FSLR - First Solar: Leading With Innovation While Structural Obstacles And Competition Remain

Summary

- Strong foundation has been set up for a long-term growth in the solar industry, and First Solar is well positioned to capture that.

- The competition in the industry is heating up and bringing down spot prices as a secular trend. The company responds with significant expansion plan in capacity and manufacturing process.

- Innovation in its technology remains the key for the company to fend off competition in the long term and maintain margin and growth.

- Infrastructural obstacles and structural imbalance in solar industry will still be at play for near term and long term.

Investment Thesis

First Solar (FSLR) has great technological and manufacturing capacity to support its medium term expansion, and is well positioned to capture the increasing demand in solar power from the US and abroad. However, a lot of the explosive growth seem to have been priced in its price while growing maturity and heating competition could drive down the spot prices for the long term. The company could use the macro tailwind to improve its financials and continue striving for further innovation and growth.

Company Overview

First Solar is an American solar technology company and global provider of PV ("photovoltaic") solar energy solutions, with R&D labs in California and Ohio. The company manufacture and sell PV solar modules with an advanced think film semiconductor technology that provide a high-performance, lower-carbon alternative to conventional crystalline silicon PV solar modules. It also committed to reducing the environmental impacts and enhancing social/economic benefits from raw material sourcing to end-of-life module recycling. It is the largest thin film PV solar module manufacturer in the world and the largest PV solar module manufacturer in the Western Hemisphere.

Strength

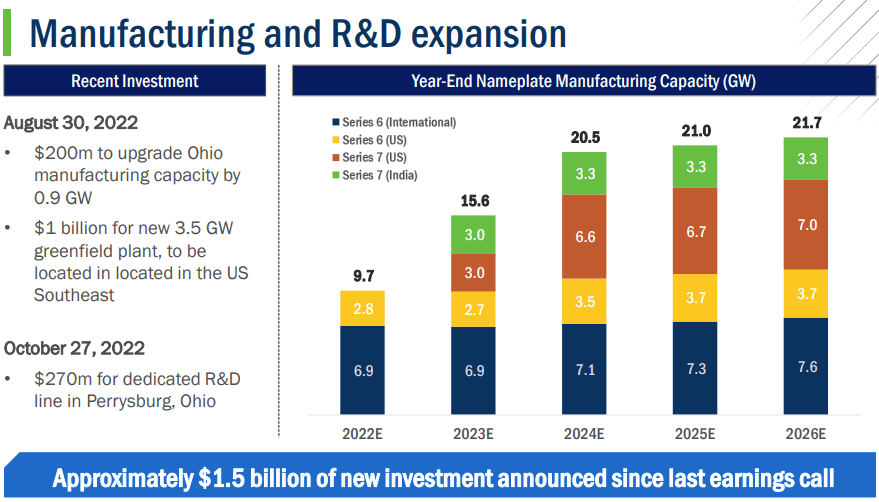

First Solar's strength and advantage mostly lie in its technological innovation, manufacturing process and continuous research and development. The company has a module semiconductor structure of a single-junction polycrystalline thin film that well matches to the solar spectrum. It delivers competitive wattage that using only 2% of the semiconductor material used in conventional crystalline silicon modules. Advanced module technology is essential to First Solar's business strategy, and producing the modules efficiently is key to its profitability at large scale. It has a high through-put manufacturing environment that automates all steps into a continuous flow line. It gave an example: a sheet of glass enters the production line and can be transformed into a completed module ready for shipment in a few hours. Then when it comes to the quality control and reliability assurance program, it conducts acceptance testing for electrical leakage, visual quality, and power measurement to meet industry and internal standards before product shipment. In other words, the company's business success and competitiveness deeply rely on its technological advancement and manufacturing implementation. It's not surprising the company continues to strengthen its lead on this front with expansion. It expected its nameplate manufacturing capacity to be doubled by 2026 comparing to the end of 2022.

