FSLR - First Solar Isn't Generating Enough Power As An Investment

Summary

- The Inflation Reduction Act might actually be a net negative for First Solar, Inc. in the present economic environment.

- Spending will generate a ripple-down effect on both operating margins and earnings.

- Unjustifiable valuation paired with a bleak future make us extremely hesitant on First Solar, Inc. stock.

First Solar, Inc. ( FSLR ) has been riding numerous clean energy tailwinds as the group has been paraded as the next big market opportunity. However, on closer inspection, we believe that these new developments in solar and their impact on the company haven't been fully digested, leading to speculative gains in First Solar stock.

IRA As A Headwind

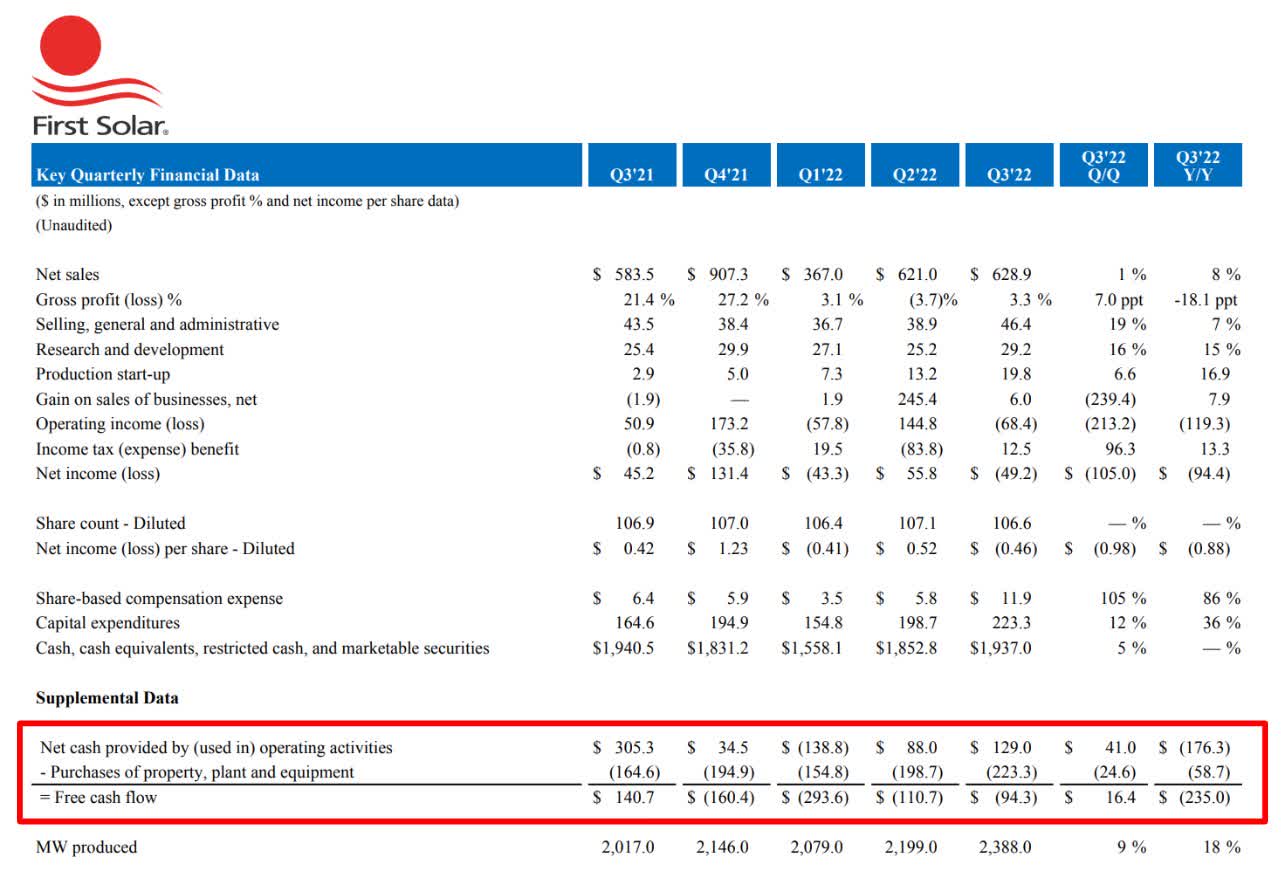

First Solar Q3 2022 Key Quarterly Financial Data Author, Seeking Alpha First Solar Q3 2022 Earnings Presentation

