SPWR - First Solar: The Sustainable Energy Giant On Sustained Growth Path

2023-10-25 07:35:40 ET

Summary

- First Solar is the largest solar panel manufacturer in the western hemisphere, with plans to significantly increase its production capacity.

- The company's superior technology and execution drive efficiency and cost reduction, with a focus on thin film tandem technology.

- Growing demand for solar panels, along with government incentives, contribute to First Solar's profitability and potential for future growth.

Editor's note: Seeking Alpha is proud to welcome Stanley Nwosu as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Summary

First Solar (FSLR) is the premiere and largest solar panel manufacturer in the entire western hemisphere. The company's superior technology and execution increase efficiency and drive down costs. Its R&D in thin film tandem technology promises groundbreaking solar energy conversion yield. The company is growing capacity to meet growing demand, which in turns achieves economy of scale. The results of these show up in increasing margins, decreasing costs, increasing profitability and cashflows. The Inflation Reduction Act of 2022 is a welcome boost to growth and profitability. First Solar is undervalued. I rate it a strong buy. Technical analysis indicates when to buy.

The Company On A Growth Path

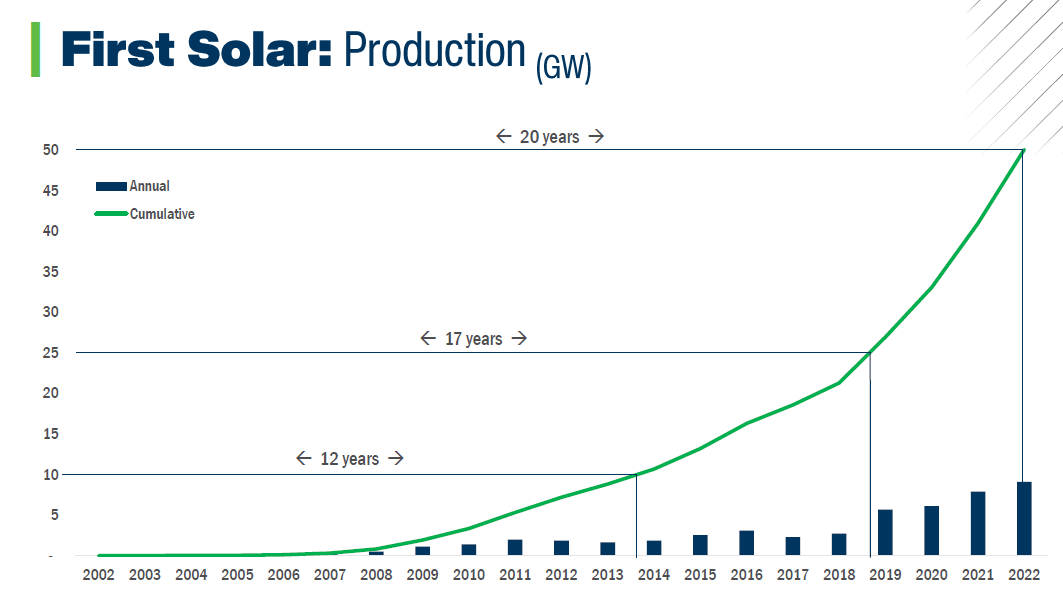

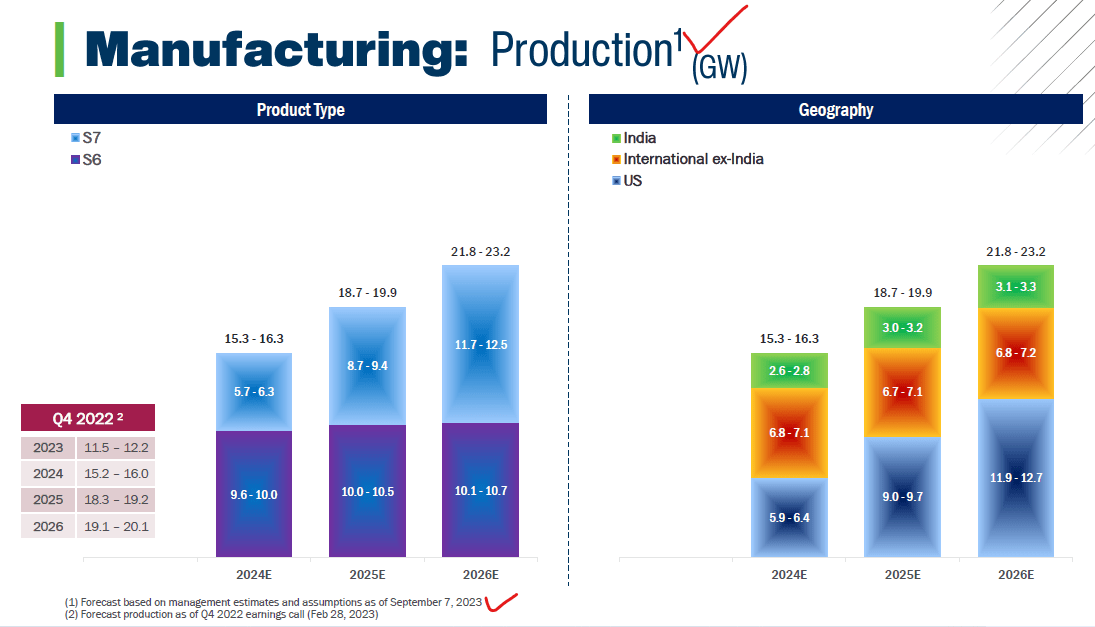

First Solar took the plunge into solar panel production back in 2002 with its first manufacturing plant in Perrysburg, Ohio. This was a time when people were not sure whether the solar industry would live or die. However, the company has continued to wax strong, increasing its manufacturing capacities, from a lowly nameplate capacity of 210 MW in 2007 to an expected nameplate capacity of 25 gigawatts by 2026. That would represent an 11,804.76% (1GW = 1000MW) increase in production capacity over that time span. Similarly, actual annual production of solar panels was at 21.5 MW per annum in 2005 and is now expected to reach 22.5 GW by 2026. To put this in context, the cumulative production of solar panels at First Solar, in the 20-year period from 2002 through 2022 was 50 gigawatts, but with this growth in manufacturing capacity and the attendant growth in productivity, it would only take the company less than 2.5 years to reach and surpass the same 50 gigawatts of production. That is an incredible growth story!

First Solar Cumulative Production, in GW, 2002 - 2022 (First Solar Investor Day Presentation 2023) Production Estimates, in GW, 2024 - 2026 (Production Estimates per FS Investor Day 2023 Presentation)

{kind=link}

{kind=link}

Superior Execution And Technology

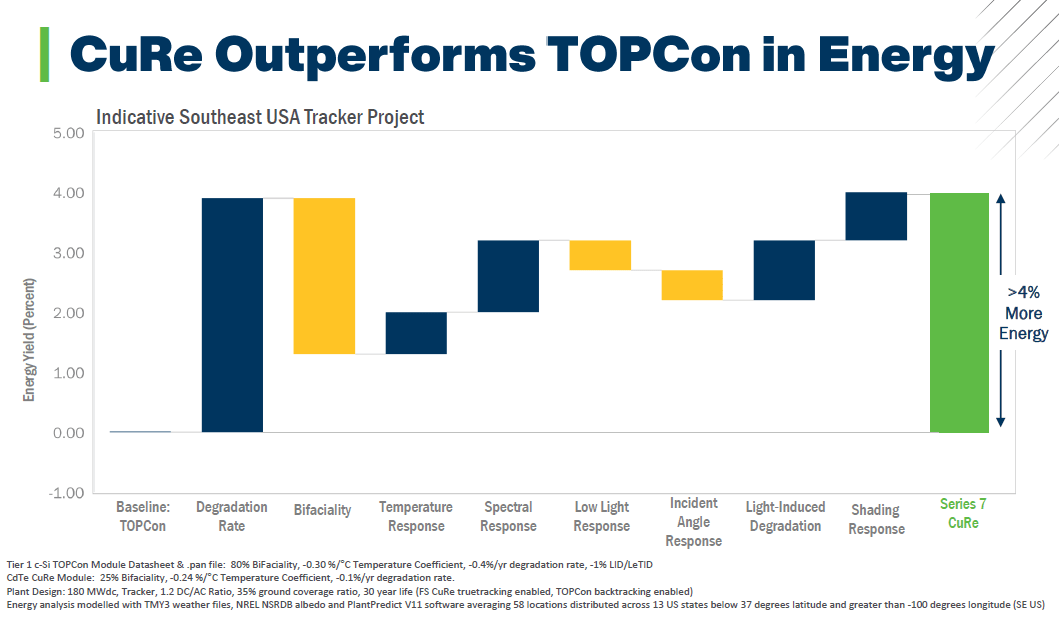

Another competitive advantage of First Solar is its superior execution and technology. First Solar takes pride in its investment in R&D. And these investments have continued to pay good 'dividend'. Just from 2018 till now, it has gone from the Series 6 modules to the Series 6-plus modules capable of generating up to 480 Watts of electricity, to the Series 7 modules capable of up to 550 Watts of electricity. This is further optimized, in the CdTe CuRe Module (expected to launch in 2024), for degradation rate, shading response, temperature response, air moisture spectral response, light-induced degradation, to yield >4% more energy giving the company >3.5X pricing power. Essentially, the solar panels of the company are optimized to produce electricity come rain, come shine.

Indication of the Optimization of the CuRe modules for Degradation Rate, Temperature Response, Spectral Response, Light Induced Degradation, and Shading Response and Increased Energy Yield (First Solar Investor Day Presentation 2023)

