WAL - First Republic Vs. Western Alliance Stock: Which Is The Better Value Buy?

2023-04-06 09:00:00 ET

Summary

- Both First Republic and Western Alliance have taken a beating this year, as fears mount that they might succumb to contagion following the collapse of Silicon Valley Bank.

- Each firm is vulnerable in its own way, but we will only know the bigger picture when the businesses report financial results in the coming days.

- Heading into earnings, Western Alliance looks like a more solid opportunity for investors.

In the coming days, two different but very interesting banks will be reporting financial results covering the first quarter of their 2023 fiscal years. This is a particularly important moment for both banks because it will represent the first comprehensive data release from these entities since the banking crisis began in early March. On the one hand, you have Western Alliance Bancorporation ( WAL ), which is down 50.7% so far this year. And on the other, you have First Republic Bank ( FRC ), which has fallen 89%. Both of these companies have been pushed down because of concerns about the contagion spreading to them. But with the stock down so much, there also exists some opportunity of tremendous upside if things go right.

Operationally, Western Alliance is the better of the two companies. Its historical financial growth has far outpaced what First Republic Bank has seen. At the same time, recent data provided by management has further stoked fears in the investment community, with its most recent update sending shares plunging 12.4% on April 5th. At the core of this is concern about a shrinking deposit base and a lack of transparency regarding the company's financial condition. First Republic Bank may not be as high-quality an operation. The company also suffers from a tremendous lack of clarity. But because of how far shares have fallen, the upside potential from here if things go well could be greater than with Western Alliance. Because of these circumstances, investors would be very wise to pay attention to what both companies report in the coming days. More now than perhaps any time in their history, the news that should come out could have a permanent and significant impact on the future of the businesses.

A primer on Western Alliance

Before I dive into expectations, it would be helpful to provide a little bit of data regarding Western Alliance and its operations. Located in Phoenix, Arizona, the company is a rather sizable bank. Total assets at the end of its 2022 fiscal year came in at $67.7 billion. It had $52.7 billion in loans on its books, fueled by $53.9 billion in deposits. Although the company is headquartered in Arizona, it has locations spread between not only that state, but also Nevada, California, Georgia, Texas, Massachusetts, Illinois, Colorado, Minnesota, New York, Washington, and Virginia. Customers at the bank have a wide variety of solutions that they can tap into.

{kind=link}

Under the Commercial segment, the company provides commercial banking and treasury management products and services to small and middle-market businesses. It also offers financial services to the real estate industry, and more. The Consumer Related segment of the company offers both commercial banking services to enterprises in consumer-related sectors, as well as consumer banking services like residential mortgage banking.