{kind=link}

{kind=link}

{kind=link}

The Inflation Reduction Act ("IRA") was designed to accelerate the transition into solar energy, providing numerous subsidies and tax credits for companies like First Solar to take advantage of.

As a large-scale utility producer, First Solar, Inc. qualifies for the same 30% base investment tax credit ("ITC") as smaller community solar projects do, granted they meet specific wage and apprenticeship requirements. In their Q3 2022 10-Q , they also said that they

expect to qualify for the advanced manufacturing production tax credit under Section 45X of the Internal Revenue Code, which provides certain specified benefits for solar modules and solar module components manufactured in the United States and sold to third parties...

which could add 10% more in ITCs.

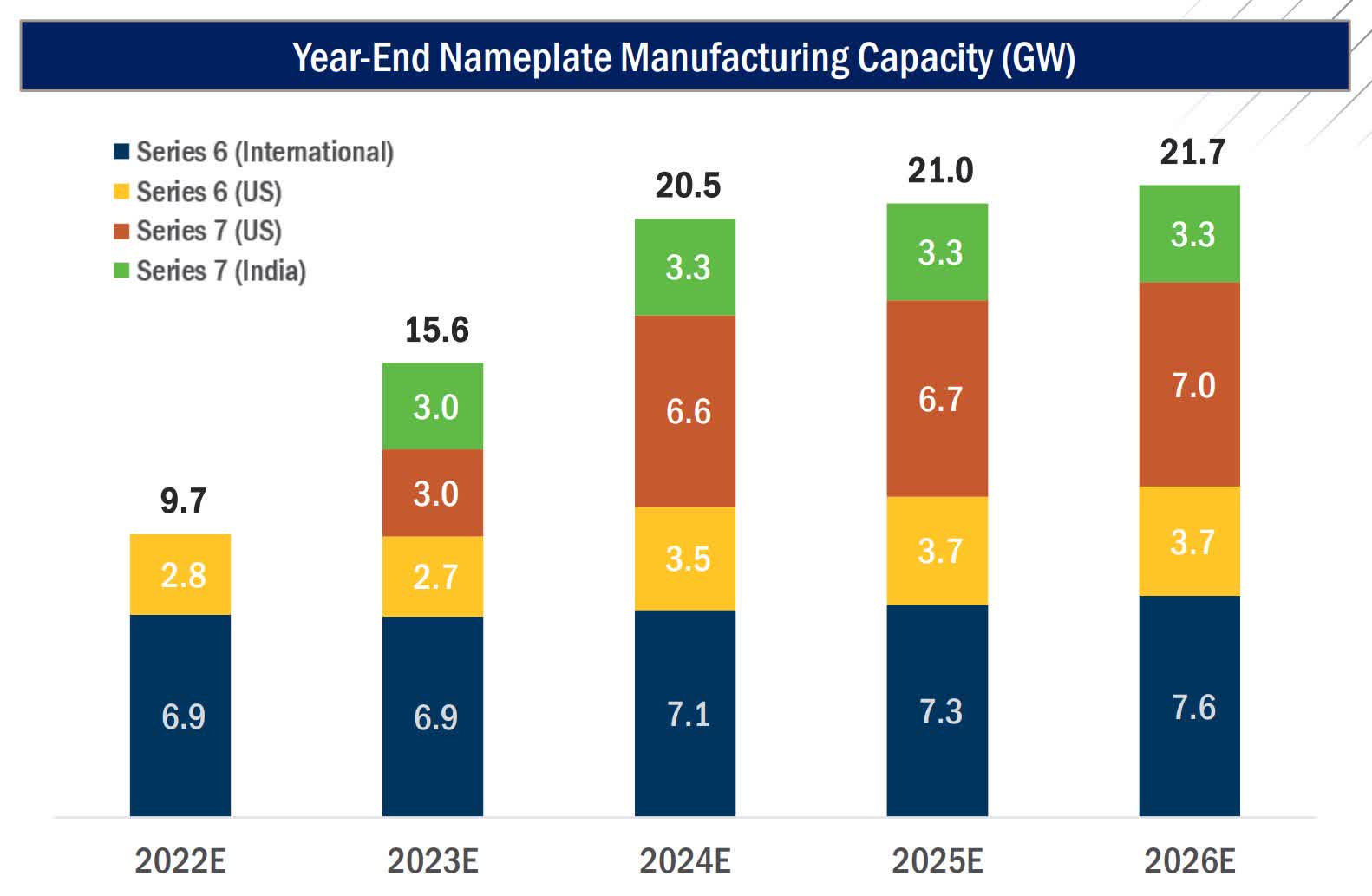

The incentivization to onshore manufacturing came at a strategic time for First Solar, which was already trying to streamline its supply chain and reduce dependence on China. It has rapidly deployed capital with $1.5B in new investments during the past quarter alone, including

-

$200M upgrade for Ohio facility (+0.9 GW in capacity)

-

$270M R&D line at Perrysburg, Ohio facility

-

$1.1B production plant in Alabama (+3.5 GW in capacity).

causing purchases of PPE to be 67% higher from $345M in the first nine months of 2021 to $577M y/y.

Management is assuming that it is cheaper to build facilities now than later due to the vast amount of ITCs they can claim. This will also help meet projected long-term demand, with a 2026 capacity of 21.7 GW, which is 124% higher than 2022 levels, and minimize the future risk of the significant supply chain costs that they are presently facing.

