FISV - Fiserv: Attractive Defensive Growth Play

2023-03-13 08:11:06 ET

Summary

- I prefer FISV over other large-scale payment processor peers, particularly due to its strong growth potential in Clover.

- I believe that the company's guidance, which factors in a mild recession, presents an opportunity for FISV to surpass current Street estimates if consumer spending trends remain robust.

- My price target suggests a 19% upside from its current level.

Thesis

Fiserv ( FISV ) is an attractive defensive growth opportunity with reliable double-digit EPS growth, even in the face of challenges presented by macro headwinds. The company is targeting 11.5% revenue CAGR to 2025 for Merchant which implies growth beyond payments. I prefer FISV over other large-scale payment processor peers, particularly due to its strong growth potential in Clover. My price target for FISV for December 2023 is $133, which applies a 16x multiple to the company’s estimated CY24E EPS of $8.34.

Q4-2022 Earnings: Encouraging FY23 Outlook

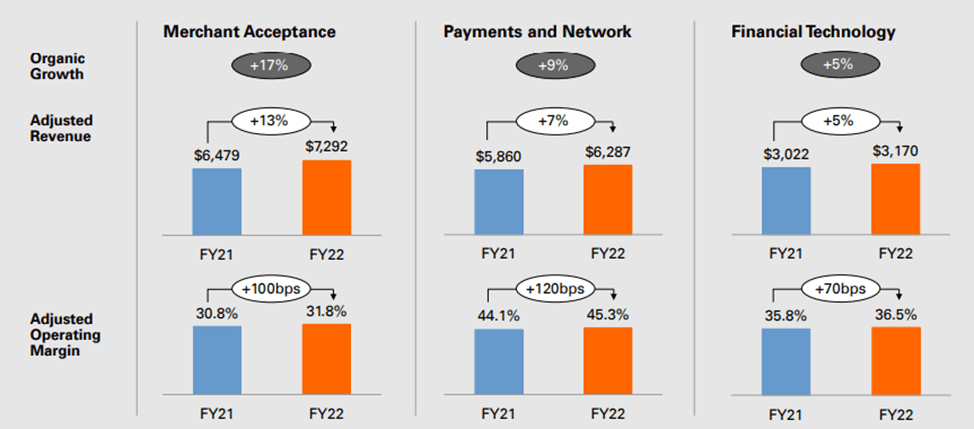

Fiserv's recent result was largely in-line, but the company's growth outlook is very promising. This suggests that the management is executing well, and the company is yielding better results with new wins such as Target (TGT). Even if there is a mild recession, Fiserv aims to grow in line with its mid-term target of 7-9% in FY23. The company is also expected to achieve above-average growth in the Merchant sector, which implies no share loss due to the momentum of its Clover product. Fiserv is cutting costs to expand margins, resulting in double-digit EPS growth. However, the company is investing more capital, and the FCF growth of around 8% is lower than expected due to the shift toward digital growth.

Expects Continued Growth in Merchant Segment

Fiserv's growth outlook indicates that the company is confident in achieving merchant revenue growth that is consistent with the global carded volume growth. To achieve this, Fiserv plans to increase the lifetime value and average revenue per user, as well as reduce churn. This will be achieved by transforming from offering point solutions to operating systems that are centered around Clover and Carat. While this strategy is promising, it will require sharp execution to succeed. If Fiserv can consistently achieve double-digit growth in merchant revenue, there is potential for multiple expansion.

Fiserv's growth strategy is two-fold: firstly, the company plans to expand its merchant base through global distribution channels, including a greater emphasis on direct selling. Secondly, it aims to broaden relationships with merchants by offering software and services beyond just payment processing. This approach aligns with the trend of software becoming more prevalent in the payments industry and the expansion of services offered by payment providers.

The SMB sector represents 69% of Fiserv's revenue, with 30% of that revenue coming from the Clover product line. Fiserv expects Clover to continue experiencing high revenue growth, in the high-twenties. Currently, the majority of the segment's revenue, 72%, comes from payment processing, while 12% comes from software and services and 16% from hardware. Fiserv plans to focus on expanding ARPU by selling more software and services and expanding its direct channel. Fiserv has disclosed that the lifetime value for a Clover restaurant client is 50% higher than for a non-Clover client, with the potential to be three times higher than non-Clover clients.

