FSLR - First Solar: Growing Capacity And A Growing Backlog Equals Growth

2023-09-01 10:14:30 ET

Summary

- First Solar, founded in 1990, is the largest producer of solar panels in the US and is currently funding large capital projects to expand capacity.

- The company has a deep backlog and opportunities to continue expanding the backlog that should produce growth opportunities for many years.

- First Solar is either fairly valued to overvalued at their current valuation. However, with the expanded capacity and deep backlog, the company is positioned to grow.

- By continuing to be funded by subsidies, the question continues of whether the solar industry could be able to stand without help from said subsidies.

First solar ( FSLR ) was founded in 1990 and was incorporated in 1999. In 2002, they finished their first commercial production facility in Perrysburg, Ohio with the capacity to create 1.5 megawatts per year. Today, First Solar is the largest producer of solar panels in the United States.

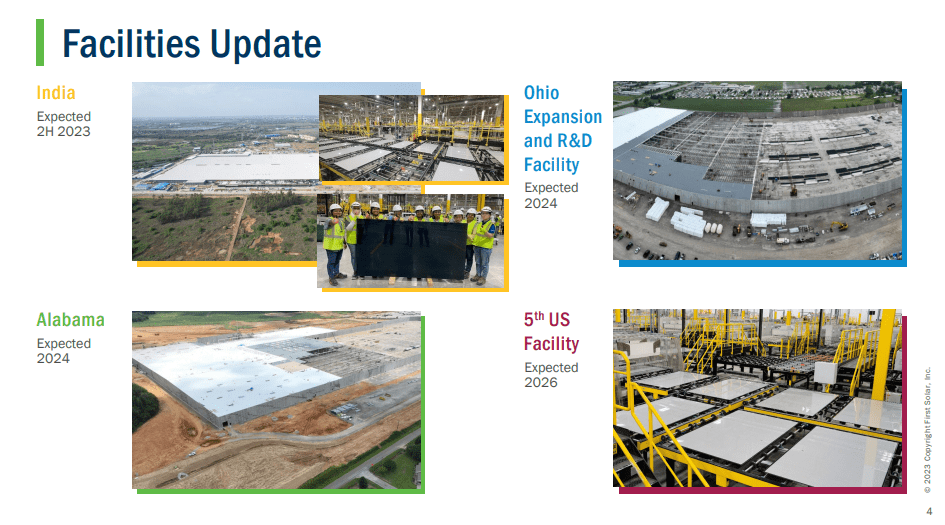

First Solar will be building their fifth manufacturing facility for a cost of $1.1 billion located in Louisiana. Funding for this new facility is partly due to the Inflation Reduction Act that was passed in August 2022. It is expected to come online in 2026 bringing 3.5 more gigawatts of manufacturing capacity per year adding to its existing 11.5 GW. Just this year alone, the company has made plans to spend an additional $1.7 billion at a new site in Alabama and by expanding a facility in Ohio.

First Solar Facility Expansion (First Solar Q2 Presentation)

{kind=link}

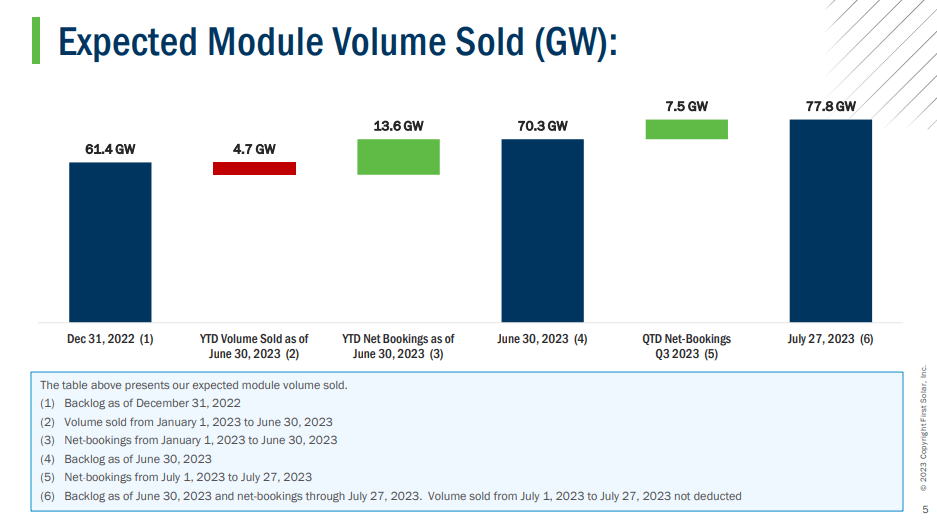

At current production levels, and with no new orders, the company has a backlog that will last until at least 2030. The slide below shows their backlog at different dates in the blue bars. And the green demonstrates how their backlog is growing throughout 2023. In other words, their order backlog is outpacing their ability to produce solar panels. This is an encouraging sign for investors.