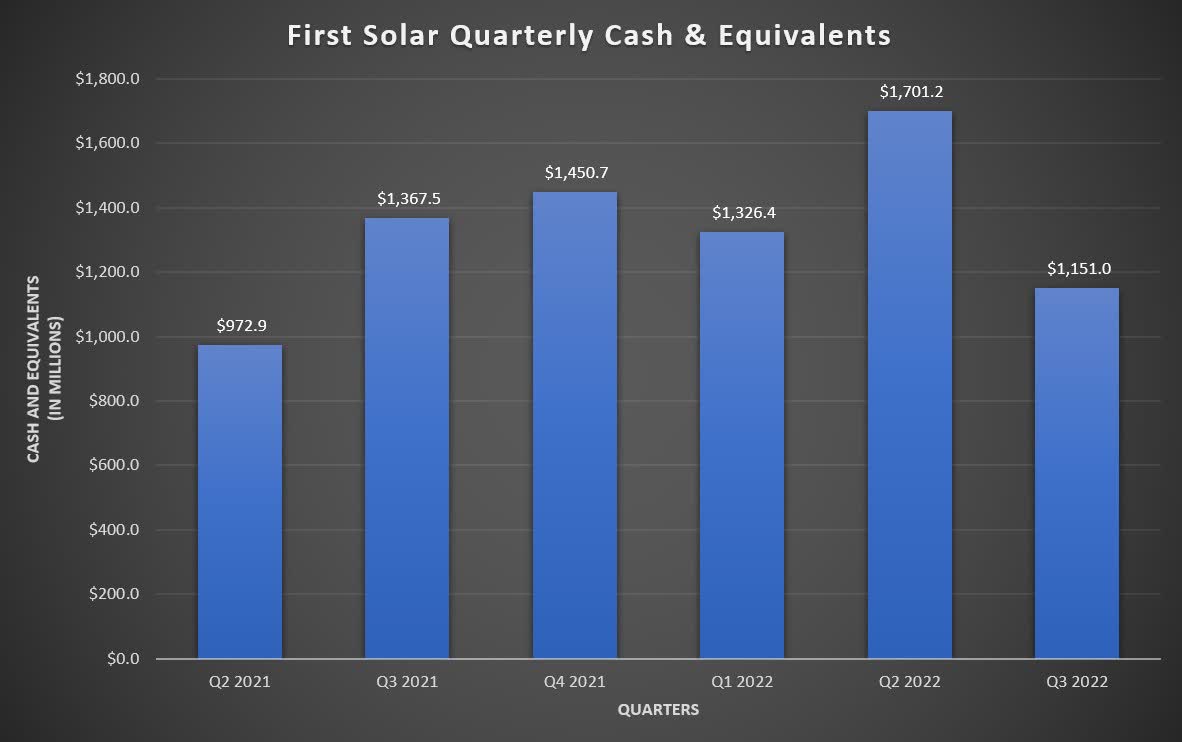

However, with a record $223M CapEx in Q3 2022 , the company has had its 4th straight negative free cash flow ("FCF") quarter. This continues to significantly hamper its cash position (down 32% since Q2 2022) as we move into a recession - a risk with higher rates that could increase debt load.

Creating higher-margin revenue for 2026 and beyond is coming at the expense of current profitability, something that doesn’t bode well with a poor macroeconomic backdrop where investors want more cost-conscious companies, not those investing in growth.

