FSLR - First Solar: Poised For Growth In A Post-Inflation Environment

2023-12-19 21:26:57 ET

Summary

- First Solar is expanding its production capacity in response to strong demand for its solar modules.

- The Investment Reduction Act should benefit its revenue growth over the next several years.

- The company has operating leverage, and increasing sales should boost profitability.

- The Federal Reserve potentially lowering interest rates could be a tailwind in 2024.

Investors' concerns about the Federal Reserve raising interest rates from March 17, 2022, to July 27, 2023, eventually halted a stock rally in First Solar's ( FSLR ) shares that started halfway through 2022. The stock started its rally based on investor optimism about favorable legislation passed by the U.S. government last year. However, pessimism over the near-term future of the renewable energy sector, weighed down by the Federal Reserve's relentless campaign of raising interest rates, eventually countered optimism over First Solar's future growth prospects.

Rising interest rates negatively impact renewable energy projects by making them more expensive to finance. As a result, the growth outlook for companies in the renewable sector has dampened. For example, NextEra Energy Partners ( NEP ) cut its unit growth rate assumptions from 12%-15% to 5%-8% until 2026. Additionally, the Chief Executive Officer ("CEO") and Chief Financial Officer ("CFO") of ChargePoint ( CHPT ), the world's largest network of electric vehicle charging stations in North America and Europe, resigned in November amid dismal prospects for the company. First Solar has not been immune from the sector's woes, and the stock has pulled back since May 2023 in line with many of its peers in the renewable industry, underperforming the S&P 500.

Now for the good news. Inflation has tapered off throughout 2023 to reach 3.1% in November, in sight of the Federal Reserve's target rate of 2%. The Federal Reserve Chairman Jerome Powell indicated last week that he and the rest of the board may lower interest rates up to three times in 2024, potentially turning headwinds for First Solar into tailwinds, making now an excellent time to start considering an investment in the company. This article will discuss what First Solar does, its growth drivers, its valuation, and why clean energy investors should strongly consider buying this stock.

What the company does to generate revenue

First Solar is primarily a solar panel manufacturer known for its advanced thin-film photovoltaic modules after selling off its development business over the last several years. Its modules are well-suited for and often chosen by developers in utility-scale solar projects and commercial and industrial applications. The solar panel manufacturing business has historically been highly cyclical. The chart below shows that quarterly year-over-year revenue growth can even change radically from quarter to quarter.

Although the solar panel manufacturing industry has enormous competition, has a reputation of competing mainly on costs, and some argue it is largely commoditized, there are reasons investors should start paying attention to the company. Let's discuss how the company can differentiate in this cutthroat industry.

How does it differentiate from competitors?

Management believes it can differentiate through its technology. The company manufactures its modules using cadmium telluride (CdTe), which is different from most of its competitors, who commonly use crystalline silicon (c-Si) in their solar panels. Management believes CdTe technology has several advantages over c-Si and lists the following advantages on its website :

From its inception, thin film Cadmium Telluride (CadTel) photovoltaic (PV) technology demonstrated a number of qualities that led First Solar to select it over conventional technologies, like crystalline silicon (c-Si). Qualities that included lower cost, superior scalability, and a higher theoretical efficiency limit. Over time, and with more than $1.5 billion invested in research and development, First Solar has also been able to harness other advantages that are unique to the semiconductor.

Source: First Solar website

The image below shows a few energy yield advantages management believes its CdTe panels have over c-Si panels. First, CdTe panels have a better temperature coefficient than c-Si panels in warmer climates, meaning in plain English that CdTe panels produce more energy than c-Si in hot climates. Second, CdTe has a better spectral response in humid conditions, meaning CdTe panels produce up to 4% more power than c-Si in humid environments. Solar panels must perform excellently in those climates since most of the world's solar capacity gets installed in hot and humid areas. Third, the company claims that when developers use its panels with trackers, a system that adjusts the panels' tilt angle throughout the day to capture more sunlight, CdTe panels are 1% more effective than c-Si panels. Last, management claims that CdTe has better features that reduce the buildup of snow and dirt on the panels, which can reduce the effectiveness or even damage a panel.