{kind=link}

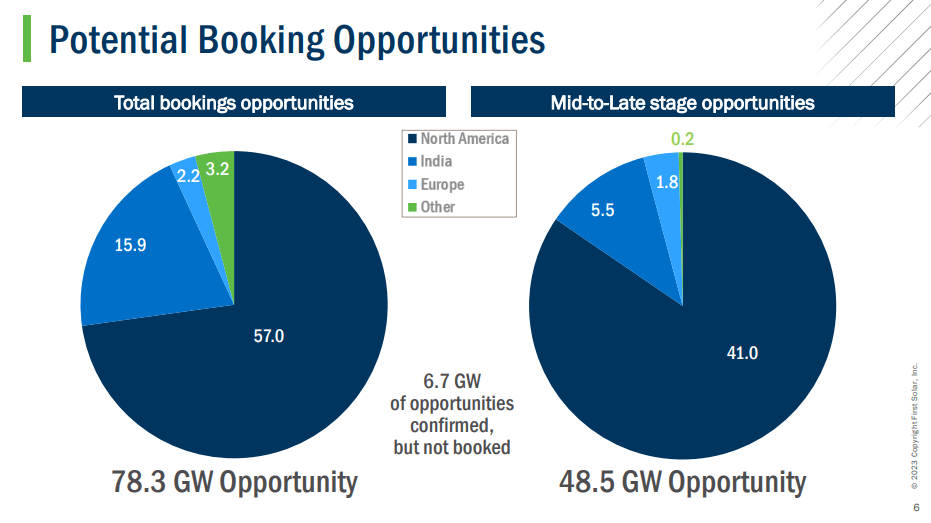

The following slide demonstrates the total opportunities that are available in the solar industry for First Solar to go out and get. This demonstrates that even though they have a backlog that will last until 2030, the potential to extend that backlog is also there.

First Solar Booking Opportunities (First Solar Q2 Presentation)

{kind=link}

Subsidies

Currently, the subsidies that individuals can receive for installing solar panels are up to 30% of the cost of the panels according to some sources. This is set to continue from 2023 all the way until 2032. This provides some strong visibility into the future demand for solar panels.

In addition, First Solar was able to begin building a fifth plant using funds from the Inflation Reduction Act. And so we can see that the solar industry is subsidized on the capital funding side as well as on the demand side.

I am not going to evaluate what percentage of First Solar's profit is dependent on subsidies in this article, but it is important to know that a certain percentage of both First Solar's demand and their capital investments are subsidized.

I rarely like to invest in a business that requires subsidies from the US government or any government, however, many people have become fabulously wealthy by investing into government tax breaks, whether that be local or federal tax breaks. And so while I might shy away from companies like this, others might see this as an opportunity.

Going forward, the question I will be interested in, is what will the economics of solar panels be when the subsidies run out in 2032? Will they be able to produce panels economically enough for subsidies to not be necessary? I don't know the answer, but I think that based on First Solar's backlog, they will have plenty of opportunities to find ways to make the panels more economical and with the full force of the climate-change narrative and the government funding backing the industry, I wouldn't expect First Solar's backlog to experience any kind of decline. So I would love nothing more than for the solar industry to be able to create energy that no longer requires subsidies. Time will tell.

Valuation

As of this writing, First Solar has a $20 billion market capitalization. So is this cheap or is this expensive relative to the performance of their current business? Let's measure this relative to operating cash flow.

Operating Cash Flows

Here are the cash flows from operations for the past four years. With a $20 billion market cap, I believe First Solar is a little over-valued relative to these cash flows. I won't discuss their balance sheet in this article, but First Solar also has a strong balance sheet. The question is, will First Solar's cash flows grow dramatically over the coming years? They certainly have potential growth catalysts in that they are expanding their manufacturing facilities. For argument’s sake, let's extrapolate that in 2024, First Solar will have Cash Flows From Operations of $1 Billion. Even then, at today's prices, you will be paying 20x for operating cash flows.

| $(thousands) |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 1H 2023 |

| Cash Flow From Operations |

| 174,201 |

| 37,120 |

| 237,559 |

| 873,369 |

| -124,276 |

Another question one might ask is, why is cash flow from operations so "lumpy?" For example, through the first half of 2023, cash flows from operations were negative. Why? One of the reasons cash flows are so lumpy is because any time an industry is subsidized, cash flows will continue to be sporadic because receivables will tend to stack up and then get paid all at once.