{kind=link}

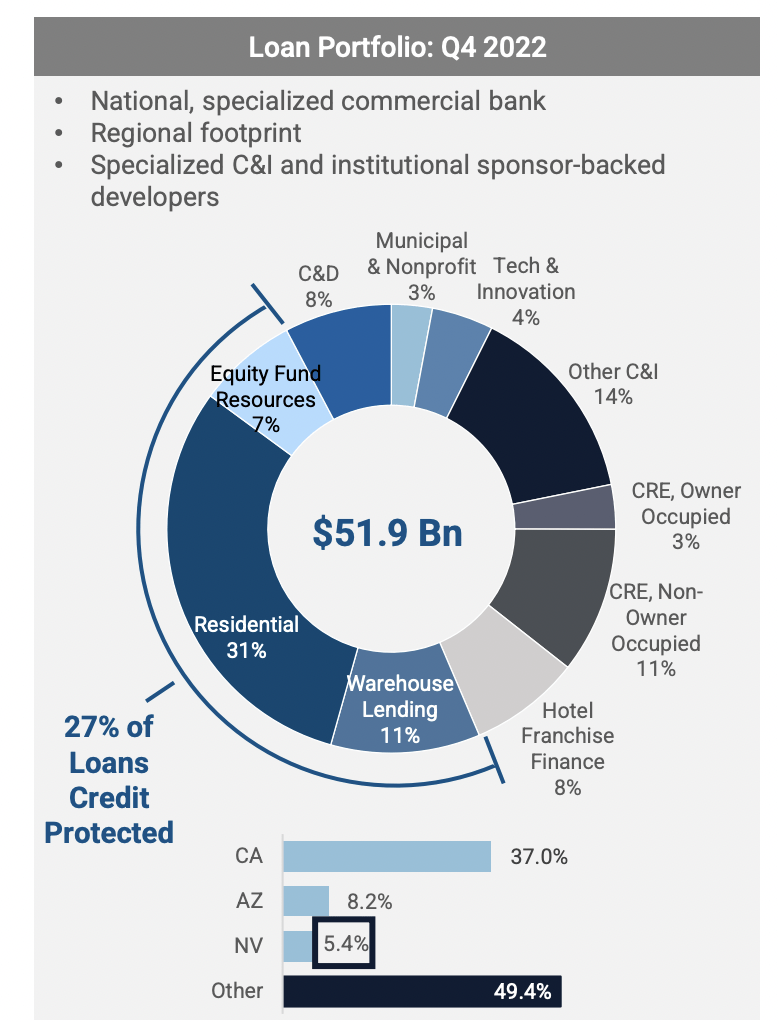

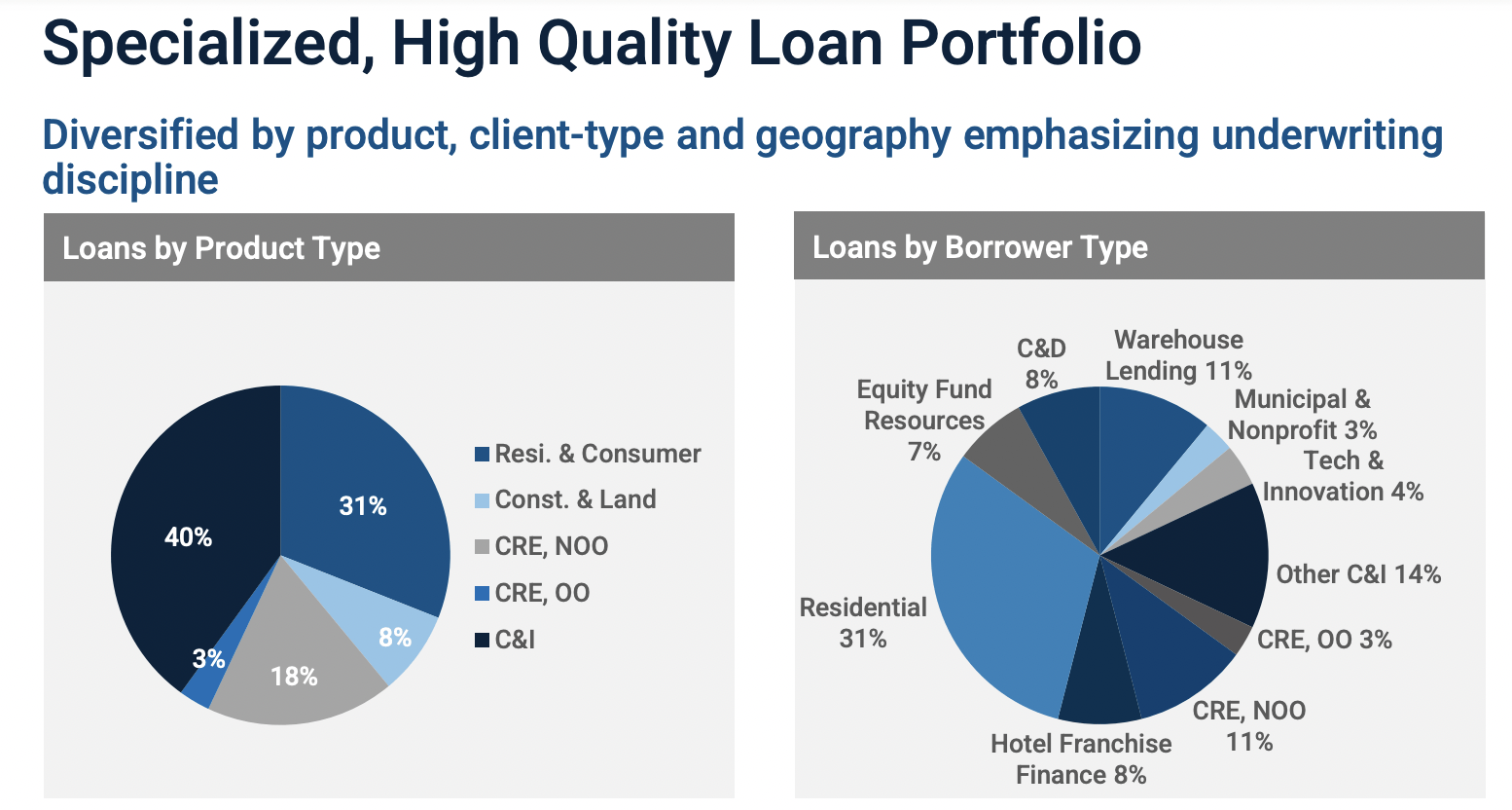

Sticking to the most recent data available, about 40% of the company's loan portfolio fell under the residential and consumer category. Another 31% of its loans were construction and land loans. When it comes to specific borrower type, the greatest exposure to the company is the residential market, totaling 31% in all. I know that one area that investors are currently worried about is the technology and startup space. Only about 4% of its loans have been made out to technology and innovation companies, with another 7% made out to equity fund resources. The latter of these is what management calls the niche that includes venture capital and private equity funds.