{kind=link}

The company doesn't just sit back and rest on its laurels. Management understands that CdTe panels have weaknesses and invests in improving the technology. Some of its newest upcoming innovations include bifacial energy generation, a technology showcased in Germany in June this year. First Solar's Chief Executive Officer ("CEO") Mark Widmar explained bifacial energy by saying, " The technology features an innovative, transparent back contact pioneered by First Solar's research and development team, which in addition to enabling bifacial energy gain, allows infrared wavelengths of light to pass through rather than be absorbed as heat, and is expected to lower the operational temperature of the bifacial module and result in higher specific energy yield. "

Another innovation First Solar is working on is quantum dot technology with a nanotechnology company, UbiQD. Solar Power World reports that these two companies are working to integrate semiconductor nanoparticle technology into solar panels, potentially increasing efficiency. However, this technology is in the very early stages of development, and there is no telling if this effort will succeed.

One technology the company has already incorporated into its panels is its CuRe technology, which is a differentiator for solar panel longevity. It significantly reduces degradation rates. No developer wants to buy a solar panel that rapidly degrades as that is lost power over time, which negatively impacts the financial viability of a utility-scale solar project. The company claims that its Series 6 CuRe solar panel technology released in 2021 has a warranted degradation rate of 0.2% per year , a solid performance. However, third parties have yet to verify the accuracy of First Solar's claims. Additionally, other companies are working on technology with similar benefits.

Outside of technology, CEO Mark Widmar identified several other factors that he believes differentiate First Solar from the competition. He said :

We positioned the company around points of differentiation that we thought could create value, whether it was inherent in our technology, inherent in our vertically integrated manufacturing process, strength of our balance sheet. All those points of differentiation, we believe, created value and created a different investment thesis for solar -- unique to First Solar.