First Solar Manufacturing and R&D Expansion (Company Q3 2022 Presentation)

{kind=link}

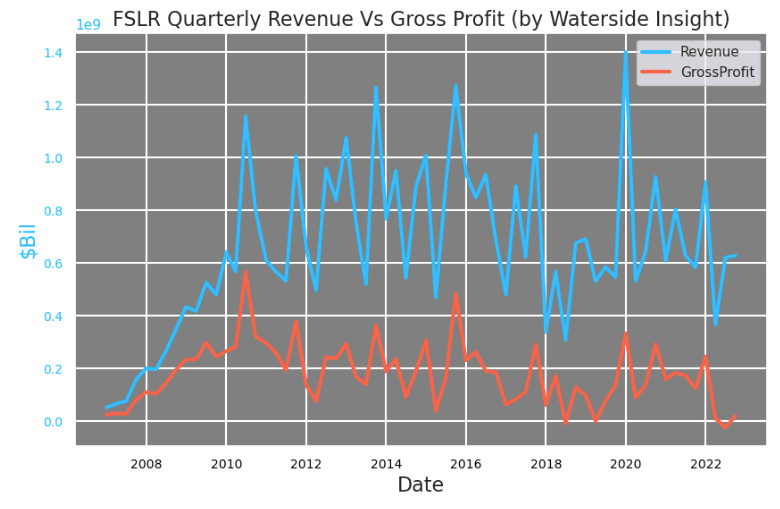

If we regard the introduction of Inflation Reduction Act in May last year was opening up a new era in the green tech industry, perhaps we can regard the past performance of First Solar as pre-IRA. During its pre-IRA period, the company's revenue was volatile on a quarterly basis, but stable as it stays within a range. Both revenue and gross profit picked up in the latest quarters from a slip in early 2022, albeit are still at their lower level historically. According to the company, the low gross profit has to do with under-utilization losses of $10-15 million and a legacy systems business asset Luz del Norte project in Chile that produced $45-50 million losses. Reviewing over 15 years' of data shows its gross profit has a slight downward trend, but higher revenue generally associated with higher gross profit. It means scale is critical to the company's bottom line, both in production and sales. It echoes back to what we just alluded to that the company's emphasis on expanding manufacturing at scale.

First Solar Quarterly Revenue vs Gross Profit (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

If we only look at the past ten years, its net sales in dollar term actually have come down. What could be the causes?

First Solar Past Ten Years Net Sales (Charted by Waterside Insight with data from the company)

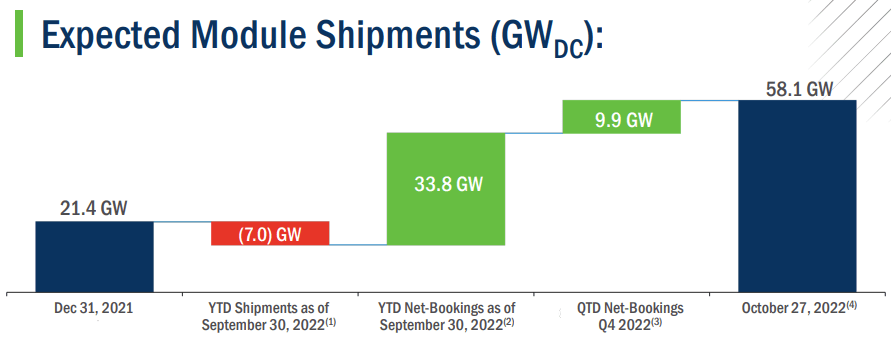

The company's expected module shipment by Q3 was 14.3 GW, 30% lower than the full year shipment of 2022, while compensated by 43.7 GW net-bookings by Sep 30, 2022. They bring the total expected module shipments beyond that date to 58.1 GW. So the lower net sales were not from the sales of modules, which is the biggest segment of its sales and revenue.

FSLR (Company Q3 2022 Presentation)

{kind=link}

Looking at its revenue by category by Q3 2022, we can see its module segment although slightly lower YoY, it wasn't anything substantial. The biggest drop came from its solar power system, which is part of its power system business. It went from $311 million in Q3 2021 to only $2.4 million in Q3 2022. Its power system business has components of project development, EPC (Engineering, Procurement, and Construction)services and Q&M (Operations and maintenance) services. This accounted for about 15.4% loss of net sales from Q3 2021's figure.