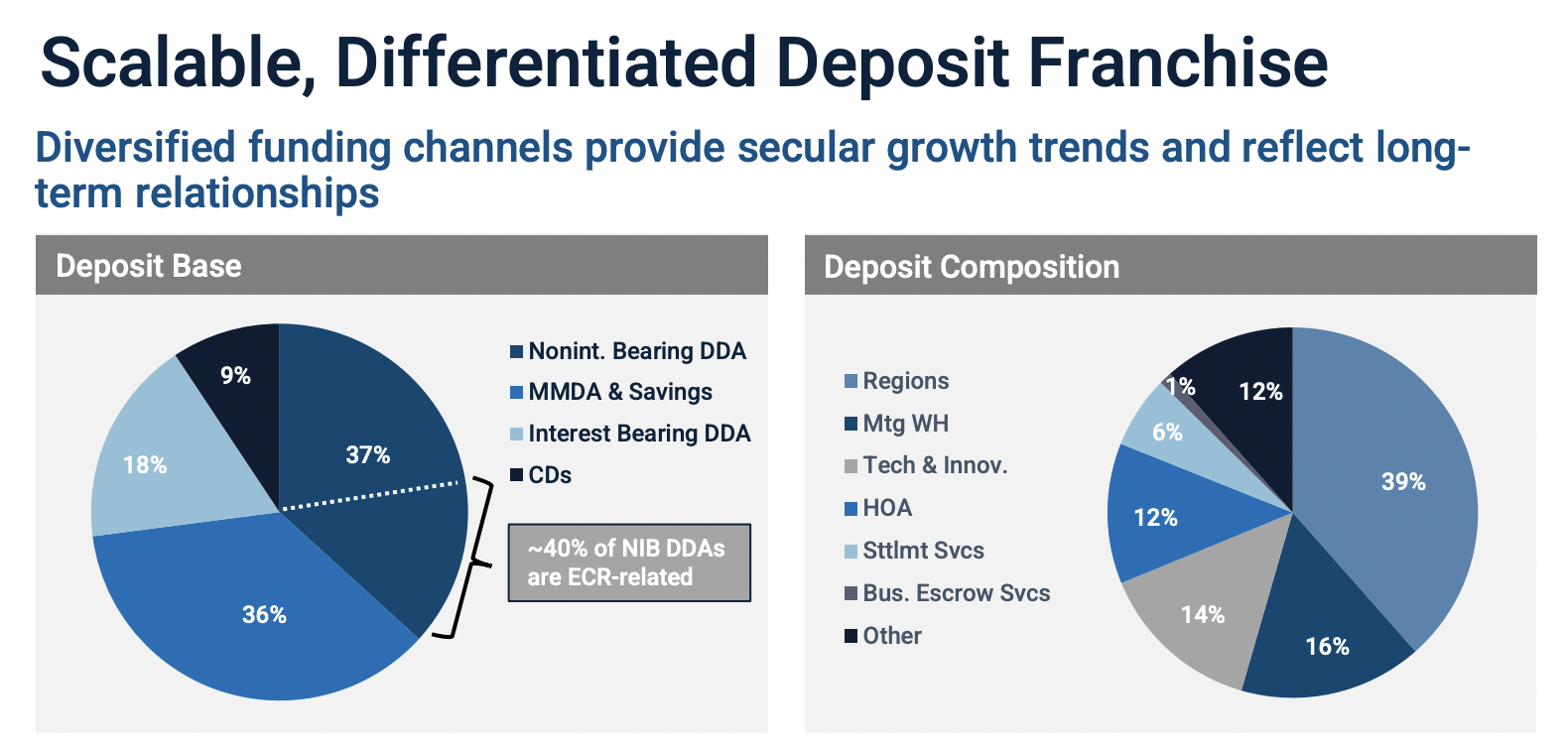

On the deposit side of things, the company is a little more exposed. And that is where a lot of the focus likely is at this time. About 14% of its deposits as of the end of last year fell under the technology and innovation category. There was no specific data covering the equity funds resources activities. But we do know that about 12% of deposits include miscellaneous other categories.

{kind=link}

Watch WAL Stock

On April 19th, after the market closes, the management team at Western Alliance is expected to announce financial results covering the first quarter of the company's 2023 fiscal year. At this moment, analysts anticipate the company generating revenue of $702.6 million. By comparison, that number last year, net of interest expense, was $546.8 million. Earnings per share, meanwhile, should come in at $2.25. That represents a modest improvement over the $2.22 per share reported in the first quarter of 2022. If management achieves the earnings per share anticipated of it, this should work out to roughly $242.1 million. That would be 2.2% higher than the $236.9 million reported one year earlier.

While the headline news is most certainly important, it is far from the most important data that investors should be watching for. Most significantly, investors should be paying attention to the deposit base of the company. On April 4th, the management team at the firm provided some data for investors. But because of how vague the data was, it further stoked fears about the company and its prospects moving forward. For instance, the only substantive discussion of deposits is that, as of the end of March of this year, 68% were insured . That compares to the 55% that were insured as of March 16th of this year.

At first glance, this may seem like a positive development. But as others have pointed out, it's more likely that the company suffered from an outflow in deposits that largely happened to be uninsured than benefited from an increase in overall deposits. If so, this would mark a significant turn from data earlier in the month of March. On March 9th, for instance, management said that deposits were $61.5 billion. That was 7.8% higher than what they were at the end of 2022. Already at that time, the technology and innovation space was showing some weakness, with overall deposits for the partial first quarter of the year seeing a $201 million decline in deposits under the technology and innovation category. Though this was offset some by $118 million rise in deposits split between equity fund resources and life sciences. Management did assure investors that they had adequate liquidity, with a coverage ratio greater than 140% of what uninsured deposits were. But beyond that, there really wasn't much to tell in that press release.

Watch First Republic Bank

At this point, I have already written two other articles dedicated to First Republic Bank. Instead of rehashing details about it, including recent changes in its overall financial condition, I would urge you to read both of those articles here and here . To be honest, I would have liked to have dug deeper into some additional numbers on this front. But management has not provided a substantive update since the last article I published on the company on March 19th of this year. My overall conclusion was that the lack of transparency by management was harming what could be an excellent opportunity for investors.

Leading up to the earnings release, analysts have formed a general consensus as to what the company should report to be. The current expectation is for the business to report revenue of roughly $1.09 billion. It's unclear if this refers to net interest income only, or if it refers to overall revenue. For context, net interest income in the first quarter of the 2022 fiscal year was $1.14 billion. Total revenue, which takes net interest income and adds to it non-interest revenue, was $1.39 billion. On the bottom line, the expectation is for the company to report earnings per share of $0.44. Adjusted earnings, meanwhile, should be $0.51 per share. For context, earnings per share in the first quarter of 2022 came out to $2, with the company generating net profits of $364 million. If analysts are correct about the first quarter results, the company should generate net profits of only $80.5 million, with adjusted profits of $93.3 million. Just like with Western Alliance, I also believe that investors should be paying very close attention to the deposit and loan data provided by the company, especially uninsured deposits.

