FSLR - First Solar: Made In America Sentiment Matters After All

2023-08-20 10:00:00 ET

Summary

- First Solar has beat our expectations again, thanks to its double beat FQ2'23 performance and growing backlog through 2030.

- Combined with the expanding opportunities, it is unsurprising that the management has intensified its capex to capitalize on Made In America sentiments.

- While much of its profitability has directly flowed into its increased manufacturing output, investors need not fret yet, since these are directly accretive to its top and bottom line.

- Investors may also look forward to the potential margin contribution from improved economy of scale, low cost manufacturing in India, and the IRA tax benefit.

- However, it is not prudent to add here with the FSLR stock also failing to sustain its upward momentum after the recent earnings call. Patience for now.

The FSLR Investment Thesis Continues To Be Supported By The Made In America Sentiment

We previously covered First Solar ( FSLR ) in June 2023, discussing its headwinds from the US Treasury's relaxation on domestic solar content, with Chinese-made polysilicon likely to trigger headwinds in its ASPs.

Combined with the glut observed in polysilicon supply through 2024, we had expected to see moderate volatility in its backlog and stock prices in the near term, ending the article with a recommendation for profit taking.

For now, we have been proven wrong after all, since FSLR reported a double beat FQ2'23 earnings call , with revenues of $810.67M (+47.8% QoQ/ +30.6% YoY) and EPS of $1.59 (+297.5% QoQ/ +205.8% YoY).

Much of the profitability tailwind is attributed to its accelerating gross margins of 38.3% (+17.9 points QoQ/ +32.7 YoY), thanks to the higher ASPs commanded by its next-generation Series 7 modules and the regulatory credits from Inflation Reduction Act.

The latter offers a benefit of $0.17 per watt, which already reduced the solar company's cost of sales by $155M in FQ2'23 (+121.4% YoY), thanks to its vertically integrated supply chain. Investors may also be encouraged by the heavier 60% weightage of IRA benefits for FQ4'23, suggesting improved EPS profitability and optics then.

Despite our original pessimism about its prospects, FSLR continues to record excellent demand with net bookings of 8.9 GW in FQ2'23 ( +85.4% QoQ / -14.4% YoY ), naturally growing its booking backlog to 77.8 GW ( +8.6% QoQ / +75.6% YoY ).

Despite its current annual production capacity of ~12.05 GW, planned expansions to ~16 GW by 2024, and ~20.5 GW by 2025, we are still looking at an impressive backlog with deliveries staggered through 2030.

In addition, FSLR has reported further booking opportunities of 78.3 GW, including 48.5 GW of mid- to late-stage opportunities in the latest quarter.

Therefore, it is unsurprising that the management has committed another $1.1B in capex to further boost its overall manufacturing capacity to 14 GW within the US (with 100% of domestically made components) and 25 GW globally by 2026.

These efforts naturally trigger the drastic expansion in FSLR's manufacturing capacity at a CAGR of +28.7% from 2022 levels of 9.1 GW, or +25.9% from 2021 levels of 7.9 GW, thanks to the robust demand for Made In America solar panels.

This same cadence has also allowed the management to iterate its previous FY2023 guidance, with net sales of $3.5B (+34% YoY) and EPS of $7.50 (+1,929.2% YoY) at the midpoint.

FSLR's long-term prospects appear to be bright as well, with the North American region commanding most of its current sales at 83.9% in FY2022 (inline YoY) and long-term booking opportunities at 57 GW or the equivalent of 72.7%.

With a higher average ASPs of $0.32 per watt over the past few quarter, it is evident that the solar company has been able to command its premium since the pre-pandemic days of $0.34 at a blended basis. This suggests the robust consumer demand for cadmium telluride based solar panels in the US and EU, thanks to the ongoing ban for Xinjiang made panels.

Then again, FSLR investors also need to temper their near term expectations, since much of its earnings have flowed directly to its intensified capital expenditure of $1.3B over the last twelve months (+82.3% sequentially), with $1.8B planned for FY2023.

Therefore, we expect its balance sheet to remain stagnant at $1.88B (-17.1% QoQ/ +2.1% YoY), until its capex moderate from H1'26 onwards. For now, investors should simply sit back and enjoy its high growth, while looking forward to the potential margin contribution from its expanded economy of production scale and low cost manufacturing in India.

So, Is FSLR Stock A Buy , Sell, or Hold?

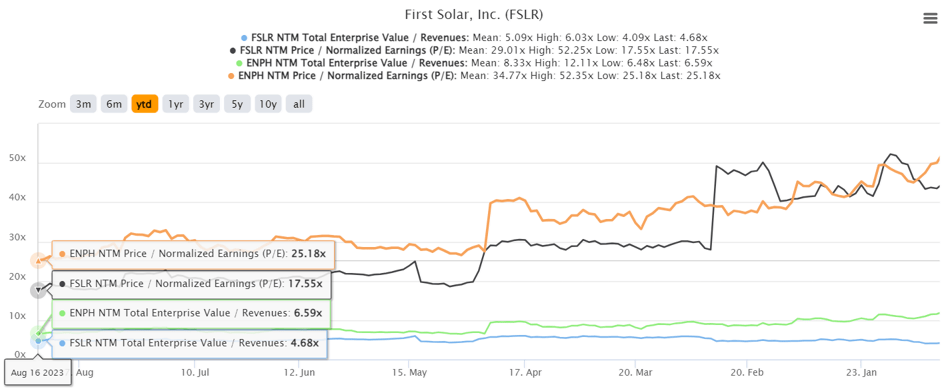

FSLR YTD EV/Revenue and P/E Valuations

{kind=link}

For now, FSLR is trading at NTM EV/ Revenues of 4.68x and NTM P/E of 17.55x, elevated compared to its pre-pandemic mean of 1.22x and 15x, respectively.