Continued Margin Pressure

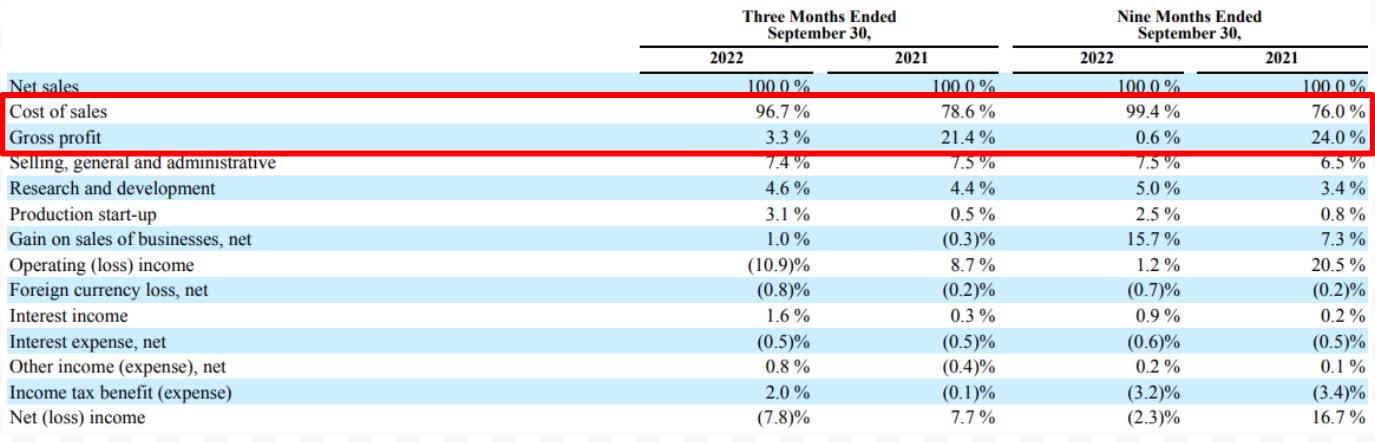

First Solar Q3 2022 10-Q Author, First Solar Q3 2022 10-Q

{kind=link}

{kind=link}

Cost of sales expanded 23.4% in the first nine months y/y, causing gross profit margins to decline to a concerning 0.6%. Higher costs associated with inflation and supply chain issues were the main culprits and a big reason why the company is investing so heavily in efficient manufacturing.