Western Alliance is superior than First Republic

{kind=link}

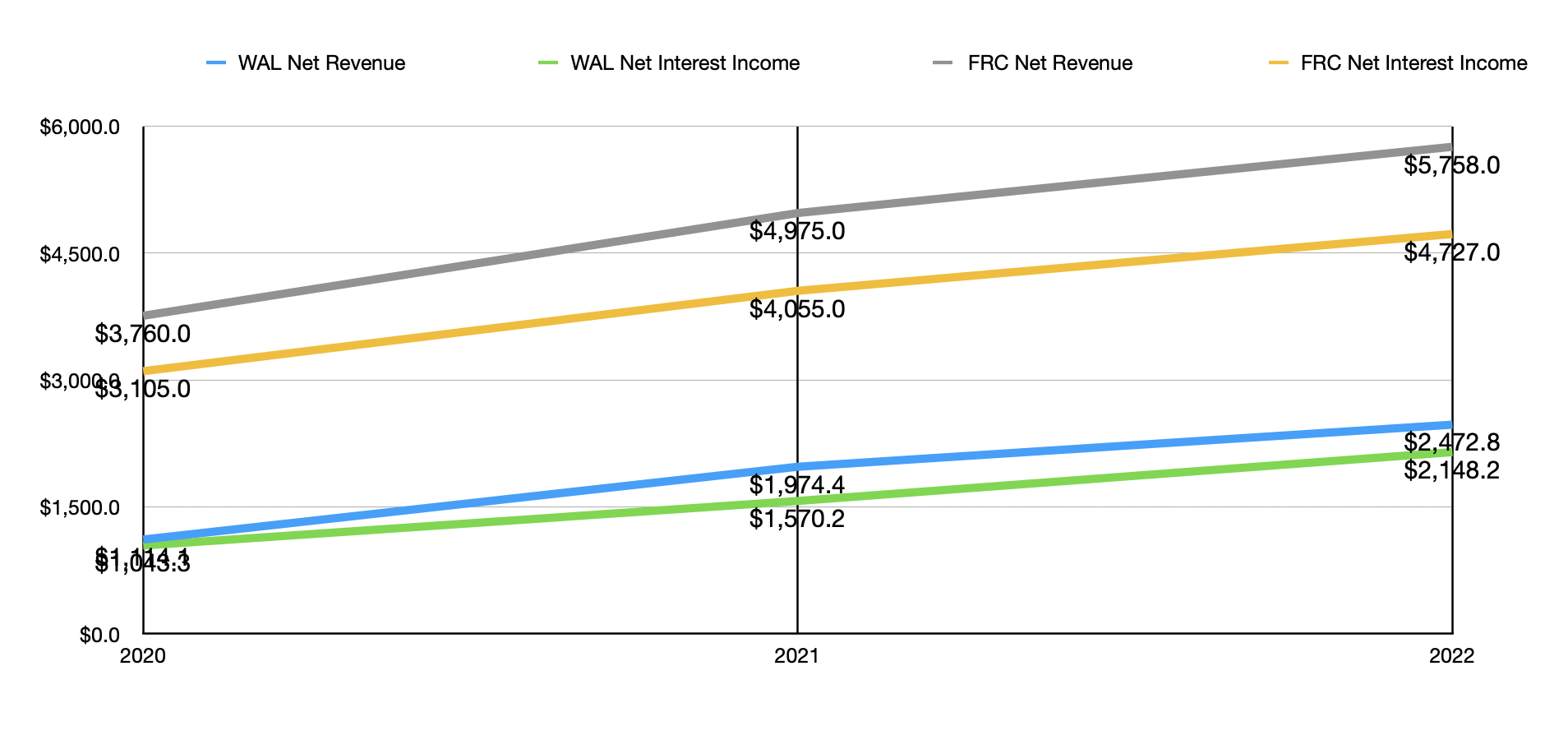

For full transparency, I am considering gambling a little bit of my money on long-term call options of First Republic Bank. Having said that, I do believe that if investors are focused on this for the long haul and they are using capital that they strongly prefer not to lose, the better opportunity is likely to be Western Alliance. I say this because of a number of reasons. First, let's look at how revenue for both of these companies has grown in recent years. From 2020 to 2022, net revenue from Western Alliance jumped 122%, climbing from $1.11 billion to $2.47 billion. Over the same window of time, First Republic Bank has seen an increase of only 53.1%.