Source: First Solar Investor Day 2023

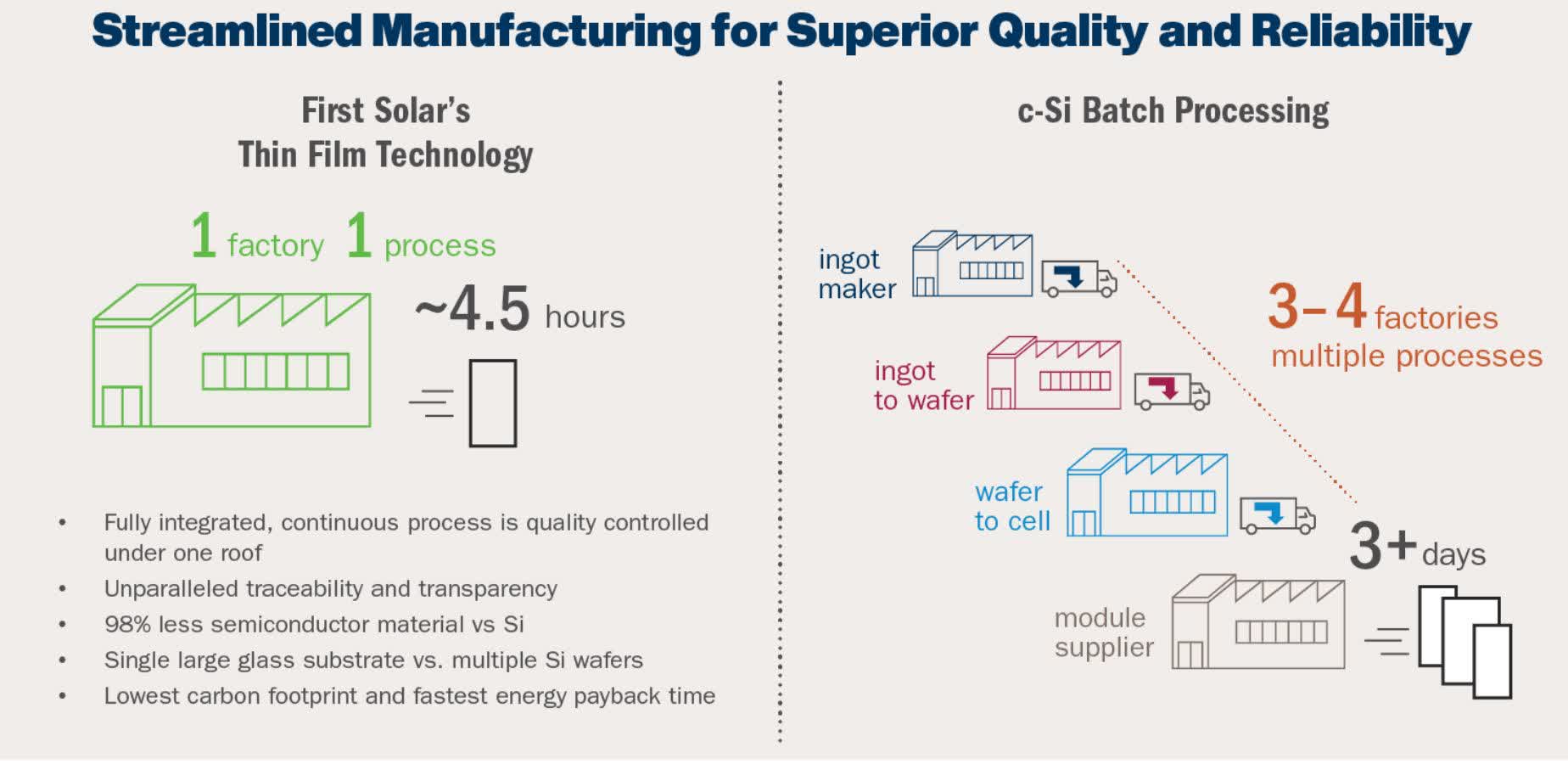

A vertically integrated manufacturing process theoretically gives First Solar several advantages competing on a global scale that include economies of scale from operating extensive integrated facilities, a smaller carbon footprint, lower risk of supply chain disruptions resulting from less use of international global supply chains, better quality control, faster energy payback time, and an increased ability to innovate.

{kind=link}

The company has a magnificent balance sheet with $1.8 billion of cash and short-term investments against $500 million in long-term debt. First Solar has a debt-to-equity ratio of 0.08, generally a positive sign indicating the company is financially stable. It has a quick ratio of 2.3 as of the end of September, a sign it can pay off its short-term obligations. First Solar's balance sheet sticks out in an industry where many solar companies go bankrupt; over 100 met that fate in 2023.

Finally, the CEO talked about "trust" being a differentiating factor. When people call solar panel manufacturing "commoditized," they often ignore that trust can be a differentiating factor that can even sometimes outweigh a lower cost. CEO Mark Widmar said at First Solar's Investor Day 2023:

We are a trusted partner. We deliver certainty. Investments, billions of dollars of investments can be made, relying on First Solar to deliver their commitments. It's a unique value proposition that we have in the marketplace. If you look at it from a crystalline silicon standpoint, there's concern around trust. There's a lack of trust. When you're making development decisions that can be multiyear projects, hundreds of millions of dollars and that $1 billion projects, to have somebody you can't rely on, to try to have somebody not deliver against their commitment, whether it's on price or supply, to have to redesign your project because you have to find a new supplier, to have to go out and refinance your project or find alternative sources of financing because your supplier didn't live up to their commitments. The value of that certainty and that value of that relationship that we have with our partners is only increasing...

Source: First Solar Investor Day 2023.

The above factors are potentially why First Solar sold out all its manufacturing capacity through 2026 despite a heavily competitive environment.

The Inflation Reduction Act

First Solar enjoyed a massive rally from mid-summer 2022 to mid-summer 2023 on the back of Congress passing the Inflation Reduction Act ("IRA") and the President signing it into law. The IRA expanded the maximum credit rate under the Advanced Energy Project Investment Tax Credit (48C ITC) from 30% to 40%, which the government provides for purchasing and commissioning property to build energy projects like solar panel manufacturing facilities, which benefits First Solar when they build new plants in the USA. Even before IRA became law, First Solar was building new U.S. solar panel manufacturing facilities as part of its strategic plan. The company is in the process of creating new manufacturing plants in Alabama, Louisiana, and Ohio. One caveat: 48C ITC may not produce an immediate benefit, as constructing new facilities takes time.

