FSLR - First Solar Has Flown Too Close To The Sun And Should Be Avoided

2023-04-24 11:24:39 ET

Summary

- The solar sector has been touted as a growth market yet, if this is so, asset growth trends will push returns down, not up.

- However, the sector is characterized by energy inertia, not rapid transition, and First Solar’s growth has been abysmal.

- In order to sustain sales, the company has to spend 97% of revenue.

- Profits are razor thin and declining, and returns are collapsing.

- With enormous cash burn, and poor profitability and returns, investors should expect a fall.

First Solar Inc. ( FSLR ) has been a stock market sensation over the last five years. Yet, an analysis of the alternative energy sector reveals that it is characterized by energy inertia rather than rapid transition. First Solar’s results show a firm that is not seeing any meaningful growth, and which is eating up most of its revenues, burning cash, and seeing falling returns. I believe this stock market sensation is due for a decline.

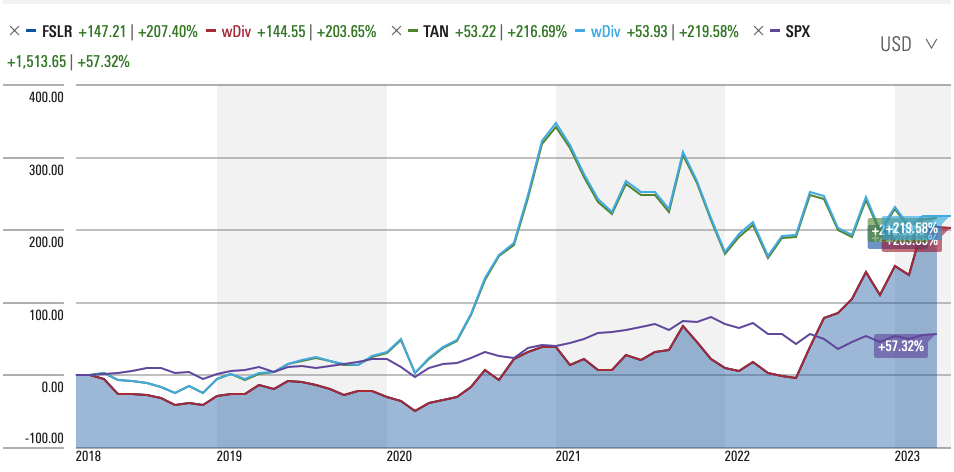

A Stock Market Superstar

In the last five years, First Solar’s share price has grown by over 207%, compared to more than 57% for the S&P 500 ( SPX ) and nearly 217% for the Invesco Solar ETF (TAN), which represents its peer group. However, taking dividends into account, the Invesco Solar ETF, earned a total shareholder return (TSR) of nearly 220%.

{kind=link}

Methodology

There is a wealth of evidence that managers (and investors) overestimate future free cash flows ((FCF)) and that managerial overconfidence leads to corporate investment distortions. This overconfidence is traditionally ascribed to a misalignment of interests between shareholders and investors; asymmetric information between the capital market and insiders. Investors are also likely to overreact to corporate earnings information . First Solar, which, despite being founded in 1999, is still in the role of a new entrant in the energy sector, trying to wrestle a meaningful chunk of the market for itself, faces an added problem, which is that entrants typically are overconfident and neglect competition threats .

The reason why we have this overconfidence and overshooting, not simply of future FCF, but of future demand, is because both managers and investors are susceptible to ignoring the outward shift of the supply curve. In terms of behavioral economics, this can be explained as being due to “base-rate neglect”. In other words, decisions are based on projections of the future without taking into account an industry's asset base, from which returns emerge. More importantly, future demand is almost impossible to predict in the long run. This leads to waves in investment and pricing , thanks to excess investment. Managers overestimate the persistence of exogenous demand shocks, or daily to truly understand the long-run endogenous supply reaction to those shocks.

How should investors react to this? The more sustainable reaction to the uncertainty of projections, is to simply not try to predict future demand, which is so fluid as to not be predictable over the long-term, but to focus on supply. This avoids the emergence of forecasting errors. My approach will be to focus on the supply-side, instead of demand. Supply is far less fluid than demand and therefore, more predictable. Supply changes are easier to predict because the supply chains are visible and changes are better known. Because most investors focus on trying to predict future demand, they are liable to be shocked by a failure to predict negative supply shocks.