{kind=link}

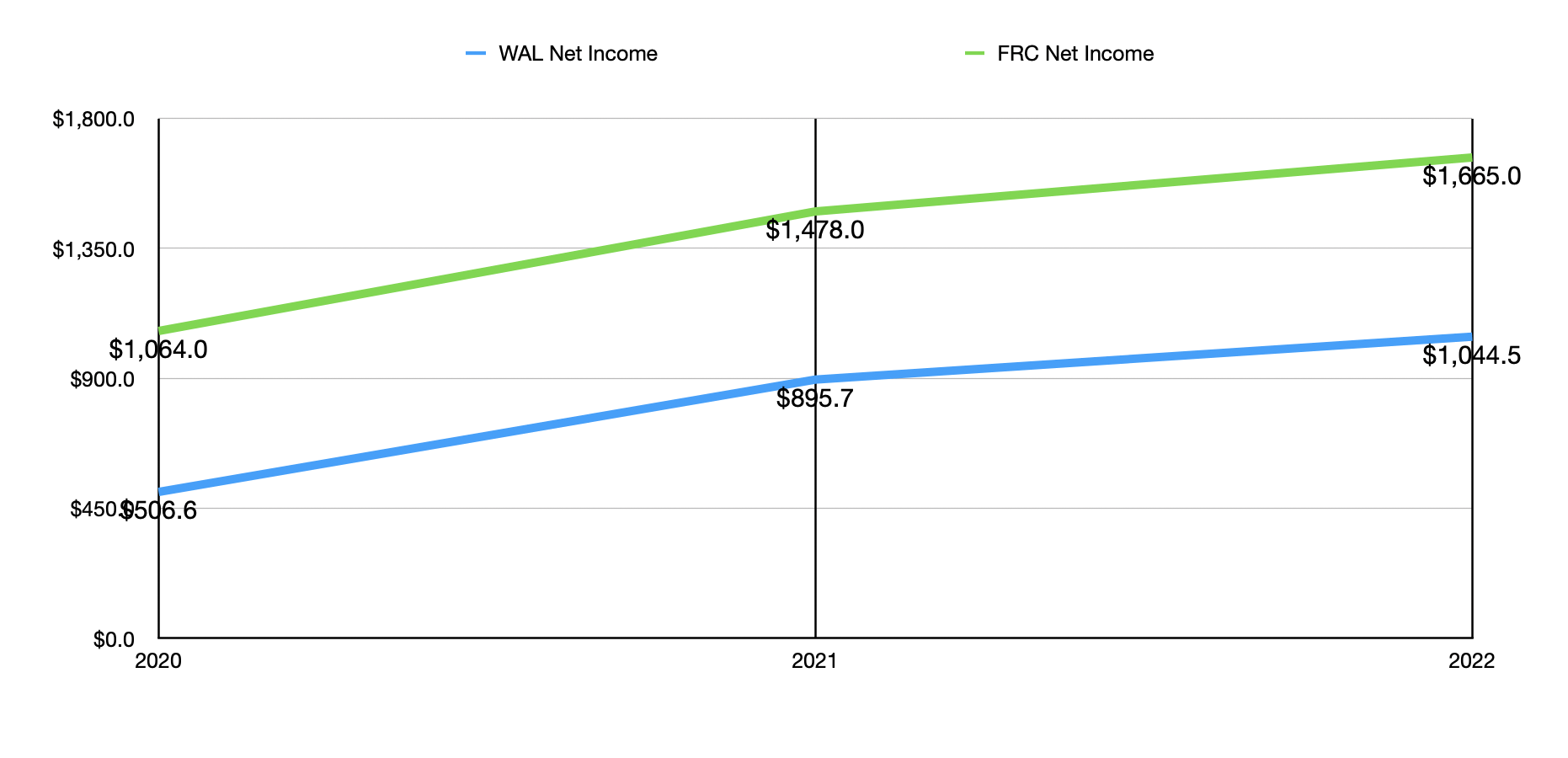

Profitability data looks remarkably similar. Net income generated by Western Alliance has grown 106.2% from $506.6 million to $1.04 billion over the same window of time. By comparison, the increase for First Republic Bank has been a more modest but still impressive 56.5%, with profits surging from $1.06 billion to $1.67 billion. A lot of the growth on both the top and bottom lines that these companies experienced is as a result of not only rising interest rates, but also growing deposits and loans.