First Solar 2023 Investor Presentation.

{kind=link}

The image below shows the estimated time for bringing the new facilities online. On another note, the picture also shows the completion of a solar plant in India. Management intends the Indian plant to sell mainly into that country's domestic market. If you listen to the company's earnings calls and Investor days, you might sometimes hear management talk about only investing in growth when they see demand ahead. This rapid expansion of manufacturing facilities indicates that management believes there is heavy demand for its solar panels, and they expect robust sales growth ahead.

First Solar Third Quarter 2023 Investor Presentation.

{kind=link}

The IRA also established the Advanced Manufacturing Production Tax Credit (45X MPTC), providing tax credits for the value of specific, domestically produced clean energy components, including solar modules. As First Solar manufactures solar modules in the US, its U.S.-based module production can benefit from 45X MPTC. If you have followed First Solar since 2022, you might already know why IRA should drive substantial revenue growth for First Solar over the next several years.

Expect improving gross and operating margins

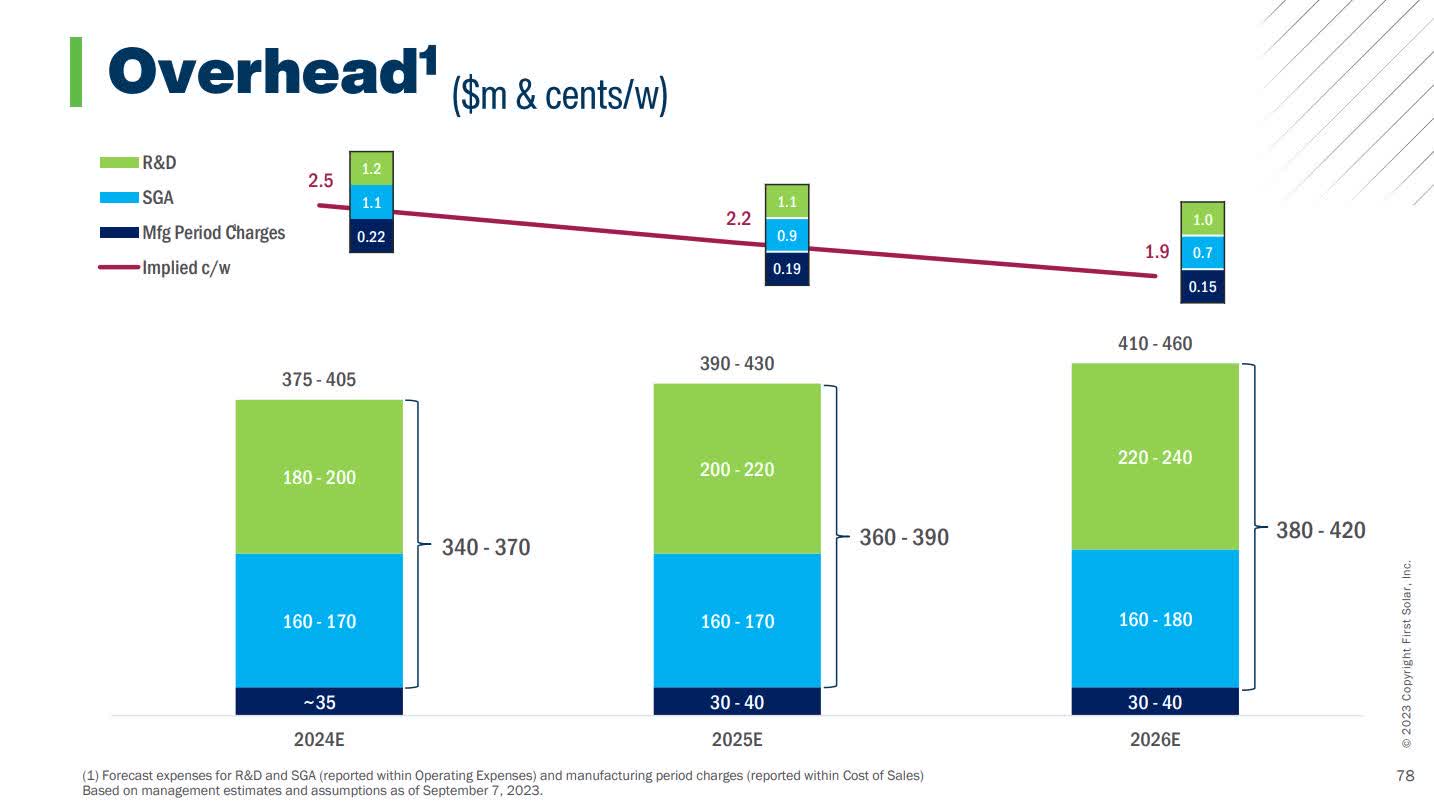

At First Solar's 2023 Analyst Day, the Chief Financial Officer ("CFO") talked a lot about the company having " a largely fixed operating cost structure, " hinting that the company can scale its business and increase its margins as it grows. Companies with a higher proportion of fixed costs versus variable costs can benefit from economies of scale as they grow. Increasing production volume spreads fixed costs over more units, lowering the average cost per unit and boosting margins. The company provided the following image, breaking down its overhead costs .