The thesis driving this article is that management’ investments in the business are based on an overreaction to the growth opportunity in alternative energy. There is little evidence to believe that the energy supply chain is on the verge of any meaningful changes, and so, First Solar does not have any real avenue for rapid growth. To show this, we will perform a backward-looking analysis to establish the base rate, or aggregate situation. When the base rate has been established, we are left with the realization that there is no reason to believe that First Solar should beat the market. In 2018, CEO, Mark Widmar talked about “strong industry growth”, in his 2018 letter , and, results will show that Mr. Widmar was extremely overconfident in his projections. Indeed, we will be forced to wonder how the company will achieve its financial goals, which Mr. Widmar described as balancing “the priorities of growth, profitability, and liquidity”.

The Growth Opportunity is Overstated

There has been a conflation of the importance and virtue of investing in alternative energies, with the investability of the sector and ease of transition. However, the reality of alternative energies shows that the growth opportunity has been vastly overstated. Rather than the rapid transition that is tacitly assumed by alternative energy investors, energy has been characterized by inertia.

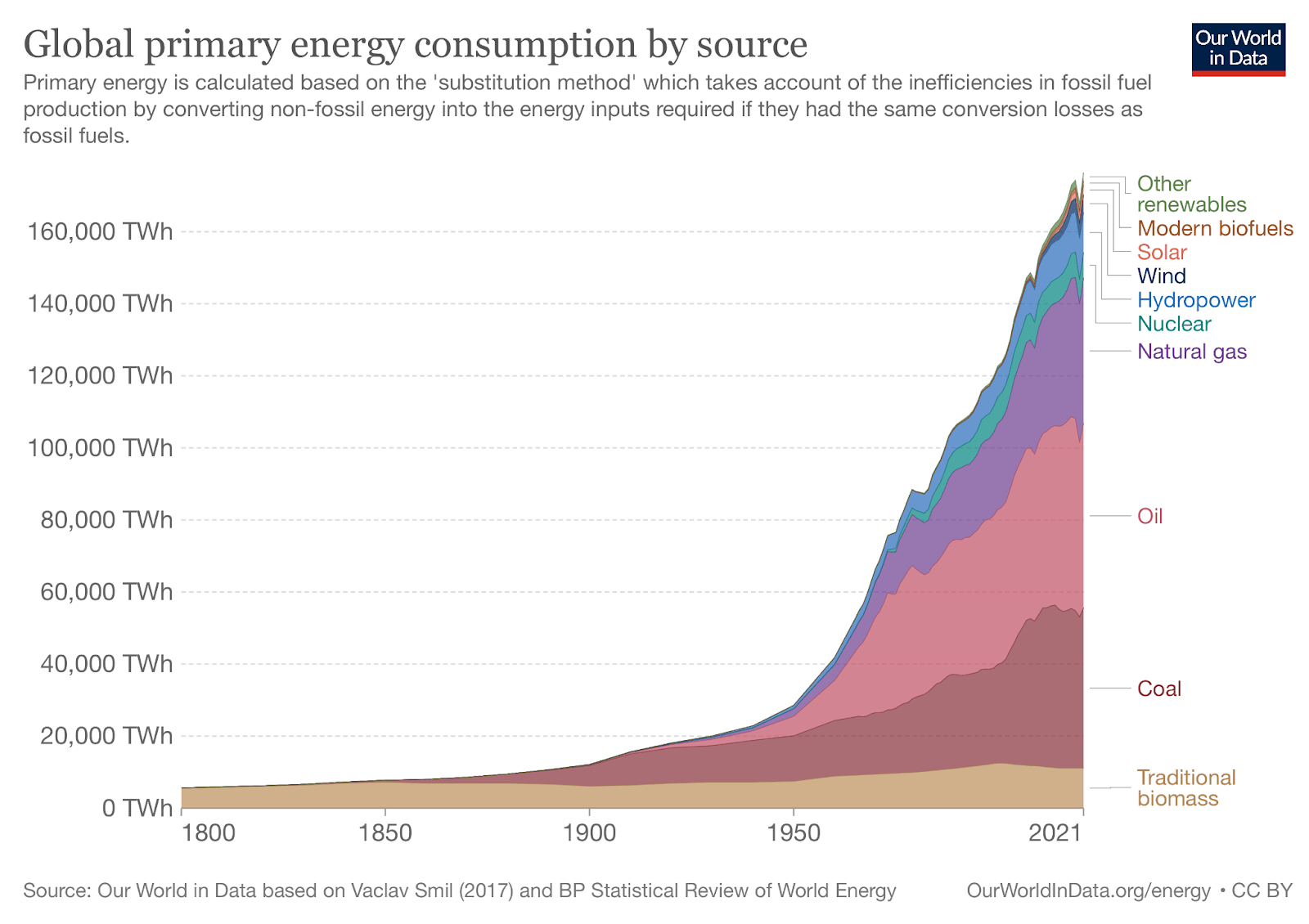

In 1970, fossil fuels were responsible for 80% of the world’s primary energy . In 2021, that number had dropped to 77.1%, a decline of 0.057% a year! Investors have, for many years, ignored the real fact of the world's dependence on fossil fuels. Indeed, energy and technology transitions are always slower than investors imagine, and, crucially, a transition still offers new growth opportunities for traditional energy sources. Transitions are seldom rapid. Since Russia’s invasion of Ukraine, it is arguable that, at least in the near-term, dependence on fossil fuels has risen. I believe it is a mistake to imagine that fossil fuels are on the verge of an Armageddon.

{kind=link}

