FISV - Fiserv: Deep Value Through Dominance In Payments

2023-03-28 03:23:34 ET

Summary

- Strong free cash flow flanked by significant debt reduction. High capex growth without impacts to free cash in FY22, allowing for revenue expansion on every front.

- Growing outside of the standard merchant services, targeting Fintech penetration with bolt-on technology services for banking customers.

- Growing contract wins in the public sector, including California DMV, California Unemployment, and California Tax Office.

- Increasing adoption of digital services like Zelle across all segments of the population, launching a digital wallet and debit card to compete in the Gen Z and Millennial markets.

Investment Thesis

Fiserv ( FISV ) is a financial technology firm specializing in payment processing. Through aggressive M&A, Fiserv hopes to establish a competitive advantage through advanced platform features. Fiserv has consistently outperformed its own estimates and has successfully leveraged several M&A actions in FY22 to gain a foothold globally. These merger actions have already realized $700 million in additional revenue due to acquisitions, 2 years ahead of schedule.

Fiserv is trading near its 52-week high at the time of writing, but we still believe there is a value proposition. FISV has large amounts of free cash generation capability, with free cash growing at a CAGR of 61% over the last 3 years allowing it to deploy capital easily. Additionally, customer growth has been consistent in every sector and expects stable high single-digit EPS and revenue growth for FY23.

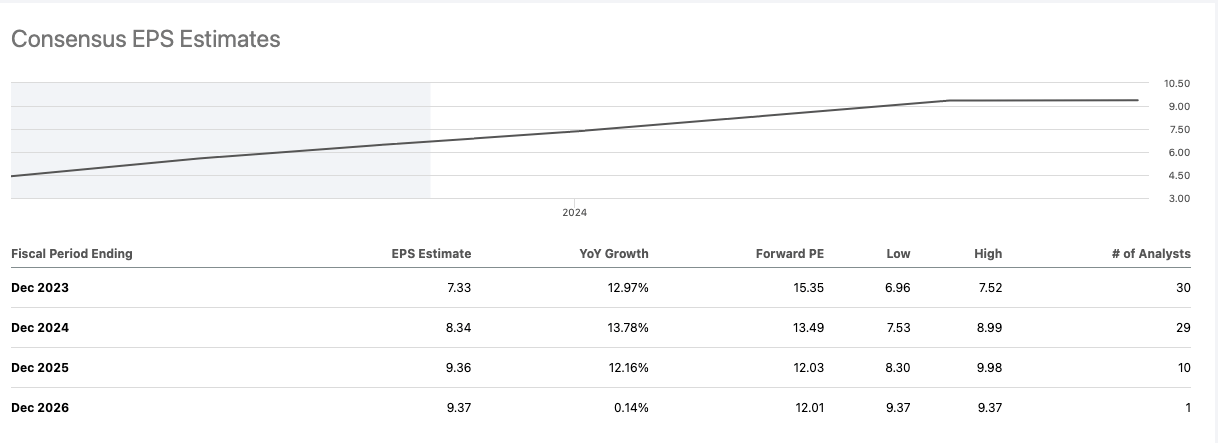

Estimated Fair Value

EFV (Estimated Fair Value) = E24 EPS (Earnings Per Share) times PE (Price/EPS)

EFV = E24 EPS X P/E = $8.30 X 18.4 = $152.72

Due to its strong core foundation, desire to expand into new segments, and significant margin expansion, we believe there is still significant value in Fiserv. It has continually expanded its addressable market in every segment and has adapted well to SMB megatrends.

| Fiserv |

| E2023 |

| E2024 |

| E2025 |

| Price-to-Sales |

| 3.9 |

| 3.6 |

| 3.4 |

| Price-to-Earnings |

| 15.2 |

| 13.4 |

| 11.9 |

Addressable Market

COVID-19 greatly accelerated the adoption of touchless payment methods, with 58% of consumers preferring touchless . Digitized touchless point-of-sale systems have become ubiquitous, but the total addressable market is only valued at $25.2 billion . By 2029, this is expected to grow to $70.8 billion. SMBs (small and medium-sized businesses) are expected to increase their IT spend by 6.1% CAGR . The requirement for POS devices to have all of these features has driven significant competition in the market. In particular, SMBs desire POS options that handle most business operations related to inventory to minimize the capital requirement.

An additional novel payment method is digital wallets. Operating like a secondary bank account, users can easily store money in accounts and send money. This is most dominant within under 40 consumer markets, with 50% reporting using a digital wallet in the last 30 days.

Point of Sale Services and Customer Payments

The acceptance segment contains B2B POS (point-of-sale) devices, sales and retention services, and inventory management. Clover is the flagship POS system targeted at SMBs (small and medium-sized businesses), with Carat as the enterprise version. Through its wide variety of features including customer relations management and inventory management, it has become a leader in omnichannel solutions for SMBs growing the customer base by 9%. International penetration remains low compared to other segments given the complexity of each individual market. Fiserv entered a JV with Deutsche Bank to provide Clover services under a joint company called Vert.