The apparent premium is also observed compared to its semiconductor/ solar peers' median of 0.55x and 8.02x, respectively, further corroborating with our Made In America investment thesis.

With FSLR gradually growing into its pulled forward valuations and prices, thanks to its expanding net bookings, it appears that the stock may have found its critical sentiment and stock support levels here.

While some bears may have posited the possibility of solar panels being commoditized in the long term, we believe the stock may be able to maintain its premium, attributed to the geopolitically secure supply chain and the technological edge offered by cadmium telluride.

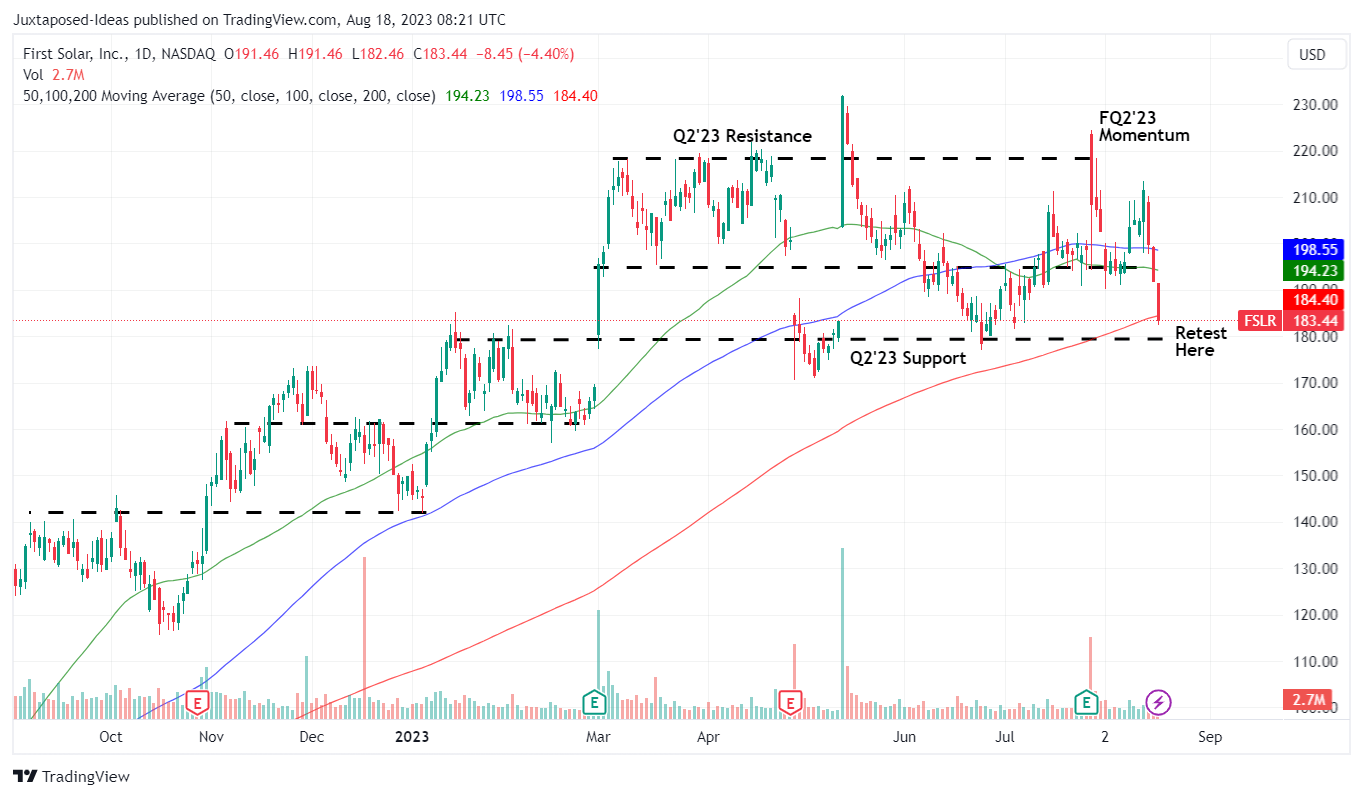

FSLR 1Y Stock Price

{kind=link}

For now, the same premium is also reflected in FSLR's stock prices, with most of its upside potential to our intermediate term price target of $200 already pulled forward. This is based on its normalized P/E and the consensus FY2024 adj EPS estimates of $13.34.

In addition, the stock also failed to sustain its upward momentum after the recent earnings call, potentially triggering moderate volatility in the short term, with it already nearing the Q2'23 support level of $180 at the time of writing.

Therefore, we believe that it may be more prudent to rate the stock as a Hold here and observe for a little longer.

Bottom fishing investors may consider adding between the January/ February 2023 levels of $140 and $160 for an improved margin of safety.

For further details see:

First Solar: Made In America Sentiment Matters After All