Clover’s revenue and GPV are larger than rivals Lightspeed and Toast combined. International is an advantage for Clover, representing high-single digit of segment revenue today, with expansion potential from bank deals like ICICI in India, DB in Germany, Caixa in Brazil and NAB in Australia.

{kind=link}

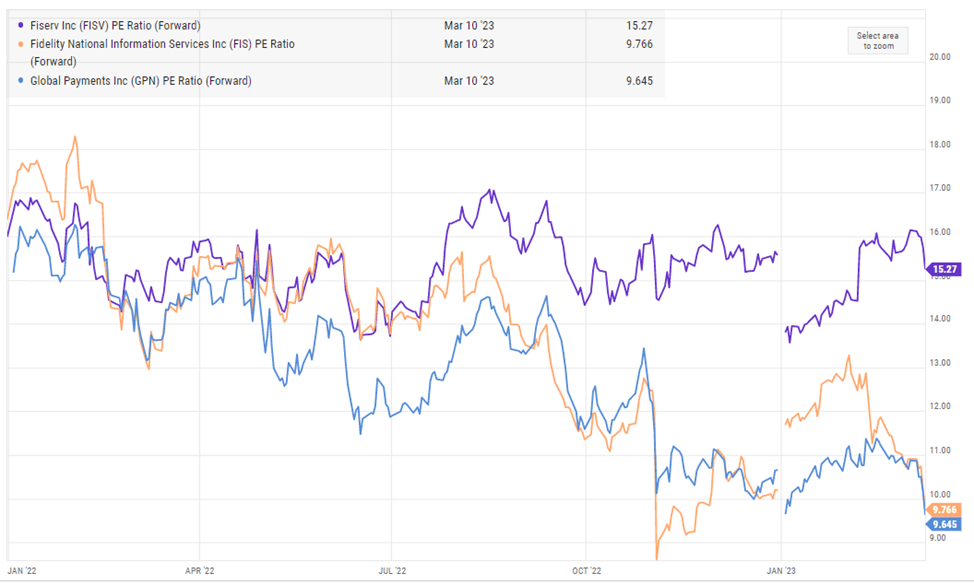

Core Processors Valuations at Steepest Discount to History

Most fintech stocks are trading below their historical average forward price-to-earnings (P/E) ratios over five or even 10 years. However, the three leading payment processors - Fiserv, FIS, and Global Payments - are trading at even deeper discounts, with forward P/E multiples nearly two or more standard deviations below their five-year valuations. This is despite significant growth in revenue run rate after their large-scale acquisitions in 2019. The selloff, potentially driven by concerns around rising competitive threats from fintechs Adyen and Stripe, as well as credit-card alternatives such as bank account-to-account payments -- appears overdone to me, at least in the near term.

{kind=link}

Valuation

My price target for FISV for December 2023 is $133, which applies a 16x multiple to the company’s estimated CY24E EPS of $8.34. Currently, FISV is trading at a higher NTM EPS multiple than its peers (15x vs. 10x). However, I prefer FISV over other large-scale payment processor peers, particularly due to its strong growth potential in Clover, which gives it the highest multiple. Over the last year, FISV has traded at a 4-turn premium compared to its peers on NTM P/E. My price target suggests a 19% upside from its current level.

Final Thoughts

FISV's Q4 results and FY23 guidance have reassured investors who may have had concerns about the company's ability to provide reliable guidance during a volatile period. I believe that the company's guidance, which factors in a mild recession, presents an opportunity for FISV to surpass current Street estimates if consumer spending trends remain robust. Additionally, FISV has demonstrated effective capital allocation, resulting in consistent revenue growth. Finally, FISV's is trading at a discount to its historical multiple which is low in my view, given its healthy, resilient, and sustainable organic growth profile, with high single-digit growth expected despite the recession and low-teens EPS growth. I keep a Buy rating on FISV stock with an end-of-year price target of $133, based on 16x multiple applied to the company’s estimated CY24E EPS of $8.34.

For further details see:

Fiserv: Attractive Defensive Growth Play