{kind=link}

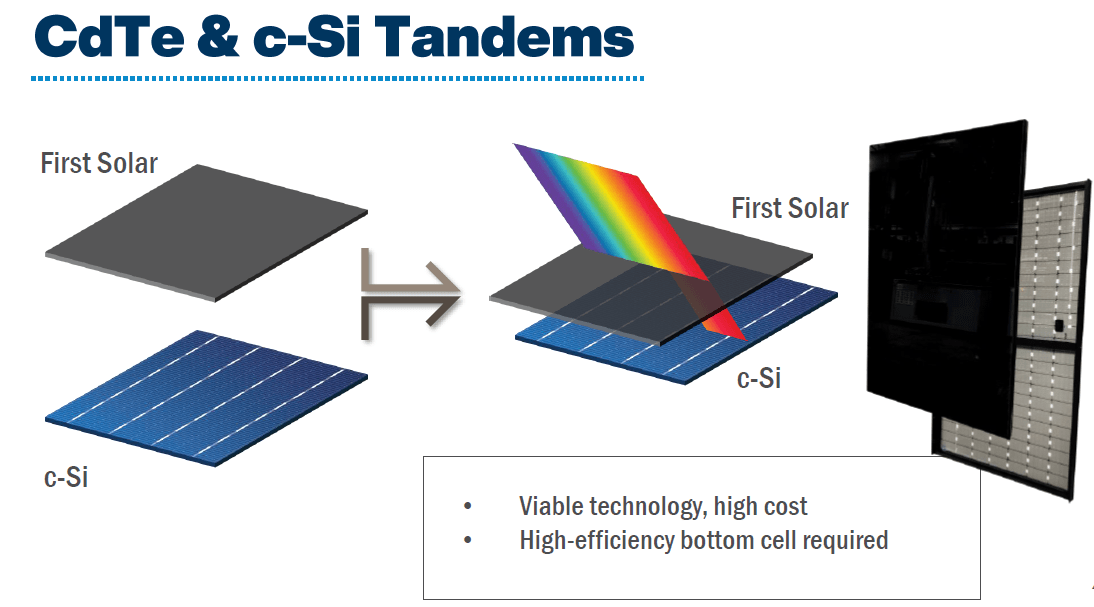

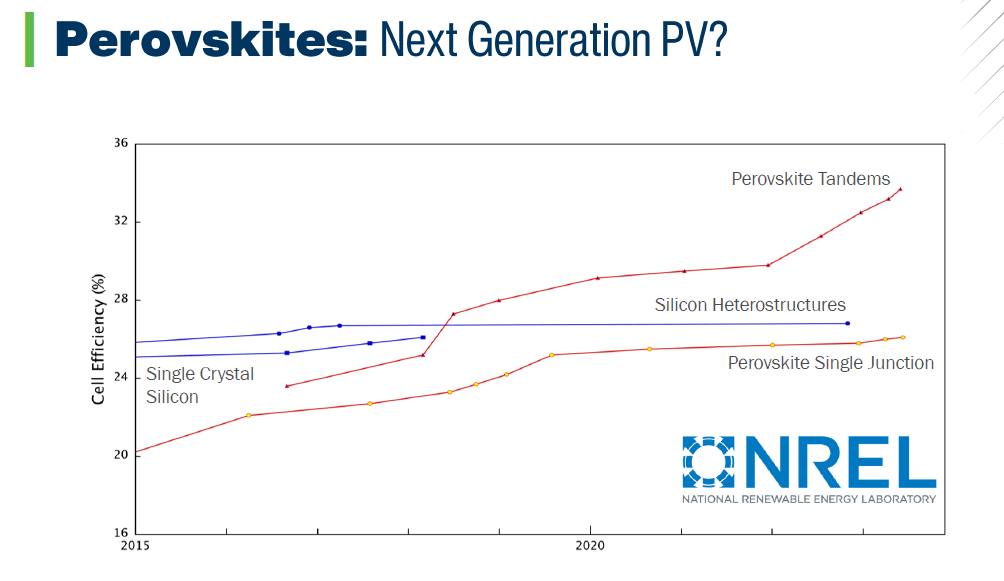

However, First Solar is not stopping here. The company is working on yet another game-changing technology - thin film CuRe bifacial CdTe modules. This would improve conversion efficiency, that is how much sunlight it converts to electricity compared to the amount of sunlight that it receives, from 15% to 25%. This technology was underpinned by the acquisition of Evolar, a European leader in perovskites and CIGS thin film technology. Based on this thin film technology, the company hopes to leapfrog to yet another groundbreaking Tandem technology, which combines the CdTe module and the c-Si module to raise conversion efficiency from 25% to a staggering 35% Higher Conversion Efficiency . This science behind this is that sunlight is first captured and converted to electric energy by the top module, and the portion of the sunlight that manages to escape conversion by the top module is captured and converted to electric energy by the bottom module. Once this 35% conversion efficiency threshold is reached, I believe that it would be final bye-bye to fossil fuels across the world. And with the company's increasing spend on research and development, it is sure to remain at the cutting edge of solar panel technology for a long time.

Thin Film - Tandem Technology (First Solar Investor Day Presentation 2023) Comparison of the Energy Conversion Efficiency of Perovskites Tandems Vs Others (First Solar Investor Day Presentation 2023)

{kind=link}

{kind=link}

In execution, First Solar employs vertical manufacturing process. This means that they would not be waiting on some third party, say, a company in China for example, to complete any part of their manufacturing process. This is also consistent with the de-risking of their logistics process, making them relatively immune to the vagaries of an unmitigated global supply chain. In summary, the superior technology and execution of First Solar make them the ExxonMobil equivalent of the solar energy industry. ExxonMobil occupied its premiere position in the oil and gas industry for a long time due to its superior technology and execution. Those are the same attributes that First Solar brings to the renewable energy industry.