While relief from gross margin pressure is expected as early as Q4 2022 (projected low-end 2022 full-year gross margins is 2.8%) and across 2023 with lower inflationary headwinds, we believe First Solar, Inc.'s rapid increase of new investments will bring operating margins under fire over the next few years.

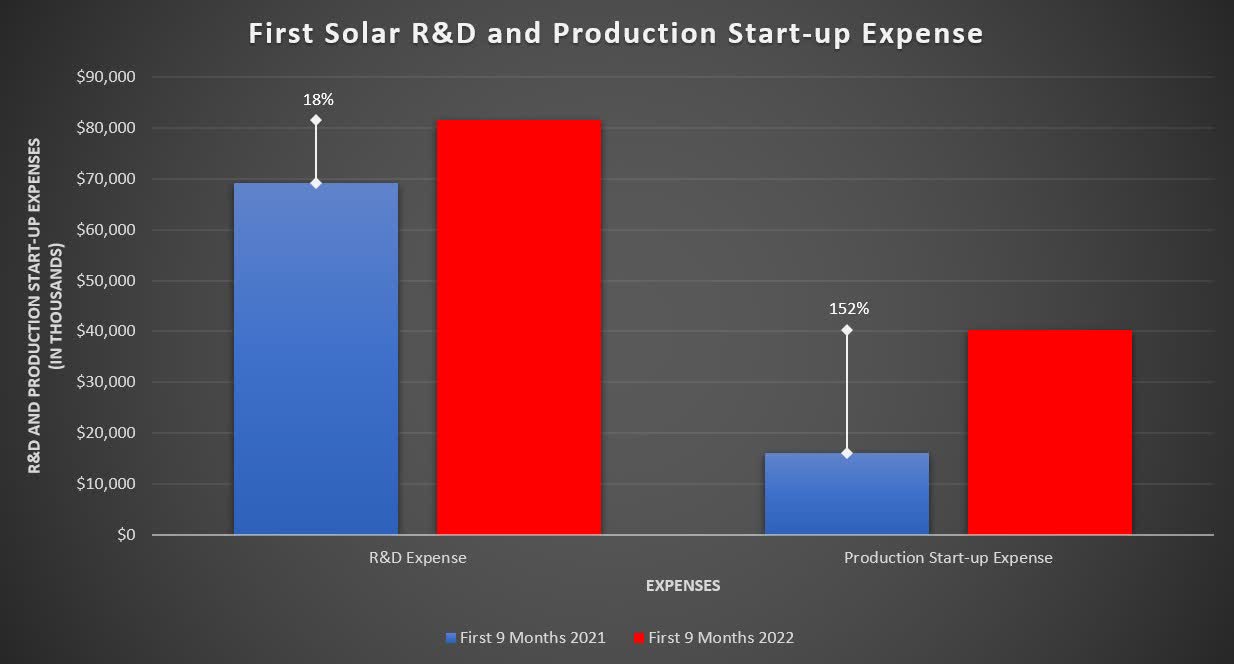

An 18% increase in R&D expense led "R&D as a % of net sales" for the first nine months of 2022 to jump to a record 5.0%, 1.6% higher than in 2020 and 2021. When looking at it in the context of a 23% decline in revenues during the same period, more spending by management isn’t exactly translating into more revenues.

Production start-up costs were another key expense that grew an astounding 152% as First Solar highlights in its Q3 2022 10-Q that it

incurred production start-up expense primarily for our third manufacturing facility in the U.S.

and

incurred production start-up expense primarily for certain manufacturing upgrades at our facilities in Kulim, Malaysia.

Both expenses will continue to rise as the company spends more on manufacturing and innovation, limiting earnings growth even in a best-case scenario of more capacity, higher gross margins, and increased demand.