Alternative energies face numerous challenges. Noted scientist, Vaclav Smil, has calculated that, in order to sustain alternative energy production, countries would have to dedicate 100 or more times the land area currently used for traditional energy uses. This leads us to a paradox for the industry: the more it grows, the greater the demand for land, which will increase land values and make it harder for solar firms to be profitable. The solar sector’s appetite for land means that a crucial resource is not just limited, but is likely to be driven up in price as the transition progresses, which will have the impact of increasing future prices. This is especially true when you factor in competition for that land from farmers. The negative impact of solar on biodiversity, as well as environmental quality, may also put brakes on growth.

Smil notes that, from 2000, when fossil fuels supplied 84% of Germany’s energy, despite building 90 gigawatts of renewable energy capacity matching its existing electricity generation, in 2017, fossil fuels still supplied 80% of its energy. The reason is simple: Germany has roughly the same solar potential as Alaska, with an average 3.08 sun hours/day. Since 2011, there has been a steady decline in investment in solar, with the costs of a transition to solar unsustainably high. Those lessons will apply in the United States, where states like Alaska have limited solar potential.

Looking at First Solar financials proves this theory. In the last five years, revenue has risen from $2.24 billion in 2018 to $2.62 billion in 2022, at a 5-year compound annual growth rate ((CAGR)) of 1.6%. If we establish a base rate using Credit Suisse’s ( CS ) “The Base Rate Book” , for data for the reference period, 1950 to 2015, we see that 28.8% of businesses achieved a 5-year sales CAGR of between 0% to 5%. In that period, the mean and median 5-year sales CAGR for the period were 6.9% and 5.2% respectively. In other words, despite the annual reports being replete with talk of “growth”, the company is far short of what the typical firm grows by. There is no reason to believe that, post-2015, growth has fallen so much to make First Solar’s numbers look better. The reality is that First Solar is not a growth company. it is growing at a sub-par rate.

