FSLR - First Solar: A Little Pricy For Me

2023-09-01 00:44:53 ET

Summary

- First Solar has improved its financials and is projected to have decent margins and revenue growth.

- Solar power is gaining popularity as countries become more environmentally conscious.

- Government subsidies and the demand for renewable energy are expected to continue, providing opportunities for FSLR.

Investment Thesis

I wanted to take a look at First Solar ( FSLR ) and how it has improved its financials since FY22. It seems like the company has improved a lot and is projected to make decent margins and revenue growth going forward, however, even with such an improvement, I believe the company is slightly overvalued and assign a hold rating until we see some more numbers in the future to confirm the positive trajectory.

Outlook

Solar power has been experiencing a boom in the last decade, going from total energy generation of around 95TWh in 2012, to over 1,200TWh by 2022. We can see that it is gaining in popularity as more and more countries become more environmentally conscious. Renewable energy has become a big topic these days with ESG factors playing a much bigger role. Millennials and Gen Z are going to be the main generations that will be investing their savings for retirement in the next decade or so, and these generations are more environmentally conscious than any previous generation. So, this naturally is a positive for First Solar. There will always be people who will want to invest in the betterment of the earth through renewable energy like solar.

Many countries are also providing government subsidies in the form of tax breaks/credits for companies like First Solar, and it depends a lot on these subsidies to generate revenues. In my opinion, these subsidies all around the world will not go away anytime soon and will most likely accelerate because of the current generations that are more environmentally conscious. The demand for renewable energy is there and governments are not going to squander that. Just recently, the Biden-Harris administration announced a $7B "Solar for All Grant competition" that aims to fund costs for families and "advance environmental justice through investing in America".

India, which still gets most of its energy, around 80%, from coal, oil, and other non-renewable energy will be a great future opportunity for First Solar, as the Indian government is starting to warm to the idea of renewable energy and it wants to have solar energy to be the leader in the country with around 60% of energy to come from solar, which will be around 280GWh by 2030. India does not represent a very big market for FSLR yet, however, with most of the country getting around 300 days of clear and sunny days, coupled with government incentives , I could see this becoming a much bigger revenue generator in the future, especially now that the construction of the factory is completed there and will begin production shortly.

It also seems like the growth of solar energy is going to continue on a strong positive trajectory, as it is predicted to grow at a very respectable 25.9% CAGR until '28. This already coincides with what FSLR can attain in terms of revenue generation, with the latest 10-Q report showing revenues increased by around 30% from the same quarter last year.

Financials

All the graphs below will be as of FY22; however, I will include some of the latest figures for extra color if it is necessary.