{kind=link}

The black on the chart that management calls "Mfg Period Charges" represents the overhead costs (around $35 million in 2024) related to the production process. Most of First Solar's overhead costs are operating expenses: Selling, General, and Administrative (SG&A) are in blue, and Research and Development (R&D) are in green.

As you can see above, management forecasts flat SG&A expenses between 2024 and 2026, indicating efficient cost management. In contrast, the company projects R&D expenses to increase, as the company intends to invest in improving its thin film solar modules. Note that although R&D costs rise in dollar terms in the bottom bar chart, those costs decrease on a cents-per-watt basis on the top bar chart due to economies of scale, meaning the cost per unit of production decreases as production volume increases. First Solar forecasts total overhead costs of around $0.02 per watt in 2026. First Solar CFO Alex Bradley said it this way at Investor Day:

You see the value of scale. So here, we're leveraging our fixed cost structure and you're seeing on a cents per watt basis, SG&A coming down by about a third. R&D, I just said to you, we are increasing dollar spend. But when you take a value of scale, you're still reducing R&D on a per watt basis. So when you look at this overall, by 2026, we see ourselves just under $0.02 a watt of overhead, which we believe to be globally competitive .

Source: First Solar 2023 Investor Day.

The above commentary suggests that First Solar has operating leverage. Why is having operating leverage significant? Investopedia says it this way :

In good times, operating leverage can supercharge profit growth. In bad times, it can crush profits.

Source: Investopedia.