A Deeply Unprofitable Business

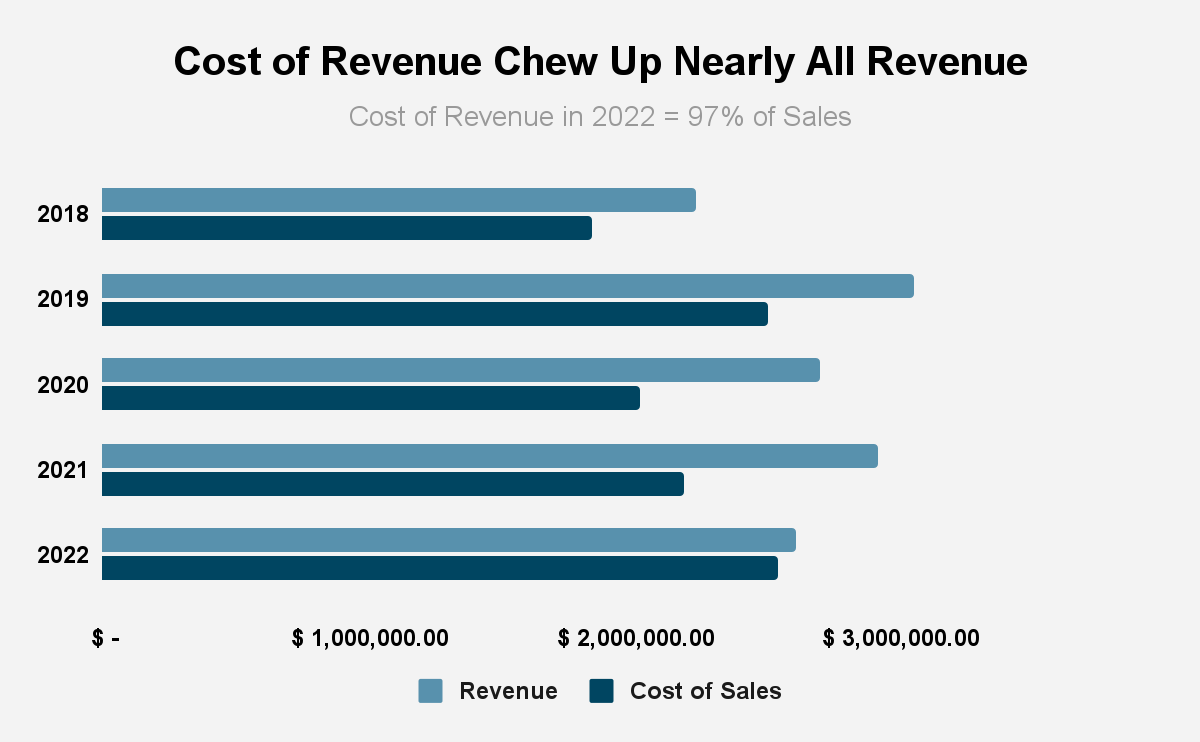

The company’s underlying business model is horrific, with 97.6% of revenues eaten up by cost of sales. The limited growth pathway outlined above suggests that the business does not have a route to meaningful profitability.

{kind=link}

Gross profits have actually declined since 2018, from $392 million in 2018 to nearly $70 million in 2022. Gross profitability, which scales gross profits by total assets, has plummeted, from 0.055 to 0.0084 in 2022. That is far from the 0.33 gross profitability level that Robert Novy-Marx’ research shows is attractive. Gross profitability is a better tool for seeing if a stock is attractive, than P/E multiples. In other words, not only is the firm declining in profitability, it does not screen as attractive.

Operating income has fallen from $40 million in 2018 to -$27 million in 2022. In that time, operating margins have fallen from a razor thin 1.79% to -1.04%. In the 1950 to 2015 reference period, the mean and median operating margins were 11.6% and 12.1% respectively. Once again, First Solar’s operating performance has been subpar since inception.

Net income has risen from -$114.93 million in 2018 to -$44.17 million in 2022. In our reference period, the mean and median 5-year earnings CAGR was 7.3% and 5.9% respectively. We cannot calculate First Solar’s CAGR given the negative values, but it is clear that the firm is deeply unprofitable, despite improvements.