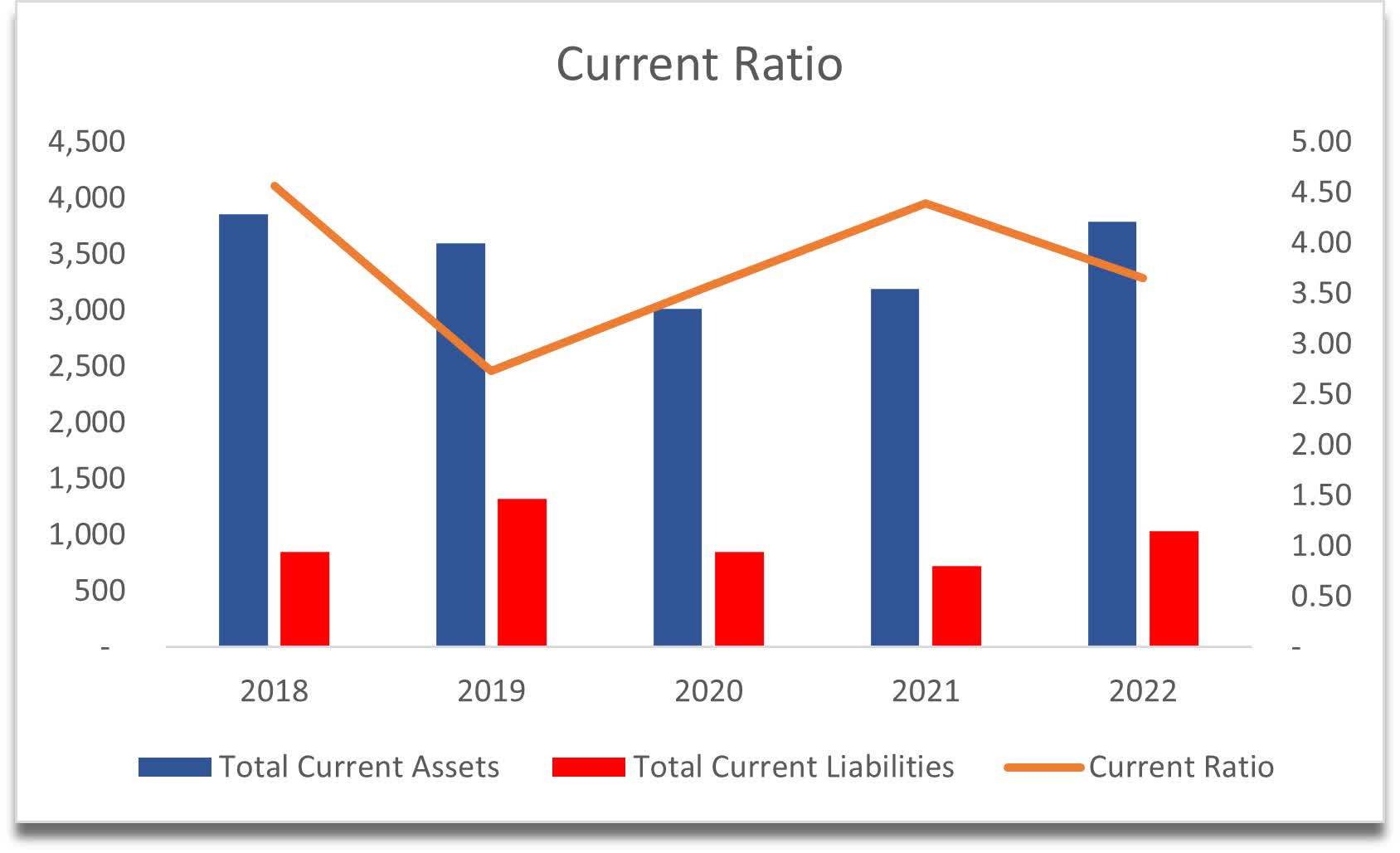

As of Q2 '23, the company had around $1.9B in cash and marketable securities, against $437m in long-term debt. This is a very strong position to be in, which provides flexibility in how the company is going to expand its global footprint and other initiatives. The company's current ratio has been a little too high in my opinion, which is a good and a bad thing. A good thing because it has no problems paying off its short-term obligations and a bad thing because this tells me that the company isn't being very efficient in using its assets for further expansion. I would like to see the company being more aggressive in future expansion. As of Q2 '23, the ratio stood at over 3.3. My ideal range is anywhere between 1.5-2.0. This is the range I believe tells us that the company is being efficient with its available liquidity and still able to pay off its short-term obligation with ease.