Demand, Government Incentives, Financials And Sustainability

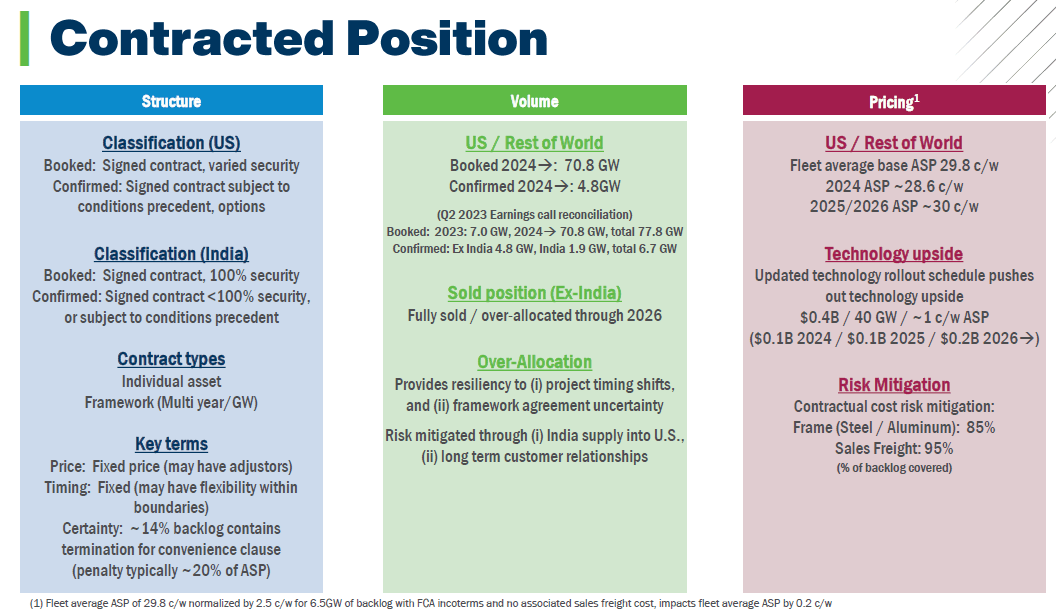

The growth in First Solar's production capacity has been in response to the growth in demand for its products - solar panels. From end of 2022 through July 27, 2023, booked volumes grew from 61.4 GW to 77.8 GW (backed by 100% security), 6.7 GW confirmed (backed by <100% security), and 16 GW in the process of being booked (pipeline) with 5.5GW of that already in mid-late stages of the booking process. Clearly, demand is growing by double digits. Another obvious but comforting characteristics of these booked contracts is that they are backed by financial securities. Every booked order is backed by solid 'collateral' analogous to the take-or-pay contracts that are rife in the fossil fuel industry. So, it is not just numbers on the book, these are actual money in the bank essentially. Of course, First Solar has to fulfil their own part of the contract as well, which is essentially why they are in business, anyway.

To make these contracts (booked orders) all the more impregnable, First Solar hedges the associated price risk by securing 85% of the frames of the modules of all booked contracts, and 95% of their freight costs. That way, the company is able to lock-in a large portion of their profits from these contracts, irrespective of any changes in their manufacturing and delivery costs.

Contracted Position (First Solar Investor Day Presentation 2023)

{kind=link}

It may be necessary to point out that First Solar had been a profitable company for over 20 years before the passage of the Inflation Reduction Act ((IRA)) of 2022. It is also no gainsaying that IRA has provided additional boosts both to its capacity expansion and to the growing demand for its products. For example, the IRA provides that US government could put up about 24% of the capital expenditure required for capacity expansion, which the company repays back to the government over a 6-year period. In addition, the government provides tax credit starting at 100% in 2023 and ending in 2032 at 25%. However, the IRA passed last year was not the basis for First Solar's success over 2 decades running now. What the IRA does is act as a catalyst that provides additional 'escape velocity' for the company's growth and profitability to move higher into the 'stratosphere', carrying her investors along for the ride.

What is interesting is that at the time the IRA would completely expire in 2032, the net zero emission targets of many countries and companies would be within sight - many by 2040 and some by 2050. I imagine that there would be a frenzy of orders flowing in to First Solar from these companies and countries in their scramble to meet their net zero emission targets. The implication is that First Solar would continue to grow in both production capacity and profitability as far as the eye can see.

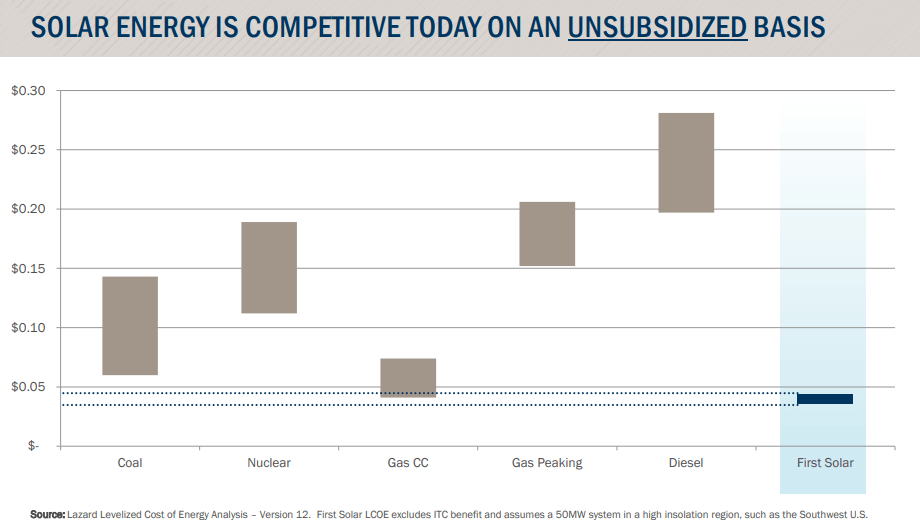

Additionally, in 2019, long before the IRA, First Solar was already determined to be competitive vs its fossil fuel and nuclear competition:

Lazard Levelized Cost of Energy Analysis - Version 12 (First Solar 2019 Earnings Report)