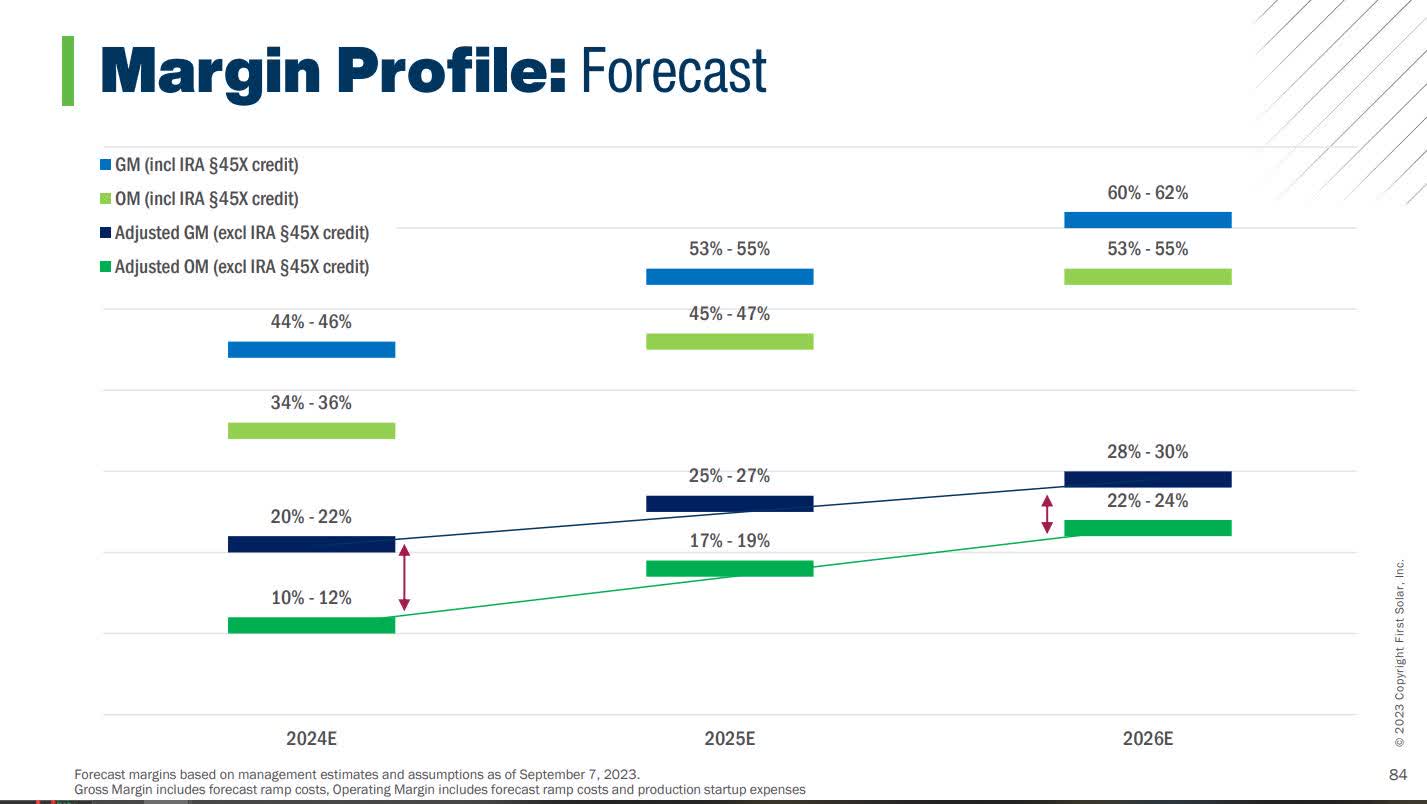

Growth is accretive. Suppose you believe the solar industry and First Solar are heading into good times; supercharged profit growth could be on the horizon. The chart below shows management's forecasts for improving gross and operating margins over the next several years. Note that the blue and green lines represent the margin forecast, including the IRA 45X MPTC impact.

First Solar 2023 Investor Presentation.