For example, through the first half of 2023, First Solar's net income was $213 million. However, on their cash flow statement, they have the following deductions which caused cash flow from operations to be negative. Most of these are receivables and although I didn't do a deep dive into the footnotes to understand what these receivables precisely are, we can clearly see that some of it is related to subsidies in the form of "grants." This is one of the caveats to investing in this industry. First, cash flow as well as capital costs are, to a certain extent, subsidized and therefore, cash flows might behave in a staggered fashion.

| Accounts receivable, trade and unbilled |

| (177,591) |

| Inventories |

| (131,625) |

| Government grants receivable |

| (225,121) |

| Other assets |

| (105,243) |

| Income tax receivable and payable |

| (20,090) |

| Accounts payable and accrued expenses |

| (42,994) |

| Deferred revenue |

| 211,721 |

| Other liabilities |

| 40,898 |

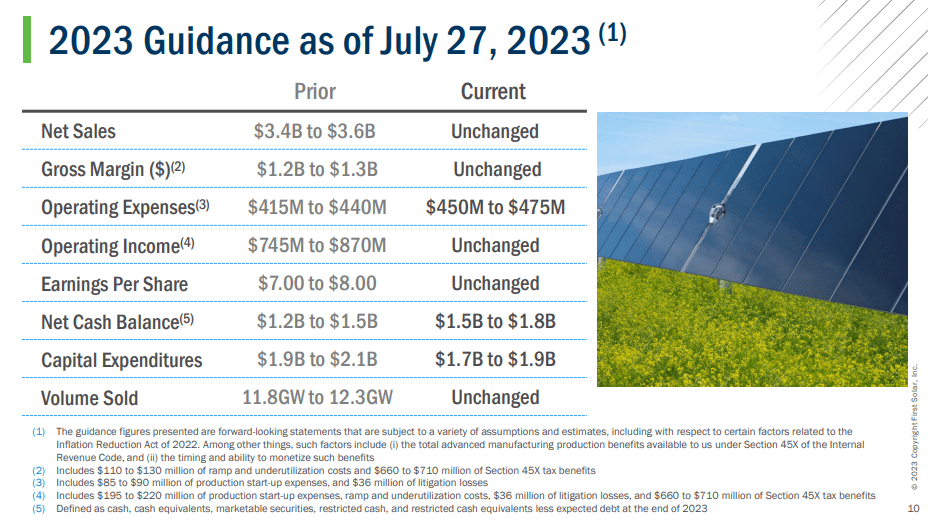

For further guidance, here is the company's guidance through the end of 2023.

{kind=link}

Conclusion

Simply put, First Solar is going to grow larger than they are right now. I know that is a profound statement but the point I want to make is that I wouldn't invest in something just because it's going to grow. Yes, the business is on solid footing thanks to a really strong backlog of work that at its current production capacity will last to 2030 and likely beyond. There are a lot of new projects that they have the potential to win by 2030 as well. And with $3 billion in capital projects in process in order to expand their manufacturing capacity, this creates opportunities for growing income. And last but not least, the United States government has chosen to heavily subsidize their industry.

However, the subsidization that this industry receives is also one of the drawbacks. I expect their cash flows to continue to be lumpy, until their industry is self-sustaining without so many subsidies. Do I think it will eventually get there? Yes, I do, but it isn't there right now. And perhaps one can make the argument that for that reason, this presents a good time to buy.

Lastly, when deciding what to invest in, it must be a relative comparison. In other words, to invest in one thing is to say NO to investing in another. And so although I think your capital can grow by investing in First Solar today, there are other investments that I believe present a better opportunity. And therefore, I can only rate First Solar a HOLD.

In case you haven't read my other articles, I am bullish on oil and gas . My bullish timeline is for at least the next 6-7 years, as I believe the industry is positioned much better than the solar industry. The oil industry is much more established and the net gains from the energy provided by hydrocarbons is greater than that provided by solar. Because of this, many of the oil and gas companies pay attractive dividends with strong balance sheets and predictable cash flows. Not to mention, companies like EOG Resources ( EOG ) are valued more fairly relative to operating cash flows.

And when comparing one form of energy (solar) to another form of energy (oil & gas), I want to position myself with the one that performs the best without government subsidies. In an inflationary or stagflationary environment, I do not believe solar will perform as well as hydrocarbons.

For further details see:

First Solar: Growing Capacity And A Growing Backlog Equals Growth