First Solar Revenue by Segments (Charted by Waterside Insight with data from the company)

In terms of prices, the solar industry has matured fast in the past ten years and the prices have been heading downward as a long term secular trend.

Cost of Rooftop Solar for Typical Residential Home (Company Q3 2022 Presentation)

So the decrease in net sales over the past ten years could be attributed to the long term trend of lower spot prices, while the recent fall could be due to some bottleneck causing power system development delay, in addition to the higher logistics cost pressure the company cited in its earnings call . In the meantime, its sales volume of modules as its main segment remains robust.

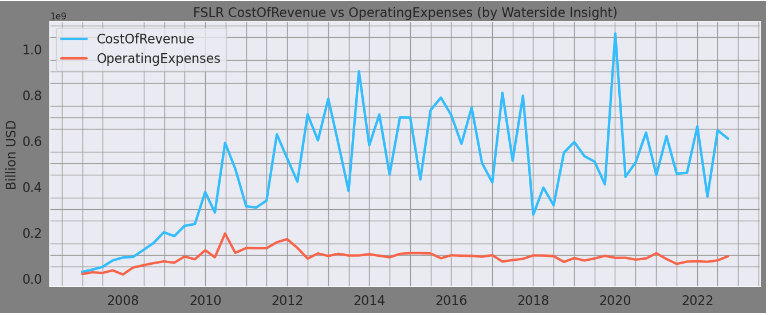

On the cost front, the company have both operating expenses and cost of revenue under control. They are at their average level without any large increase. As a green energy generator manufacturer, the sustainability in First Solar's production and operational process is especially important to the business viability. The company is the only PV solar module manufacturer with global in-house recycling capabilities. So after factoring this into its cost and expenses, it shows the company is doing a good job in this regard. Going forward, it is important to see, with the large expansion it planned on having, how will cost and expenses evolve in the upcoming quarters and years.

First Solar Cost of Revenue vs Operating Expenses (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

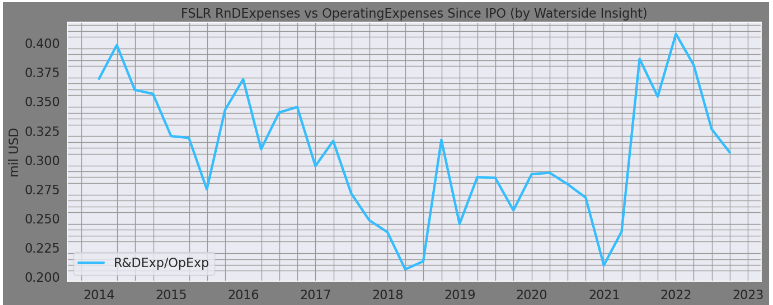

Closely related to operating expenses, its R&D expenses as a percentage of the operating expenses have come back down to average level after reaching a peak in late 2021 early 2022. Given the relatively flat operating expenses, this fluctuation mostly reflected the different spending level for R&D alone. For First Solar, the R&D spending is actually a direct contributor to the cost reduction. It cited its R&D model's vertical integration, from advanced research to product development, manufacturing, and application, as its advantage over competitors. It means higher R&D spending should bring down future operating expenses as it aims at increasing wattage gains with lower cost. The current level seems reasonable for what its goal is.

First Solar R&D Expenses vs Operating Expenses (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

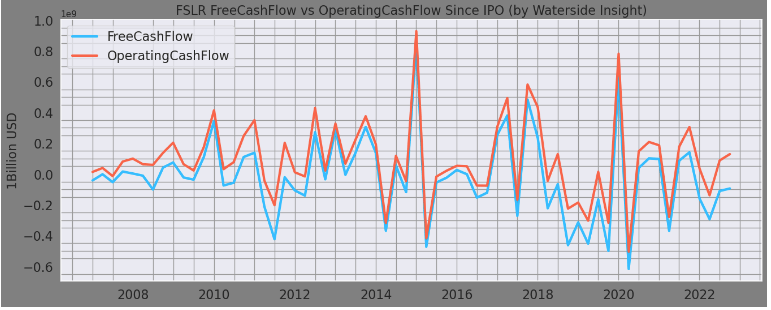

The company's operating cash flow has been improving as well as its free cash flow.