{kind=link}

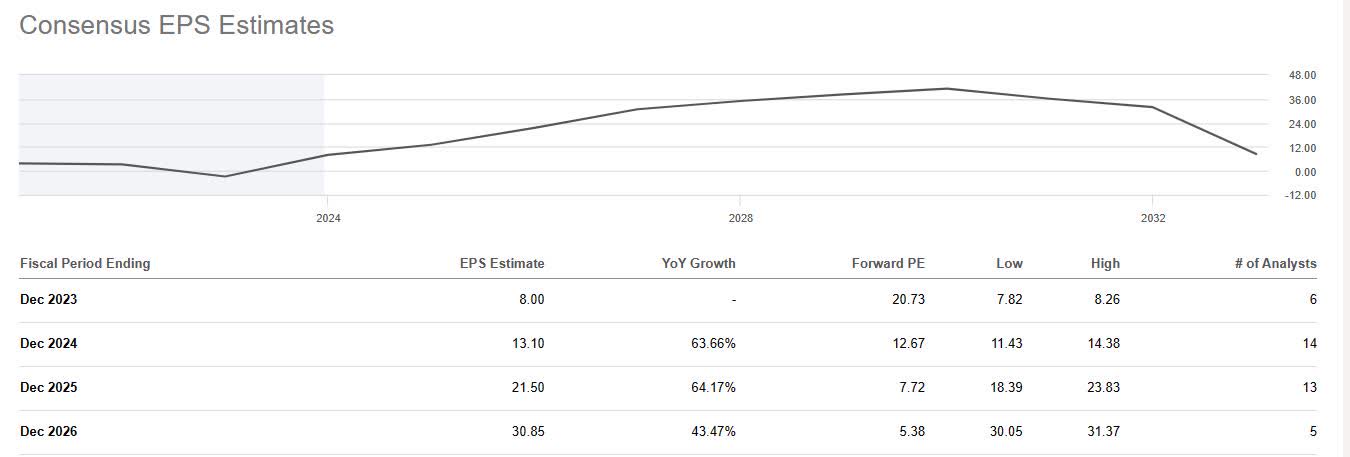

The above image speaks well for First Solar's potential future profitability. Improving margins and sales growth could significantly boost the company's EPS. The below image shows consensus analyst estimates until 2026. Notice how analysts forecast substantial EPS growth, 63.66%, 64.17%, and 43.47% in 2024, 2025, and 2026, respectively.

{kind=link}

Wall Street analysts seem to believe in the company's forecasts and expect rapid sales growth, improving margins, and rapid bottom-line growth. So, what are the things that can upset the apple cart?

Risks

Remember, operating leverage works both ways. While it can amplify profitability as sales rise, it can exacerbate losses as sales growth slows. If the economy worsens and First Solar's sales growth declines, the company's profitability could drop if management lacks strategies to mitigate the impact of a sales slowdown. Unexpected spikes in inflation that force the Federal Reserve's hands to start raising interest rates again would also likely cause problems for the company.

Competition in the solar industry is intense. According to IEA, China has 80% of the global solar module and component manufacturing market share. Some Chinese manufacturers can be cutthroat and sell modules for near or below what it costs to make them. Additionally, the Chinese government subsidizes some Chinese manufacturers, and critics of Chinese solar panel manufacturers accuse some companies of operating at exceptionally low or negative operating margins for sustained periods, potentially harming manufacturers outside China. Another risk First Solar faces in the industry's competitive dynamics is that if global solar module supply exceeds global demand, it could drop the average selling price, potentially harming the company's sales.

Last, its competitors are not sitting still. Other companies are innovating within the solar industry, and another company might create a better mousetrap. If First Solar's technological innovations fail to match or exceed the capabilities of its competition, it could face obsolescence risks. A few up-and-coming technologies investors should be looking for are Quantum dot solar modules, Perovskite solar modules, Tandem solar modules, Organic photovoltaics, and Concentrated photovoltaics.

Should you buy it?

First Solar stock's retreat since hitting its 52 -week high on May 12, 2023, has opened an opportunity for investors who thought they had missed the IRA-induced rally.

Barclays analyst Christine Cho first highlighted the market potentially undervaluing the stock on October 12, 2023. She said , " We think FSLR's contracted backlog, domestic content advantages, and current valuation offers an attractive entry point. " I think the stock remains undervalued by the market in December. Here's Why.

First Solar sells at a one-year forward price-to-earnings (P/E) ratio of 12.88, which I believe is too low for the earnings growth the company expects over the next several years. The chart below shows how investors historically valued the stock on a one-year forward P/E ratio since January 2022. While I believe a valuation above 20 is too high for the risk level of this company, the current valuation is a tad too low. In my opinion, a more appropriate valuation for the expected $13.10 earnings-per-share in fiscal 2024 ranges between 14 and 15, which equates to a stock price between $183.40 and $196.50. At the midpoint of $189.95, the stock price is 13% over the December 15 closing price of $168.67.

Clean energy investors looking to invest in one of the best-positioned companies in the solar industry should look at First Solar. It's one of the few solar companies worth owning through the ups and downs in the industry. I recommend interested investors' dollar cost average into the stock, buying a larger percentage if it goes down. I rate the stock a moderate buy.

For further details see:

First Solar: Poised For Growth In A Post-Inflation Environment