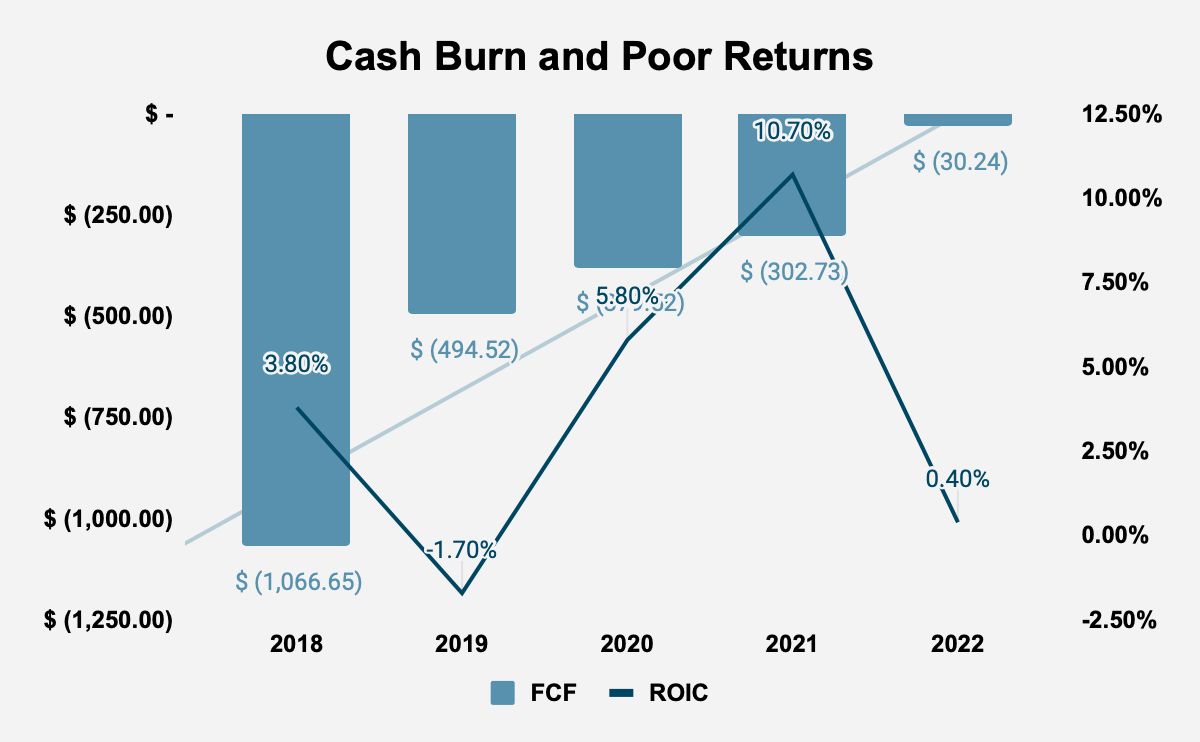

The most powerful predictor of future returns is asset growth. There is an inverse relationship between asset growth and future returns, a phenomenon known as the asset growth effect . This is because, as we discussed in our methodology section, firms tend to overestimate their growth opportunities, and raise too much capital, and invest too heavily, leading to a collapse in returns when the implied growth and subsequent profits do not materialize. This is true especially when a firm does not have sustainable competitive advantages. Despite shrinking profitability, and the absence of a real growth market, First Solar’s assets have grown from $7.12 billion in 2018 to $8.25 billion in 2022, compounding at 2.99%. The question is, is management overconfident and investing too heavily in their business? Well, the returns on invested capital ((ROIC)), which is a strong predictor of the direction of company valuation, has declined from 3.8% to 0.4%, between 2018 and 2022. This decay in economic profitability has occurred at a time where economic profits rose in the wider market . Adding to the intrigue, Mr. Widmar has spoken about the lack of differentiation in First Solar’s competitors, and the differentiation provided by the CadTel technology, but the firm’s returns are undeniably declining.

It is axiomatic that the value of a business is a function of its ability to earn FCF, so, another sign against the firm’s ability to grow corporate value is that FCF has risen from -$1.07 billion in 2018 to -$30.24 million in 2022. In that time, the firm has burnt through $2.27 billion in FCF, or 9.87% of its market capitalization.

{kind=link}

Valuation

First Solar has a price/earnings (P/E) multiple of -0.0019 compared to a P/E multiple of 22.07 for the S&P 500 . The Invesco Solar ETF has a P/E multiple of 18.92. Although you could argue that this shows that the business is “undervalued”, we have already seen that the firm’s gross profitability, a stronger sign of attractiveness than P/E, is abysmal, at 0.0084 against a threshold of 0.33. Finally, with an FCF yield of -0.14%, the company’s FCF is not only trading at a negative yield, we see that the economics of the business is very poor, and it is unlikely to beat the market.

Conclusion

Despite a media and investor clamor around alternative energy, no evidence exists to support the idea that there will be a rapid transition to alternative energies, including solar. In fact, First Solar’s revenue shows that the company itself is not seeing the growth that you would expect. First Solar’s business model is awful, with high costs of sales, poor profitability, declining returns, and high cash burn. Placed alongside the firm’s sensational stock market performance, it is doubtful that the firm can continue to outperform the stock market.

For further details see:

First Solar Has Flown Too Close To The Sun And Should Be Avoided