First Solar Free Cash Flow vs Operating Cash Flow (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

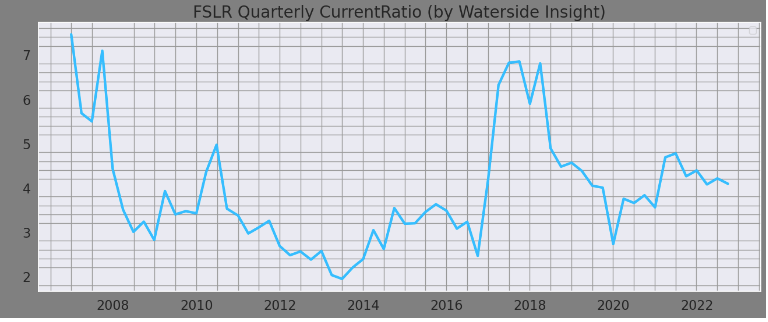

And its liquidity position is still in good shape to support near term expansion.

First Solar Quarterly Current Ratio (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

Overall, we find First Solar in a strong growth position with competition and headwinds remain. The company has great momentum moving forward in both development plan and manufacturing expansion.

Weakness/Risks

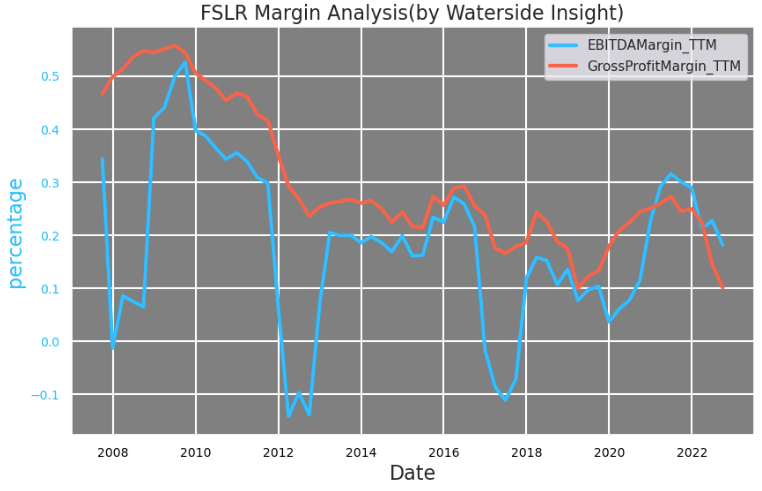

As the solar industry matures, the competition has inevitably drive down profit margin. We can see the profitability of First Solar has turned lower as a long term trend. Although EBITDA margin is still at historic average, gross profit margin has turned to almost its lowest.

First Solar Margin Analysis (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

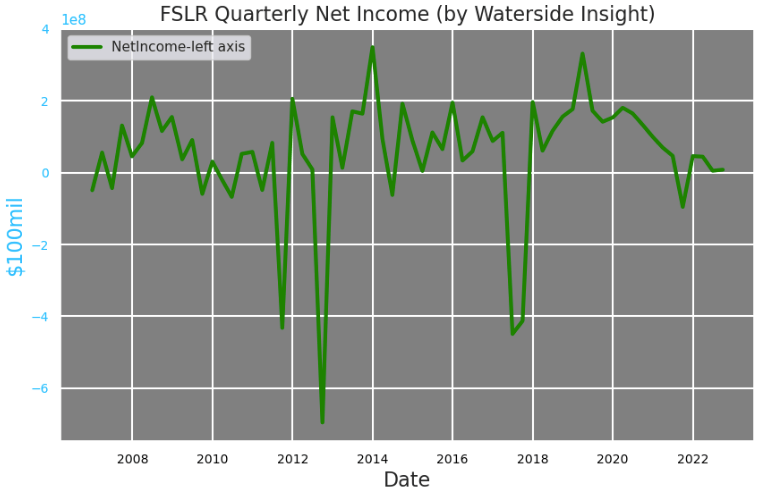

Net income has turned from $337 million gain in 2021 into a small losses of $37 million in 2022, mostly due to lower net sales while operating expenses stayed at similar level.