{kind=link}

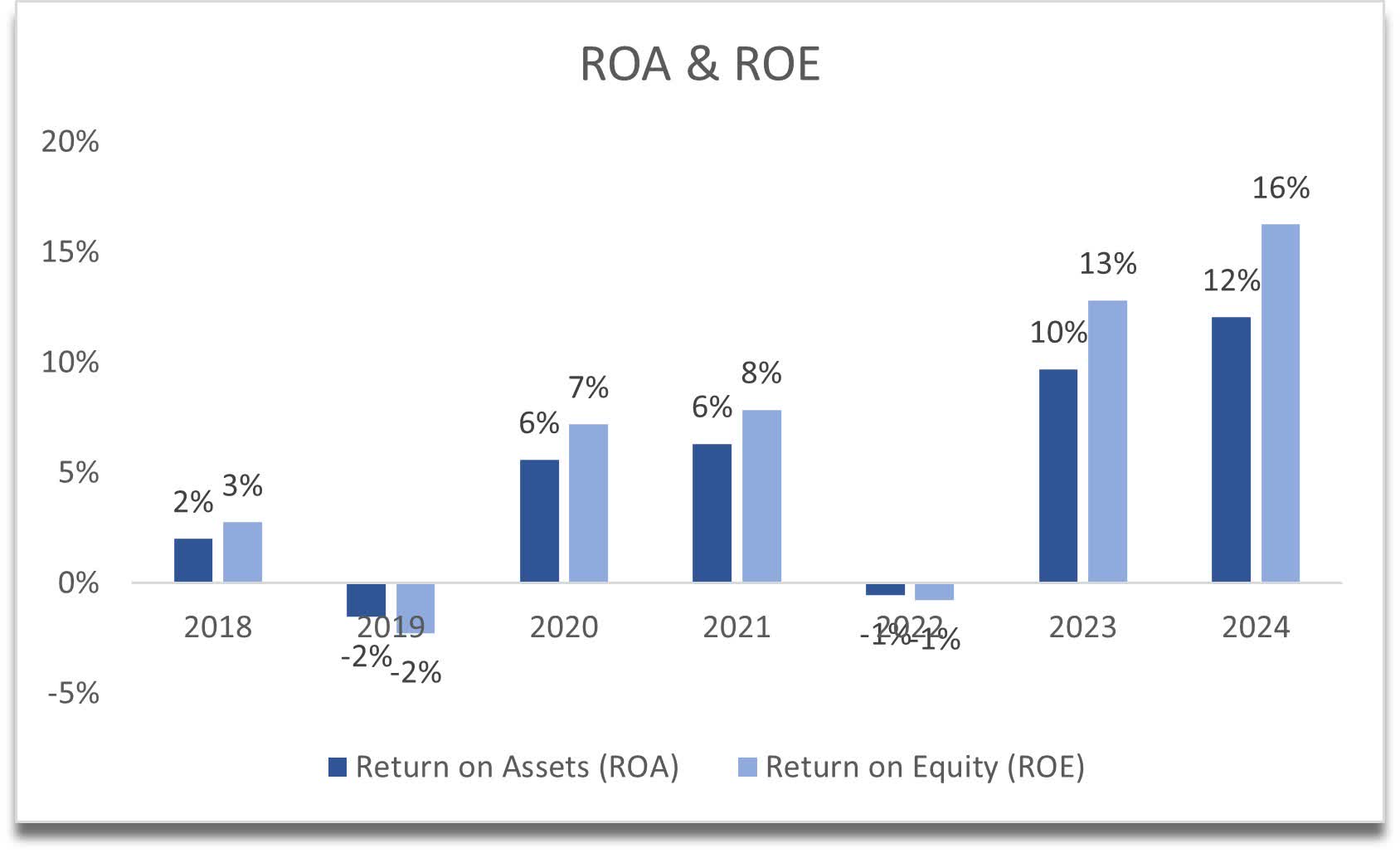

The company's historic ROA and ROE have not been very impressive to say the least, however, since the company has become quite a bit more profitable if we look at the analyst's estimates, the graphs below will include years '23 and '24 which show how these metrics might evolve and they look much healthier than before.

{kind=link}

If the numbers in '23 and '24 are close to where the company might end up, then it is a very good return on both metrics.

