Fed cannot even quickly cut interest rates to stimulate the economy again, because this move would only further fuel inflation. It is basically an extremely complex situation that I personally do not see how it cannot culminate in a financial crisis. After years of economic expansion, a time of contraction has probably arrived.

After all, Jamie Dimon already warned us a month ago:

The current crisis is not yet over, and even when it is behind us, there will be repercussions from it for years to come.

For further details see:

First Republic Bank: As Always, JPMorgan Comes To The Rescue