First Solar Quarterly Net Income (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

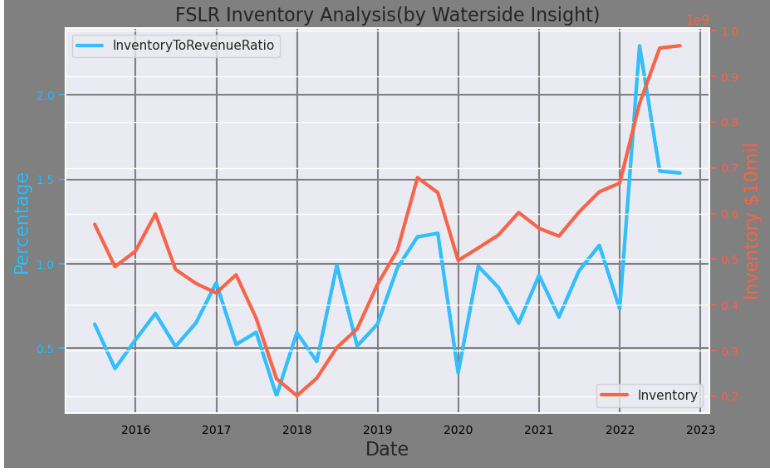

The company's inventory increased in absolute term, although on a relative to revenue basis has come down after the last quarter's improvement of revenue. Revenue will need to keep on the recovery trend to bring it back down to its average level.

First Solar Inventory Analysis (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

In general, we see the expected jump of growth in 2023 to be a necessary improvement to First Solar instead of a next level upgrade. The company needs to lift its financials back to its average historical level before taking off.

Big picture: Macro Tailwind, Structural Obstacles, and Competition Co-exist

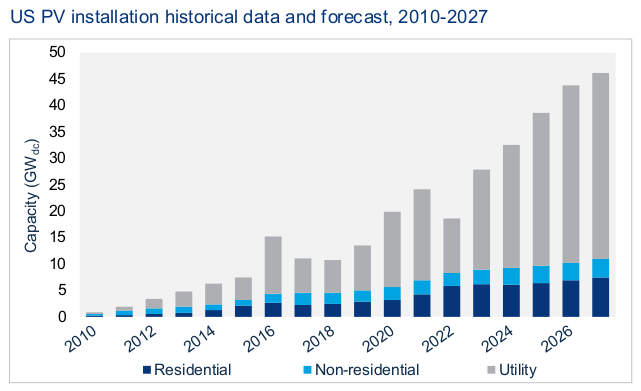

The Inflation Reduction Act (IRA) will initiate huge new spending on clean energy, collectively $369 billion investment in the modernization of the American energy system. The company expect most of the provisions in IRA to take effect starting in 2023. This new wave of investment likely to last for years if not over a decade in the span. For solar power, Wood Mackenzie and SEIA forecast about 27.9 gigawatts of additional US solar capacity this year, which is a big increase YoY with estimated 18.6GW in 2022.

US PV Installation historical data and forecast 2010-2027 (Wood Mackenzie)

{kind=link}

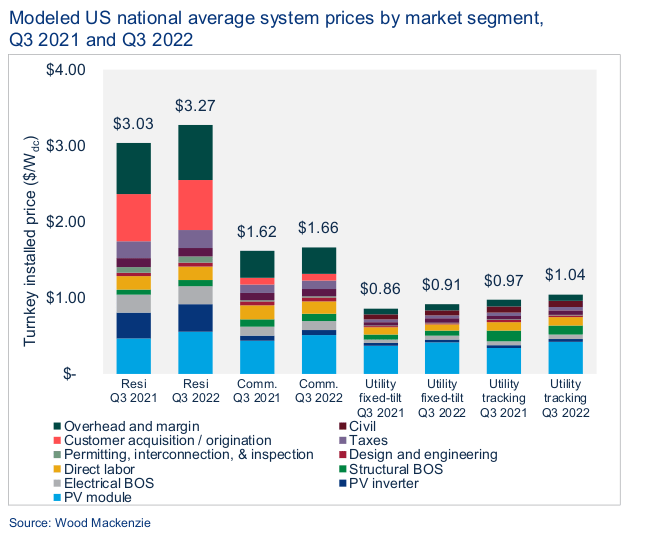

Moreover, removal of the technical obstacle of battery storage has become reality for many solar power generators and households, which increased solar power's competitiveness with natural gas. So increased demand combined with factors of higher logistics and commodity cost, the national average system prices in the US have increased instead in the past year, according to data compiled by Wood Mackenzie and SEIA.