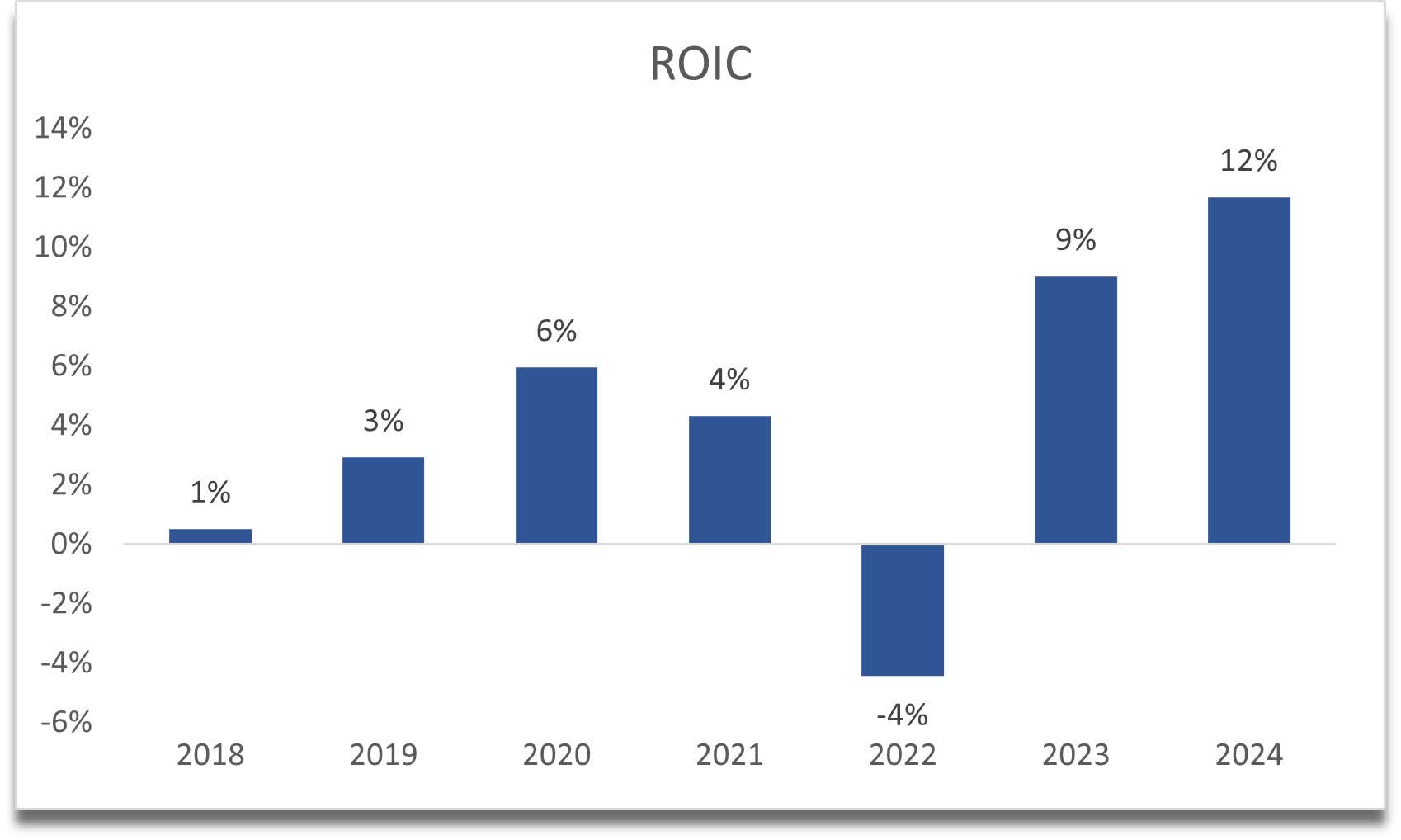

The same can be said about the company's return on invested capital. The historic numbers were quite disappointing, however, since the company seems to be having a turnaround, ROIC might develop like this in the future:

{kind=link}

This would tell me that the company has a decent moat and a competitive advantage.

Overall, if we just look at the historical figures, it will show quite a mixed bag of results, and certainly not the best, but if we make some assumptions, the profitability and efficiency will improve quite considerably in the upcoming years. Take the estimates with a grain of salt because these are just my estimates, and a lot can happen over the next couple of years. Prices may fluctuate, and production costs increase once again, which will bring down these metrics as they did in the past.

Valuation

It seems like the past revenue growth doesn't apply to FSRL because, in the past decade, the company managed to lose 21% of revenues. FY15 to FY16 and FY17 to FY18 drops can be explained by divestitures. Now, with the recent performance in the latest quarter, analysts are estimating around 33% growth in FY23 and around 30% in FY24. Let's say the time has come for FSLR to shine, so for my base case, I went with an 18.8% CAGR over the next decade, 22.5% for my optimistic case, and 16.8% CAGR for an optimistic case.

I admit these figures are more than just optimistic, but analysts see a lot of improvement over the next decade in terms of revenues and margins, so I will stick with these estimates.

Speaking of margins, FY22 was a very bad year for FSLR. Cost of sales accounted for 97.3% of net sales. The biggest cost came in from freight, demurrage, and detention charges, which accounted for $167m. In the latest quarter, gross margins came in at around 38%, which tells us that the costs have stabilized, and the company is going to perform much better in the future.

I decided to improve gross margins from around 35% in FY23 to around 45% by FY32, which I believe is slightly optimistic also.

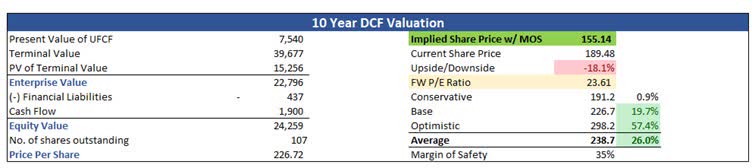

Because I decided to go with such optimistic assumptions and because the financial estimates also look great on assumptions, I will add a 35% margin of safety to the intrinsic value calculation. With that said, First Solar's intrinsic value is $155.14 a share, implying that currently the company is slightly overvalued.

{kind=link}

Closing Comments

The company has a lot of potential to perform very well, with many countries subsidizing the future of energy consumption, FSLR is going to be one of the leaders to capture a lot of growth in this segment, however, does this mean that the company is going to be so much more profitable going forward than it was in the past? Is the revenue growth that I assumed for the model attainable? It is hard to tell given the past revenue growth, or lack thereof.

Nevertheless, if the share price retreats slightly to my implied share price, the risk/reward would be much more enticing than now, and I would seriously look into opening a position and see how it goes in the next couple of years.

Currently, the company is trading at 15.6x '24 earnings according to my model, and at my PT it would be trading at around 12x, which I would prefer to be honest, so I will be waiting patiently for a pullback if one happens. If not, then I'll keep looking for a company that is closer to my risk/reward profile.

For further details see:

First Solar: A Little Pricy For Me