{kind=link}

Furthermore, the self-sustainability of First Solar's business is evident in their financial data. For example, the company's cash balance at the end of 2nd quarter, 2023 was $1.899 billion. This compared to existing debt of $435 million in the same period, resulting in a cash-to-debt ratio of >4.36:1. To put this in context, all the other so-called competitors to First Solar, including Canadian Solar (CSIQ), SunPower Corporation (SPWR), and Sunrun Inc. (RUN), have cash-to-debt ratios <1.0. In fact, the one common thread that runs through them is the high level of debt that they are laboring under. They are all heavily indebted. And the current higher for longer interest rate environment has further compounded their woes. This is reflected in their downbeat business forecasts. To a large extent, First Solar is insulated from the whims of the prevailing interest rate regime. This is because, the company's customers are mainly utilities, many of which have credible credit standing, and whose projects are likely backed by take-or-pay power purchase agreements. I have compiled the cash-to-debt ratios in the table below for comparison:

| Company Name/Ticker Symbol |

| Cash + Marketable Securities () |

| Debt () |

| Cash to Debt Ratio |

| First Solar Inc./FSLR |

| 1,899 |

| 437 |

| 4.35 |

| Canadian Solar Inc./CSIQ |

| 2,011 |

| 3,300 |

| 0.61 |

| Sunrun, Inc./RUN |

| 364 |

| 9,604 |

| 0.04 |

| SunPower Corporation/SPWR |

| 131.274 |

| 347.994 |

| 0.38 |

From the table above, based on cash-to-debt ratio alone, it is easy to see that First Solar is in a class of its own as far as financial strength is concerned vis-a-vis the others who may be tethering on the verge of financial distress. On this score alone, First Solar is, far and away, the more financially stable company. In addition, the company has a 5-year credit facility of $1.0 billion, currently undrawn. This credit facility is like an extra ammo that the company does not need but is happy to have, all the same, for good measure. So, there is no risk of financial distress at First Solar. The company is clearly able to meet its debt obligations with the substantial cash pile at its disposal.

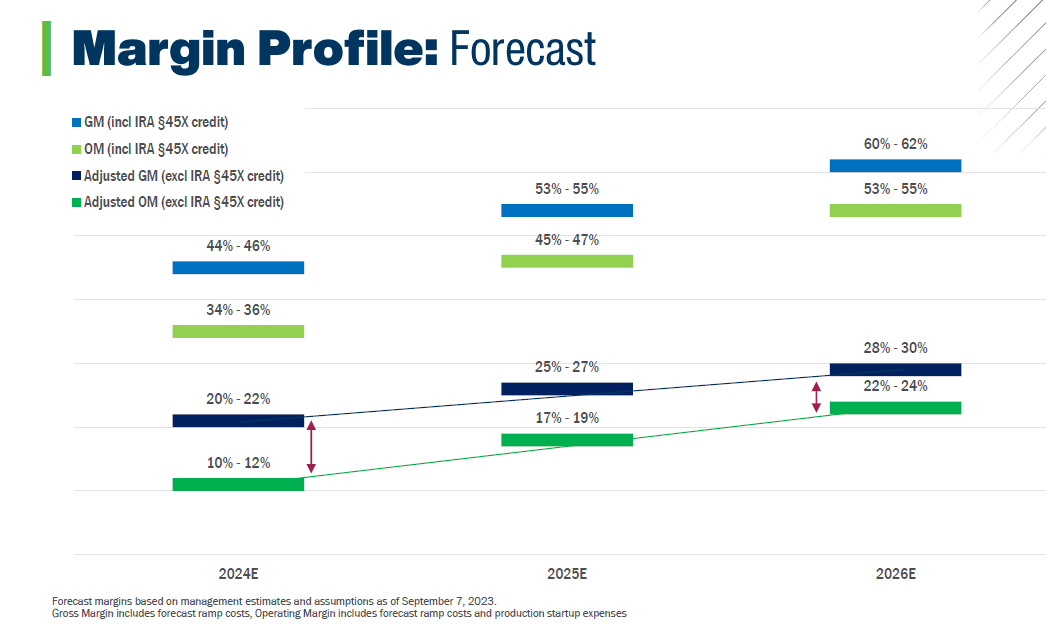

In the same vein, First Solar boasts of double digits positive gross margin, and double digits positive operating margin even after you subtract the effects of the IRA (government incentives). These positive margins are expected to keep expanding in the coming years.

Margin Profile: Forecast, 2024 - 2026 (First Solar Investor Day Presentation 2023)