Clover has significant revenue opportunity, charging 2.3% on processing fees . ARPU (average revenue per user) increased 13% year over year, well on target for the FY25 goal of $3.5 billion in revenue. Clover has seen 23% revenue growth in 4Q22 year over year, demonstrating sustained strength.

Carat is a far more mature business segment, providing the standard network capabilities like gift cards and ACH for large-scale businesses. In 4Q22 Fiserv saw 17% growth in the active credit card account area. Because of this, Carat's revenue grew 18% year over year.

Fiserv has lofty goals for the point of sale and payments segment, projecting it to grow at an 11.5% CAGR in revenue until it breaches $10 billion in revenue in 2025 . It has grown at 17% organic growth in FY22, with Clover reaching $230 billion in annualized GPV (gross payment volume).

Fintech Services

is a global provider of professional services related to financial technology. Fiserv operates a clearing network and account processing for depository customers and FP&A tools for those depository customers. The segment's core is made up of the acquisition of Finxact in early FY22. Still considered developing by Fiserv, the competitive advantage they are hoping to establish is to give developers access to tools that enable hyper-personalized financial planning and access to Real Time Payments.

The financial technology segment has had exceptional contract wins in FY22, with 10 new core customers defined as clients with over $1 billion in assets. We expect this to expand in FY23, as Fiserv has partnered with Banking as a Service provider, Central Payments , to provide additional technologies to banking customers.

While revenue for the segment has only grown at 8% organically, the operating margin has expanded by 400bps.

Network

Fiserv had a major win in 4Q22: Target and Desjardins, and The State of California. Target is one of the largest retailers in the world, and Desjardins is Canada's largest credit union consortium and the countries 4th largest card issuer. This will be the first market breach into Canada for Fiserv.

Fiserv has an existing relationship with California over being the processor for the Middle-Class Tax Refund Program and the state DMV using the previously discussed Clover platform. This relationship was expanded to include several California unemployment insurance program components. This expands on the $2.8 trillion in public sector money processed through the segment cumulatively .

Zelle is the flagship e-payment product of Fiserv. P2P payments are an increasing part of consumer preference, especially with under 40 consumers. There are still significant awareness gaps . A 2021 survey conducted by Fiserv found that 79% of consumers have used P2P payments in the last year, only 33% of P2P users have used their financial institution to conduct the transaction. Zelle has seen explosive growth in users, with a 37% increase in clients and a 27% increase in transaction volume in 4Q22 alone. While Fiserv has not published updated statistics for FY22, it processed $429 billion in payments in FY21. Fiserv intends to launch a debit card system similar to that of Venmo or PayPal, allowing users to make payments in person using their Zelle wallet.

Payments and network saw 9% organic growth for the year. Most impressively, operating margins have expanded 230 basis points over the year.

Guidance and Full Year

FY22 had a total of $2.5 billion returned to shareholders and $1 billion deployed toward M&A. Companywide operating margin expanded 360bps over the course of the year, averaging 89% free cash flow conversion. Debt to EBITDA was reduced to 2.8x despite the large amount of deployed M&A.

Traditionally, we would be worried about the debt level when a company deploys M&A so frequently. However, Fiserv's efficient free cash conversion allows for expansive debt repayment, it has gone below its 3.0x target, and only 19% of its debt is variable to interest rates.

Fiserv's capital expenditures have increased 24% year over year, hitting $1.5 billion. Share repurchases for the year are flat year over year, but the share repurchase agreement has been renewed to the tune of 75 million additional shares or an additional $8 billion.

For FY23 Fiserv projects 7-9% organic EPS growth, with a further 125 bps of expansion in operating margin. This will translate to $3.8 billion in free cash flow or 8% growth year over year.

{kind=link}

Risk

Fiserv expects a mild consumer recession in FY23 but does not expect it to meaningfully impact operations on a full year basis.

Fiserv has deployed capital extensively to gain market share, but competition is fierce. Because of their free cash generation and previous success integrating acquisitions quickly and efficiently, we believe that this risk is minimal and acceptable.

Consumer credit card balances are near all-time highs, and Fiserv is one of the largest issuers of cards in the world. While this nominally is only architecture provision, excessive consumer delinquency would considerably impact the number of cards issued and the volume of revenue from enterprise clients.

Final Thoughts

Processing 80 billion transactions a year is no easy feat, and with touchless payments and digital wallets increasingly becoming the norm Fiserv still has room to grow. t has continually expanded its addressable market in every segment and has adapted well to SMB megatrends. Fiserv has grown its revenue significantly over the previous five years and has not been afraid to expand to new markets like fintech. Our main concern lies with the debt level, but so far Fiserv has grown its free cash flow in tandem with the debt level, and the debt has gone toward revenue-increasing capex.

For further details see:

Fiserv: Deep Value Through Dominance In Payments