Bubbled Up Valuation

Author, Seeking Alpha, Morningstar

{kind=link}

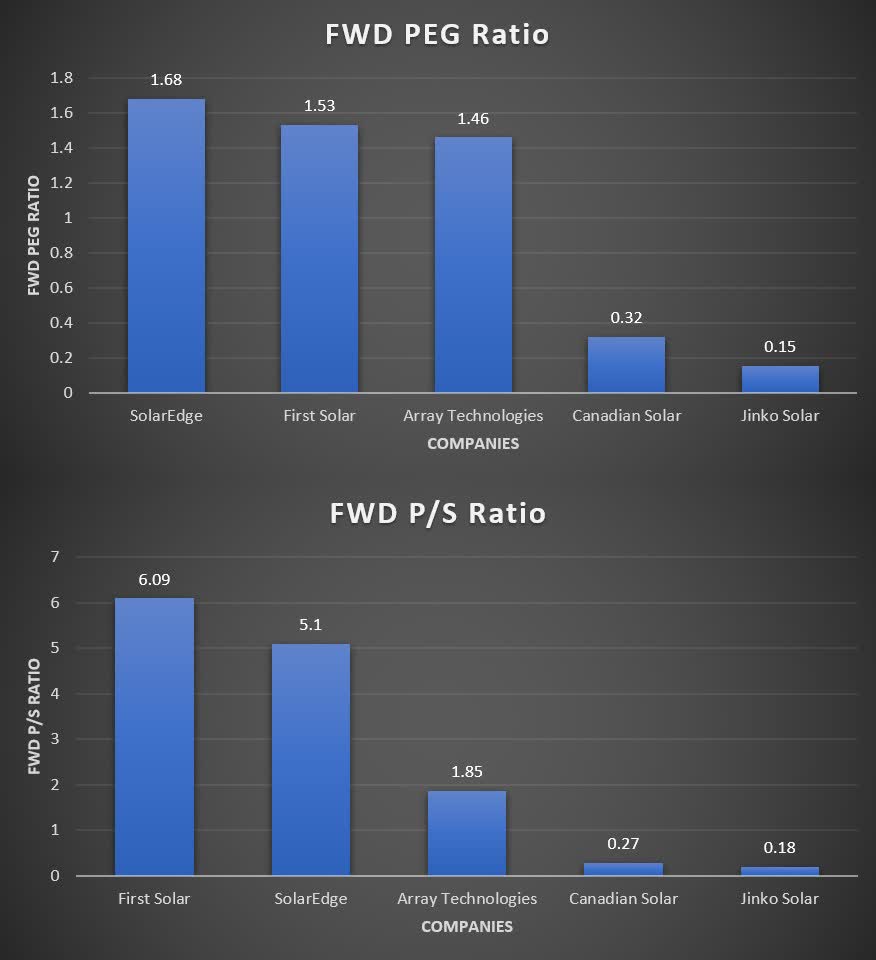

As First Solar's stock has irrationally doubled since the IRA gained traction in congress, it has brought an unreasonable valuation with abysmal earnings and revenue trends.

On a PEG basis, it has the second-highest ratio compared to other utility-scale solar companies, showing that the stock has run up too much in relation to future earnings growth and that its earnings aren't growing as fast as others.

The company also has the highest P/S multiple relative to competitors, meaning that its stock price isn't trading on fundamentals or considering the decline in sales and continued downward revisions for 2023.

Outlook Moving Forward

We view First Solar as a fragmented growth story, where it will take multiple fiscal years for everything to come together, if at all.

Despite the IRA providing structural tailwinds for the solar industry and creating an unprecedented opportunity for companies to ramp up manufacturing capabilities, it couldn’t have come at a worse time given a recessionary economy and less capital from risk-on investors.

The company continues to bleed cash in hopes of future revenue growth and probability is in serious question due to short-term supply chain costs and long-term R&D and production-related costs which will force earnings to lag behind potential revenue growth.

With a shaky future ahead, we recommend against putting money to work in First Solar, especially at this price point.

For further details see:

First Solar Isn't Generating Enough Power As An Investment