{kind=link}

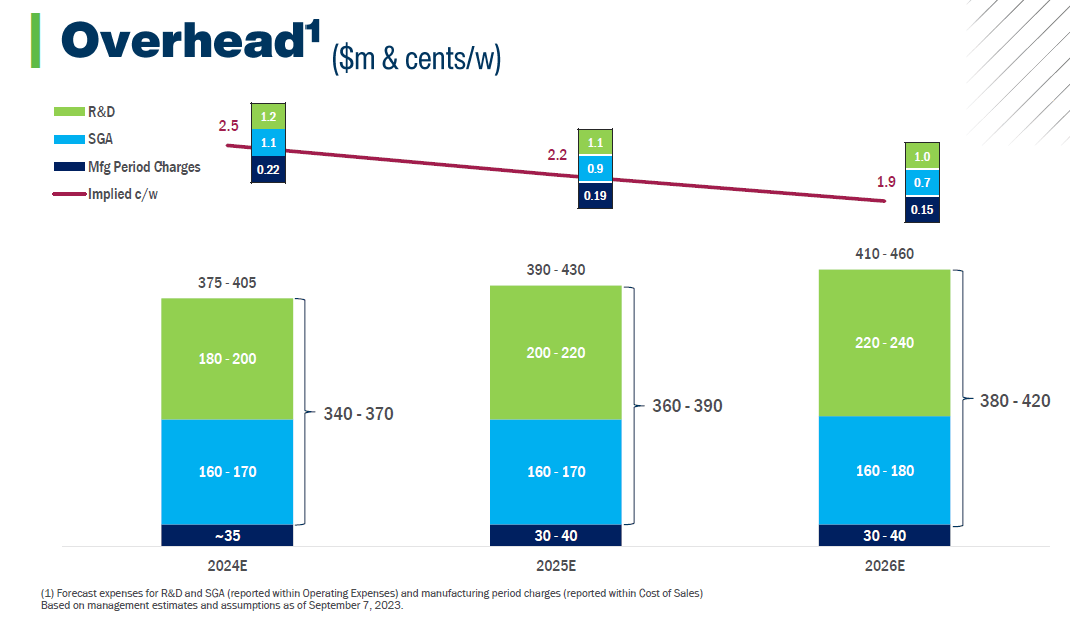

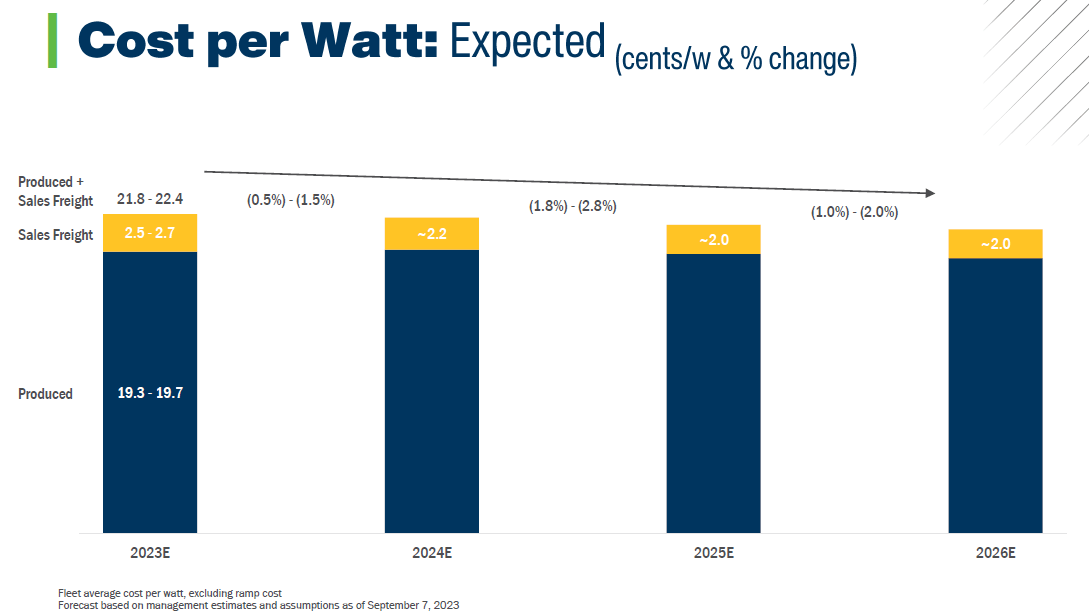

Investors would be even more delighted to discover that at the same time that margins are expected to expand, the costs of producing 1 watt of electricity are also expected to fall at First Solar.

Forecast of Overhead Costs, 2024 - 2026 (First Solar Investor Day Presentation 2023)

{kind=link}

Expected Cost per Watt, 2023 - 2026 (First Solar Investor Day Presentation 2023 )

{kind=link}

This is further testament to the company's execution and economy of scale. Decreasing costs and increasing margins, that is the holy grail of profitability and sustainability.

Valuation

There are many ways to value a company, including the intrinsic value method, adjusted net present value method, EBITDA multiple method, etc. But extensive valuation is without the scope of this article. However, for the purposes of our discussion, here, if we look at the forward P/E multiple for First Solar, we see that currently, that ratio stands at [$150.77/7.82] = 19.28. So, if we hold this multiple constant and assume that the earnings per share would grow at 19.37% per year, just approximately in line with the expected average production growth rate , then, the company would be earning about $18.95/per share in about 5 years' time. A 19.28 earnings multiple would take the price of the stock to about $365.42 per share. In 10 years' time, that price would be $885.66/share of First Solar, all things being equal. That makes the price today ($150.77/share) look cheap to me.

First Solar does not have any comparison, in the true sense of it. There is no other publicly traded, pure play solar panel manufacturer that I found in the US. The other companies, like Canadian Solar, that came anywhere close, have other lines of businesses like power storage, project development, etc., that I consider side distractions that make comparison with First Solar difficult. Still, other companies like Sunrun Inc., and SunPower Corporation are primarily into the residential side of the solar business, and worse still, have negative forward EPS values SPWR Forward EPS , Sunrun Forward EPS so their comparison with First Solar is not quite apple-to-apple.