{kind=link}

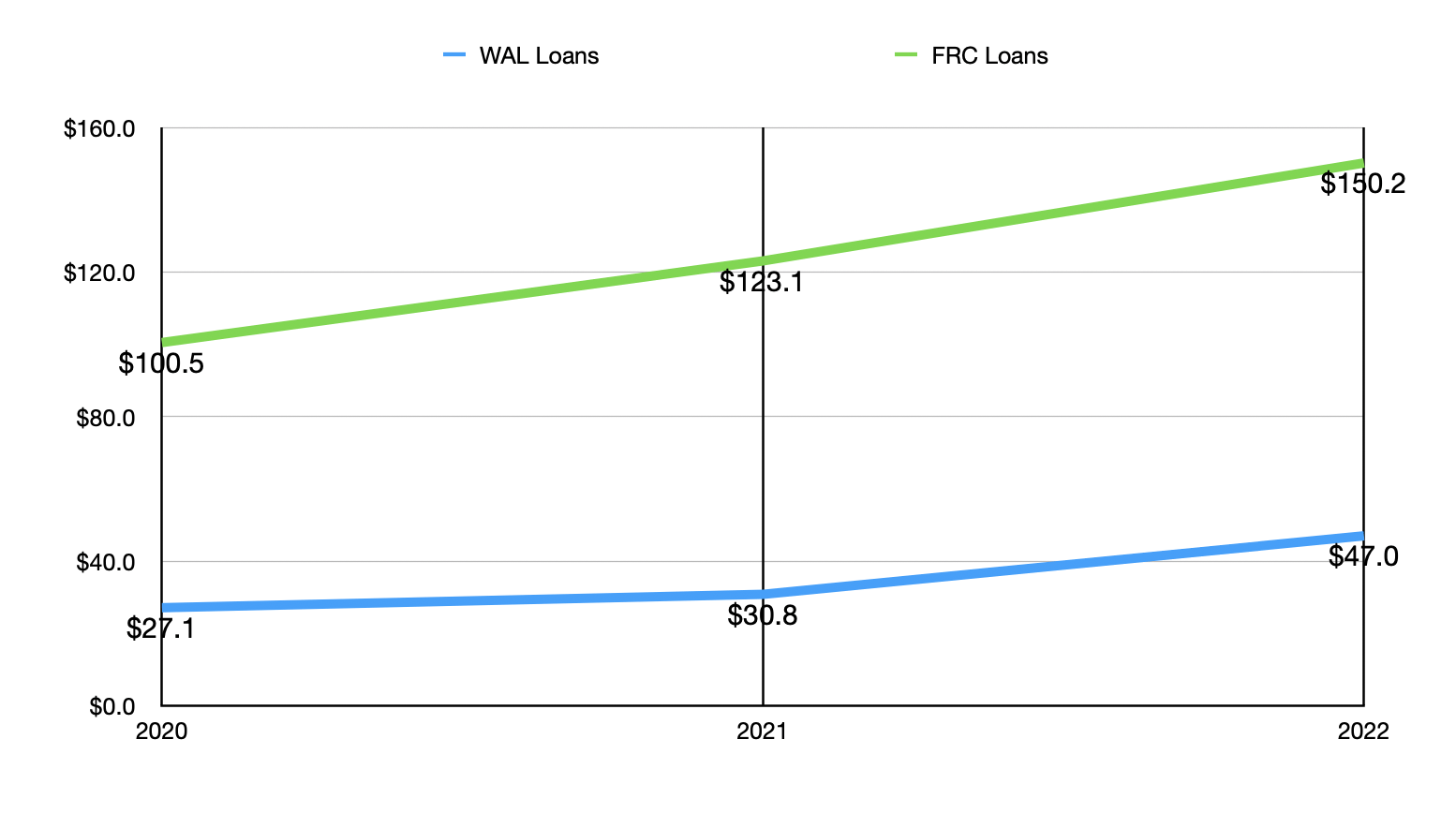

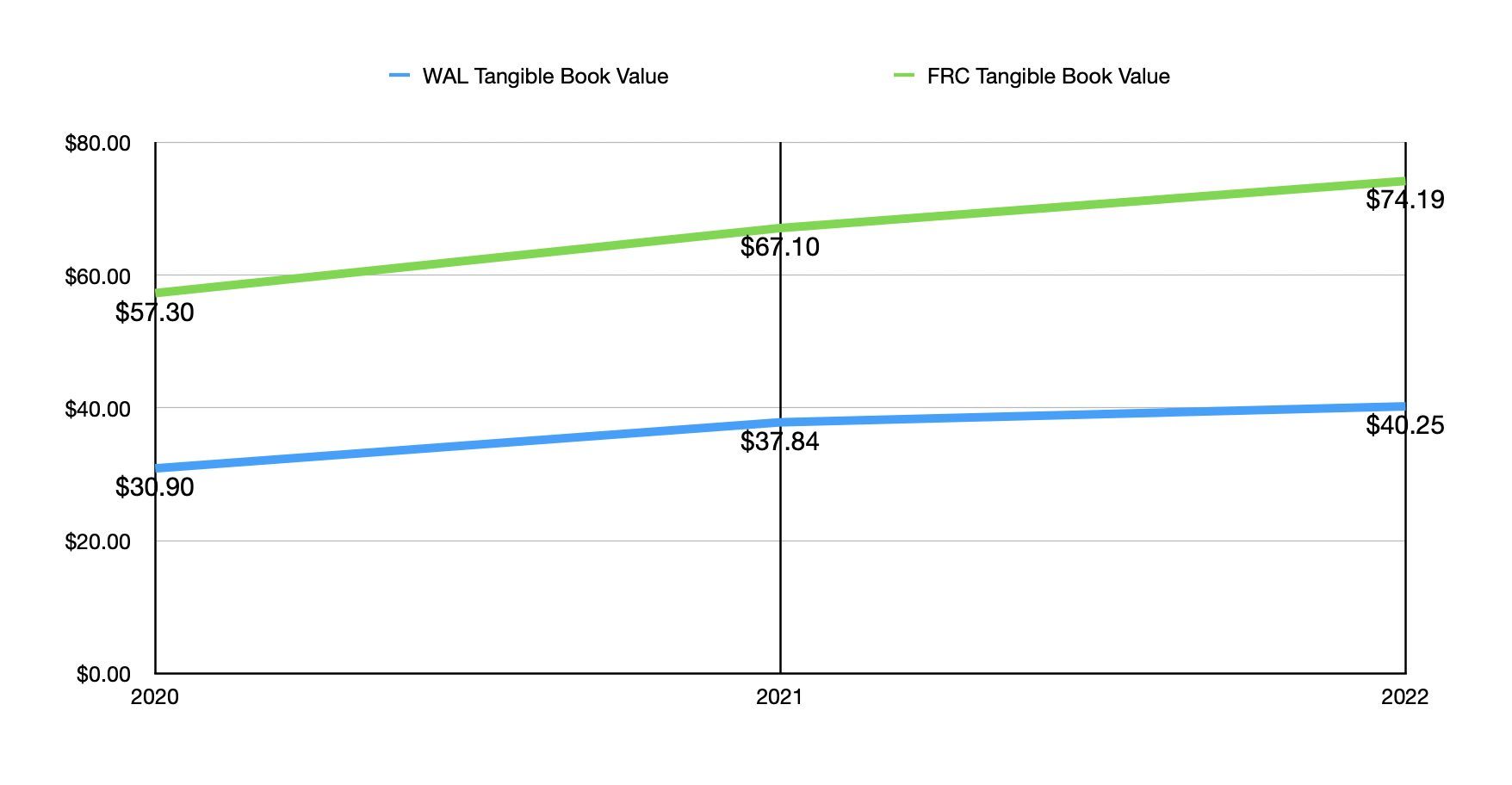

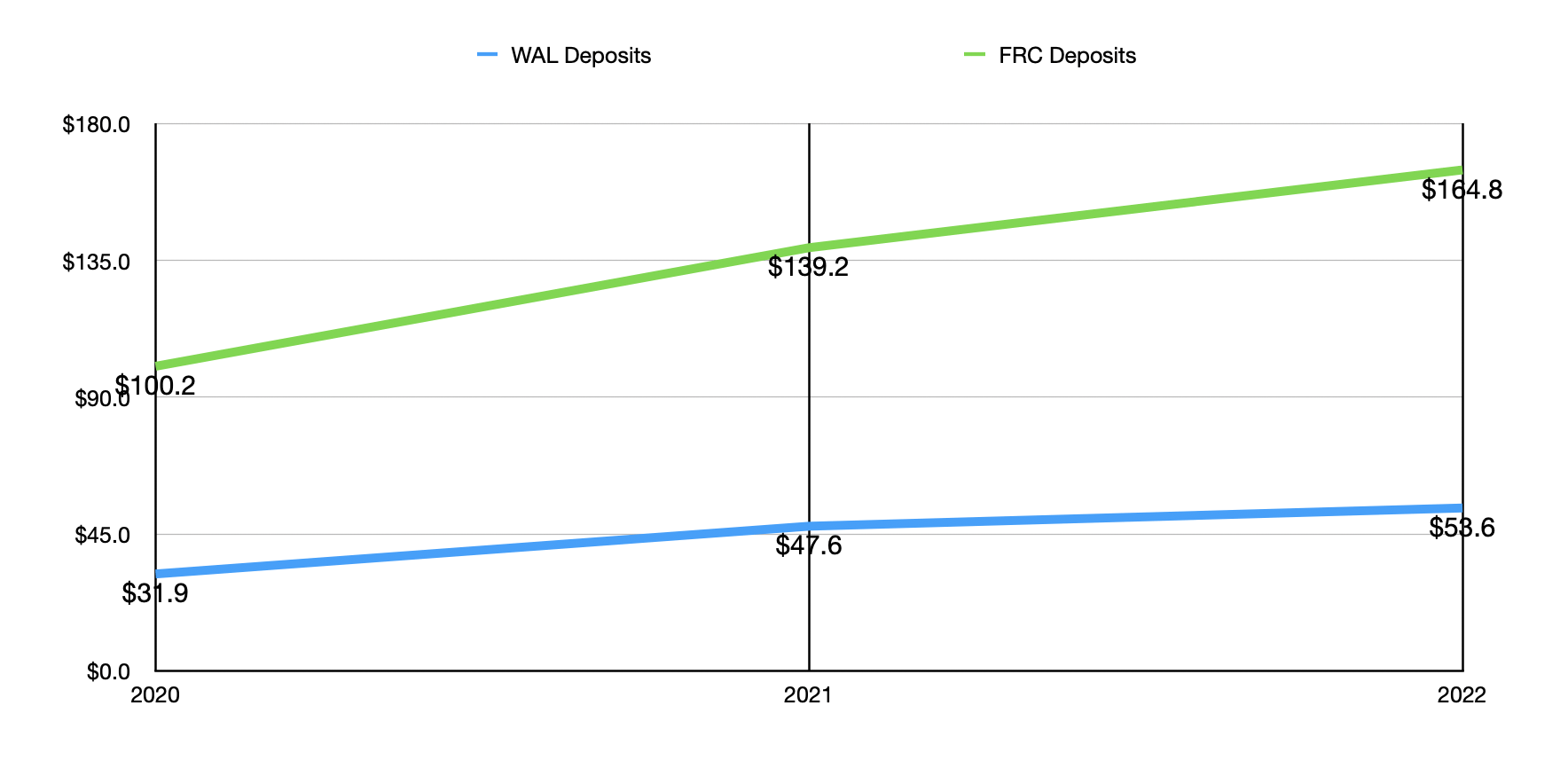

As an example, consider that the number of loans owned by Western Alliance shot up 73.4% from $27.1 billion to $47 billion over the three years ending in 2022. For First Republic Bank, the increase was 49.5% from $100.5 billion to $150.2 billion. A similar increase was seen when it came to deposits. Western Alliance reported a rise in its deposits from $31.9 billion to $53.6 billion, a total increase of 68%. First Republic Bank's deposit increase was only slightly lower than this at 64.5%. Its deposit base ultimately expanded from $100.2 billion to $164.8 billion. It is worth noting that, despite this difference in growth rate, the rise in tangible book value for both companies has been similar at around 30% over the past three years.