Modeled US National average system price by market segment (Wood Mackenzie )

{kind=link}

Under this backdrop, investors' enthusiasm was ignited and it spurred rallies in First Solar. However, there are structural obstacles that might cause delays. The US depends on Asia for at least 80% of its panel supply, and the sanction against China, who provide about half of the world's supply of polysilicon, will cause certain delay in the supply chain. And domestically, there is lengthy wait for approval to connect projects to existing state or regional power grids. So it might still take a few years for all necessary conditions to line up for a complete take off of the industry.

Overall, the competition in the industry continues to heat up. Since recent collapse of material cost, leading Chinese module manufacturers are planning on ramping up production for the year. In response to the overseas competition, the company positions itself to be a responsible solar manufacturer with industry-leading ESG ratings . And its first factory in India is expected to open in 2H and its 4th manufacturing facility in the US is expected commence operations in 2025.

Polysilicon and wafer price plummet (Bloomberg NEF)

In the meantime, new products, such as bifacial modules that capture diffuses irradiance and reflected light on the back side, or N-type solar cells that provide improvements to efficiency, performance and degradation advantages, are being introduced by its competitors. The R&D efforts by First Solar will decide its future growth and development from this perspective. The company currently working on the operational and market readiness of their next-generation Series 7 modules and CadTel bifacial modules based on their Series 6 platform. The competition continues to heat up for the company.

As the company put it in its 10-K , it sees the solar industry to have supply and demand structural imbalance from time to time on the path towards maturity, which production capacity exceeds global demand could put pressure on pricing and adversely affect the operational results. We agree and believe long term investors should also price that in for the valuation, while embracing the long term growth trajectory of the industry and the company as the foundation has been laid and set up.

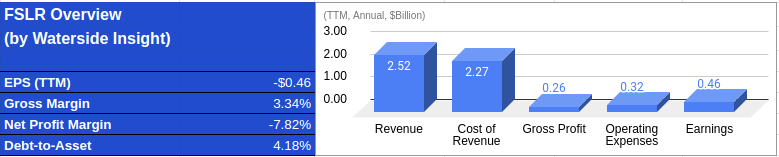

Financial Overview

First Solar Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

Valuation

We take into account of all the analysis above and use our proprietary models to assess First Solar's long term fair value with a ten years forward projection. In our bullish case, the company has positive growth in its cash flow for the next six years, including an explosive upgrade to decisively turn the negative cash flow into high positive value, and eventually its free cash flow reached $4.1 billion annually by 2032; it was valued at $167.11. In our bearish case, the company's growth has a spotty moderation in the next five years, and its cash flow hovers around $3-3.5 billion by 2032; it was valued at $138.71. In our base case, First Solar has similar strong growth as in the bullish case while with some slow down in the next five year, it rebounds and resumes strong growth; it was valued at $149.98. Currently, the price is between our top estimate and base case.

First Solar Fair Valuation (Calculated and Charted by Waterside Insight with data from the company)

Basically, in all scenarios we constructed a strong growth path for the next five to six years for the company without much discount, and only differentiate the next five years after that due to maturity of the industry and re-balance of supply and demand dynamics. This implicitly assumes that First Solar will continue maintain its lead in technological innovation and manufacturing process.

Conclusion

The lower spot price for solar modules due to intense competition will be made up by higher sales volume and the unleashed strong demand following the IRA. First Solar, as the largest solar producer in the US, is in a good position to capture that growth. On the other hand, the structure obstacles and competition could slow down the near term growth while imbalance of the industry from time to time in the long term should be expected. We, as many enthusiastic investors, look forward to a new dawn in the solar industry and a robust growth trajectory for First Solar. But we see a lot of the visible future growth has been immersed into the current market price. We recommend a hold at this level.

For further details see:

First Solar: Leading With Innovation While Structural Obstacles And Competition Remain