However, for the sake of our discussion, if we compared these companies based on forward P/E multiples alone, against expected growth rate, the picture leaves no one in doubt as which company is the best bet. In estimating the growth rate for Canadian Solar, I used the growth, YoY, in net revenues in the 2Q2023 vs 2Q2022. I thought that this value was more representative of the state of things at Canadian Solar. For context, whereas CSI business line revenues grew 11% YoY in the same period, recurrent energy business line revenues declined by -35% CSIQ Growth Basis accordingly. Relatedly, Sunrun and SunPower are both expected to post negative forward PEs, so their forward PE ratios could not be calculated.

| Company Name/Ticker Symbol |

| Forward EPS |

| Forward P/E Ratio |

| Expected Growth Rate |

| Forward EPS in 5 years |

| First Solar Inc./FSLR |

| $ 7.82 |

| 19.28 |

| 19.37% |

| $ 18.95 |

| Canadian Solar Inc./CSIQ |

| $ 5.23 |

| 3.95 |

| 2.00% |

| $ 5.77 |

| Sunrun, Inc./RUN |

| $ (1.13) |

| N/A |

| 15.00% |

| N/A |

| SunPower Corporation/SPWR |

| $ (0.14) |

| N/A |

| 15.00% |

| N/A |

| Company Name/Ticker Symbol |

| Stock Price in 5 Years |

| Stock Price in 10 Years |

| Return on Investment in 5 Years |

| Return on Investment in 10 Years |

| First Solar Inc./FSLR |

| $ 365.42 |

| $ 885.66 |

| 142.37% |

| 487.42% |

| Canadian Solar Inc./CSIQ |

| $ 22.83 |

| $ 25.21 |

| 10.41% |

| 21.90% |

| Sunrun, Inc./RUN |

| N/A |

| N/A |

| N/A |

| N/A |

| SunPower Corporation/SPWR |

| N/A |

| N/A |

| N/A |

| N/A |

The expected returns in 5 years and 10 years in the table above, everything being equal, speak for themselves. Very few investments boast of such potential returns.