{kind=link}

Investors who are critical of my assertion that Western Alliance is the better play would make the case that since none of this data covers recent events, we can't know how the companies have fared during the recent turmoil. This is a fair point, but we do have a bit of information. As I mentioned in one of my prior articles on First Republic Bank, the company did receive uninsured deposits on March 16th of this year totaling $30 billion from a consortium of the largest banks in the country, bringing total cash balances as of that day to $34 billion compared to the $4.3 billion it was at the end of 2022. No such development occurred when it came to Western Alliance, but we also know that First Republic Bank also ended up increasing its borrowings from the Federal Home Loan Bank by $10 billion from March 9th of this year through March 16th. As of the end of March of this year, meanwhile, Western Alliance had no borrowings from the Federal Reserve's discount window, plus if posted access to liquidity exceeding $20 billion.

{kind=link}

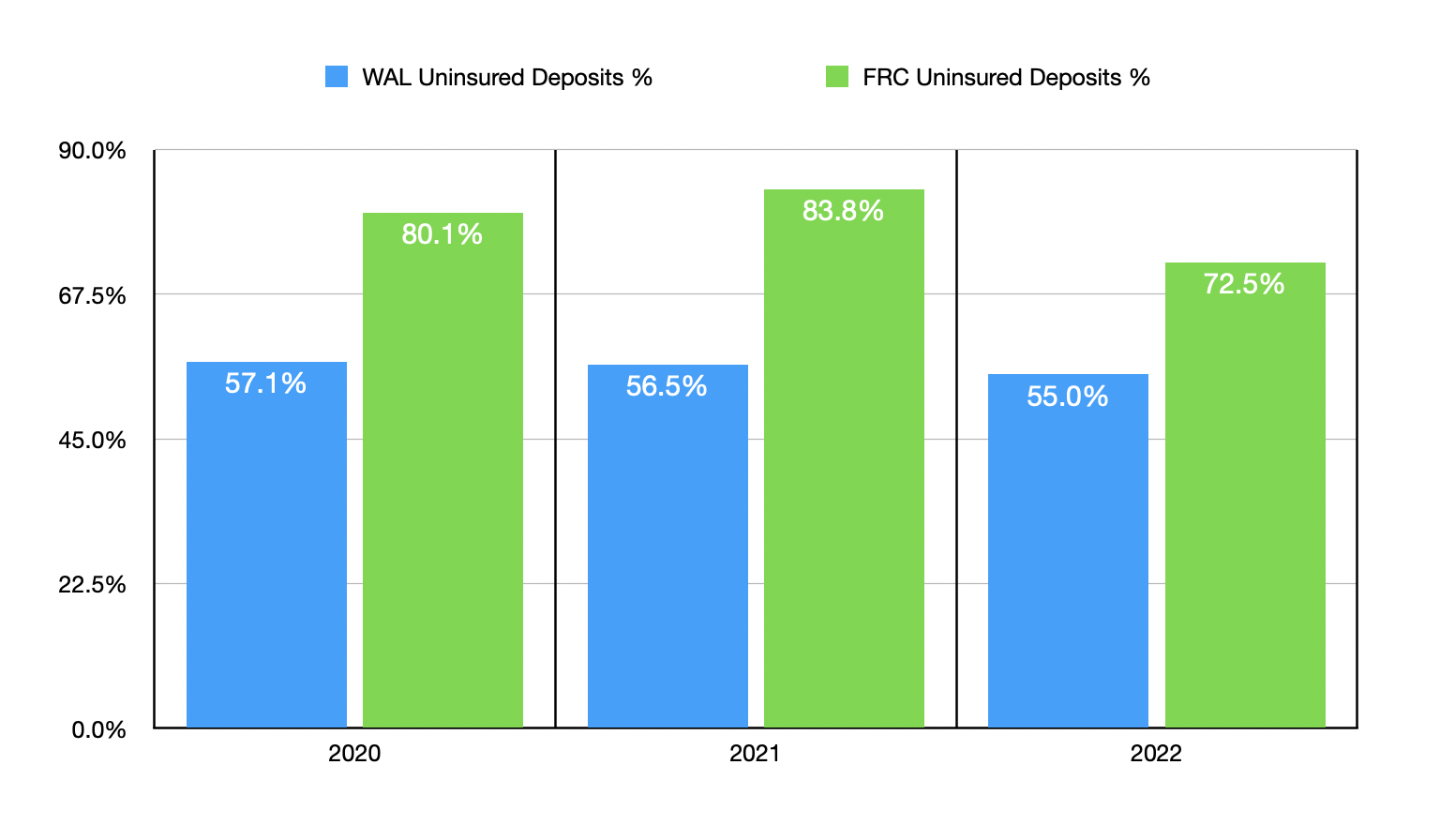

While this only gives us a slight glimpse into the picture of the business, we know that, as of the end of 2022, Western Alliance was far less exposed to uninsured deposits than First Republic Bank was. $119.5 billion, or 72.5%, of the deposits that First Republic Bank had on its books at the end of last year were uninsured. That number was a more modest 55% for Western Alliance. And although it's probable that the company did see an outflow of assets in recent weeks, it is at least a relief to know that this number has dropped further to about 32% as of the most recent update provided by management.

{kind=link}

Takeaway

Based on the data provided, I do believe that both Western Alliance and First Republic Bank are quite risky leading into earnings. We don't know what to expect, and neither firm has provided as much transparency as they should have. First Republic Bank has offered more insight, but it's not as high-quality an operation as Western Alliance was as of the end of last year. Because of this lack of clarity, I am personally rating both companies a 'hold' for now, only because they do seem to offer tremendous upside should things turn out well. But investors who aren't comfortable with the significant lack of information we have, may be better off waiting to buy in after the companies report in the coming days.

For further details see:

First Republic Vs. Western Alliance Stock: Which Is The Better Value Buy?