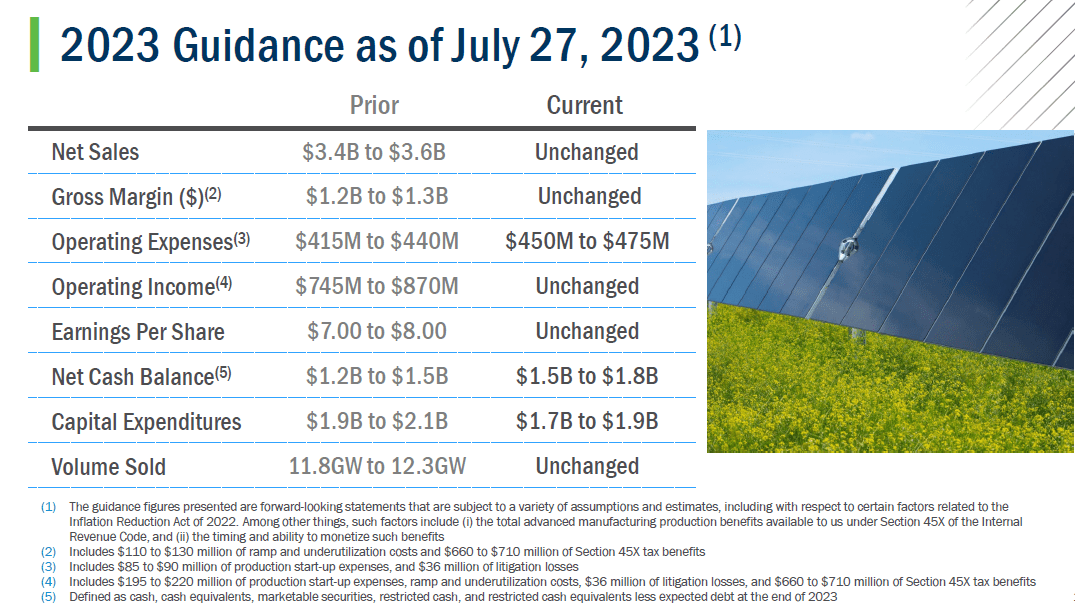

2023 Guidance as of July 27, 2023 (First Solar Investor Day Presentation 2023)

{kind=link}

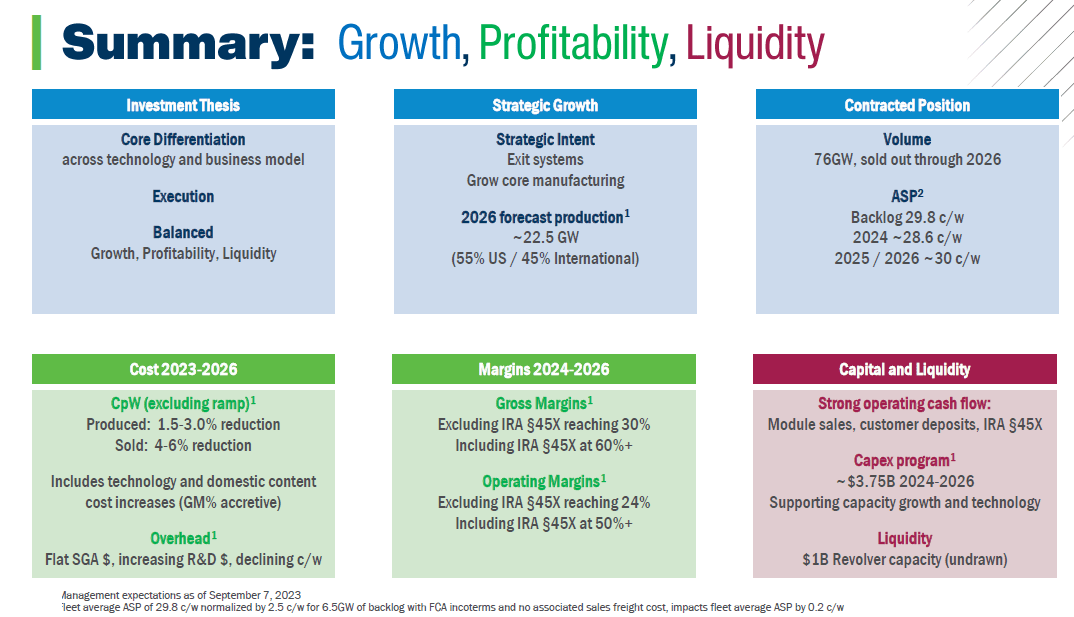

Summary of Growth, Profitability, Liquidity (First Solar Investor Day Presentation 2023)

{kind=link}

Risks

Just as in all investments, there are risks in investing in First Solar as well. The first to consider, in my opinion, is technology fail. If their expected technological improvements fail, or if some other company comes up with superior technology that guarantees higher solar energy conversion rate at a cheaper price, then, all bets are off. Another challenge would be if they are not able to continue to grow the size of their addressable markets, then, the company's growth would stall, and with that, its valuation as well. But so long as they can keep their eyes on the ball as far as R&D is concerned, to keep pushing the boundaries of solar technology; and so long as they can keep making inroads into the other markets in Asia, Europe, and Africa, then, the company's future would remain on solid footing.

Conclusion

From the foregoing analysis, First Solar is the biggest solar panel producer in the entire western hemisphere. It is also clear that the company is experiencing a growth spurt, and that this growth is expected to continue as far as the 'eye' can see. The company is profitable on its own to begin with, and this profitability has been boosted by the Inflation Reduction Act of 2022. First Solar is also committed to research and development which keeps it on the cutting edge of solar panel technology, making it a manufacturer of choice to its customers. It has de-risked its supply chain and manufacturing process making them more reliable. The company has a good risk management process to hedge its price risks per booked contracts to ensure that inflation does not 'eat' too deep into its profits. Forward PE ratio and expected growth rate make the company's stocks look cheap at today's prices. An investor with a 5 - 10-year time horizon could profit handsomely as the stock prices move higher.

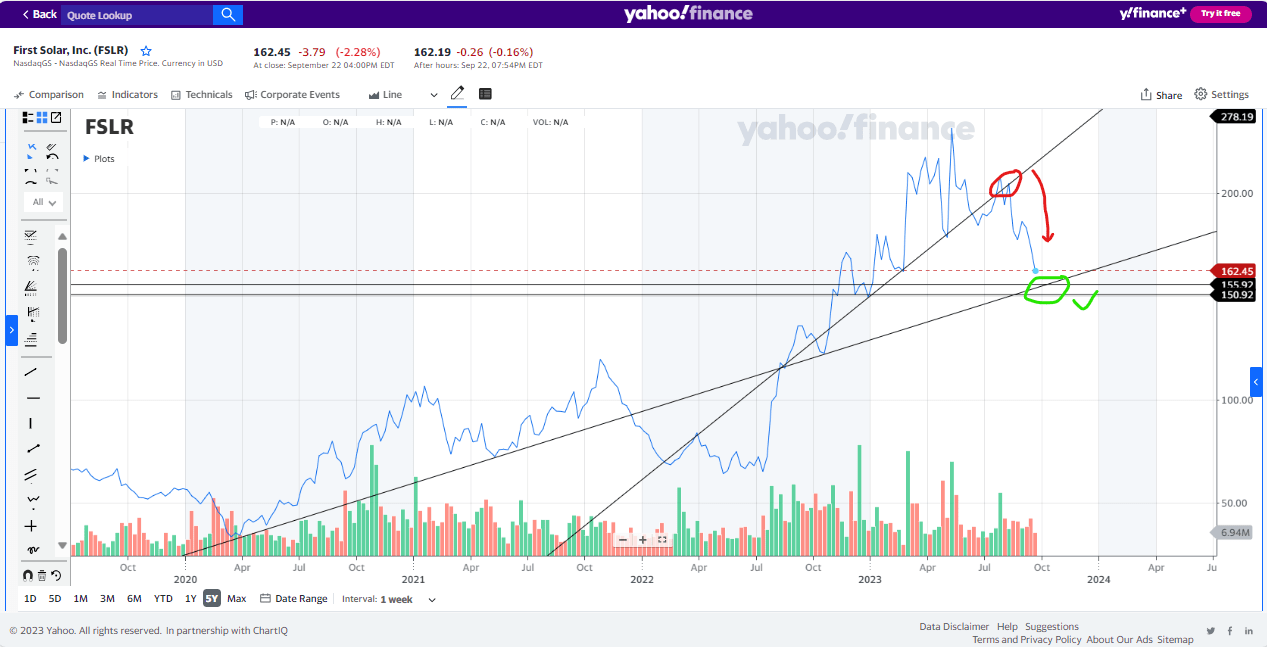

A look at the stock price chart shows that the stock has broken an upward trend. I would wait to buy at the next strong support around $156 and $150:

Chart of Technical Analysis of First Solar Stock Prices (Yahoo Finance)

{kind=link}

For further details see:

First Solar: The Sustainable Energy Giant On Sustained Growth Path